Hello Guest User, You are visiting this website from a computer with an IP address of 172.69.58.40 with the name of '?' since Wed Apr 24, 2024 at 9:17:29 AM PT for approx. 0 minutes now.

Kaiser Media Watch Blog - November 1, 2022 to November 30, 2022

KRO Blog Overview

The KRO Blog is where unrestricted content of a time sensitive nature is posted. It includes the Kaiser Media Watch Blog which features content involving John Kaiser produced by third parties such as the Discovery Watch series by HoweStreet.com, interviews by outfits such as Investing News Network, SDLRC related commentary, the KRO Monthly Summaries, and just about anything else John writes that is not intended exclusively for the fee based KRO Membership.

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

This week's Kaiser Watch will be an overview of a 90 minute video presentation I gave to the Vancouver Kimberlite Cluster on November 16, 2022 on the topic "Why have investors lost interest in diamond exploration and what will it take to bring them back?" In the presentation I review the successes and disappointments of 3 decades of diamond exploration and address the 7 key obstacles that today discourage investor interest in diamond exploration.

While preparing this presentation I was able to remember many of the emotions I, subscribers and investors experienced as we followed various diamond plays during the past 3 decades. And I recognized a remarkable similarity with what I am experiencing today with Lithium Mania 2.0, the hunt for lithium enriched pegmatites which will deliver the second half of the ten-fold lithium supply expansion needed to make EV replacement of ICE cars a reality by 2035. Furthermore, the Great Pegmatite Hunt does not suffer from any of the 7 obstacles that discourage investors from betting on diamond exploration. I also realized that Lithium Mania 2.0 is only in the early awakening stage, equivalent to exactly 30 years ago December 1992, four months before the diamond boom inflected on the upside. In a sense my VKC presentation is my diamond swan song as I pass the torch to lithium pegmatites. To make it easier to digest the VKC presentation I have broken down the topic segments below.

Vancouver Kimberlite Cluster November 16, 2022: Why have investors lost interest in diamond exploration and what will it take to bring them back?

Younger Generation Obstacle: knowledge barrier and rules that prevent non-millionaires from participating in private placements, the primary funding mechanism for resource juniors

The Vancouver Kimberlite Cluster is a seminar series sponsored by the University of British Columbia and SRK Consulting started in 2012 which presents a talk every one or two months on a topic related to diamond exploration. It used to be held in downtown Vancouver with a visit to a pub afterwards where participants could loosen up and say what they really think. Since Covid hit in early 2020 it has been a virtual event, which isn't as much fun after the main presentation and recorded Q&A, but it does allow people from around the world to plug in to the live event and participate in the subsequent Q&A. The presentations are posted on YouTube and you can access past events through the VKC Web Site.

Normally the presentations are done by technical people and academics, but UBC's Dr. Maya Kopylova, a diamond expert, asked me to do a presentation from the perspective of a market analyst who has closely followed the diamond exploration sector for the past three decades. Back in the nineties the Ekati discovery by Dia Met in the Canadian Arctic unleashed a tremendous exploration boom that went global and involved hundreds of juniors. Today there are less than a dozen still engaged in diamond exploration and they have a hard time raising capital and attracting investors.

Dia Met's brief Nov 5, 1991 News Release launched a 3 decade Global Diamond Exploration Boom

The Global Kimberlite Map as of 2010

Jim (0:04:05): In your presentation you contrast two diamond juniors, Arctic Star Exploration Corp and Craton Minerals. Why did you focus on these two companies?

Buddy Doyle's Arctic Star and Brooke Clements' Craton Minerals represent opposite ends of the exploration spectrum.

Craton Minerals, which is still private, is engaged in grassroots exploration in one of the few areas of North America which is prospective for diamondiferous kimberlites but has seen very little exploration. The reason is that this region does not have a sampling medium that allows regional exploration for indicator minerals which tell you that kimberlites which sampled the diamond stability field are waiting to be found. Craton has to rely on stream sediment sampling to generate peripheral clues and geophysical surveys to generate drill targets. Looking for kimberlite pipes, clusters and even fields through grassroots exploration was what drove the first two decades of diamond exploration. The problem 3 decades later is that this exploration wave was quite successful and while it is always possible to discover new kimberlites within known fields or clusters, finding a brand new cluster with world class scale potential in North America is doubtful except in areas like the Western Superior Craton. But back in the nineties the discovery potential in Canada was wide open. Only De Beers had made a serious earlier effort which included discovery of the Fort a la Corne and Attawapiskat kimberlite fields though nothing had resulted in a Canadian diamond mine. Ironically, the limitations of De Beers' own early assessment tools, micro diamond analysis and pyrope chemistry, delayed recognition of Victor's diamond potential. Brooke Clements has spent his career in diamond exploration and provided the VKC Dec 3, 2020 Presentation: Diamond exploration in COVID-19 times: challenges and opportunities which is an excellent tour of the past 3 decades of diamond exploration from the perspective of a diamond geologist.

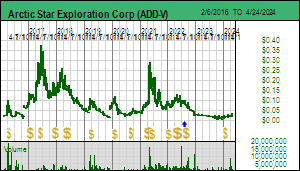

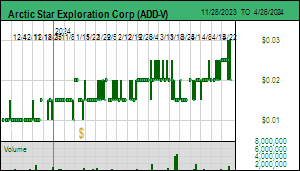

Arctic Star is a public company which I featured as part of my September emerging discovery MIF session. About 5 years ago Arctic Star staked the Hardy Lake block next to Ekati and Diavik which De Beers dropped after holding it for more than 2 decades. De Beers discovered a couple dozen kimberlites within the first decade of Ekati's discovery using a combination of indicator mineral sampling and geophysical surveys. Many of the pipes were diamondiferous but De Beers did not see the scale needed for a standalone diamond mine and never took any of these kimberlites to the mini bulk sampling for grade stage. Apart from the location of the kimberlites De Beers has not shared any of the data generated by its exploration effort, which is a terrible shame. When the claims came open in 2016 Arctic Star grabbed them with the goal of demonstrating that there are kimberlites present which could become future feed for the Ekati and Diavik mines which are threatened with depletion within a decade or so. The strategy is to rethink the Diagras project in two ways: use newer geophysical methods to find pipes De Beers missed, and revisit some of the existing pipes which might me better than De Beers thought, or at least good enough to feed Ekati or Diavik. Part of the rethink strategy is the potential for high value gem diamonds within lower grade pipes.

Arctic Star has already been successful in finding 5 new kimberlites, one of which, Sequoia has yielded micro diamond results that suggest a macro grade in the 20-60 cpht range. It also appears to have a decent size. During Q2 of 2022 Arctic Star drilled additional holes to further delineate this body and beef up the micro diamond profile. The first step will be to confirm macro grade through mini bulk sampling. But the most important challenge will be to establish carat value. The problem with diamond pipes is that the lower the macro grade, the larger and thus more expensive a bulk sample you will need to get a representative parcel of diamonds. Arctic Star may also revisit the Finley pipe discovered by De Beers and on which it did the most work, though not enough to establish carat value.

The poster child for this rethink approach is Lucara's Karowe kimberlite in Botswana which De Beers discovered and named AK6 but discarded because it was small and low grade compared to the nearby giant Orapa pipe. Karowe ended up producing big and valuable type IIa diamonds such as Lesedi da Rona. Recent work by the GIA's Dr. Evan Smith suggests that these type IIa diamonds form deeper in the mantle and are unrelated to the peridotitic and eclogitic diamond populations which a kimberlite magma entrains and which represent the bulk of a diamond mine's output. His VKC February 27, 2019 Presentation: Origin of Type II diamonds and their super-deep genesis provides an excellent overview. In a recent VKC presentation Andy Moore made the case that the big diamonds with evidence of having formed spotaneously within a super deep metallic melt are only a fraction of the large gem quality diamonds that have been recovered. Dr. Andy Moore believes many of these "big diamonds" formed fairly quickly within the deeper portion of the lithosphere, possibly triggered by an approaching kimberlite magma which itself is not a source of diamonds. He provided the VKC October 5, 2022 Presentation: Framesite and CLIPPIR Type II diamonds - a link to the megacryst suite. This is not a trivial question because if Type IIa diamonds only form super-deep within the mantle courtesy of subducted ocean slab, the places where they might show up in a kimberlite with any meaningful abundance will be very few. But if they form in association with an eclogitic megacryst setting, which, unlike the peridotitic megacryst that features the G10/G9 pyrope garnets everybody has heard about, was also fed by subducted ocean slab, the locations where you might find Type IIa diamonds in meaningful abundance would be much more widespread. A lot of diamond experts are trying to figure out where and how such diamonds are formed, and whether there are any clues within a kimberlite's rock chemistry that point to the presence of Type IIa diamonds.

Two Diamond Story Paths: Craton Minerals Grassroots and Arctic Star Rethink

Arctic Star's Rethink of De Beers' Hardy Lake

Lucara's Karowe Mine discarded by De Beers as AK6 is the Rethink Poster Child

The Quest for Big Diamonds

Jim (0:13:30): What is the main message of your VKC presentation?

The main message of my VKC presentation is that investors are not interested in betting on a new kimberlite field or cluster discovery because of the long and expensive timeline needed to demonstrate economic value which always requires bulk sampling. If the juniors are to attract investor interest they need to revisit existing kimberlites and build a case why although not high grade they may have high value. A curse that seems to afflict Canada is that the combination which makes Jwaneng world class - high grade, high value carats and large tonnage - never happens. It's as if Canadian pipes can only have two of these features like the "fast, cheap and good" curse of IT solutions. My presentation walks through various kinds of diamond disappointments experienced by investors.

The heartbreaker was the Chidliak field on Baffin Island whose discovery benefited from sound exploration methods including indicator mineral chemistry and micro diamond analysis. This resulted in high grade kimberlites with high value diamonds but small tonnage, with the result that a project with an after-tax NPV of $450 million was acquired by De Beers for $110 million, a little more than Peregrine Diamonds and its partners had spent bringing the project through the PEA stage with bulk sample supported carat values. Because the historical exploration bias was towards high grade pipes, not much effort was invested in kimberlites that early on showed low grade potential. The future opportunity for juniors lies in revisiting large, lower grade pipes which have never been assessed for carat value. What is missing is a coherent argument based on micro diamond data and indicator mineral chemistry as to why high value diamonds may be present. This is the challenge that the exploration and academic community must overcome in order to bring investor interest back to diamond exploration.

Reasons why investors are not interested in diamond plays

Reasons why investors are interested in lithium plays

Jim (0:16:55): At the start of your presentation you talk about the Sheahan Diamond Literature Reference Compilation. What is that all about?

The Sheahan Diamond Literature Reference Compilation is the work of Patricia Sheahan who has spent the last 4 decades documenting every technical article relevant to diamonds, news releases by companies engaged in diamond exploration, and media articles about diamonds. She would assemble them into a monthly publication which she initially mailed for a fee, but when the Internet came along she emailed it as a free pdf to a list of about 400 people from around the world interested in diamond exploration. In 2015 I approached her with the idea of migrating all this information stashed away in excel spreadsheets into a relational database and post it online. It was a huge amount of work involving over 100,000 references but it is now available on KaiserResearch.com in the Diamond Resource Center which is free to the public.

You can check out everything published in each year. You can look up the references by individual author to see what he or she has published. You can look up references based on key words such as indicator minerals. And you can look up references by regions. If anybody wants to write a book about the past 40 years of diamond exploration everything is there. Stockwatch has all the news releases and Sedar, the government repository for regulatory filings, is a treasure trove of technical reports.

Pat also organized the March PDAC 1993 diamond short course which was hugely popular with resource junior geologists who literally knew nothing about diamonds other than that they were pretty and expensive. She also organized each year's PDAC diamond technical session, all of which I attended during the past 3 decades to learn the latest about the diamond industry. Unfortunately Pat learned in May that she has terminal cancer and is unable to continue the monthly reference compilation or run the next PDAC diamond technical session. My web site has a Collection of Tributes written by diamond exploration people which reveal what a vast impact Pat Sheahan has had on the diamond exploration sector. If PDAC were to ever consider somebody for its Mining Hall of Fame that wasn't a mine finder or builder Patricia Sheahan would be a perfect candidate.

The Sheahan Diamond Literature Reference Compilation

Jim (0:22:03): Your first reason why investors have lost interest in diamond exploration is that there are limited story paths for rethink plays. What do you mean by that?

Although I am best known as a resource junior bottom-fisher, what I really am is a story hunter. Yes, capital, structure and people are important, but the path to success is the value creation story. I use my KRO Search Engine to screen for capital, structure and people, but to figure out a junior's story you have to dig into the company's web site, corporate presentation and news releases. My four decades covering the exploration sector has given me an intuitive feel for the range of stories that answer the basic question: what are you doing differently from others before you that will be your path to fundamental success understood as a future mine? The simplest story path which is also the beginning for all other story paths is grassroots exploration, using various exploration methods to discover new deposits. Ekati was found in this manner. Almost the entire Canadian diamond exploration history of the past 3 decades was of this nature. It is what made diamond exploration exciting for investors during the 1990s and 2000s. But it has also created a sense that very little of world class scale remains to be found, at least in Canada. Angola, because it was trapped in a multi-decade civil war, is perhaps the only bluesky exploration frontier left in the world. But it is a difficult place for resource juniors to succeed because of Angola's history of corruption. Canada has, of course, been hit hard with grassroots exploration for over a century and while it is harder to make world class discoveries, that doesn't stop juniors from trying and attracting investors to precious and base metal plays, and these days also critical metals such as rare earths and lithium.

Earlier this year I created a visual story path template to make it easier to recognize the story paths juniors are pursuing. Most of the 100 plus resource junior buyouts during the China super cycle that ran from 2003 to 2013 were based on a rethinking of an existing deposit discovered in past exploration cycles and never developed for a variety of reasons, chief among which was that they were not economic at prevailing metal prices. The rise of China into the world's second biggest economy boosted metal demand by an order of magnitude, and after decades of declining real prices the resource sector experienced substantial real price gains that dragged many of these forgotten deposits into the money. The resource juniors, which used to be focused mainly on discovery exploration, expanded into feasibility demonstration. This so called Lumina model of a rethink play has not worked very well during the past decade as metal price trends flattened or retreated.

A more popular story path during the past decade is to rethink a mineralized system to see if it is bigger and better than previously understood. New geological concepts and exploration tools such as deeper penetrating geophysical surveys plus digital compilations are keys to success for these rethink style story paths. There is no shortage of such stories resource juniors can come up with and it is the investor's job to assess their plausibility.

The problem with diamond exploration is that kimberlites are mini volcanoes that exist as discrete deposits. Often they have internal complexity created by multiple eruptive phases. Dykes and sills are more like vein deposits except that like pipes there is no zonation nor are there any structural traps for concentrating metals from fluid flow.

Although diamond prices have increased over time, they are largely tracking inflation with demand following macro-economic trends. Gem diamonds have only one usage and that is vulnerable to fashion trends and increasingly ESG concerns which turn lab grown diamonds into cheaper competition. If a diamondiferous kimberlite has already been assessed as marginal, there really isn't an optionality play on dramatically higher real prices. Gold benefits from the dream that financial crises will dramatically expand ownership demand and raise real prices. Base metals like copper and nickel face expanded demand from an entirely new usage such as the electrification of the transportation sector driven by climate change policy.

The story path of looking deeper or along trend of an existing mineralized system for something better makes no sense for a known marginal kimberlite. You can explore for brand new pipes within a cluster, as Arctic Star is doing with its Diagras project, but you are not going to find a Jwaneng scale pipe because De Beers would not have missed it when it explored the Hardy Lake block. And while dykes may not have made it to the surface, all pipes did, and those that have been buried by younger sediments or volcanic flows are nearly impossible to find and certainly not with the help of indicator mineral chemistry.

One story path available for other metal deposits involves metallurgy, often a reason a deposit proved sub-economic. Coming up with a new processing flow-sheet can be a story path to success. The only rethink style story path for a kimberlite is the one demonstrated by Lucara for the Karowe pipe, namely demonstrating that the value of the diamond content is higher than previously assessed. Diamonds are unique in this regard because their value is based on the 4 Cs: color, clarity, carat weight and cut (crystal shape). Crush a 100 carat type IIa diamond and the total value of the pieces will be a fraction of the original stone's value. Because a kimberlite's diamond content can be a blend of unrelated diamond populations formed at different depths it is difficult to predict from micro diamonds or indicator mineral chemistry how the quality and size of considerably rarer high value diamonds will behave without the results of a bulk sample.

The rethink story path for a large, low grade diamond deposit is available, but a plausible argument that justifies the expense of a bulk sample does not exist. The argument that you cannot be sure type IIa diamonds aren't present until you spend the money on a bulk sample does not interest investors. If the academic community could develop a way to predict the "big diamond" potential from the kimberlite's rock chemistry, the rethink story path would become available to resource juniors. Chuck Fipke claims he has developed a method to predict "big diamond" potential based on kimberlite chemistry but he has not shared the basis for this claim. One has to ask, if his method is valid, why has his post-Dia Met diamond exploration vehicle Metalex accomplished nothing of value during the past two decades?

Dia Met's Ekati grassroots story path to success

Arctic Star's Digras proposed story path to success

Jim (0:27:11): Does lithium share this rethink story path obstacle?

Every story path is available for lithium pegmatites. What people generally do not know is that the rough diamond market was worth $6-$8 billion during the 1990s when the Canadian diamond boom started, and in 2021 had only grown to $14 billion. The uranium market was worth only $4-$5 billion in 2021 but it most of the story paths are available for uranium juniors. In 2015 when Lithium Mania 1.0 erupted as the market began to take electric vehicles seriously the lithium market was worth less than $1 billion. Prior to 2005 its annual value was only $100-$200 million because its usage was mainly for the glassware and ceramics sector. But in 2021 the world's lithium supply of about 100,000 tonnes metal was worth $18 billion at the average price of $15/lb lithium carbonate and with the price double that this year its value will have swollen to $40 billion. Various groups like Rio Tinto predict that annual lithium supply will have to grow ten-fold if policy goals of replacing ICE car sales with EV sales by 2035 are to be achieved. Those projections assume that the holy grail of a solid state electrolyte that allows lithium metal to substitute for graphite in the anode to make the lithium ion battery truly good will never happen. The current lithium price is not sustainable for the simple reason that EVs will never become affordable for the masses. But a long term price range of $10-$15/lb lithium carbonate, which is needed to justify mining hardrock lithium, suggests a future lithium market worth $100-$200 billion. That is huge, putting lithium in the same league as copper, gold and aluminum.

This emerging monster change allows resource juniors to embrace both grassroots and existing system rethink story paths. Numerous LCT type pegmatites have been documented over the decades as a by-product of exploration for other metals in places. Until recently nobody has ever explored specifically for new LCT pegmatites because the market was tiny and readily supplied by the giant Greenbushes deposit in Australia and the brine salars in Chile. Lithium Mania 1.0 involved grabbing and advancing the known pegmatites at which Australian juniors proved particularly adept, in fact so much so that their supply helped crash the lithium carbonate price below $3/lb in 2018.

In 2021 EV demand caught up and surpassed lithium supply, driving the lithium price up ten-fold. Now the carmakers have gone beyond the point of no return with their EV plans, and policy mandates in places like California and Europe have been cemented. Hundreds of billion dollars are being invested in gigafactories and even lithium refineries for converting spodumene concentrates into battery grade lithium chemicals. But only now are car and battery makers waking up to the problem of where the lithium feedstock is going to come from. You can zone and build a gigafactory or refinery within two years, but discovering a new deposit and turning it into a mine requires at least ten years. An intense urgency is building about future lithium mine supply. Even if we suffer a nasty recession next year which dampens precious and base metal prices, extending the current bear market for juniors, the lithium supply problem will be unaffected and Lithium Mania 2.0 will attract investors who get the story. Grassroots exploration within pegmatite trends and the rethinking of known pegmatites are equally valid story paths to success.

The recent and anticipated growth of lithium demand is staggering

Jim (0:35:16): Why are long timelines for the exploration-development cycle a problem for diamond plays but not lithium plays?

Diamond projects have long timelines for two reasons. One is the nature of diamond deposit evaluation which does not deliver an indication of economic value until the stage where a junior with almost any other metal deposit is already doing cost discovery in the form of economic studies such as a PEA. The other is that government agencies do not feel any urgency in timely approval of a new diamond mine. Diamonds are not perceived as essential for anything other than generating revenues. Lithium exploration reveals the size of the prize with the first few drill holes. The rock value isn't as easy to calculate as it is with a gold or copper intersection, but investors will soon enough figure out how to do it. Eyeballing the tonnage footprint of a pegmatite will be a lot easier than trying to figure out the tonnage potential of a high grade gold system. Pegmatites have shapes ranging from narrow parallel dykes to fairly wide elongated bodies. The latter are preferable to support open pit mining. Compared to sulphide metal deposits pegmatites are environmentally benign.

Grades of 1% Li2O or higher have a rock value of $545/tonne at $10/lb lithium carbonate and $1,636 at $30/lb. That's equivalent to a gold grade ranging from a third of an ounce to one ounce per tonne. Where is a junior going to come up with a 100 m intersection grading 1 opt gold? It is possible that lithium carbonate prices rise higher in the interim while new lithium supply is not yet matching demand growth, and that will make investors crazy. Lithium pegmatites can be turned into a resource estimate within a year, during which metallurgical studies can also be done because they outcrop or are close to surface. Governments recognize the urgency of the lithium supply problem in the context of climate change and are not going to let their permitting bodies drag out the permitting cycle just because they can. The window to identify the future mines is the next 3 years, with economic studies and permitting unfolding 2025-2028, and mine construction in 2028-2030 so that the lithium supply is available when EV demand goes exponential in the 2030s. As they say where there is a government will there is a permitting way.

Jim (0:38:12): Why are micro diamonds and indicator mineral chemistry unreliable in assessing diamond targets? What tools are available for assessing pegmatite targets?

Pegmatites are spawned like magmatic missiles from granitoids in a continental collision setting. During the mini magma's journey something called fractionation takes place, which is the concentration of certain elements within the magma. Pegmatites that chill close to the granite source tend to be barren with just background levels of critical elements. But as they travel abroad from the granite source they become enriched. There are various types of enriched pegmatites but the one of interest to the lithium sector are the LCT type, which stands for lithium-cesium-tantalum enrichment. The pegmatite magma cools slowly which allows big crystals to form, of which the most common minerals are spodumene, petalite and lepidolite. These minerals need to be processed into a concentrate which must then be cracked to liberate the lithium, similar to what needs to be done with rare earths. Petalite is the lithium mineral historically mined because it has a higher purity than spodumene which makers of glassware and ceramics prefer. But a petalite concentrate hits a maximum of about 3.5% lithium compared to 5%-6% for spodumene which is why spodumene concentrates are preferred by refineries that convert concentrates into battery grade lithium hydroxide or carbonate.

The lithium grade of a pegmatite is measured by assaying drill core. Because lithium's value resides in its elemental properties the physical form in a deposit is irrelevant except in terms of the cost to extract and purify the lithium. Because pegmatites consist of quartz and feldspar they do not show up in geophysical surveys though when they outcrop they are visually very distinctive. Pegmatites that are not exposed are difficult to develop as targets. When a company talks about doing geophysical surveys the goal is to identify structures which formed paths of least resistance along which the pegmatite magma traveled and crystallized within. While pegmatite bodies are visually distinct from the surrounding country rock, this does not tell you if they are LCT enriched. Assaying a rock sample will provide a grade, but that can take 8-12 weeks.

Geologists consequently use an XRF unit to read the X-ray fluorescence generated by the various elements in a rock. This portable "gun" costs about $50,000 and is very useful for assessing base metal grades. It does not work for gold, nor for lithium. However, rubidium, which has very few commercial uses, is always present in LCT pegmatites and its presence can be detected with an XRF gun. Field geologists use the XRF gun to prioritize pegmatites for sample collection. If assays indicate a decent Li2O grade, ideally 1% or higher, and the pegmatite body appears to have decent tonnage potential, ideally 5 million tonnes or higher, then it becomes a drill target. The lithium assays tell you very quickly whether you have a development candidate.

While pegmatites tend to be harder than the country rock, they can be covered by swamp, overburden and vegetation. In glaciated terrains, such as Canada, the pegmatite will have been eroded by the ice sheets and theoretically there should be pathfinder elements that till sampling can identify and trace back to the source. However, lithium crystals don't travel far before breaking down and diluting to background levels. Rubidium, however, will show up in lake bottom sediments at elevated levels at quite a distance from an enriched pegmatite, and geologists can use this data to ballpark the general source area for LCT type pegmatites. But at the end of the day it is all about drilling and assaying.

Kimberlites form as magmas in the mantle. As they work their way through the lithosphere towards the earth's surface where the magma either chills out as a dyke or erupts as a mini volcano, the magma will encounter diamonds that form in various parts of the diamond stability field which is a combination of pressure and temperature that allows carbon to crystallize into a diamond with an octahedral crystal structure rather than form graphite with a hexagonal crystal. Sometimes the diamonds grow around other mineral crystals which we call inclusions. Scientists extract these inclusions and document their chemistry. The two most important inclusion types are pyrope garnets better known as G9s and G10s which are associated with peridotitic diamond populations, and eclogitic garnets associated with eclogitic diamond populations which exhibit a carbon isotope formed only when exposed to sunlight. Through careful studies led by people such as John Gurney the diamond sector has been able to establish which garnet chemistry only forms under the same conditions that foster diamond formation. But while indicator mineral chemistry will tell you that a kimberlite magma sampled a part of the lithosphere favorable for diamond formation, it cannot tell you whether diamonds were present, what their quality might be, nor how much was entrained by the magma. Furthermore, diamonds with an eclogitic paragenesis will have formed at a different depth than those with a peridotitic paragenesis, but the kimberlite magma may have picked up both populations and mixed them.

Once a kimberlite is discovered the next step is to assess the micro diamond content which involves dissolving the kimberlite sample with caustic fusion which leaves behind the diamonds and other heavy minerals. The diamonds have to be picked out of this concentrate and then they are measured through a sieve system. Diamond crystal abundance has a lognormal distribution which means there are a hell of a lot more tiny diamonds than diamonds big enough to cut and polish for setting in a piece of jewelry. During the first decade of the diamond boom juniors reported micro diamonds as micro and macro counts based a 0.5 mm measurement in the longest dimension. This was nonsense started by Dia Met and copied by everybody else even though there is no scientific basis for predicting macro grade on the basis of an arbitrary 0.5 mm distinction. The Torrie pipe was the first of many macro-micro based disappointments generated by this disclosure method. The controversy over Winspear's Snap Lake dyke in 2000 coincided with the arrival of a new square mesh sieve based reporting standard that CIM formalized in 2003. Snap Lake proved to be high grade in the 150-200 cpht range which was established by bulk sampling. Winspear never reported micro diamond results using this standard, but when Diamondex was spun out to hold the down dip extension of the dyke on the King property and it drilled a deep hole, we did get a micro diamond curve that shows what a high grade kimberlite should look like.

Today the term "macro" diamond is only used to refer to diamonds large enough to be cut, polished and set in jewelry. Only a very high grade kimberlite will yield micro diamonds that qualify as macro diamonds caught by a 1.18 mm sieve unless the sample is in excess of 1,000 kg, far more than a typical kimberlite drill intersection weighs. There are complex calculations for projecting the macro grade from micro diamond distributions but I use a simple system where I normalize the counts per sieve to a per tonne basis and plot them on a log scale against the sieve sizes. Since 2003 when CIM formalized the guideline for reporting micro diamond results I have been able to build a database of micro diamond curves for kimberlites whose macro grade has been established by at least mini bulk sampling. In principle, the higher and flatter the curve, the higher your grade will be. But there are lots of things that can go wrong with this approach. One is that for lower grade kimberlites the sample tested may not be large enough. In some cases the micro diamonds are depleted, which almost caused De Beers to overlook the Victor pipe which turned out to be large with a 25 cpht grade and high value diamonds. The worst part about micro-diamond based grade projections is that it is not enough to allow you to calculate rock value as you can with a lithium pegmatite.

Original micro-macro distinction based on 0.5 mm in longest dimension was worthless

Winspear's Snap Lake marked the transition to a new micro diamond reporting standard

The CIM Micro-Diamond Reporting Guidelines became official January 1, 2003

Jim (0:46:13): What is an S-Curve and why does it happen at a later stage for diamond plays than for other metals such as lithium?

(Jim's question and the start of my response is missing from the audio). Investors love discovery focused resource juniors because they typically start with a low valuation, but if they pull a discovery hole that justifies advancing the target to the discovery delineation stage, the stock's value can expand 5, 10, or even 100 times very rapidly. I call this S-Curve action and it has also been called the Lassonde Curve. The exploration-development cycle involves 9 stages from grassroots through production. My rational speculation model assigns an uncertainty range for each stage. As exploration moves a project through the various stages the uncertainty about what the outcome will look like and be worth diminishes. The market's ability to dream fades away and market valuation reverts to the betting principle that what you should pay now is the certainty of an expected outcome multiplied by the value of that expected outcome. But during the early stages of a new discovery the market does not know what the limits of the outcome will be.

With a typical metal discovery, and this includes lithium, you can calculate the rock value of a discovery hole by multiplying the grades by the metal prices that you can look up. You can then do a tonnage footprint guess by calculating the volume represented crudely by length times width times thickness in metres, and then multiplying the volume by the specific gravity which is 2.6 for a typical host rock like granite or 4.0 if it is a massive sulphide zone. There is lots of information about the cost of building and operating a mine published through other companies' economic studies, so it is possible for non-engineers like myself to create an outcome visualization.

An OV is a simple life of mine discounted cash flow model that generates an after-tax net present value. I then multiply that potential outcome by the uncertainty range for the stage of the project to get a fair value range for the discovery. At the discovery delineation stage that certainty range is only 2.5%-5.0%, so if you think you have hooked a prize with a $1 billion size, the implied project value should be in the $25-$50 million range for the stock price to represent fair speculative value. If the stock started with a $5-$10 million implied value, that means the discovery will have handed you a very quick 5-10 bagger gain. But S-Curve action is even better. Until the limits of the discovery are known, under the right market conditions investors may speculative that the size of the prize could be $10 billion. So the stock may reach a $1 billion implied value during discovery delineation.

Strangely, what I have observed in the case of what turns out to be a valuable mine, is that the future value eventually established by the entire exploration-development cycle will have been reached by the S-Curve peak valuation during the discovery stage. The lithium pegmatite hunt is primed for S-curve market dynamics because at current lithium carbonate prices the rock value of a 1% Li2O plus grade is very high, pegmatites will be open-pit mined, and while you can see some of the dimensions at surface, usually there is room to imagine that there is a lot more beneath the surface. And there are enough economic studies for Canadian lithium pegmatite projects to allow me to construct an outcome visualization.

Unfortunately, this does not work for diamond plays because during the discovery delineation stage you may get tonnage and projected macro grade, but the carat value will not be known until after stage 4 is completed. With metal deposits stage four involves infill drilling to support a resource estimate and preliminary metallurgical studies to support a PEA in stage 5. With a diamond discovery the junior spends stage 4 conducting mini-bulk samples to convert macro grades projected from micro diamond data into measured macro grade. This level of bulk sampling does not yield enough diamonds to allow a meaningful assessment of carat value. That comes in stage 5 when a large and expensive bulk sample is extracted to yield a parcel of diamonds big enough to allow valuation.

During the 1990s diamond plays experienced S-Curve market action during the kimberlite discovery stage based on indicator mineral chemistry and micro diamond results. Today investors know better and are unwilling to engage in S-Curve style speculation until some understanding of grade and carat value has been achieved. Because it is so expensive both in cost and time to establish the carat value of a new diamond bearing kimberlite discovery, the diamond juniors gets stuck on a dilution treadmill because the stock price does not rise. This deferral of S-Curve dynamics is the biggest reason investors have lost interest in diamond exploration plays.

Dia Met's Ekati experienced S-Curve action much earlier than it would today

The Rational Speculation Model and S-Curve Dynamic for most metal plays

Today S-Curve is not possible for diamond plays until stage 5 when carat value is established

S-Curve contrast between a diamond and precious-base metals play

Jim (0:52:22): Why is there diminished discovery potential for new kimberlite fields but not pegmatite fields?

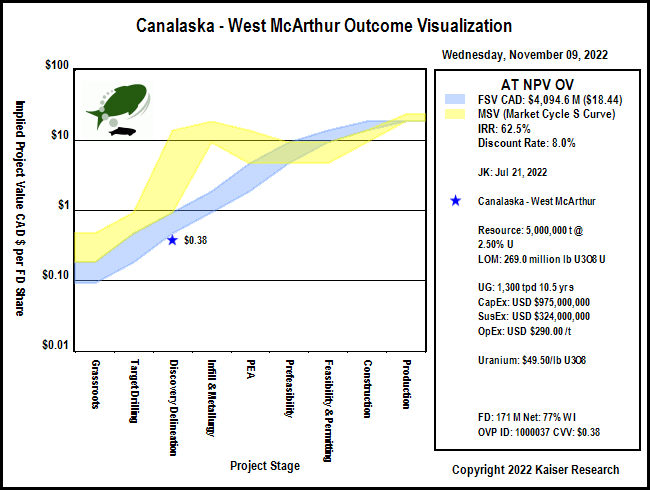

Since the Ekati discovery in 1991 billions have been spent exploring Canada's cratons using till sampling in glaciated terrains or testing geophysical targets in places like Alberta's Buffalo Hills and Saskatchewan's Fort a la Corne region. The best discoveries have been developed as mines. Some have failed. Some like Victor were depleted. And the two biggest operations, Ekati and Diavik, are facing depletion and reclamation within a decade unless brownfield exploration reveals new development candidates. There are few places left to look for a new kimberlite field or cluster that might contain a Jwaneng scale kimberlite. Exploration is limited to poking around within known clusters for pipes that may have been overlooked, or perhaps revisiting known kimberlites with low grade implications. The Chidliak experience has taught Canadian investors that finding high grade kimberlites is not good enough if tonnage is small. I think a revival for rethinking lower grade kimberlites with the goal of demonstrating that they contain high value "big diamonds" is possible, but what is still missing is an early stage, low cost argument as to why a low grade kimberlite might contain high value diamonds.

The opposite is the case for lithium pegmatites which occur in settings similar to where kimberlites occur. Lithium pegmatites were geological curiousities because the lithium market was tiny for decades compared to the diamond market. But the shift to electric vehicles is changing the lithium market dramatically. Not only is every known pegmatite being revisited to see if it is LCT type, but exploration is now surging in areas that are prospective for LCT enriched pegmatite fields. For example, take southern Finland. Pegmatites were quarried for feldspar and never considered as lithium mines. All that is changing and fleet-footed resource juniors like Brunswick Exploration are going to become champions.

The economic reward for shareholders broke the diamond exploration market's heart

What is left to keep Canada in the diamond production game?

Jim (0:55:14): How does title risk in exploration frontiers differ between diamonds and lithium?

Canada no longer qualifies as a major diamond exploration frontier. Russia could qualify but not even De Beers can operate in Russia. During the first decade of the diamond boom a junior called Archangel Diamonds discovered the Grib pipe in the Archangel region just east of Finland. It was large, high grade and had high value diamonds. De Beers invested over $35 million in Archangel in order to assess the Grib discovery. At the end of the day the 49% interest to which Archangel was entitled was simply never transferred. An oil producer called Lukoil ended up owning the Grib pipe. Angola is the best remaining diamond exploration frontier because during the first two decades of the global diamond exploration boom it was trapped in a civil war. That war is over, but Angola is also among the most corrupt African nations. Lucapa has dared to explore in Angola, but for most resource juniors Angola has too much title risk.

Exploration of lithium pegmatite fields is a frontier in its own right, and the best potential is in secure jurisdictions like Australia, Brazil, Canada and Scandinavia. The biggest risk will be in the form of NIMBY and First Nations opposition.

Archangel's Grib Discovery - Large, High Grade & High Value - was stolen by Putin's Russia

True diamond exploration frontiers like Angola are too risky for resource juniors

Lithium Pegmatite Exploration Frontiers are most in low title risk jurisdictions

Jim (0:58:14): Why do diamonds raise ethical concerns but not lithium?

Civil war during the nineties in places like Sierra Leone and Angola was bankrolled by rebels through the mining of alluvial deposits with forced labor. Initially called conflict diamonds, these illegally mined diamonds became a marketing nightmare for the diamond sector when they were rebranded as blood diamonds by the likes of Leonard DiCaprio. The Kimberley Process was established to allow differentiation of properly mined diamonds from conflict diamonds so that consumers could be confident their purchases were not supporting brutal conflicts.

More recently, however, the ESG movement has turned its attention to the carbon footprint of mining in general. There is plenty of anti-mining hand wringing about future lithium mines, but because lithium is essential to the new generation of electric vehicles, one has to accept tradeoffs. As one article recently pointed out, why should we fret about future small open pit lithium mines when the future tradeoff of climate change mitigation is the elimination of open pit mining. Mining companies are making an effort to reduce their carbon footprint and this includes diamond mining.

However, diamond mines have a problem because natural gem diamonds are not essential to the world's future. One can argue that diamond mines in many parts of the world support local communities. What would Botswana be like without its Orapa and Jwaneng diamond revenue? The threat to diamond exploration comes from the emergence of lab grown diamonds where chemical vapor deposition technology allows gem quality diamonds to be manufactured from basic carbon sources. The younger generations, in so far that they are interested in the cosmetic aspect of diamond jewelry, are quite happy buying cheaper lab grown diamonds. Investing in diamond exploration for future mines that will likely have a carbon footprint makes no sense to them. But investing in lithium exploration so that there is adequate future lithium supply to replace ICE car sales with EV sales makes a lot of sense. And betting on the next big lithium discovery as a way to make a lot of money while helping save the planet has to be much more attractive than betting on the greater fool scam called crypto.

Ethical concerns have shifted from conflict diamonds to the carbon footprint of mined natural diamonds

Only a dozen juniors still engaged in diamond exploration

More than a hundred juniors exploring for lithium and the list grows every day

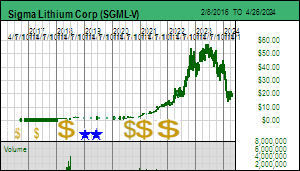

Sigma Lithium and Brunswick Exploration at opposite ends of the exploration-development cycle

Lithium Mania 2.0 with its focus on the Pegmatite Hunt is on the verge of inflecting

Disclosure: JK owns Brunswick Exploration; Arctic Star and Brunswick are Bottom-Fish Spec Value rated

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch November 18, 2022: Why is Twitter good for Resource Juniors?

Jim (0:00:00): Will Elon Musk's ownership of Twitter change how you use Twitter?

The Twitter controversy is mainly about how it is used to spread mis-information and hate, and to what extent Twitter should try to moderate the worst abuses. It is possible that under Elon Musk Twitter could become a free for all that channels online and physical harm at people. But Twitter is also used by dissidents to push information into the public domain which has made abusive governments like Iran very unhappy and eager for access to the actual identities of such people. Elon's quest for cash flow may require accommodating the demands of thug governments. Twitter could see a big drop in membership usage. But none of that affects me because I only use Twitter Kaiser Research as a notification system. The public can choose to follow or unfollow me at its leisure.

When I publish a Kaiser Watch Episode I also create an unrestricted blog comment on my KaiserResearch.com web site which includes links to its location on YouTube. I include written comments and graphics with the blog comment to illustrate the audio version on YouTube. It is also set up so that if somebody is just interested in the Bell Copper question they can click on the YouTube link and start the audio at Bell Copper. I then tweet a link to the latest KW Blog comment which alerts my followers that the latest KW is available. This brings them to my web site which does not require blue check verification. I use Twitter as a one way broadcast system.

I also include the Twitter handles of companies that I mention so that people can go to their profiles and find out more. I am busy collecting corporate Twitter handles and adding them to the KRO profiles so that members who use the KRO Search Engine to research the juniors can easily follow those companies that interest them. I myself follow the Twitter accounts of companies that interest me because I expect these companies to tweet whenever they have a press release or new presentation on their web site. The tweet should include the headline and a link so that I can go to their web site and review the new content. I also like it when they tweet a link to third party web site hosted content relevant to their story. Public companies should not engage in Twitter conversations with their followers. Like me they should just use it as an alternative to email.

Email is dead as a notification system. Spam filters, opt-in requirements and blacklisting have made email unreliable as a one to many broadcast tool. The fact that my Twitter feed is polluted by sponsored tweets sucks, but anything that is truly free won't survive. There is always a price.

I encourage resource juniors to set up a Twitter account and use it as a notification system, not just because it dispenses with the headaches of email, but because it also allows organic audience growth. Kaiser Research is a membership fee based information portal for whose content I alone am responsible. But I also run a Slack Forum. New KRO members are sent a slack invite that allows them to register for KaiserResearchOnline at Slack. I've created 30 theme based channels into which I post off the cuff comments and links to anything new I have posted on KRO. Members can also post links, ask questions, engage in conversations. If anybody becomes uncivil or uses it to pump some garbage I can deactivate their membership. Most KRO members just lurk and read. A small percentage are active posters. This is where I engage in conversations.

There are no advertisements. It is like a private forum on CEO.ca, except nobody is running analytics to extract knowledge from our private activity. Slack is not free. It is now owned by Sales Force and its target market are businesses whom it wants to charge $10 or so per month for every employee that is a member. Because Slack facilitates collaboration and direct messaging this $120 annual cost per employee is a good deal. But it would be a quarter of the annual $450 membership fee which is not a good deal for me. Slack is free to me and my members because there is a price. It used to be that only the last 10,000 posts were visible, which, based on the level of activity in my Slack space, meant that only the last year's posts were visible. In September Slack switched to a new policy where it displays only the last 90 days of posts. This means KRO Slack will be mainly useful to KRO members for current conversations. That still is hugely useful to me and my members.

I mention Slack because the real value of Twitter for myself and resource juniors is that Slack is an example of the millions of social media clubs out there whose members engage in conversations. Slack is ideal for an investment club run by a moderator who also controls who has access. Public forums like Stockhouse and Hot Copper in Australia inhibit thoughtful posting because there is an army of anonymous pumpers and bashers ready to trash the poster or pollute the thread. Twitter is the place where influencers hang out to market products and ideas. Some of these influencers follow the resource juniors and develop their own following. When they receive a tweet they like they can publicly like or retweet it to their followers, who in turn can do likewise. Or, when they are members of a social media club such as KRO Slack, they can post the tweet link or the tweet's embedded link in the channel where appropriate.

The benefit for resource juniors is that their audience can grow virally with only the effort of tweeting the latest news release, corporate presentation, or third party web site link relevant to their story. And it doesn't cost them a penny.

Example of Interactive/Collaborative Activity in KRO Slack

Jim (0:09:30): Is Bell Copper any closer to resuming work at its Big Sandy emerging copper discovery?

Kaiser Watch October 6, 2022: Cheering for Bell Tower Endurance has graphics and a good description of Bell Copper's Big Sandy story so I include only a couple here. The question then was financing needed to resume drilling at Big Sandy. On November 15 BCU bit the bullet and announced a private placement to raise up to $3 million by offering 25 million units at $0.12 with a full 2 year warrant at $0.20 whose expiry will be accelerated to 30 days if the stock's VWAP price is $0.40 or higher for 20 consecutive trading days. If it closes in its entirety this would push fully diluted to 204 million shares. This is not an automatic trigger because BCU will have 20 days after it is hit to make it effective.

The potential 50 million share dilution is a disappointment in light of the stock trading in the $0.30-$0.70 range in February through March after announcing that hole BS-3 encountered 287 m of chalcocite mineralization at a hole depth of 1,302 m in the Big Sandy target. The stock had jumped from the $0.20 level because the market interpreted this intersection as confirmation that the truncated top of the Diamond Joe porphyry root 13 km to the southwest across a basin had finally been discovered. Explorers have searched in vain for decades for the missing top because the width of the root and the remnant mineralization indicated a world class scale porphyry deposit. Arizona's basin and range faulting assumed that the top had slid to the east and was lurking somewhere under the gravels of the 13 km wide basin valley through which the Big Sandy River flows. Even Bell Copper under Tim Marsh took a crack at it a decade ago but gave up when the bedrock proved a couple thousand metres deep. The conclusion was that wherever it ended up, it was too deep and expensive to find, and perhaps too deep to mine, even though it had the potential for a copper rich supergene enrichment blanket above the primary copper zone.

Marsh shifted BCU's attention to finding the missing top of the Wheeler Wash porphyry stock farther north which used to be called Kaaba but is now called Perseverance. Robert Friedland's Cordoba Minerals optioned it in 2018 and has yet to find the missing top. Bored with waiting for Cordoba to find the prize and meditating on what the effort was revealing, Marsh decided in 2020 to revisit Diamond Joe. This time he went all the way across the basin, much farther east than he had ever imagined the truncated top could have wandered, and started exploring the range front east of the Big Sandy River. There he observed exotic copper of the kind that forms when groundwater dissolves copper, carries it towards the surface, and precipitates the copper in rocks unrelated to the original porphyry system. This is different from a supergene enrichment blanket which forms when circulating groundwater leaches primary chalcopyrite and drops its copper payload as another sulphide called chalcocite father down. This repetition leaves the upper part of the zone barren but enriches the copper grade of the deeper chalcopyrite zone.

Since there wasn't any room for the Diamond Joe top in the eastern range, Tim Marsh came to the stunning realization that it must be buried east of the Big Sandy River near the eastern edge of the basin, over 13 km from the source. So he staked the Big Sandy claim, whose outlines he has never revealed in any corporate graphics, conducted an MT survey which indicated a major conductive body at 400 m depth, and started a drill vectoring strategy. The conductor turned out to be fake, probably caused by clays in the basin, and bedrock proved 1,000 m deep. This first hole hit the edge of a porphyry system, confirming the truncated Diamond Joe had traveled this far east. The second hole hit older country rock that the Diamond Joe had intruded and would have traveled with the porphyry zone when it faulted off the root. The third hole excited the market because the presence of a leach cap followed by supergene mineralization confirmed that the missing Diamond Joe head had finally been found.

Tim, however, knew, with the help of his XRF gun, that the grade was not going to be the 0.6% plus copper needed to support an underground block-caving operation and he made no secret about that. But as the hole passed into the underlying primary chalcopyrite zone it was too low grade to have been the source from which the chalcocite grade was enriched. It resembled the pyritic shell which flanks the richer primary copper shell that is draped around the low grade core of a porphyry stock. This led him to conclude that the chalcocite enrichment was partly created by lateral flow from the center of the stock. He had also observed that the Diamond Joe top was tilted, with the unfortunate result that hole BS-3 hit bedrock deeper than where the fully enriched blanket would be located. But because of the tilt angle it was possible that if he pushed BS-3 deeper it might hit the edge of the primary copper shell, delivering definitive confirmation of Diamond Joe's location. He pushed the hole another 524 m to a depth of 2,026 m, but the copper mineralization never improved and he finally quit the hole. After surveying the hole he understood why, namely that the angled hole had straightened and was in effect coring parallel to the primary copper shell if it was where he expected it to be. The key benefit was that he now knew exactly where to spot the fourth hole to hit the supergene blanket above the primary copper shell.

When BCU reported 200 m of 0.42% copper for the chalcocite zone and 524 m of 0.16% copper for the chalcopyrite zone the market reacted very negatively because together they seemed to suggest a low grade copper system that could only be mined underground and thus had zero economic potential. Part of this reaction was due to the resource sector having finally also gotten caught up in the 2022 equity market decline, but also because the market did not understand the geological context. For that Tim Marsh was partly to blame, because although his written descriptions made sense to competent geologists, who realized Marsh had landed a major emerging copper discovery, lay people need cartoons to understand geological word salads. Later in the summer he capitulated by creating graphics for the presentations he was giving to geology societies whose members like retail do actually prefer staring at cartoons rather than converting words into mental graphics. But by then the market perception damage had been done, and the cost of pushing the hole to 2,026 m had left the junior with a near empty treasury. By the time he secured a permit and a special rig to pre-collar hole BS-4 through the gravel, which should reduce the prior hole's 3 month gravel drilling ordeal to 1 month, the market was no longer interested, and majors which had signed NDA's were distracted by the declining copper price. And so in mid November Tim Marsh bit the bullet so that he could drill what could be a make or break hole.

The financing, while appearing hideously dilutionary, is well thought out. First of all, the press release says up to $3 million. Closing is not conditional on all $3 million being raised. Bell Copper will close it in tranches. If it all comes in at once, so be it. But if $1 million comes in the door quickly, Bell will close that tranche and start hole BS-4. The hope is to start BS-4 in early December so that it is poised to intersect bedrock in early January. Once that milestone is reached BCU will close the financing because the visuals will reveal lots about how the hypothesis is playing out. The private placement has a four month hold, so it won't be free trading until April, and even if the trigger is reached in Q1, BCU is unlikely to pull the trigger until the four month hold is over. By March BCU would be in a position to report visuals, setting the stage for assays by June.

BCU has 9,648,922 warrants at $0.25-$0.26 from earlier financings that expire in March through June of 2023 (mostly in early June) which could raise about $2.4 million. If the results are good enough to allow the stock to trade above $0.40 and generate the trigger, it would be wise for BCU to pull the trigger, because clip and flippers will be tempted to dump their $0.12 stock. A discovery hole that inflects Big Sandy from emerging discovery to confirmed discovery, unleashing S-Curve speculation, would bring in new buyers that can absorb the selling created by placees being forced to exercise their $0.20 warrants. If the older and accelerated warrants end up exercised, BCU would start H2 2023 with an extra $7.4 million in the bank, and no warrant overhang left. With 204 million fully diluted and 100% ownership of Big Sandy confirmed as a major new copper discovery in Arizona, the stock, carrying an implied value of only $100 million at $0.50, would have upside room to deliver a 5-10 bagger as BCU gets to work delineation drilling the new discovery.

Aerial View of the Diamond Joe Displacement Hypothesis at Big Sandy

Geological Cartoon of Big Sandy Target

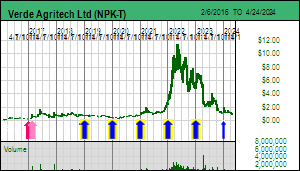

Jim (0:24:13): Can you give us a summary of Verde Agritech's third quarter conference call?

The third quarter financials were released on Monday Nov 14 and the conference call was held Thursday Nov 17. The entire call was 1 hour 17 minutes. The first 21 minutes has the CFO going through the results. In summary for the first 9 months of 2022 NPK has generated CAD $63 million in revenues, almost 3 times that for last year, and generated $23 million in cash flow, almost 5 times last year. In terms of volume they have sold 503,000 tonnes of K Forte compared to 266,000 tonnes last year. The stock, which almost hit $8 on Monday, has since retreated below $6. The best explanation is that the market has realized that NPK may not make its revised 2022 guidance of $87 million revenue and $31 million cash flow. Plant 2 is now fully operational at its 2.4 M tpa capacity, bringing total capacity to 3M tpa, but the road access problem that emerged in early September and was not fixed until late October cost the company over 100,000 tonnes of K Forte in cancelled orders because it could not be delivered from Plant 2. Q4 and Q1 are low demand quarters because it is the rainy season and if the farmers don't have the fertilizer in time they won't need it until the next planting season which starts in Q2. Cris Veloso made it very clear that the company is working very hard to meet its 2022 guidance of 700,000 tonnes which is a warning to the market that when the full year results are announced in mid April they may fall short of guidance. As far as I am concerned it doesn't matter to me because it was always optimistic that Plant 2 would be operational in time to ship K Forte during the third quarter. The company is now positioned to expand sales and revenues four-fold in 2023 and by the time we get the annual results the market will be focused on the extent that orders have been booked for delivery in Q2-Q3.

The interesting part of the conference call was the nearly hour long Q&A. Here are a few themes that caught my attention.

The first batch of questions were of a technical accounting nature. I am not a financial analyst so these sorts of questions are boring. But they are an important sign that Verde Agritech has graduated into the league of an operating company and is attracting analysts who care about revenues and costs.

Verde Agritech attracted a lot of market attention earlier this year after Russia invaded Ukraine and concern arose about Russian and Belarusian potash supply which is about 37% of global output. Potash, however, was never put on the sanctions list, and Belarus managed to figure out an alternative route to market when Lithuania stopped being a transportation corridor. The Brazilian ports are now bulging with potash and some of it is being diverted to other countries. The price, however, is still $740/t KCl, well above the $360/t the company uses in its feasibility study. NPK's pricing strategy allowed Plant 1 to operate at capacity, and in May NPK boosted its guidance on the expectation that Plant 2 would be operational by July, but it didn't happen until late August, and then came the water problem that prevented them from operating Plant 2 while they built a new bridge and upgraded the access road. Apparently NPK has only 15,000 tonnes of storage capacity, so its plants operate only to fulfill orders that can be immediately trucked to farmers.

There were several questions about providing K Forte in a granular form which is the form preferred by the bigger farms. Apparently there is a limit to how much powdered K Forte NPK can sell to farmers, but apparently that limit will not be hit by the current 3M tpa capacity. The problem with converting K Forte powder into a granular form is that it requires adding water and a binder to the powder and then drying the result to remove the moisture. Drying is a significant cost and the company has been researching a method to create granular K Forte that avoids the drying step. Their bigger concern right now is boosting sales to 3M tpa and they are planning to use discounted prices for Q4-Q1 deliveries which is shaping up to be a difficult period for all fertilizer companies.

There was a question about BioRevolution being sold at a 90% discount from its list price which CV explained was necessary to persuade farmers to try out the microbe loaded K Forte as a soil rehabilitation strategy. That makes sense because this is a brand new concept and farmers will want to see it work before committing to use it.

There was a question about carbon credits which the company is exploring and which is a benefit of Lula's election and Brazil's pivot back to caring about climate change.

There were also questions about the US listing with no definitive timing offered though they are still working on it. They are also close to unveiling a brand new web site which will include translations of the 100 Portuguese testimonials about the efficacy of K Forte. That in itself could help investors overcome concern about how quickly sales grow in 2023.

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch November 10, 2022: Canadian Stupidity & Hypocrisy

Jim (0:00:00): What do you think of Canada's recent order that Chinese companies divest their holdings in three lithium juniors?

On October 28, 2022 the Government of Canada announced a new Policy Regarding Foreign Investments from State-Owned Enterprises in Critical Minerals under the Investment Canada Act and François-Philippe Champagne, Minister of Innovation, Science and Industry, ordered that three Chinese entities divest themselves of their equity stakes in three Canadian listed resource juniors. These orders are a demonstration of monumental stupidity and hypocrisy. They make absolutely no sense and should be opposed because they jeopardize the role of Canadian resource juniors in identifying and mobilizing new critical mineral supply. If Prime Minister Justin Trudeau were truly serious about the energy transition he should streamline the exploration-development permitting system, resolve issues with First Nations that encourage them to block mining, provide support for downstream processing capacity, and reform securities law so that Canadians who do not qualify as "millionaires" can easily participate in private placements, the primary mechanism through which resource juniors raise risk capital.

At this point the lithium market is not vulnerable to a single point of failure or Spof for short. Lithium Mania 1.0 which started in 2015 when the EV sector took off has mobilized plenty of supply from Australia and the Lithium Triangle which over the next 5 years will deliver half the supply needed for total demand projected for 2035-2040. Lithium Mania 2.0 which began in 2021 when lithium carbonate prices started a 10 fold rebound from the 2020 gutter below $3/lb will deliver the other half from Archean cratons in eastern Canada, Scandinavia, Brazil and Africa. The supply will come from many small to medium sized mines. A Chinese state owned enterprise having a stake and even offtake agreement in one of hundreds of contenders does not alter the collective outcome, but it does help the inflow of capital from a wide range of sources.

The 3 orders seem arbitrary and capricious. What does it matter to Canada that a Chinese entity invests indirectly in a project in another country? Does this perhaps give that country the right to expropriate the project from the Canadian company and sell it to the foreign investor? And even with a Canadian based project, why interfere with what is a collective race to develop new lithium supply? So what if concentrates get exported to China for refining? The government should focus on supporting the construction of refineries in Canada and facilitating the permitting cycle. Let's look at the 3 juniors targeted by the Canadian government divestiture orders.

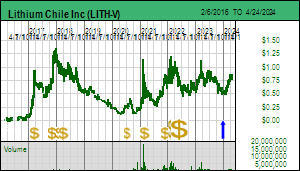

Lithium Chile Inc raised $28 million at $0.95 from Chengze Lithium International Ltd for its brine projects in Chile and Argentina. What business does Canada have ordering a Chinese company to not have a stake in Lithium Triangle brine projects via a Canadian listed company? Is that not the job of the Chilean and Argentine governments? If the Arizaro project does not advance because of lack of capital, maybe Argentina should take it away from the Canadian junior and give it to the Chinese investors.

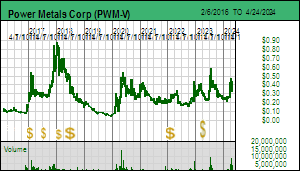

Power Metals Corp has the Case Lake project which hosts a set of narrow dykes that include high grade cesium. Sinomine Rare Metals Resources Co bought 7.5 million shares in late 2021 to invest $1.5 million. As part of the financing Sinomine secured an offtake for all lithium, cesium and tantalum. But Case Lake does not even have a resource estimate yet, and Exploration VP Julie Selway, an expert on Canadian pegmatites, is still trying the find the best pegmatites at Case Lake. The offtake agreement is meaningless at this stage. Furthermore, Case Lake is very unlikely to become a future single point of failure. There are lots of other potential LCT type pegmatites in eastern Canada that will emerge as Lithium Mania 2.0 unfolds. And if by any chance 5-10 years from now it becomes necessary to allocate lithium and cesium supply to domestic users, the government can create export controls. The United States just did that to China with high end chip technology. The age of globalized free markets is over. Telling Sinomine to sell its stake in an exploration stage junior makes no sense. Sinomine already owns the Bernic Lake operation which used to produce cesium but Sinomine now wants to mine the spodumene left behind. Wouldn't it make more sense to force Sinomine to divest itself of the former Tanco operation in Manitoba it bought from Cabot?

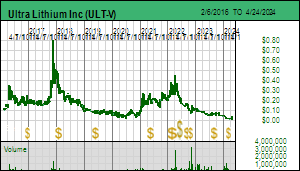

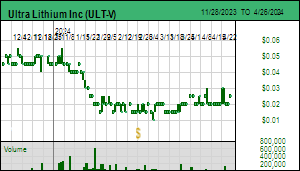

Ultra Lithium Inc owns the Laguna Verde brine project in Argentina and a net 40% stake in its Georgia Lake area properties after selling 60% to a Chinese company called Yahua which has been busy doing deals with Australian companies. Zangge Mining Investment (Chengdu) Ltd invested $4.1 million at $0.18 to acquire 23 million shares earlier this year. The junior has 2 China based directors from a decade ago who together own 40.5 million shares. Why not also create a ban on Chinese nationals owning shares in any Canadian listed company? Do we really want to decide who is allowed to invest in resource juniors? Maybe it might make sense to block a Chinese entity from buying out a Canadian junior with a critical metals project in Canada that is ready to be built. But worry about that later. None of Ultra Lithium's projects are at an advanced stage.