| Kaiser Watch November 10, 2022: Canadian Stupidity & Hypocrisy |

| Jim (0:00:00): What do you think of Canada's recent order that Chinese companies divest their holdings in three lithium juniors? |

On October 28, 2022 the Government of Canada announced a new Policy Regarding Foreign Investments from State-Owned Enterprises in Critical Minerals under the Investment Canada Act and François-Philippe Champagne, Minister of Innovation, Science and Industry, ordered that three Chinese entities divest themselves of their equity stakes in three Canadian listed resource juniors. These orders are a demonstration of monumental stupidity and hypocrisy. They make absolutely no sense and should be opposed because they jeopardize the role of Canadian resource juniors in identifying and mobilizing new critical mineral supply. If Prime Minister Justin Trudeau were truly serious about the energy transition he should streamline the exploration-development permitting system, resolve issues with First Nations that encourage them to block mining, provide support for downstream processing capacity, and reform securities law so that Canadians who do not qualify as "millionaires" can easily participate in private placements, the primary mechanism through which resource juniors raise risk capital.

At this point the lithium market is not vulnerable to a single point of failure or Spof for short. Lithium Mania 1.0 which started in 2015 when the EV sector took off has mobilized plenty of supply from Australia and the Lithium Triangle which over the next 5 years will deliver half the supply needed for total demand projected for 2035-2040. Lithium Mania 2.0 which began in 2021 when lithium carbonate prices started a 10 fold rebound from the 2020 gutter below $3/lb will deliver the other half from Archean cratons in eastern Canada, Scandinavia, Brazil and Africa. The supply will come from many small to medium sized mines. A Chinese state owned enterprise having a stake and even offtake agreement in one of hundreds of contenders does not alter the collective outcome, but it does help the inflow of capital from a wide range of sources.

The 3 orders seem arbitrary and capricious. What does it matter to Canada that a Chinese entity invests indirectly in a project in another country? Does this perhaps give that country the right to expropriate the project from the Canadian company and sell it to the foreign investor? And even with a Canadian based project, why interfere with what is a collective race to develop new lithium supply? So what if concentrates get exported to China for refining? The government should focus on supporting the construction of refineries in Canada and facilitating the permitting cycle. Let's look at the 3 juniors targeted by the Canadian government divestiture orders.

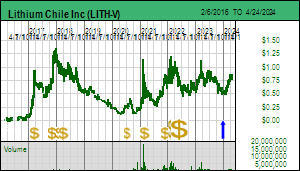

Lithium Chile Inc raised $28 million at $0.95 from Chengze Lithium International Ltd for its brine projects in Chile and Argentina. What business does Canada have ordering a Chinese company to not have a stake in Lithium Triangle brine projects via a Canadian listed company? Is that not the job of the Chilean and Argentine governments? If the Arizaro project does not advance because of lack of capital, maybe Argentina should take it away from the Canadian junior and give it to the Chinese investors.

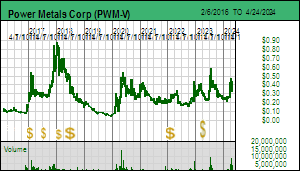

Power Metals Corp has the Case Lake project which hosts a set of narrow dykes that include high grade cesium. Sinomine Rare Metals Resources Co bought 7.5 million shares in late 2021 to invest $1.5 million. As part of the financing Sinomine secured an offtake for all lithium, cesium and tantalum. But Case Lake does not even have a resource estimate yet, and Exploration VP Julie Selway, an expert on Canadian pegmatites, is still trying the find the best pegmatites at Case Lake. The offtake agreement is meaningless at this stage. Furthermore, Case Lake is very unlikely to become a future single point of failure. There are lots of other potential LCT type pegmatites in eastern Canada that will emerge as Lithium Mania 2.0 unfolds. And if by any chance 5-10 years from now it becomes necessary to allocate lithium and cesium supply to domestic users, the government can create export controls. The United States just did that to China with high end chip technology. The age of globalized free markets is over. Telling Sinomine to sell its stake in an exploration stage junior makes no sense. Sinomine already owns the Bernic Lake operation which used to produce cesium but Sinomine now wants to mine the spodumene left behind. Wouldn't it make more sense to force Sinomine to divest itself of the former Tanco operation in Manitoba it bought from Cabot?

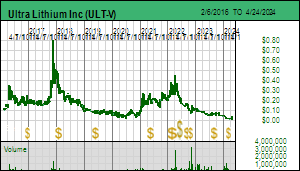

Ultra Lithium Inc owns the Laguna Verde brine project in Argentina and a net 40% stake in its Georgia Lake area properties after selling 60% to a Chinese company called Yahua which has been busy doing deals with Australian companies. Zangge Mining Investment (Chengdu) Ltd invested $4.1 million at $0.18 to acquire 23 million shares earlier this year. The junior has 2 China based directors from a decade ago who together own 40.5 million shares. Why not also create a ban on Chinese nationals owning shares in any Canadian listed company? Do we really want to decide who is allowed to invest in resource juniors? Maybe it might make sense to block a Chinese entity from buying out a Canadian junior with a critical metals project in Canada that is ready to be built. But worry about that later. None of Ultra Lithium's projects are at an advanced stage.

What the Canadian government should really focus on is its permitting cycle and unresolved First Nations problems. Consider the Spof vulnerability created by Brazil's domination of niobium supply from a single giant world class deposit called Araxa. Niobium is indirectly critical to the energy transition for its role as an alloy that strengthens steel which in turn allows light-weighting, meaning lower energy consumption when transporting goods. There is only one other deposit like Araxa, and it is also in Brazil in a hopelessly remote corner of the Amazon Basin. All other niobium enriched carbonatites are substantially smaller and lower grade. Global supply comes from 2 other such mines, one in Brazil controlled by a Chinese company called China Molybdenum, and the other is privately owned Niobec in Quebec. Araxa supplies 85% of global niobium output which goes mainly into steel. Toshiba is working on a niobium-titanium anode which would be a superior replacement for the graphite anode in the lithium ion battery. Brazil just went through a tumultuous election. Araxa is a huge single point of failure risk.

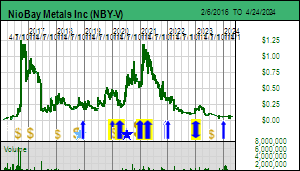

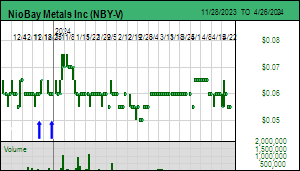

Canada's second best niobium deposit after Niobec is the James Bay deposit in northern Ontario owned by NioBay Metals Inc. A PEA done in 2020 shows that the deposit is viable at current niobium prices which Araxa's owner CBMM cultivates to maximize its domination of global supply, just high enough to allow some other deposits to be profitable, but not others such as Niocorp's Elk Creek carbonatite in Nebraska. Niobay has a drill permit that would let it take James Bay through the PFS stage. Local politics involving the Moose Cree First Nation has stalled work on advancing James Bay. The stock, which should be in the $2-$5 range while it advances James Bay toward a production decision with a future target price range of $10-$20, has collapsed to a dime after raising $10 million plus in 2020. Why doesn't Prime Minister Justin Trudeau step in and get exploration of the James Bay deposit back on track? Lithium Mania 2.0 will deliver dozens of potential pegmatite lithium mines in eastern Canada. Right now there is only one potential additional niobium mine in Canada and it is blocked by a local anti-mining lobby encouraged by outsiders who do double duty railing about the need to ban fossil fuels. Shame on Trudeau for his stupidity and hypocrisy. |

Lithium Chile Inc (LITH-V)

Unrated Spec Value |

|

|

| Arizaro |

Argentina - Other |

2-Target Drilling |

Li |

Power Metals Corp (PWM-V)

Unrated Spec Value |

|

|

| Case Lake |

Canada - Ontario |

3-Discovery Delineation |

Li Ta Cs |

Ultra Lithium Inc (ULT-V)

Unrated Spec Value |

|

|

| Laguna Verde |

Argentina - Other |

2-Target Drilling |

Li |

NioBay Metals Inc (NBY-V)

Bottom-Fish Spec Value |

|

|

| James Bay |

Canada - Ontario |

6-Prefeasibility |

Nb |

Lithium Chile's Lithium Triangle Focus |

Power Metals Case Lake Project |

Ultra Lithium's Early Stage Brine & Pegmatite Projects |

NioBay Metals Solution to Niobium Single Point of Failure Risk |

NioBay NPV per Share Model for James Bay Niobium Project |

NioBay NPV Model for James Bay Niobium Project |

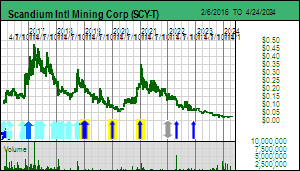

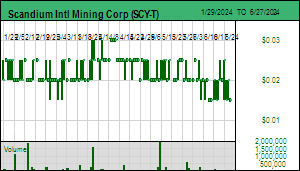

| Jim (0:11:32): How did the scandium conference affect the outlook for Scandium International? |

Scandium International Mining Corp has now updated its web site and posted both the slide presentation and script for Peter Evensen's speech at the 1st International Scandium Symposium held October 20, 2022. The stock has since fallen because Evensen makes it clear that the company is not going to work on helping end-users discover uses for Al-Sc alloy as George Putnam attempted in 2018-2019 through the LOI strategy, nor will SCY build Nyngan until it has committed offtakes for at least 20 tonnes of scandium oxide with a minimum $1,500/kg price. That is the price Friedland uses for his Sunrise scandium output and Peter Cashin's Imperial Mining Group uses for the Crater Lake project before ramping it up to $6,000/kg by switching to selling master Al-Sc alloy.

Nyngan's DFS was done at $2,000/kg, but it still is profitable at $1,500/kg. However, the USD $87.1 million CapEx is probably over $100 million today, and OpEx will also be higher, so at $1,500/kg the NPV for a 35 tpa Sc2O3 operation will be lower than the AT NPV of USD $177 million (8%) projected by the DFS. The message the market has taken from Peter's speech is that SCY has become a scandium optionality play waiting for Rio Tinto to build up scandium demand incrementally through its Sorel-Tracy operation where it recovers scandium while upgrading the titanium slag to the rutile equivalent grade the pigment makers demand. Sorel-Tracy has a scandium output limit of about 40 tpa scandium oxide, and it make take Rio Tinto several years to hit this limit. That means SCY ownership will be dead money while Lithium Mania 2.0 ramps up over the next few years as it delivers a Canadian exploration boom bigger than the diamond boom Dia Met launched in 1991.

The emphasis on having refinanced the company and being prepared to wait 5 years for Rio Tinto to max out its Sorel-Tracy scandium supply potential is a downer, but there were clues in the speech that SCY may not just sit back and wait for Rio Tinto to build scandium demand. If Rio Tinto can build current scandium demand of 20-25 tpa to 50 tpa, that will be a tipping point where demand growth can accelerate toward a future potential of 1,000 tpa, provided there is a primary, scalable supply operational. Unfortunately, the permitted 35 tpa capacity of Nyngan would be woefully inadequate for Rio Tinto. And while Nyngan's modular nature allows capacity to be expanded to 100 tpa over time processing only the limonite resource, Rio Tinto or an Alcoa would want to start with a higher output capacity.

When Peter mentioned seeking a partner for the development of Nyngan that has negative implications if the partner is an entity like Rio Tinto. Ideally CapEx gets funded with debt rather than equity or ownership dilution. One of the companies at the conference was Materion which started out as the world's dominant beryllium producer through its small Spor Mountain operation in Utah, but has since branched into a wide range of specialized materials, some of which require scandium. Materion makes its margin from the IP embedded in these products, but is also the world's only vertically integrated beryllium producer. Bloom Energy is similar in that its Bloom Boxes which require scandium in the electrolyte of the solid oxide fuel cell also are unrelated to aluminum alloys. One path SCY could immediately pursue is to partner with Materion or Bloom in exchange for 20 tpa offtake agreements at $1,500/kg with rights to increase offtake down the road should their products take off. The Nyngan operation is really a giant pilot plant. It can be expanded once it is operating as expected, but there is an alternative supply growth path.

Peter mentioned the possibility of revisiting the nearby Honeybugle deposit which SCY drilled in 2014 when it thought it would lose Nyngan. Grades are similar to Nyngan, and Honeybugle may even be bigger and richer than Nyngan. Drilling shallow RC holes to support a JORC resource estimate would likely cost less than $1 million. If SCY can find a partner for Nyngan sooner than later, which would allow it to demonstrate the flowsheet, the availability of the Honeybugle resource would make SCY a future buyout target for Rio Tinto because it could be permitted to start at 100 tpa capacity to feed surging Al-Sc alloy demand. Peter also indirectly alluded to the Kiviniemi deposit in Finland which has a similar size and grade as IPG's Crater Lake project but with a much better location and simpler mineralogy. Earlier this year he was dismissive of Kiviniemi, but with the EU becoming more supportive critical mineral supply in its backyard, Kiviniemi deserves additional metallurgical studies. It might even attract the interest of Heinz Schimmelbusch's AMG Advanced Metallurgical Group NV, a billion dollar revenue company that produces alloys and specialty metals. It even has an aluminum alloy operation in Pennsylvania. I do recommend carefully reading the script of Peter Evensen's speech, because while a quick read will leave you with the impression the company will hibernate for the next few years, a closer read hints at steps that could launch SCY into an uptrend. |

Scandium Intl Mining Corp (SCY-T)

Bottom-Fish Spec Value |

|

|

| Nyngan |

Australia - New South Wales |

8-Construction |

Sc |

Cover of SCY's Conference Presentation |

Potential Partners for Nyngan? |

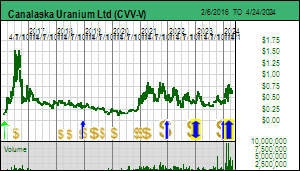

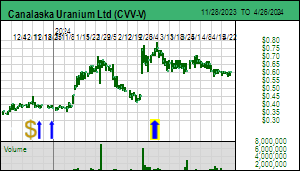

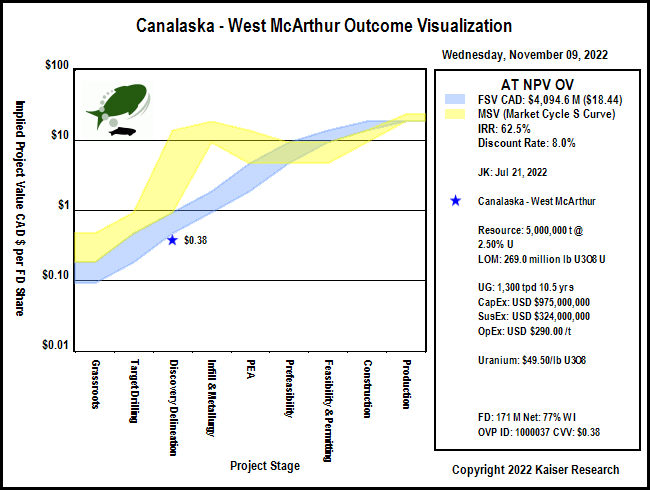

| Jim (0:21:54): Where is Canalaska Uranium with its West McArthur emerging discovery? |

Canlaska Uranium Ltd has an emerging uranium discovery at its 78.91% owned West McArthur project in Saskatchewan's Athabasca Basin. Since reporting the discovery hole last summer within the C10 South corridor 6 km SW of the 42 Zone where Canalaska has spent most of its effort during the past 5 years it has drilled 7 additional holes from 3 drill pads. The first 2 drill pads are near each so that the seciond rig could help sort out the geometry of the new zone within the basement at a depth of 800-1,000 m. The C10 South corridor has a SW strike and contains graphitic metasediments below the sandstone unconformity that dip to the SE. Hole #67, which assayed 9 m of 2.4% U3O8 within the basement, tested a part of the corridor where a north-south fault structure is present and which was the gateway for the hydrothermal activity that allowed the fluids to drop their uranium payload when they encountered the graphite.

3 of the holes encountered segments of uranium mineralization. Of these #72-3 drilled from the second drill pad had a 12.4 m interval with multiple sections of uranium mineralization including a 20 cm interval of massive pitchblende that will have a very high grade. The other 3 holes did not hit mineralization but did encounter bleaching and alteration. None of the holes have yet intersected the location where the basement hosted graphite bed encounters the basin sandstone, the so called unconformity target where one can hope for McArthur River scale volume and grade.

The last hole #73 was drilled from a pad 160 m NE of the original #67 fence. It was intended to hit the unconformity target but appears to have overshot it by 60 m. Canalaska plans to resume drilling in January with a rig that allows better control of directional drilling from pilot holes to test the 800-1,000 m depth of the emerging discovery at West McArthur. Canalaska has presented a $10 million budget to Cameco which has 30 days to decide if it will contribute or continue to dilute.

Last week Canalaska closed a $10 million flow-through financing first announced on October 6 as an $8 million financing. The regular flow-through was done at $0.52 per unit and the charity flow-through at $0.70. The unit included a 3 year half warrant at $0.75. $6.9 million was raised from the regular FT and $3.1 million from the charity FT. Flow-thru is both a blessing and a curse. It is a blessing because the company can raise capital at a premium to the market. But it is a curse because the purchasers tend to be interested only in the tax benefits and don't plan to hang around for a fundamental success outcome. So after the 4 month hold ends, which will be early March, the market will have to eat the flow-thru paper. Although Canalaska will resume drilling in January, it won't be reporting assays that elevate West McArthur from emerging to full-blown discovery that launches S-curve style speculation until Q2 of 2023. |

Canalaska Uranium Ltd (CVV-V)

Bottom-Fish Spec Value |

|

|

| West McArthur |

Canada - Saskatchewan |

3-Discovery Delineation |

U |

West McArthur Emerging Discovery Drill Plan & Section |

Photo of Hole 72-3 Mineralized Core Interval |

OV Chart for Nexgen style Outcome |

| Disclosure: JK owns NioBay Metals and Scandium Intl; Canalaska, NioBay & Scandium Intl are Bottom-Fish Spec Value rated; Lithium Chille, Power Metals & Ultra Lithium are unrated |