| Kaiser Watch October 28, 2022: Slump Reversals & Premium Financings? |

| Jim (0:00:00): Verde Agritech has recovered from its slump. Is the alternative potash story back on track? |

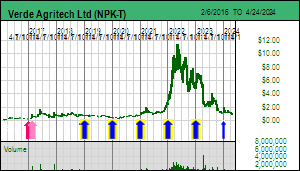

Verde Agritech has reversed the slump created on September 9 when it announced that, just when Plant 2 had been commissioned to produce K Forte at a nameplate capacity of 1.2 million tpa shipments with only a month of the primary March through September application window left, production had to be suspended for 4-8 weeks because the access road had developed groundwater problems. At the same time NPK reverted to its January guidance for 2022 which projected 700,000 tonnes of production for 2022 representing CAD $87 million in revenues and $31 million in EBITDA cash flow. The company had expanded its guidance in May to 1,000,000 tonnes production with $109 million revenue and $49 million EBITDA cash flow. The caution in January was based on uncertainty that Plant 2 would be operational in time to produce K Forte during the primary application window. Given that the rainy season doesn't begin until November, the market was unhappy that NPK was blindsided by access road problems in early September. On October 19 NPK announced that 22 km of road had been upgraded with asphalt laid on 14 km and a new bridge built so that commercial scale shipments could resume. A week later on October 26 NPK announced that phase 1 nameplate capacity had been achieved at Plant 2 but that shipments had to be postponed because the company was "sold out".

What that really meant was that NPK had shipped what it could from Plant 1's 600,000 tpa capacity but was unable to fulfill orders that counted on Plant 2 production. November through February is a slow period, and because NPK has not built warehousing capacity, Plant 2 is only operating at a level to meet the less conventional demand during this window. What this means is that while one thinks of a mine operating 24/7 all year, which would suggest a grinding capacity of 200,000 tonnes per month, Plant 2 actually has a physical capacity of grinding close to 400,000 tonnes per month. Farmers do not store fertilizer; they expect delivery just in time for application to their fields ahead of planting. However, this is consistent with the reverted guidance so not fresh negative information. In fact, the lull will allow NPK to complete the phase 2 installation and commissioning which will bring Plant 2 capacity to 2.4 million tpa output for the 2023 season for which NPK is still guiding 2 million tonnes of sales. The real question facing the market is if this expanded supply capacity will be matched with Q1 2023 demand.

The seasonal production lull is allowing NPK to repurpose Plant 1 to provide the specialty versions of K Forte like supplementing K Forte with nutrients such as sulphur as well as N Keeper which reduces nitrogen loss in the fields. Plant 2's larger footprint is also allowing NPK to develop its supply of Bio Revolution which loads K Forte with microbes chosen to rehabilitate depleted soils. The company also dropped the name of Cambridge Technology which prompts one to wonder if NPK is experimenting with the Cambridge Process developed with the help of Derek Fray during 2010-2012 when it worked to deliver a bankable feasibility study for converting the glauconite into conventional potassium chloride (KCl). The stock crashed and burned when the FS could not be declared bankable because larger pilot plant studies were needed to support the required equipment scale, which would have cost another $10-$20 million. By then the potash price was falling, and, given that NPK needed a $400/t KCl price for the Cambridge Process to be viable, this approach was doomed as potash settled into a $200-$250/t range. With cfr Brazil potash still around $600/t one can't be blamed for wondering if NPK will revive the Cambridge Process. But Cris Veloso explained that NPK is only deploying IP developed as part of the Cambridge research which deals with mechanical modification of the glauconite so as to manipulate the potassium release schedule. NPK wants to preserve the branding of its K Forte product as a natural material that does not require chemical processing and does not introduce salt to Brazilian fields.

With the disappointment of the reverted guidance out of the way, and evidence that NPK has its road access problem under the control, the market can focus on the contrast between the projected 2022 results and those of 2021, which involved shipping 400,133 tonnes of K Forte for revenues of CAD $27.7 million and EBITDA of $6,450,000. We are talking about a greater than 200% increase in revenues and 400% increase in cash flow. That is the really story driving the slump reversal. The bigger picture story is the May PFS which presented scenarios for expanding output to 50 million tpa by 2030, which would represent more than 50% of Brazil's potash consumption. That is a monster game changer scenario. It is not reflected in the current stock price because the market wants to see that farmer demand tracks the expansion of supply capacity expansion. That is the big test for 2023 and we hope to see the order book start filling in Q1 of 2023. The big picture scenario, however, is why I project a future price in the $50-$100 range, which assumes that NPK can fund expansion with cash flow and keep its current 54.3 million fully diluted stable.

The wild card heading into 2023 which Brazilian farmers are not thinking about is how Russia's invasion of Ukraine will play out during the winter. Sanctions against Russia have avoided including potash supply from Russia and its ally Belarus, and the Belarus problem in Q1 when Lithuania shut down its country as a transportation corridor seems to have been solved by diverting potash through Russian ports. Putin has underestimated Ukraine's resilience and the willingness of the United States and Europe to provide support, but Putin is counting on the spinelessness of poodles at both ends of the political spectrum to force a dirty deal which sacrifices the Ukrainians. He has even floated the preposterous idea that Ukraine will detonate a dirty bomb within its own country, which smells a lot like he has plans to make that happen instead of explicitly using a a nuclear weapon which could cause NATO to get serious about curtailing Putin's megalomania. Should it come to that, it is likely that shipping logistics will get disrupted and cause global potash prices to spike in H1 of 2023. At 3 million tpa K Forte capacity NPK can only supply 500,000 tonnes of KCl equivalent which is less than 10% of Brazil's potash consumption. So not a solution for Brazil's ensuing potash supply problem, but certainly an end to skepticism that NPK will generate the sales needed to meed its 2023 guidance.

Plans to secure a NASDAQ listing have been delayed for technical reasons, but Cris Veloso thinks a listing could be achieved in January 2023. Such a listing would greatly expand the audience for this phenomenal and transformational growth story, so the last two months of 2022 could sustain an uptrend that delivers new highs in Q1 of 2023. |

Verde Agritech Ltd (NPK-T)

Favorite

Good Spec Value |

|

|

| Cerrado Verde |

Brazil - Other |

9-Production |

K |

K Forte Application Windows in Brazil |

Optimistic May and Reality Check September Guidance for 2022 |

Brazil's Potash Demand and Supply History in 1961-2019 |

| Jim (0:13:26): FPX Nickel hit a two year low last week. Is something wrong with the Decar story? |

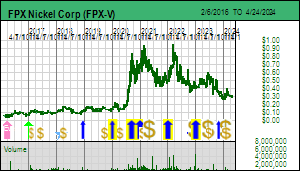

FPX Nickel has been in a perplexing downtrend given its positive fundamentals which should override the gloomy outlook for the resource sector. The problem has been a persistent seller through RBC since September which has spooked the market and made life miserable for CEO Martin Turenne. This episode discusses a possible explanation which is that a major buyer in the April 2021 bought deal that loaded FPX Nickel's treasury has lost interest in two stages. A Salt Lake City based mutual fund group had two generalist micro cap funds participate, and one of them became a heavy seller through Coremark in December 2021 that ended with a block trade in early January 2022. That this fund had liquidated was confirmed by quarterly mutual fund filings that reveal end of period holdings. As of June 30 the other fund showed as still holding 1.68 million shares. However, RBC became a net seller in September for a client which did not make contact with FPX but has been selling the stock in batches on the bid without much concern about what that might be doing to market perceptions. On Friday October 21 this selling stepped up into a blowout of 767,000 shares that took the stock to a two year low at $0.345. RBC sold another 127,000 shares on Monday, but has since been absent as a net seller and FPX Nickel's price has started to recover. The trouble is that FPX Nickel does not know it was the Wasatch group fund selling, and won't know until Q1 of 2023 when the year end filings are available. The concern remains that there is some other large shareholder who is liquidating without signaling to management that it needs to get rid of a large position. That makes the market worry that somebody knows something is wrong with the Decar story and is trying to lose a position without revealing their identity so that it can be done quickly. It wasn't helpful that director Jim Gilbert dumped a couple hundred thousand shares in September, though there probably is some reason unrelated to company fundamentals for the sales such as realizing that those cheap options exercised earlier in the year have deemed income tax consequences regardless what the stock is eventually sold at. Canadian listings are forced to withhold the calculated income tax when a Canadian resident exercises options, and given the nature of juniors and options such party will have to raise money from elsewhere and remit the wihtholding tax to the company before the exercise is executed. But those rules may not apply to a US resident though Uncle Sam will want his pound of flesh. Whatever the explanation, the market generally is ignorant about underlying realities and only contemplates the optics of an insider selling when everything supposedly is on track.

As far as I can tell everything is on track. Van drilling results are due before the end of the year, though at this point the market does not care if Van is better than Baptiste or not. The market will be able to ballpark tonnage footprint and grade estimates, but Martin Turenne has told me that the deposit needs at least another 5,000 m of drilling to achieve the drill density needed to support a 43-101 resource estimate.

An updated resource estimate for Baptiste is also expected, which may include cobalt grades, though that is likely contingent on the truly important milestone expected by the end of 2022, namely the results of a pilot plant study that involves converting 15-17 tonnes of Baptiste ore into 16-18 kg of ferro-nickel concentrate with at least 65% nickel as projected by the 2020 PEA flow-sheet. This milestone is important because no nickel deposit grading 0.1%-0.12% nickel DTR with awaruite as the primary nickel mineral has ever been commercially mined, nor has the PEA flow-sheet ever been applied to a nickel deposit. Metallurgy causes the eyes of retail investors to glaze over, but for parties such as producers who will make multi-billion dollar acquisition and development decisions they are critical. And in the case of FPX Nickel there is an alternative phalanx of backers in the form of car and battery makers eager for a secure supply of nickel sulphate and possibly cobalt sulphate whose origin also checks ESG boxes. They might not need nickel sulphate by 2030 when Decar might be in production, but they would certainly want to know that whatever they invested to help FPX Nickel with feasibility demonstration will at a minimum feed the stainless steel market.

If FPX Nickel achieves this pilot plant study milestone it will use the 16-18 kg of ferro-nickel concentrate for small scale hydrometallurgical studies as outlined in a recent scoping study to make battery grade nickel sulphate. The car and battery makers will be looking closely at the certified specifications of the resulting nickel and cobalt sulphates. FPX Nickel will of course be very interested in the implied cost of converting the concentrate into sulphates.

The validity of the flow-sheet aside, another market concern is the future price of nickel, which is currently around $10/lb, and what inflation has done to the CapEx and OpEx assumptions in the October 2020 PEA. To stress test the potential impact I have increased the CapEx and OpEx assumptions by 20% and run a DCF model using the PEA's ore schedule which does not assume any payability for the magnetite by-product or any premium for upgrading the ferro-nickel concentrate to battery grade sulphates that include cobalt. At the base case price of $7.75/lb nickel the after tax NPV per share ranges from $2-$10 per share for 10% and 5% discount rates. But at $9.96/lb that range jumps to $8.66-$21.65 per share. If you think $10/lb will be the new long term price for nickel and inflation will be back to 2% or lower as a result of quantitative tightening now trying to engineer a global recession, and you assume FPX Nickel will achieve its milestones, then it is clear why I regard it as a KRO Favorite with Good Speculative Value and a future buypout target in the $2-$5 range. The junior will have to raise more capital to deliver a PFS, but it will have $5 million working capital left by the end of 2022, which means it will not need to finance until the next set of milestones have been delivered. |

FPX Nickel Corp (FPX-V)

Favorite

Good Spec Value |

|

|

| Decar |

Canada - British Columbia |

6-Prefeasibility |

Ni |

FPX Selling Selling History of RBC and Coremark since July 1, 2021 |

AT NPV DCF Sensititivity Analysis of Decar 2020 PEA |

AT NPV DCF Sensititivity Analysis of Decar 2020 PEA with 20% CapEx & OpEx Escalation |

Long Term Nickel Price and Warehouse Stocks Chart |

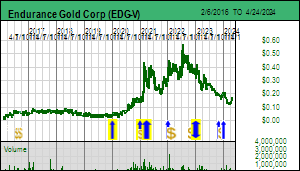

| Jim (0:22:37): Endurance Gold did something unusual last week, namely announced a financing at a premium to the market. How is that possible in the current market climate? |

In a market where brokerage firms are bullying juniors into doing deeply discounted bought deals, with the stock price subsequently ending up even lower as existing shareholders vomit with revulsion, it is very odd to see a $1.5 million private placement at a premium to the market with only a half warrant that not only has a term of just 2 years but whose exercise price is more than 50% above the stock price at the time the PP is announced. Endurance Gold is clearly not dealing with graduates from the Carlsbad School of full five year warrants who have been trained to invest only in losers that do nothing for the next five years before getting rolled back and given dumb names like "outcrop gold" as if there is anything of that sort left to be found on planet earth. Especially in a bear market where clients think brokers, analysts and newsletter writers are unusually endowed with stupidity. I suspect family offices already long EDG are adding to their positions, and newcomers, who have watched the company deliver positive fundamentals in 2022 without getting any market reward in the form of a higher stock price, are eager to pay up to get a position in a market whose existing shareholders are rather reluctant to sell any stock.

EDG doesn't have to finance right now but CEO Robert Boyd is a rather risk averse individual who likes to see money in the bank that he does need quite yet, even though he has released assays for 16 holes in 2022 that have greatly expanded the understanding of the mineralizing architecture at the Reliance gold project in southern British Columbia, and still has assays pending for at least 20 holes from the 8,000 m program that will arrive by the end of the year. Reliance can be drilled year round and it makes sense to resume in Q1 of 2023 rather than wait until late Q2 as has happened in previous years. Since optioning Reliance in late 2019 EDG has systematically built up its understanding of this orogenic gold system it hopes will prove a rival to the nearby depleted 4 million oz high grade Bralorne system. But it has not yet delivered that no-brainer barnburner intersection that tells the world Reliance is a multi-million ounce winner. That is why, in the bear market context, EDG is still limping along in the $0.35-$0.45 range it started out at the beginning of 2022, and which is why, much to my frustration, I have not been able to promote it from a Bottom-Fish Spec Value rated junior to a Good Spec Value rated KRO Favorite. But the company sure looks like a candidate for my 2023 KRO Favorites Collection.

EDG has had a busy week. After announcing the PP last week it announced an exploration agreement with the Bridge River Indian Band which outlines how EDG and the band will collaborate on various issues like archeaology and sensitive habitat in their traditional territory (much of which was obliterated long ago by BC Hydro's Carpenter Reservoir). I checked out their web site and discovered that this group has lots of business interests, and doesn't seem overly interested in the woke monster recommendation that they ditch the word "Indian" and rename themselves the Bridge River Indigenous Band. Somebody there probably felt it sounded too much like "Indigent". Instead I discovered they have renamed themselves the Xwisten people which makes me immediately think, oh no, images of "twisting in the wind" like shareholders of certain Canadian resource juniors whose management deals with its incompetence by rewarding everybody with a severe rollback. But apparently it is pronounced "hoist-in" which does exude a can do mentality unlike what one can detect in places like Moosonee where they celebrate traditional arts like trapping wild fur bearing animals so their pelts can adorn Putin Poodles hiding in Switzerland and blasting migrating birds out of the sky. No, the Xwisten sound like realists and it is good to see EDG work out an understanding with them that respects everybody's interests.

The other development was to option on reasonable terms the Sanchez claims adjoining to the east of the Olympic claims optioned earlier this year from Avino and recently made definitive. When you look at the map it is important to understand that the Bralone district from which 4 million ounces were mined at 15 g/t from a system of deep orogenic veins is part of a continuum that wraps around the Bendor Batholith to the northeast of Bralorne and south of the Reliance-Olympic-Sanchez land package. It is becoming clear that Boyd's understanding is scaling from an initial rethink of something he looked at during his Homestake days when a dowser controlled the Reliance story to a big picture vision that not only is the Royal-Treasure corridor a major gold system higher up in the orogenic model than Bralorne, as evidenced by the antimony rich nature of showings within his land package, but it repeats itself along the northern flank of the Bendor Batholith. Key to his vision is that past exploration has been hindered by the heavily forested mountainside and a blanket of ash from the very recent Meager Creek volcanic eruption. EDG's Reliance play is about to scale from chasing what appeared to be a limited scale high grade gold system into a major district play within a 10 km by 5 km area. |

Endurance Gold Corp (EDG-V)

Bottom-Fish Spec Value |

|

|

| Reliance |

Canada - British Columbia |

3-Discovery Delineation |

Au |

Map of Endurance Gold's Expanded Reliance Land Position |

Regional Geology Map for Bralorne-Reliance Area |

| Disclosure: JK owns Endurance Gold, FPX Nickel, Verde Agritech; FPX Nickel and Verde Agritech are Good Spec Value rated Favorites; Endurance is Bottom-Fish Spec Value rated |