On April 29 the Mexican Senate jammed through a couple constitutional changes unrelated to the mining sector and a new mining law. This was accomplished by members of the ruling Morena party secretly gathering in another chamber to put the proposals to a vote while the opposition was gathered in the main chamber to protest the proposed rule changes. Last year Mexico's president nationalized the mining of lithium, effectively stripping owners of mining concessions with lithium potential from having the right to develop and mine lithium. The result has been that exploration for lithium in the form of claystones, brines or pegmatites simply stopped. Now the government is trying to come up with a system that will attract exploration and development capital of the sort juniors typically bring to the table. Chile's leader Gabriel Boric recently proposed a change which would give Chile a major stake in all new brine projects. The Chilean system was already messed up due to the government's excessive role in granting production leases. Some juniors have claimed that greater clarity will get things moving for the Chilean portion of the Lithium Triangle, but for now Chile's state copper mining entity has been instructed to study how to best take a higher stake in existing brine operations and figure out what the investment and title regime will be for undeveloped lithium projects. However, because the proposed Chilean change must get approval from another government branch, it may be quite some time before anything is formalized. In the meantime, all Chilean brine projects not already in production are in limbo. This has helped spotlight why Argentina is a better jurisdiction for developing brine projects and it has given brine producers like Albemarle, SQM and Wesfarmers extra reason to look at supply expansion through pegmatite lithium projects. Chile's foolishness may turn out to be of great benefit to Canadian juniors engaged in Lithium Mania 2.0 exploration in Canada. The Mexican mining law change may also boost the fortunes of resource juniors with a focus on Canadian projects.

The first implication of this Mexican mining law change is to create a period of limbo. Because of the manner in which the laws were passed it will be challenged to the Mexican Supreme Court which has resisted Andres Manuel Lopez Obrador's efforts to undermine Mexico's democratic institutions. Amlo is a populist like Trump but chases left wing goals such as more state control of everything. His term ends in 2024 so he will not be in a position to claim the election was stolen. But like Vladimir Putin and Xi Jinping he will do his best to get the rules changed so that he can stay in power beyond the current 6 year term limit. Because of the urgency of the matter a court decision could be in hand within a couple months.

Amlo has been pushing for mining law reform for some time, arguing that the existing mining concession system is too generous. In countries like Canada mineral title is established by staking open claims, online in most provinces through map-staking. There are staking fees and assessment work reporting requirements to keep the claims alive. Countries like Mexico have a claim application system where a company or individual must file a request for a land package. Once the application has been made nobody else can apply for those claims which are either confirmed as a mining concession or not. These mining concessions have a 50 year term. As a result Mexico is checkered with existing concessions covering most prospective geology. Canadian companies have typically done deals on these claims so that they can explore and develop them if an orebody is outlined.

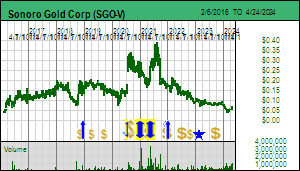

Sonoro Gold is an example of such a junior which has done deals with the mining concession title holders in the area of the Cerro Caliche project in Sonora State. These deals require Sonoro to pay USD $4.9 million by March 2024 of which $3.5 million has already been paid since 2018. Over 57,000 m have been drilled to delineate an indicated and inferred resource of 30,450,000 tonnes of 0.43 g/t gold which at $2,007 gold represents a rock value of $31 per tonne. That's just over 400,000 ounces gold. Sonoro delivered a PEA in September 2021 for a 15,000 tpd open-pit heap leach operation which it updated in May 2022. The mining plan involves several shallow open pits which represent only a portion of the known mineralized zones on the property. The resource supports only a 6-7 year mine life, which is normally a deal-breaker because nearby communities, when they support a mine in their backyard, want a longer mine life to sustain the local economy. However, Cerro Caliche is within an established mining district, there are no nearby communities, and the mineral title has been secured from the local surface rights holders. This has allowed Sonoro to adopt a strategy of designing for a larger scale operation with the goal of using cash flow to fund delineation drilling of additional zones to extend the mine life. For example, I've done an outcome visualization for 75 million tonnes of ore that would yield about 700,000 ounces over 14 years.

This is a low sulphidation epithermal system with gold smoke all over the place, and which, while it has yielded some high grade ore shoots, has not yet yielded deeper higher grade veins such as the Mercedes vein being mined next door by Bear Creek Mining after acquiring it from I-80 Gold. The problem for a junior is that it cannot afford to drill off a 20 year mine life backed by a feasibility study, especially during a bear market and with a gold system whose average grade is at the lower end of what is generally put into production. Sonoro has chosen to seek debt financing supported by a PEA with the argument that at current gold prices not only will lenders be paid back, but there will be sufficient cash flow for reinvestment in expansion drilling and scaling up production down the road with a 1-2 million ounce scenario a plausible outcome. With that goal in mind Sonoro submitted a mine permit application in May 2022.

Since 2018 when Amlo was elected no new mining concessions have been granted. Back in late 2021 Sonoro was confident it could have a mining permit in hand within 6-8 months of application. It is 18 months later and there still is no indication when a mining permit will be granted. Sonoro cannot secure project financing until mine approval is in hand. The COO Jorge Diaz who has put numerous Mexican mines into production has observed a distinct slowdown in the approval process from what he was accustomed to. Part of the problem is that during the covid pandemic bureaucracies such as Semarnat (Scretaria de Medio Ambiente y Recursos Naturales) slowed down activities substantially and lost competent personnel.

At the other end of the regulatory system no new mining concessions have been granted because Amlo wanted to reduce the concession term from 50 years to 15 years. That was a non-starter for the mining industry because any new concession application will be of a grassroots, generative nature where you can spend at least 5 years to be in a position to make a production decision, if you are lucky with exploration early on, at least another year to get mine approval, and then a couple years to build and commission the mine assuming you don't have to sit out a metal price bear market before you can secure CapEx funding. Nobody is going to bother with grassroots exploration if the best outcome is a 7 year mine life. As a result of industry feedback Amlo agreed to a 30 year concession term with a 15 year renewal.

Since Sonoro is paying to acquire existing concessions whose terms are grandfathered, the new concession rules are irrelevant to this Canadian junior with an advanced project in Mexico. But they are deadly to the type of junior that styles itself as a prospect-generator-farmout type. An important change to the concession granting process is the first come first serve principle has been abolished. Any concession application submitted by a party will be made available for anybody under an auction system where the highest bidder is awarded the concession. This makes sense when a land package within a government mineral reserve is being offered for exploration and development to third parties, but not when somebody has applied geological creativity to identify an area as prospective. An earlier version of the mining law reform included a requirement to describe what metals one hoped to find and how much. There was even a plan for the concessions to be metal specific. So if you have an idea for a carbonate replacement type deposit, which would be rich in silver, lead and zinc, you would need 3 concessions to be able to profit from mining all three. Common sense prevailed and these requirements were scrapped. But if this new mineral concession system is adopted, grassroots exploration will be limited to existing mineral concessions.

The big mining companies like Gruppo Mexico, Penoles and Fresnillo have indicated there are no implications for their existing mines, and their landholdings are large enough to offer plenty of greenfields and brownfields exploration potential. Furthermore, when Canadian resource juniors lose interest in Mexico the existing mineral concession holders with grandfathered rights will be easier to deal with. The new mining law does include tougher water usage scrutiny. Until now if a mining company secured water rights from an existing holder it would simply start using them. Now the plan to use water for a mining operation must undergo a study in terms of its impact on the basin from which it will be drawn. Since most mines use a relatively small portion of the water available in a basin the thresholds that would trigger a denial are unlikely to be hit. But the permitting cycle now has an additional study and approval layer. In the case of Sonoro it has secured water rights so this simply means extra studies. The main negative implication of this mining law reform for Sonoro is the uncertainty about when it will become law. The permitting department is not going to speed up processing until clarity has been achieved. If the Supreme Court strikes the mining law down on procedural grounds, Amlo will simply try to change the mining law in another manner. That means further sluggishness in the permitting department.

Sonoro Gold Corp is dealing with the situation by doing a private placement of 30 million units at $0.10 with a full 2 year warrant at $0.15. Insiders will take down a third of the financing to help pay loans Sonoro secured to make property payments due earlier this year and accumulated exploration expenses. Enough money will be set aside to take care of remaining payments this year, though more will have to be raised for the final Q1 2024 payments that secure title, something project lenders will insist on. A portion of the financing will be spent on drilling the western trend defined by the Cabeza Blanca, Guadalupe and El Colorado Zones where more recent drilling has intersected high grade shoots whose grades SRK Consulting capped at 3 g/t gold. The goal is to better flesh out these zones so that the resource grade can be boosted for the starter pits in the proposed mine life. So even if the mining law uncertainty drags on in Mexico Sonoro will be in a position to improve the Cerro Caliche project from the perspective of the project lenders waiting in the wings.

The financing does add 60 million shares of dilution, boosting fully diluted from 232 million shares to 292 million shares. However, 55.6 million warrants at $0.30 expire by the end of 2023, 38.6 million on August 12 and 16.9 million on Dec 20. The first batch was done in September 2020 when the covid response launched gold above $2,000 for the first time. A major participant was Pallisades which embraced a strategy of clipping the warrant and flipping the stock as soon as it became free trading. It did this with most of the juniors it bankrolled during that frenzied financing period. In another 7 months the free-lunchers will have no stake left in Sonoro and the overhang that remains will be in the hands of shareholders who invested in 2021 when the gold market had cooled and who were investing in the Sonoro team's plan to fast-track develop a gold mine that would benefit from a rising gold price. Sonoro will have 236 million shares fully diluted with the dilution held mainly by parties who understand the development dynamics of this story which will become much easier to appreciate when $2,000 becomes the base for gold's future price rather than its ceiling.

|