Hello Guest User, You are visiting this website from a computer with an IP address of 172.70.178.103 with the name of '?' since Tue Apr 23, 2024 at 1:16:45 PM PT for approx. 0 minutes now.

Kaiser Media Watch Blog - October 1, 2022 to October 31, 2022

KRO Blog Overview

The KRO Blog is where unrestricted content of a time sensitive nature is posted. It includes the Kaiser Media Watch Blog which features content involving John Kaiser produced by third parties such as the Discovery Watch series by HoweStreet.com, interviews by outfits such as Investing News Network, SDLRC related commentary, the KRO Monthly Summaries, and just about anything else John writes that is not intended exclusively for the fee based KRO Membership.

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch October 28, 2022: Slump Reversals & Premium Financings?

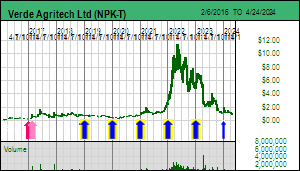

Jim (0:00:00): Verde Agritech has recovered from its slump. Is the alternative potash story back on track?

Verde Agritech has reversed the slump created on September 9 when it announced that, just when Plant 2 had been commissioned to produce K Forte at a nameplate capacity of 1.2 million tpa shipments with only a month of the primary March through September application window left, production had to be suspended for 4-8 weeks because the access road had developed groundwater problems. At the same time NPK reverted to its January guidance for 2022 which projected 700,000 tonnes of production for 2022 representing CAD $87 million in revenues and $31 million in EBITDA cash flow. The company had expanded its guidance in May to 1,000,000 tonnes production with $109 million revenue and $49 million EBITDA cash flow. The caution in January was based on uncertainty that Plant 2 would be operational in time to produce K Forte during the primary application window. Given that the rainy season doesn't begin until November, the market was unhappy that NPK was blindsided by access road problems in early September. On October 19 NPK announced that 22 km of road had been upgraded with asphalt laid on 14 km and a new bridge built so that commercial scale shipments could resume. A week later on October 26 NPK announced that phase 1 nameplate capacity had been achieved at Plant 2 but that shipments had to be postponed because the company was "sold out".

What that really meant was that NPK had shipped what it could from Plant 1's 600,000 tpa capacity but was unable to fulfill orders that counted on Plant 2 production. November through February is a slow period, and because NPK has not built warehousing capacity, Plant 2 is only operating at a level to meet the less conventional demand during this window. What this means is that while one thinks of a mine operating 24/7 all year, which would suggest a grinding capacity of 200,000 tonnes per month, Plant 2 actually has a physical capacity of grinding close to 400,000 tonnes per month. Farmers do not store fertilizer; they expect delivery just in time for application to their fields ahead of planting. However, this is consistent with the reverted guidance so not fresh negative information. In fact, the lull will allow NPK to complete the phase 2 installation and commissioning which will bring Plant 2 capacity to 2.4 million tpa output for the 2023 season for which NPK is still guiding 2 million tonnes of sales. The real question facing the market is if this expanded supply capacity will be matched with Q1 2023 demand.

The seasonal production lull is allowing NPK to repurpose Plant 1 to provide the specialty versions of K Forte like supplementing K Forte with nutrients such as sulphur as well as N Keeper which reduces nitrogen loss in the fields. Plant 2's larger footprint is also allowing NPK to develop its supply of Bio Revolution which loads K Forte with microbes chosen to rehabilitate depleted soils. The company also dropped the name of Cambridge Technology which prompts one to wonder if NPK is experimenting with the Cambridge Process developed with the help of Derek Fray during 2010-2012 when it worked to deliver a bankable feasibility study for converting the glauconite into conventional potassium chloride (KCl). The stock crashed and burned when the FS could not be declared bankable because larger pilot plant studies were needed to support the required equipment scale, which would have cost another $10-$20 million. By then the potash price was falling, and, given that NPK needed a $400/t KCl price for the Cambridge Process to be viable, this approach was doomed as potash settled into a $200-$250/t range. With cfr Brazil potash still around $600/t one can't be blamed for wondering if NPK will revive the Cambridge Process. But Cris Veloso explained that NPK is only deploying IP developed as part of the Cambridge research which deals with mechanical modification of the glauconite so as to manipulate the potassium release schedule. NPK wants to preserve the branding of its K Forte product as a natural material that does not require chemical processing and does not introduce salt to Brazilian fields.

With the disappointment of the reverted guidance out of the way, and evidence that NPK has its road access problem under the control, the market can focus on the contrast between the projected 2022 results and those of 2021, which involved shipping 400,133 tonnes of K Forte for revenues of CAD $27.7 million and EBITDA of $6,450,000. We are talking about a greater than 200% increase in revenues and 400% increase in cash flow. That is the really story driving the slump reversal. The bigger picture story is the May PFS which presented scenarios for expanding output to 50 million tpa by 2030, which would represent more than 50% of Brazil's potash consumption. That is a monster game changer scenario. It is not reflected in the current stock price because the market wants to see that farmer demand tracks the expansion of supply capacity expansion. That is the big test for 2023 and we hope to see the order book start filling in Q1 of 2023. The big picture scenario, however, is why I project a future price in the $50-$100 range, which assumes that NPK can fund expansion with cash flow and keep its current 54.3 million fully diluted stable.

The wild card heading into 2023 which Brazilian farmers are not thinking about is how Russia's invasion of Ukraine will play out during the winter. Sanctions against Russia have avoided including potash supply from Russia and its ally Belarus, and the Belarus problem in Q1 when Lithuania shut down its country as a transportation corridor seems to have been solved by diverting potash through Russian ports. Putin has underestimated Ukraine's resilience and the willingness of the United States and Europe to provide support, but Putin is counting on the spinelessness of poodles at both ends of the political spectrum to force a dirty deal which sacrifices the Ukrainians. He has even floated the preposterous idea that Ukraine will detonate a dirty bomb within its own country, which smells a lot like he has plans to make that happen instead of explicitly using a a nuclear weapon which could cause NATO to get serious about curtailing Putin's megalomania. Should it come to that, it is likely that shipping logistics will get disrupted and cause global potash prices to spike in H1 of 2023. At 3 million tpa K Forte capacity NPK can only supply 500,000 tonnes of KCl equivalent which is less than 10% of Brazil's potash consumption. So not a solution for Brazil's ensuing potash supply problem, but certainly an end to skepticism that NPK will generate the sales needed to meed its 2023 guidance.

Plans to secure a NASDAQ listing have been delayed for technical reasons, but Cris Veloso thinks a listing could be achieved in January 2023. Such a listing would greatly expand the audience for this phenomenal and transformational growth story, so the last two months of 2022 could sustain an uptrend that delivers new highs in Q1 of 2023.

Optimistic May and Reality Check September Guidance for 2022

Brazil's Potash Demand and Supply History in 1961-2019

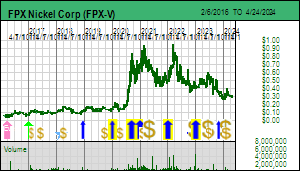

Jim (0:13:26): FPX Nickel hit a two year low last week. Is something wrong with the Decar story?

FPX Nickel has been in a perplexing downtrend given its positive fundamentals which should override the gloomy outlook for the resource sector. The problem has been a persistent seller through RBC since September which has spooked the market and made life miserable for CEO Martin Turenne. This episode discusses a possible explanation which is that a major buyer in the April 2021 bought deal that loaded FPX Nickel's treasury has lost interest in two stages. A Salt Lake City based mutual fund group had two generalist micro cap funds participate, and one of them became a heavy seller through Coremark in December 2021 that ended with a block trade in early January 2022. That this fund had liquidated was confirmed by quarterly mutual fund filings that reveal end of period holdings. As of June 30 the other fund showed as still holding 1.68 million shares. However, RBC became a net seller in September for a client which did not make contact with FPX but has been selling the stock in batches on the bid without much concern about what that might be doing to market perceptions. On Friday October 21 this selling stepped up into a blowout of 767,000 shares that took the stock to a two year low at $0.345. RBC sold another 127,000 shares on Monday, but has since been absent as a net seller and FPX Nickel's price has started to recover. The trouble is that FPX Nickel does not know it was the Wasatch group fund selling, and won't know until Q1 of 2023 when the year end filings are available. The concern remains that there is some other large shareholder who is liquidating without signaling to management that it needs to get rid of a large position. That makes the market worry that somebody knows something is wrong with the Decar story and is trying to lose a position without revealing their identity so that it can be done quickly. It wasn't helpful that director Jim Gilbert dumped a couple hundred thousand shares in September, though there probably is some reason unrelated to company fundamentals for the sales such as realizing that those cheap options exercised earlier in the year have deemed income tax consequences regardless what the stock is eventually sold at. Canadian listings are forced to withhold the calculated income tax when a Canadian resident exercises options, and given the nature of juniors and options such party will have to raise money from elsewhere and remit the wihtholding tax to the company before the exercise is executed. But those rules may not apply to a US resident though Uncle Sam will want his pound of flesh. Whatever the explanation, the market generally is ignorant about underlying realities and only contemplates the optics of an insider selling when everything supposedly is on track.

As far as I can tell everything is on track. Van drilling results are due before the end of the year, though at this point the market does not care if Van is better than Baptiste or not. The market will be able to ballpark tonnage footprint and grade estimates, but Martin Turenne has told me that the deposit needs at least another 5,000 m of drilling to achieve the drill density needed to support a 43-101 resource estimate.

An updated resource estimate for Baptiste is also expected, which may include cobalt grades, though that is likely contingent on the truly important milestone expected by the end of 2022, namely the results of a pilot plant study that involves converting 15-17 tonnes of Baptiste ore into 16-18 kg of ferro-nickel concentrate with at least 65% nickel as projected by the 2020 PEA flow-sheet. This milestone is important because no nickel deposit grading 0.1%-0.12% nickel DTR with awaruite as the primary nickel mineral has ever been commercially mined, nor has the PEA flow-sheet ever been applied to a nickel deposit. Metallurgy causes the eyes of retail investors to glaze over, but for parties such as producers who will make multi-billion dollar acquisition and development decisions they are critical. And in the case of FPX Nickel there is an alternative phalanx of backers in the form of car and battery makers eager for a secure supply of nickel sulphate and possibly cobalt sulphate whose origin also checks ESG boxes. They might not need nickel sulphate by 2030 when Decar might be in production, but they would certainly want to know that whatever they invested to help FPX Nickel with feasibility demonstration will at a minimum feed the stainless steel market.

If FPX Nickel achieves this pilot plant study milestone it will use the 16-18 kg of ferro-nickel concentrate for small scale hydrometallurgical studies as outlined in a recent scoping study to make battery grade nickel sulphate. The car and battery makers will be looking closely at the certified specifications of the resulting nickel and cobalt sulphates. FPX Nickel will of course be very interested in the implied cost of converting the concentrate into sulphates.

The validity of the flow-sheet aside, another market concern is the future price of nickel, which is currently around $10/lb, and what inflation has done to the CapEx and OpEx assumptions in the October 2020 PEA. To stress test the potential impact I have increased the CapEx and OpEx assumptions by 20% and run a DCF model using the PEA's ore schedule which does not assume any payability for the magnetite by-product or any premium for upgrading the ferro-nickel concentrate to battery grade sulphates that include cobalt. At the base case price of $7.75/lb nickel the after tax NPV per share ranges from $2-$10 per share for 10% and 5% discount rates. But at $9.96/lb that range jumps to $8.66-$21.65 per share. If you think $10/lb will be the new long term price for nickel and inflation will be back to 2% or lower as a result of quantitative tightening now trying to engineer a global recession, and you assume FPX Nickel will achieve its milestones, then it is clear why I regard it as a KRO Favorite with Good Speculative Value and a future buypout target in the $2-$5 range. The junior will have to raise more capital to deliver a PFS, but it will have $5 million working capital left by the end of 2022, which means it will not need to finance until the next set of milestones have been delivered.

FPX Selling Selling History of RBC and Coremark since July 1, 2021

AT NPV DCF Sensititivity Analysis of Decar 2020 PEA

AT NPV DCF Sensititivity Analysis of Decar 2020 PEA with 20% CapEx & OpEx Escalation

Long Term Nickel Price and Warehouse Stocks Chart

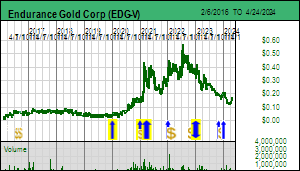

Jim (0:22:37): Endurance Gold did something unusual last week, namely announced a financing at a premium to the market. How is that possible in the current market climate?

In a market where brokerage firms are bullying juniors into doing deeply discounted bought deals, with the stock price subsequently ending up even lower as existing shareholders vomit with revulsion, it is very odd to see a $1.5 million private placement at a premium to the market with only a half warrant that not only has a term of just 2 years but whose exercise price is more than 50% above the stock price at the time the PP is announced. Endurance Gold is clearly not dealing with graduates from the Carlsbad School of full five year warrants who have been trained to invest only in losers that do nothing for the next five years before getting rolled back and given dumb names like "outcrop gold" as if there is anything of that sort left to be found on planet earth. Especially in a bear market where clients think brokers, analysts and newsletter writers are unusually endowed with stupidity. I suspect family offices already long EDG are adding to their positions, and newcomers, who have watched the company deliver positive fundamentals in 2022 without getting any market reward in the form of a higher stock price, are eager to pay up to get a position in a market whose existing shareholders are rather reluctant to sell any stock.

EDG doesn't have to finance right now but CEO Robert Boyd is a rather risk averse individual who likes to see money in the bank that he does need quite yet, even though he has released assays for 16 holes in 2022 that have greatly expanded the understanding of the mineralizing architecture at the Reliance gold project in southern British Columbia, and still has assays pending for at least 20 holes from the 8,000 m program that will arrive by the end of the year. Reliance can be drilled year round and it makes sense to resume in Q1 of 2023 rather than wait until late Q2 as has happened in previous years. Since optioning Reliance in late 2019 EDG has systematically built up its understanding of this orogenic gold system it hopes will prove a rival to the nearby depleted 4 million oz high grade Bralorne system. But it has not yet delivered that no-brainer barnburner intersection that tells the world Reliance is a multi-million ounce winner. That is why, in the bear market context, EDG is still limping along in the $0.35-$0.45 range it started out at the beginning of 2022, and which is why, much to my frustration, I have not been able to promote it from a Bottom-Fish Spec Value rated junior to a Good Spec Value rated KRO Favorite. But the company sure looks like a candidate for my 2023 KRO Favorites Collection.

EDG has had a busy week. After announcing the PP last week it announced an exploration agreement with the Bridge River Indian Band which outlines how EDG and the band will collaborate on various issues like archeaology and sensitive habitat in their traditional territory (much of which was obliterated long ago by BC Hydro's Carpenter Reservoir). I checked out their web site and discovered that this group has lots of business interests, and doesn't seem overly interested in the woke monster recommendation that they ditch the word "Indian" and rename themselves the Bridge River Indigenous Band. Somebody there probably felt it sounded too much like "Indigent". Instead I discovered they have renamed themselves the Xwisten people which makes me immediately think, oh no, images of "twisting in the wind" like shareholders of certain Canadian resource juniors whose management deals with its incompetence by rewarding everybody with a severe rollback. But apparently it is pronounced "hoist-in" which does exude a can do mentality unlike what one can detect in places like Moosonee where they celebrate traditional arts like trapping wild fur bearing animals so their pelts can adorn Putin Poodles hiding in Switzerland and blasting migrating birds out of the sky. No, the Xwisten sound like realists and it is good to see EDG work out an understanding with them that respects everybody's interests.

The other development was to option on reasonable terms the Sanchez claims adjoining to the east of the Olympic claims optioned earlier this year from Avino and recently made definitive. When you look at the map it is important to understand that the Bralone district from which 4 million ounces were mined at 15 g/t from a system of deep orogenic veins is part of a continuum that wraps around the Bendor Batholith to the northeast of Bralorne and south of the Reliance-Olympic-Sanchez land package. It is becoming clear that Boyd's understanding is scaling from an initial rethink of something he looked at during his Homestake days when a dowser controlled the Reliance story to a big picture vision that not only is the Royal-Treasure corridor a major gold system higher up in the orogenic model than Bralorne, as evidenced by the antimony rich nature of showings within his land package, but it repeats itself along the northern flank of the Bendor Batholith. Key to his vision is that past exploration has been hindered by the heavily forested mountainside and a blanket of ash from the very recent Meager Creek volcanic eruption. EDG's Reliance play is about to scale from chasing what appeared to be a limited scale high grade gold system into a major district play within a 10 km by 5 km area.

Map of Endurance Gold's Expanded Reliance Land Position

Regional Geology Map for Bralorne-Reliance Area

Disclosure: JK owns Endurance Gold, FPX Nickel, Verde Agritech; FPX Nickel and Verde Agritech are Good Spec Value rated Favorites; Endurance is Bottom-Fish Spec Value rated

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch October 21, 2022: Update on May 2022 MIF Picks

Jim (0:00:00): In May you presented 5 companies at the Metals Investor Forum in Vancouver. How have they fared in the current bear market for juniors?

When we talk about TSXV juniors these days we have to distinguish between resource and non-resource listings. When I started working in the sector in 1983 resource juniors ruled, but that decade the VSE quickly became ruled by non-resource listings. By the 1990s regulatory reforms had shifted the balance back to resource listings, and, after the Bre-X debacle, the 43-101 reforms set the stage for resource juniors to benefit from the China super-cycle which shifted the focus from discovery exploration to feasibility demonstration. I have TSXV value traded data back to 2000, but I am only able to differentiate value traded between resource and non-resource listings from 2009 onwards. Thes TSXV Index created in 2001 initially reflected the resource listing skew of the TSXV, and in the first graphic below which depicts the traded value of all TSXV listings the performance of the TSXV Index you can see a strong correlation bwteeen the daily traded value and the performance of the index until about 2013 by when the resource listings had settled into a decade long bear market. When you look at this chart you see modest TSXV Index fluctuations since 2016 but two major value traded spikes in Q4-2017:Q1-2018 and Q1 2021.

The TSXV Index is a misleading indicator because it represents only 10% of listings, and their composition is constantly adjusted to reflect company market capitalization, with a selection mechanism that preserves the value of ousted members. At this stage the composition is roughly 50:50 between resource and non-resource listings. Given the completely different market dynamics, the TSXV Index is useless, not because its 50% decline from the peak in early 2021 exaggerates the performance, but rather because it understates how hideously negative TSXV listings as a group have performed. The second set of graphics keeps the TSXV Index but isolates the resource and non-resource listing traded value. The daily value traded scale on the left is the same for both charts, which allows you to see that since the 2009-2012 post crash rebound the TSXV non-resource listings have experienced two major capital inflow booms while the resource listings had a modest awakening in 2016-2018 and a somewhat better capital inflow in 2020-2022. It is important to understand how uninterested the market has become in non-resource TSXV listings this year. The third and fourth charts show on a long term and short term scale the relative percentage of traded value. The value traded value bars are stacked so it is not easy to see which is dominant, but the relative percentage line charts (red non-resource, yellow resource) clearly show which group was dominant.

The crossover to non-resource listing dominance began in 2012 and persisted except for a brief period in 2020 when gold charged through $2,000 in the wake of the Covid response. But a major crossover in favor of resource listings took place in December 2021 and it persists to this day. Both groups are suffering dwindling daily traded value, but the decline in non-resource listing traded value is much worse than for resource listings. Intuitively, when you consider that cannabis and and cryptocurrency related listings were dominant themes during the past decade, this reversal makes sense. KRO, however, only covers resource listings, so while it is nice to see cannabis and crypto stories fade away, the more important question is where are the resource juniors headed?

The final chart of this collection groups TSX and TSXV resource companies into price ranges, of which the most important one is the % of stocks trading below $0.10, a level which means nothing on the ASX, but which on the Canadian exchanges has historically represented companies headed for extinction as a defunct delisting or a rollback that wipes out existing shareholders. This graphic shows how hideous the decline was from mid 2011 until late 2015 when 66.1% of resource listings traded below a dime. There was a modest resource rally in 2016-2018, but that reversed in mid 2018 and hit a nadir at 53.7% in March 2020 during the Covid meltdown. The gold rally and general hysteria in early 2021 pulled up resource listings so that only 22% were left stranded in purgatory. Since then the trend has reversed, and has accelerated in 2022, with currently 41.5% trading below a dime. My prediction is that this percentage will be much, much worse by the end of 2022. In fact, we are facing a monster house-cleaning event in December as shareholders assess the resource juniors left in their portfolios and dump everything that does not reveal a committed management with a plausible long term story. The point of this KW Episode is to assess my five May 2022 MIF picks in terms of how they will be dealt with by the coming capitulation.

Long Term Chart of TSXV Index and Daily Traded Value for All Listings

Comparison of TSXV Value Traded between Resource and Non-Resource Listings

Long Term Chart of Relative Traded Value of TSXV Resource and Non-Resource Listings

Short Term Chart of TSXV Resource and Non Resource Realtive Traded Value

Relative Performance of Cdn Resource Listings in terms of Price Ranges

Jim (0:06:17): Let's start with P2 Gold, one of your KRO Favorites which is working on the Gabbs copper-gold project in Nevada. What is needed to reverse its downtrend?

At the end of 2021 I introduced a new concept where I would create a collection of KRO Favorites which weren't missing any pieces for success like those resource juniors I tag with a Bottom-Fish rating, and make them available on an unrestricted basis to the public. The 2022 Favorites featured only 8 companies, of which P2 Gold was one. The idea was that individuals would pay $450 per year to get access to the research platform and my collection of Bottom-Ftagged juniors which needed to secure some missing piece in order to develop an uptrend. As these pieces fell into place I would convert them into a KRO Favorite, ideally after the stock had risen several times from its bottom-fish equilibrium level. What a terrible year to launch this initiative!

At first it worked well, with the group gaining 32.8% by April, but since then it has been downhill, bottoming down 39.4% in September and currently limping along at down 33.9%. Worse, or perhaps fortunately so, I have not felt it necessary to add any bottom-fish graduates during 2022. Gold is down 9.7% so far this year, and the TSXV Index is down 36.8%, but it is no consolation that the 2022 KRO Favorites Index is down slightly less than a market index which is 50% polluted by non-resource juniors which we know have done much worse than resource juniors. The table below shows that only one KRO Favorite, Verde Agritech, is up for the year; the rest are down 31%-67%.

P2 Gold is down 59.6% thanks largely to how gold and copper have performed this year. Copper is understood as a proxy for the trend in the global economy, and despite all the talk about the demand boost required by the energy transition, a demand boost whose deliverability is not evident in the copper mine development pipeline, copper is not just signalling a macroeconomic downturn, but a failure of the energy transition dream. Or, more charitably, a disconnect between the market and projected reality. Gold is another matter because if Mr Goldfinger turned the 6.8 billion ounce above ground gold stock stored in vaults radioactive, it wouldn't change a thing in the way the real world operates, just as the flash evaporation of every Bitcoin wallet wouldn't. So what gold's price should be is anybody's guess, but in the case of copper it needs to be high enough to justify mining enough to make the energy transition a reality.

The flagship project of P2Gold is the Gabbs copper-gold project in Nevada for which the junior plans to deliver a PEA by the end of 2022. Early this year I created an outcome visualization which imagined a 20,000 tpd open-pit operation that simultaneously heap leached the higher gold grade oxide cap and milled the copper rich sulphide resource. At the time when gold was $1,900 and copper $4.50 the LOM DCF model just barely cleared development hurdles with the existing resource. But that didn't matter because what P2 Gold's Ken MacNaughton and Joe Ovsenek planned to do was create an optimized mining plan which heap leached the gold cap first and used the cash flow to fund the later CapEx to mill the the sulphides. Meantime the prices of gold and copper have declined sharply, such that my simplistic OV's outcomes are far below development hurdles. The question now is what have current prices done to the assumptions in the optimized PEA mining plan?

The market has given Gabbs a big thumbs down, which is only fair if you assume current metal pricing relative to costs represents the long term reality. But not if you consider that once the PEA is published, the clock starts ticking on a balloon payment to the vendor that is not in the bank. The vendor is Waterton, which as part of the Gabbs deal is the largest shareholder of P2 Gold. Ken and Joe have put serious personal money above the current market price into P2 Gold, so this is not an example of some deal where the principals got nearly free paper in a private company that was then folded into a shell. The value of the PEA will be that it establishes the optimal mining scenario for Gabbs and its underlying cost structure. It may not be viable at current gold and copper prices, but in the case of copper it is reasonable to assume that the future which depends on copper is not viable at the current copper price. Now if Waterton operates in the mold of the Carlsbad school where you always press your advantage, next year it will force a default, leaving it in control of a shell whose only asset is the Bam gold project in the Golden Triangle and a couple principals who put their money where their mouth was and upgraded the optionality value of the Gabbs project which Waterton scavanged during the bear market of the past decade.

The upside now hinges on Bam. During 2022 P2 Gold drilled 13,958 metres in 95 holes into the epthermal Monarch gold zone of which 59 holes are still pending. At the start of 2022 there was a plan to test the hypothesized feeder for this gold mineralization which required some deep holes. But weather delayed the geophysical surveys so the company has focused on shallower drilling designed to outline a near surface resource and provide zonation data which when correlated with the geophysical data will allow vectoring into the likely feeder target for testing in 2023. Bam has its own approaching vesting deadlines which may not be achievable if Waterton extracts Gabbs and tries to turn Ken and Joe into P2 Gold minions. So P2 Gold is in a sense a complex bet on how title to Gabbs will be established on a win-win basis. The wild card is that the remaining Bam results are so good that Gabbs becomes irrelevant as P2 Gold turns into a Golden Triangle gold discovery delineation story.

P2 Gold Performance relative to KRO 2022 Favorites Index

Long Term Charts for Copper and Gold

Gabbs outcome Visualization Charts

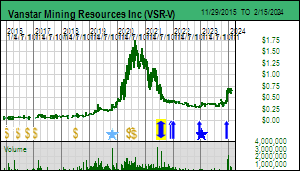

Jim (0:10:24): Vanstar is an advanced gold resource junior that is trending lower. Is Vanstar's future still tied to that of partner IAMGOLD?

Vanstar was invited to the May 2022 MIF because on the one hand it had a carried 20% interest in the Nelligan gold project in Quebec for which an open-pittable resource of 3.2 million oz had been established by IAMGOLD in 2019 at 1.02 g/t, and on the other hand it had secured an option on the Bosquet project near IMG's underutilized Doyon mill which allowed Vanstar to chase the down plunge potential for blossoming gold zones which IMG had ignored when it looked for a quick-fix open-pittable feed for its mill. Vanstar still has Bosquet assays pending, but there is no body language suggesting that anything special has been intersected at depth. The option commitments are such that Vanstar can think about Bosquet for much of 2023 while it waits to see what IMG does next with Nelligan. Since 2019 IMG has done a fair pit of drilling to extend the deposit to the west and it is planning an updated resource estimate by the end of 2022. The market would like to see the resource grind above 5 million ounces without too much decline in grade, but an increase to 4 million should be a more reasonable goal, especially given that there are still some drill density holes within the the mineralized footprint that may limit what IMG delivers later this year. In 2021 I created an outcome visualization based on the FS cost assumptions of the similar Springpole project of First Mining Gold. This 30,000 tpd open-pit scenario yields a 9 year mine life and CAD $914 million after-tax NPV at 8% using $1,643 gold, which implies a fuiture $2.82 price for Vanstar, a tenth the current valuation.

The problem is that IMG is a distressed company following a CapEx blowout this year at its Cote gold project in Ontario. However, during the past week it reached a deal to sell its Rosebel gold mine in Suriname to the Chinese miner Zijin for USD $360 million, which the creditors approved provided the money is allocated to Cote. On the one hand this means IMG lives to see another day, but on the other hand it means Nelligan sits on the sidelines. IMG still owns the Essakane gold mine in Burkina Faso, a country in the Sahel where the predations of jihadis have resulted in several recent military coups. Now there is talk of recruiting the Russian mercenary Wagner group to keep the peace, which really isn't a good scenario for western operators, but good for Chinese companies courtesy of the Russia-China axis Putin and Xi forged ahead of Putin's invasion of Ukraine. So my hope is that IMG also sells Essakane for a pretty penny which allows it to make complete a retreat to Canada as its primary operating jurisdiction. Its next best project is Nelligan, so if this were to happen, the market's doubts about the timeline for Nelligan's development and an eventual buyout of Vanstar's stake, possibly at ten times the current market price, would ease. Given that Vanstar is carried at Nelligan, I see this as a classic long term asset play.

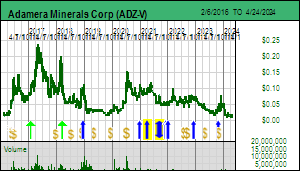

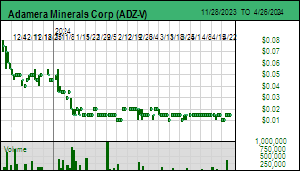

Jim (0:15:49): Adamera Minerals is a gold discovery focused exploration junior. Is it any closer to making a discovery?

Adamera Minerals has its origins as a diamond explorer in the Canadian Arctic which split itself to also engage in uranium exploration during the 2004-2008 bubble. But in 2012 Mark Kolebaba recombined the companies and changed the focus to gold exploration in northeastern Washington where high grade gold mines in the Republic Graben had shut down. This became the Cooke Mtn project which ADZ tackled with a new round of geophysical surveys designed to detect skarn hosted sulphide bodies overlooked by past exploration. While tidbits were intersected such as Oversight, nothing grew into a meaningful discovery. In 2020 the Peruvian high grade miner Hochschild optioned the project with the idea of applying a deeper form of IP surveys. This led to some promise on the Lamesfoot South claim, but Hochschild dropped out in 2022.

This year ADZ drilled several more holes which yielded high grade gold over short intervals less than 1 km from the depleted Lamefoot deposit from which Echo Bay underground mined 1 million oz at 8 g/t. The market has largely ignored this development, partly because it has been fooled before by such intervals, but also because it is hard to believe Echo Bay would have missed anything so shallow nearby. However, these zones are rod like and you need to get lucky to tag into one. We will have to wait to see if additional drilling fleshes out the zone or makes it disappear. So the100% owned Cooke Mtn story may undergo a revival.

But the real story is Buckhorn 2.0, the original land position Kinross assembled around its Buckhorn Mine lease. Crown Resources Corp discovered the Crown Jewel deposit in 1988 and initially tried to develop it with Battle Mtn as an open pit mine, but that went nowhere in Washington. Kinross acquired Crown in 2006 and developed Buckhorn as an underground mine whose ore it trucked to the 2,100 tpd Kettle River mill in the Republican Graben area where the Cooke Mtn claims are. Buckhorn produced 1.3 million oz at 13 g/t from 2008 until 2017 when it ran out of ore. Located in the Torodo Graben this skarn deposit was the only mine to emerge despite a century of groups poking around the gold teases at surface in the surrounding area.

Kinross assembled a 3,600 ha land package around the Buckhorn lease and drilled 281 shallow holes for 50,250 m mostly to the east. As Buckhorn's depletion approached Kinross filed a monster plan of operations with the USFS in what was going to be a massive search and destroy mission in the surrounding area. It hit a wall, Kinross gave up, and by 2020 had let all the claims lapse except the mining lease for whose reclamation it remains responsible. With Cooke Mtn optioned to Hochschild Kolebaba staked the entire former land package in 2020 and began to conduct geophysical surveys. In 2021 Adamera was able to strike a data deal with Kinross that gave ADZ access to all the historical data outside the lease. The company has been busy integrating these data sets and supplementing it with new data sets such as a Lidar survey which has helped reveal where prospectors ages ago beavered away. Buckhorn 2.0 straddles 3 permitting jurisdictions: State, BLM and USFS. Drill permits have been secured for the State and BLM portions and this summer ADZ began drilling geophysical targets on these claims. The best targets, however, sit on the USFS land and ADZ is still waiting for these permits which seem imminent but always slip into tomorrow.

This week ADZ announced that it has intersected sulphides in the first three targets, which the market liked somewhat because the gold in the Buckhorn skarn deposit is associated with sulphides, a necessary condition, but not a sufficient condition. The true significance of the news is that the geophysical targets are being validated by drilling and we can now hold our breath for assays. Buckhorn 2.0 will be a process of elimination drill strategy seeking a zone that has running room. I have created an outcome visualization of what Buckhorn 1.0 would be worth today if underground mined at 900 tpd with the ore trucked to the Kettle River mill which is mothballed. The AT NPV at 8% is CAD $920 million which translates into a future price target of $3.48. The size of this prize has not been negatively impacted by the recent decline in the price of gold, so Adamera Minerals remains a Bottom-Fish Spec Value rated junior with siginficant discovery exploration upside potential. What is important is that exploration is being done in the same geological context as Buckhorn 1.0, so if ADZ starts hitting a similar zone, the market is primed to understand the upside implications. It is also helpful that Crown alumni such as Mark Jones and Chris Herald have joined the board.

Relative Location of BUckhorn 2.0 and Cooke Mtn Project areas

Graphic showing structural axis of new Lamefoot South Zone

Google Earth shot of new Lamefoot South zone relative to depleted Lamefoot deposit

Comparison of Buckhorn Drill History with Gold Geochemical Data

Outcome Visualization of original Buckhorn Mine

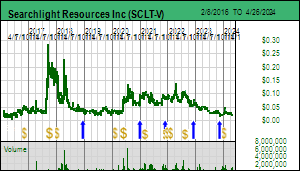

Jim (0:20:42): Searchlight Resources is a Saskatchewan focused junior with exposure to a wide range of metals. Is it any closer to delivering a discovery?

Searchlight Resources is a Saskatchewan focused junior headed by Stephen Wallace and Alf Stewart which started off assembling a gold district callled Bootleg Lake west of the Flin Flon VMS mining camp but has more recently branched into Saskatchewan's critical metals potential with Kulyk Lake as the current flagship. The idea at Bootleg Lake was to consolidate the fragmented ownership and start chasing the high grade orogenic veins down plunge to see if they blossom at depth. But market interest in such plays has stalled. Kulyk Lake has a high grade rare earth showing discovered decades ago and studied by academics but never drilled. During the 2009-2012 Rare Earth Mania 1.0 Eagle Plains staked it and cut a number of maximum 1 m wide trenches across the monazite showings. A table of the results is provided below. I have averaged the trench values and generated a REO distrbiution chart which also includes the in situ value distrbution based on current rare earth oxide prices.

The REO distribution is typical for monazite with 97.4% light rare earths. 85% of the $4,491/t rock value resides in neodymium and praseodymium, the light rare earths used for permanent magnets. The average grade of 16.59% TREO is meaningless - a 0.6 m trench averaged 45.1%. Kulyk Lake has never been drilled because the monazite appears to occur as narrow seams tracking Kulyk Lake. To turn this into a mine one needs to develop a multi-million tonne zone that can be open-pit mined. Such a deposit needs to grade 3%-6% to be worth developing, which translates into a rock value of $800-$1,000 of which only 85% in the form of Nd and Pr is worth recovering.

In 2021 Searchlight conducted a radiometric survey over the Kulyk Lake trend in an effort to use thorium to assess the potential scale of the monazite mineralization. The thorium data revealed a 6 km trend on the northwestern flank of Kulyk Lake which also repeats itself a km to the northwest. The survey also collected uranium data and revealed a sizable uranium anomaly to the southwest of the thorium anomaly. This got the company excited last year while the uranium bugs were flexing their muscles because it was large and unexpected. Field visits this summer have revealed that this is a pegmatite hosted system grading less than 0.1% U3O8 similar to the Rossing deposit in Namibia. This target will need a drill program to see if it represents a bulk mineable resource. The company has also done several sampling passes over the thorium anomaly and is still awaiting results.

The market question is whether or not a case can be made for drilling the rare earth target in 2023 to see if the monazite seams can average out into a mineable zone. As such Kulyk Lake does not yet qualify as an "emerging discovery" but it remains intact as a story. The Saskatchewan Research Council has created a pilot plant to process monazite samples as part of an initiative to develop rare earth expertise, so if there turns out to be size and grade at Kulyk Lake it could quickly become a big story.

The latest development that intrigues me is some staking SCLT did this week in an area north of Hanson Lake west of Flin Flon where SCLT owns claims covering a cluster of LCT pegmatites whose grade and size do not appear overly interesting. The junior optioned them to a private party earlier this year which was interested in the VMS potential. I grumbled about that to Stephen and Alf at the May MIF, and asked why does Manitoba have good lithium pegmatite potential and not Saskatchewan. Stephen mumbled that Hanson Lake seems to be the best documented, but did digest my argument that Lithium Mania 2.0 is based on the idea that the economic irrelevance of LCT pegmatites until the past decade discouraged exploration and that the documented showings were largely a result of prospectors doing a face-plant onto a whitish outcrop. Being GeoDataGeek he couldn't resist going through the data archives in search of potential pegmatite fields that were not recognized as such. An area north of Hanson Lake caught his interest, but it was already owned by parties looking for something else. These claims lapsed this year and the MARS system opened them as part of a monthly opening of lapsed claims. Wallace didn't have any competition so got what he wanted, and is now awaiting title confirmation before announcing the acquisition. He cautions that while he is confident a pegmatite field is present, he has no data indicating that they are LCT enriched because nobody appears to have bothered sampling antyhing in this area. At this point the Hanson Lake North pegmatite play is a longshot, but it is an example of the Great Lithium Rethink now underway which could be transformative for toiling geologist style juniors.

Location map of Searchlight's Saskatchewan Projects

Kulyk Lake Thorium Anomaly and Photo of Monazite Outcrop

Table of Kulyk Lake Trench Results collected in 2009-2012 by Eagle Plains

Rare Earth Content and Value Distribution of Monazite at Kulyk Lake

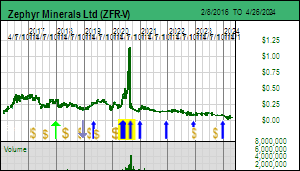

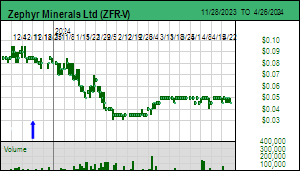

Jim (0:26:28): Zephyr Minerals is trying to establish itself as a gold junior in Zimbabwe. Is it any closer to doing so?

Zephyr Minerals was invited to my May 2022 MIF session because in 2021, building on management's international experience, the company decided to investigate the gold potential of Zimbabwe which after decades of misrule by Mugabe had transitioned from autocracy to democracy and reformed its mining law so that foreign countries can have majority ownership of future mines. Zimbabwe has a century long history as a gold producer thanks to the orogenic gold systems in its Archean craton's greenstone belts. But when Mugabe took control decades ago commercial gold mining dwindled and most of Zimbabwe's gold production came from artisanal workers chasing the high grade structures down to the water table. Consequently Zimbabwe missed the boat during the past two decades enjoyed by West Africa where mining companies acquired the near surface depleted workings of artisanal workers and evaluated the systems as lower grade open pit mining opportunities.When Zimbabwe changed is mining law in 2020 there was a rush of companies led by Australians to apply for "exclusive prospecting orders" or EPOs, most of which were granted by early 2022. Zephyr was part of the second application wave in mid 2021 and hoped to have its 2 EPOs granted by this summer. However, it is still waiting for approval but seems to think this may finally happen in November. The stock meanwhile has languished because until it has the EPOs granted it only has a pending story.

But something else is happening in Zimbabwe As juniors are discovering in Newfoundland, pegmatite trends often occur parallel to gold mineralization trends. Back in May Loren Komperdo wasn't much interested in lithium, but since then the idea of Lithium Mania 2.0 has gained momentum. In fact, there is a new wave of EPO applications in Zimbabwe targeting pegmatite fields. During the middle of the past century Zimbabwe was the biggest lithium producer in the world because its pegmatites tend to feature both petalite and spodumene lithium mineralogy. But only the petalite zones were mined because they have the purity required by the main users at the time, the glassware and ceramics industry. The spodumene was ignored. Lithium demand picked up in the 1990s thanks to lithium ion batteries in electronic equipment such as laptops and cell phones. But around 2015 Lithium Mania 1.0 kicked in as the market realized that the car industry was embracing electic vehicles in response to climate change policy and the example set by Tesla. In 1995 lithium supply was about 10,000 tonnes lithium metal equivalent but by 2021 it had increased ten-fold thanks to EV battery demand. Now the projection is that by 2030 demand will increase another five-fold and ten-fold by 2035-2040 when EV sales are mandated to replace ICE sales. The carmakers are busy investing in GigaFactories to make batteries, and are now investing in refinieries outside China to make battery grade lithium hydroxide or carbonate from concentrates. While these facilities can be built quickly, the EV sector is now waking up the reality of the hideous 5-8 year timelines for finding and developing a new mine.

The Australian pegmatites and Lithium Triangle brines may only supply half of future projected demand. The rest may have to come from pegmatites in other cratons such as eastern Canada, Brazil, Scandinavia and Africa. Lithium Mania 2.0 is premised on the reality that if these future mines are to become reality by 2030, they need to be identified right now. Lithium Mania 2.0 is not so much about the M&A sweeping the lithium supply identified by Lithium Mania 1.0 during 2015-2017 and now in or close to production, but rather about an exploration boom during the next 2-3 years which will lead to feasibility demonstration, permitting and construction in 2026-2030. This is the ideal arena for resource juniors which, starting with very low market capitalization bases, have the potential to undergo 100 fold price increases very quickly if they find a large pegmatite grading 1% Li2O or higher.

In the case of Zimbabwe, ASX listed Prospect Resources Ltd acquired the Arcadia deposit not far from Harare during Lithium Mania 1.0 and brought it to the stage of an optimized feasibility study. Then in December 2021 it received an offer from Huayou Cobalt to purchase its 87% stake for USD $377.8 million. This deal closed in April 2022 and Prospect distributed AUD $0.96 per share as a special dividend and kept about $35 million to continue exploring for lithium on its Step Aside project in Zimbabwe and the Omoruru prospect in Namibia. Although the total resource was 72.1 million tonnes of 1.06% Li2O, the proven and probable resource was 42.3 million tonnes of 1.19% Li2O. This deposit has both petalite and spodumene zones. Zephyr's management has taken note of this development and the subsequent application rush, taken a second look at its EPO applications, and realized that one of them has a footprint which straddles both the targeted gold structure and a parallel pegmatite trend. So if this EPO gets granted, Zephyr will end up with a major "frontier" style land position in Zimbabwe that has both bulk tonnage gold and lithium pegmatite potential.

Zephr's Exclusive Prospecting Order Applications in Zimbabwe

Disclosure: JK owns Adamera; P2 Gold is a fair Spec Value rated KRO Favorite; Adamera, Searchlight, Vanstar and Zephyr are Bottom-Fish Spec Value rated

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch October 14, 2022: IMF keen on India's Growth Potential

Jim (0:00:00): The IMF published its semi-annual world economic outlook this week. Did anything catch your attention?

The semi-annual World Economic Outlook was published by the IMF on October 11, 2022. I like to look at the GDP data set in the form of current USD GDP for each year, which means that each year's data is based on the GDP converted from the national currency into USD at the exchange rate the IMF has chosen for that year. This is not a "constant" dollar data set where figures get adjusted for inflation. What interests me are the IMF forecasts for 2022-2027 which, given the projection that global GDP will grow 29% from $104 trillion in 2022 to $134 trillion in 2027, gives me pause to wonder how that is supposed to happen if inflation battling monetary policy crashes the global economy into a recession. Not only does the IMF have to guess what domestic GDP will be, but it needs to guess each nation's inflation rate and what the corresponding USD exchange rate will need to be. So one has to take a common sense approach with regard to these forecasts. What I find implausible is that China's growth rate will remain at 6.8% while the United States' will drop below 4%, which would allow the relative share of global GDP to converge to almost even with 22.7% for the United States and 21.1% for China in 2027. Given that Xi Jinping is about to be confirmed for a third term as China's president, has struck a "best buds" axis with Russia's megalomanical thug Vladimir Putin, and is keen on folding Taiwan's 20 million people into the hyper-surveillance slave cage he has erected for China's people on the pretence of protecting them from Covid, creating challenges for growth in exports and domestic consumption, it is hard to imagine ongoing growth of 6.8% per year. Especially given that in 2022 growth has dropped below 4% and China has not even started to face the external consequences of pumping autocracy as a superior alternative to democracy. China has a serious demographic problem and the policies it has adopted will make it worse, not better. What I did find interesting was the IMF's forecast of 8%-10% annual growth for India over the next 5 years which would grow the world's fith largest economy 54% to $5.4 trillion by 2027. That will still only be 4% of projected global GDP of $134 trillion, but that is what China's GDP represented in 2001 when it hit a tipping point that kicked off the China super cycle that was so good to the resource sector, especially the juniors that focused on demonstrating the new feasibility of marginal deposits found decades earlier. If India can overcome its self-limiting bureaucracy and corruption, it could be the driving force behind a new macro-economic growth based raw material super cycle that will be underway by 2030. While India has a young population base, and is still a fairly open society despite Modi's desire to create a Hindu theocracy, it is not a major producer of raw materials, unlike China. Furthermore, India does have nuclear weapons capacity and a distinct ethnicity that guarantees India will never let itself feel the heel of China's boot.

IMF WEO Data Current USD GDP 1980-2027

IMF WEO Data Current USD GDP Share 2022

Relative Global GDP Share Trends for USA, China & India

China GDP Growth History

India GDP Growth History

India's Share of Raw Material Production

Jim (0:08:24): Nice to see India getting its act together but will the junior resource sector still be around by then?

The market had another bad week when the September CPI figures showed that year over year inflation was still at 8.2%, down from 8.3%. Evidence that the overall inflation rate is no longer rising should be good news, but the bad news lay within the Core CPI which strips out the Food and Energy sub-groups whose price changes are volatile. The decision by Saudi Arabia and Russia, both autocracies, to curtail oil production in order to reverse the summer decline in oil prices raises the prospect that CPI will soon enough be trending higher. Core CPI is 6.63% year over year but on month over month basis it remains stuck between 0.4%-0.8% which the market interprets as interest rate hikes not yet having an impact on consumer demand. This means the Federeal Reserve has no choice but to jam rates higher and further risk a collapse in asset prices and ensuing recession. None of this is good news for gold. There is speculation that the Opec-Plus decision to force oil prices higher is designed to push the US mid-term elections into the hands of the Putin Poodle Party which will do its best to prevent Biden from steering America out of a Powell recession, as the Tea Party so effectively did after 2010 when its control of the House enabled it to block Obama's fiscal policy efforts to grow the economy out of the 2008 Crash engineered by Wall Street. Gold doesn't do well in a high interest rate environment, and it also floundered in the past decade's ultra low interest rate environment. So it is hard to see gold do well in the face of interest rate hikes that are still a fraction of what Paul Volcker inflicted on the market over 3 deacdes ago. For this reason I am only interested in gold exploration plays which deliver a discovery with the grade and scale to remain interesting even if gold slips back into the $1,200-$1,400 range. In my personal view gold should be soaring past $2,000 to reflect the extreme uncertainty afflicting so much of the world. But these days there is the new distraction of Bitcoin whose miners are happy to use cheap natural gas Putin is no longer delivering to Europe. It's already clear that the "libertarian" song of Bitcoin lovers has nothing to do with freedom but rather the freedom of individuals to raid the freedom of others because of an inherent superiority. But how long before individuals who own Bitcoin simply out of greed realize that they are unwitting Putin Poodles? The two themes that interest me with regard to resource juniors are the security of supply issues created when the global economy splits into autocracy and democracy defined trading zones, and where the lithium is supposed to come from to make the EV replacement of ICE cars by 2035 a reality. The China-Russia axis poses a major problem for democracies. Russia is now doomed to be a pariah nation for a very long time. Its economy is 2.1% of global GDP and ranks in ninth place just behind Canada. The IMF projects Russia's GDP to hardly grow at all over the next five years, which would shrink its share of global GDP to 1.6%. Russia is the world's fifth largest military spender at $66 billion for 2021, which is just 3.2% of the $2.1 trillion the world spent on defence in 2021. Compare that to $801 billion for the United States at 38.5% and China at $293 billion for 14.1%. If Russia did not have a legacy arsenal of nuclear weapons it would be a nothing burger in military terms. China itself is headed toward becoming a pariah nation, so it makes sense for Russia to carry on its tradition of enriching its oligarch elite through resource extraction for the benefit of China while letting its domestic economy stagnate as Russians who abhor the idea of being a Putin Poodle flee the country. Going forward we can expect European nations as well as Japan and South Korea to ramp up military spending which is below 2% of GDP compared to Russia's 3.7% as they contemplate a possible election turnover in the United States to a party increasingly dominated by people who admire Putin and autocracy. These are not people who fear the heel of a boot but who imagine they will be one with the boot heel that crushes the freedom of others. But if this spell ends up broken, Russia cannot prevail on its own and will become a future colony of China which will be very interested in the vast riches of Siberia. Unless this growing geopolitical conflict resolves itself in a manner that allows globalized trade to resume, there will be a scramble to develop new raw material supply in demcoracy run jurisdictions that are secure, and the resource juniors will play a major role in that effort.

Comparison of DJIA in 1920-35 with 2010-2025

US Consumer Price Index 2000-Present

US Consumer Price Index Core (minus Food and Energy)

Tracking how much CPI Sub-Groups have increased since 1980

Long Term Price Chart for Gold

Long Term Price Chart for Oil

Potential Gold Price Limits based on Uncertainty

China and Russia combined share of Raw Material Production

Russia GDP Growth since 1991

Global Military Spending in 2021

Top Military Spenders in 2021 and the share of domestic GDP

Lithium Mania 2.0 is based on the idea that by 2035-2040 the world will need to produce 10 times more lithium than in 2021 if the goal of replacing ICE car sales with EV sales is to become reality. Depending on the lithium carbonate price that represents a future market worth $100 billion annually at $10/lb lithium carbonate ranging to $300 billion at $30/lb. Half of that future demand will likely be supplied by current producers led by Australia, the Lithium Triangle in South America and perhaps China. The rest will have to come from low grade claystone style deposits such as those in Nevada, direct lithium extraction from brines associated with oil fields, and LCT enriched pegmatites. The first requires a high lithium price that may prove an obstacle to large scale adoption of affordable EVs. The second is an emerging process technology that still needs to be commercialized. The third is the simplest solution because there is an abundance of 5 million tonne pegmatites grading 1% Li2O or better that are open-pittable and yield a spodumene concentrate whose conversion into battery grade lithium hydroxide or carbonate is established process technology. The pegmatites occur in Archean shields such as those in eastern Canada, Scandinavia, Brazil and parts of Africa. Their presence has been documented as part of exploration for other metals, but never seriously explored because global lithium demand until recently was readily met by a few giant pegmatite mines like Greenbushes and Bernic Lake and the salar brines in Chile. While this additional supply is not needed until 2030 when we can expect EV adoption to go exponential, the 5-8 year exploration, permitting and development cycle means the time to recognize this supply problem and deal with it is right now. Lithium Mania 2.0 is based on the idea that resource juniors will scour these pegmatite trends over the next two years and very rapidly delineate open-pittable deposits with sufficient size and grade to move into feasibility demonstration. The huge potential value of the future lithium market will attract major mining companies such as Rio Tinto. Because it is unlikely that the supply will come from a view monster deposits such as is the case for niobium with the Araxa carbonatite deposit in Brazil, this is a game which will have many winners as multiple deposits are developed to feed centralized refineries. It will be something like the uranium boom in 2004-2008 whose institutional capital inflow supported aggregation of uranium deposits through mergers and acquisitions that flooded the uranium juniors with liquidity. When you consider that uranium supply in 2021 was worth only $4.4 billion compared to lithium worth $18 billion, and at least double that in 2022 thanks to a persistent lithium carbonate price double the 2021 average, and that the car companies have gone past the point of no return with their EV rollout plans, Lithium Mania 2.0 will be an absolute necessity. The KW August 25, 2022 Episode provides additional commentary.

Lithium Supply Growth since 1930

2021 Global Lithium Supply

Long Term Lithium Carbonate Price Chart

Rio Tinto's Vision of the Looming Lithium Supply Gap

Relative Value of Metal Production in 2021

Jim (0:23:43): How does one get up to speed on juniors that benefit from Lithium Manis 2.0?

KRO is a research platform that covers all resource focus companies listed on the Canadian and Australian exchanges. For the past few months we have made an effort to identify companies involved in lithium exploration and updated their profiles. This is an ongoing process. The KRO search engine allows one to filter for lithium juniors and do one's own research. Many of these companies are cheap and liquid. Some are leftovers from Lithium Mania 1.0 while others like Brunswick Exploration are newcomers who made the pleasant discovery that past juniors tended to focus on postage stamp sized claims covering known showings rather than exploring from a district perspective. KRO is a membership fee based service that costs USD $450 per year. Lithium Mania 2.0 will be a bubble like none before. Brunswick, which is still bottom-fish spec value rated because we are awaiting confirmtation that some of their land packages do indeed host LCT enriched pegmatites, was a member of my June Toronto MIF session so it is no secret that KRO members have been accumulating this lithium junior. The one I allude to in this episode trades below a nickel and is supposed to be involved in precious and base metals exploration in the James Bay region of Quebec where Patriot Battery Metals has made waves with its Corvette discovery. It is Bottom-Fish Spec Value rated but I don't mention its name because at this point paying KRO members are waiting to accumulate some more at cheap prices. The junior may have gold-copper discovery assays in a a month or so, but what we are really waiting for is news that field work revisiting a pegmatite trend owned and dropped years ago as part of a gold exploration play does indeed host LCT enriched pegmatites that have never been explored. The only evidence that this might be the case is a regional lake bottom-sediment rubidium anomaly. Rubidium is one of the elements that shows up in these LCT pegmatites so it is a promising indicator. In that sense Lithium Mania 2.0 also reminds me of the diamond boom Chuck Fipke launched in 1991 when Dia Met announced initial results for a diamondiferous kimberlite at Ekati. Gold may be a bear slog for the next couple years, Putin and XI might get booted out, and the plague of Putin Poodles may go back underground where it belongs, making the search for alternative raw material supplies unnecessary. But the need for substantially more lithium supply will not go away. There are many alternative EV battery technologies under development, but none will be ready for commercialization until the end of the decade, with the risk that none will be ready period. The car makers are committed to lithium ion based configurations and are going to tool up for producing lithium ion based cars, and they will want to be sure there is enough lithium supply to make that possible. Furthermore, just as much R&D is being put into developing a solid state electrolyte for the lithium ion battery which would allow lithium metal to substitute for graphite in the anode without a risk of thermal runaway (aka explosions) due to dendrite growth. This would yield a superior battery and greatly expand the future demand for lithium which currently assumes this breakthrough will never happen. We are organizing everything needed for KRO members to think intelligently about lithium juniors. It's going be a lot of fun while the overall sector and nearly everything else wallows in the gloom of Powell's coming recession.

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch October 6, 2022: Cheering Bell Tower Endurance

Jim (0:00:00): What is the significance of the latest news for the Rabbit North project of Tower Resources?

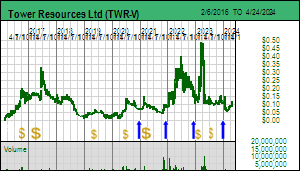

Tower Resources Ltd revealed 2 important developments with its latest update for the Rabbit North project in southern British Columbia. The first was that the last of 5 holes from the summer program drilled to cut through the Lightning Zone beneath the #26 discovery hole intersected similar mineralization with the bonus that the "crushed" appearance of the veinlets raises hopes of a higher gold grade because is evidence for deformation of the Lightning zone which enhances the capacity to absorb gold in an orogenic gold system. We dod not have assays for any of the holes yet, but the reported visuals indicate that the re-interpretation of the zone's initial ENE orientation to north-south has been confirmed. On this basis the downhole length of the #22-38 mineralized interval indicates a true width of 40-42 m over a 72 n vertical extent. The positive development is that additional till sampling has yielded evidence for a parallel structure a couple hundred metres west of the Lightning Zone that also disappears under thin basalt cover to the north. The Central Train is in addition to the Durant Creek Train inferred from the original 2021 till sampling about 500-1,000 m to the west of the Lightning Zone. Evidence for this train showed up 10 km down-ice, and in light of the Lightning zone being parallel to the Dominic Lake Train cannot explain the grains to west. The implication is that there are multiple north-south structures like Lightning whose past discovery may have been hindered by a thin post-mineral veneer of basalt. We hope to see assays by mid-November which will become the basis for funding a followup drill program that can run through winter. I've included the price based Ultimate Implied Outcome chart for the Rabbit North project. What this type of chart does is present the future valuation path of a project (assuming fully diluted does change much) in terms of share price for 2 scenarios. One is that the current implied value represents the mid-point of the fair spec value range as defined by the uncertainty ladder of my rational speculation model for the stage of the project. I am treating Rabbit North as being in the discovery delineation stage during which peak S-Curve valuation can take place. In fair value terms the current $39.2 million implied value indicates a future outcome of CAD $1.045 billion which translates into a $7.20 price target if there is no additional dilution (the blue channel). The other scenario assumes the $39.2 million implied value already represents peak S-Curve value which implies a future outcome of CAD $52.3 million or $0.36 per share as a price target (the yellow channel). Neither says what the fundamental outcome will be, but they provide a way of judging whether the current pricing represents good speculative value. For the blue channel outcome, you ask yourself, is $1 billion a plausible outcome for the sort of system and target footprint evident? The best way to find out is to do an outcome visualization for a plausible outcome based on the costs of an existing outcome already in production or for which an economic study has been published. I have not yet done that for Rabbit North. The $52.3 million peak S-Curve projected outcome is equivalent to saying the project is a bust because no mine in Canada with an NPV that low goes into production. The days of mom and pop mines in Canada are over. So that number is telling me Tower is not over-priced at this stage for a positive outcome.

Drill Plan and Geology Map for Lightning Zone area of Rabbit North

Gold in till trains and geology map for Rabbit North

Pristine god grains from new Central Train till samples at Rabbit North

Outcomes implied for North Rabbit if current value represents fair spec value or S-Curve peak value

Jim (0:03:24): What is the latest news from the Reliance project of Endurance Gold?