Hello Guest User, You are visiting this website from a computer with an IP address of 172.70.178.110 with the name of '?' since Wed Apr 24, 2024 at 3:02:29 AM PT for approx. 0 minutes now.

Discovery Watch is a weekly 15-30 minute audio show produced by HoweStreet.com where Jim Goddard interviews John Kaiser about resource juniors with projects that have caught John's attention. The projects will not be limited to companies he has covered as Bottom-Fish and Spec Value Hunter picks and will include projects that may be of interest only because they are in the limelight. Jim and John will periodically circle back to review the projects and if necessary close them out as no longer worth watching. KRO will keep track of projects mentioned through Discovery Watch with HoweStreet.com. Discovery Watch is available via YouTube or Podcast.

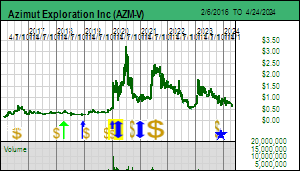

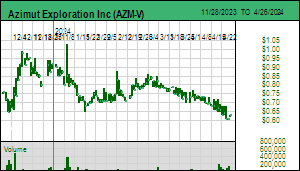

Azimut Exploration In was introduced to Discovery Watch in September 2016 due to its minority stake in the Eleonore South project in the James Bay region of Quebec which covers the southern half of the Cheechoo intrusion where Sirios Resources Inc caught the market's imagination in early 2016 by rethinking a low grade bulk tonnage gold optionality into a potential high grade underground mineable system. Sirios started drilling the intrusion with NE oriented holes instead of SW holes and while initially this seemed to deliver high grade intervals more consistently, after several years it became apparent that the Cheechoo intrusion did not host coherent high grade zones that would lend themselves to underground mining. Sirios has since reverted to a bulk tonnage model and published a resource estimate in late 2019. Azimut's CEO Jean-Marc Lulin became the champion for Eleonore South which it had staked during the early days of the Eleonore discovery by Virginia. Work by Goldcorp and Eastmain failed to deliver a discovery because it was focused on the margins of the Cheechoo intrusion. JML focused on potential high grade zones such as Moni, but that effort grounded out just like that of Sirios. Today it is clear that Eleonore South and Sirios' Cheechoo needs to be consolidated as one property with a large open pit operation which has the support of Newmont (after acquiring Goldcorp), which is also a major shareholder of Sirios. The stick in the mud resisting a win-win proposal has been Azimut, which stopped funding its share of Eleonore South in 2018 when it decided to violate the PGFO strategy by drilling the Chromaska chromite target with its own money. Chromaska died quietly, and it looked like Azimut was a DW bust on two fronts. But in early 2019 when Midland's Mythril copper discovery ignited hopes for a base metals area play in the James Bay region Azimut's Pikwa project to the west became a DW focus after Azimut was able to swing a deal with SOQUEM to earn back a 50% interest. Mythril fizzled in H2 of 2019 when it became apparent that the very high grade copper mineralization was restricted to thin margins of dykes that weren't spaced closely enough to deliver a bulk mineable resource similar to that of the Aitik copper mine in Sweden. During 2019 Azimut focused on mapping and sampling the 20 km Copperfield Trend which projects SWW from the 10 km trend on Midland's Mythril project and established that there were major copper anomalies in the western and eastern ends of the anomaly. The middle seemed to be a dead zone though it did contain 2 prominent EM conductors, the only such anomalies within this trend. The geochemical dead zone may be due to the presence of a giant esker of glacially transported debris that obscures the bedrock. An IP survey in the East Copperfield portion yielded chargeability highs similar to those on the Mythril property to the east, which raised the question of whether Pikwa hosted more of the same marginal copper mineralization. Azimut decided to extend the IP survey west to include the EM conductors, because these could be part of a "center of gravity" for the mineralizing system where bigger zones may have evolved in this Archean setting. We are still awaiting the outcome of this IP survey and what Azimut plans next for Pikwa. Since December 2019, however, the DW focus has been on the Elmer project in the James Bay region where Azimut has demonstrated that the small 200 m by 80 m Patwon outcrop hosts 3 sets of mineralized gold veins: a set of short NW oriented Riedel type dilational veins, a set of sub-horizontal veins, and a set of NE-SW oriented veins, all occurring within what appears to be a 7 km NE trending shear structure. The high grades within the Patwon zone attracted market attention in January 2020 and Elmer was shaping up as a Discovery Watch success story. The association of pyrite with the gold prompted Azimut to conduct an IP survey which generated multiple chargeability highs of the sort associated with sulphide mineralization. Drilling resumed in late May 2020 with the first update occurring in late June after 29 new holes were drilled. Although the market initially responded positively, driving the stock as high as $3.50, the cautious wording by Azimut and the shifts in the drill location sequences of the two rigs suggested that expansion drilling was not playing out as expected. On July 27 Azimut disclosed results for holes close to Patwon which extended the strike 350 m and confirmed mineralization persists to a depth of 200 m. But it is disrupted to the SW and in the NE direction where holes not discussed are pending and where the IP chargeability anomaly is low rather than high. In fact, early holes drilled in ELM-1 where the IP anomaly is strong were not prioritized for assaying. During July Azimut drilled only 7 more holes, most of them in the other ELM IP anomalies. 18 holes were still being logged and assays are unlikely before September. The DW premise was that the Patwon zone would repeat itself along the 7 km shear, most of which is covered by swamp or overburden, with IP anomalies highlighting targets. It now looks like IP is not highlighting gold zones, so until we learn more about the geology and gold controls, the Elmer play is focused on definition drilling of the Patwon zone for a possible open pit scenario and chasing this style of mineralization deeper for an underground scenario. Elmer qualifies as a discovery, but for now it is not a game changing development for the gold potential of the James Bay region. (Jul 29, 2020)

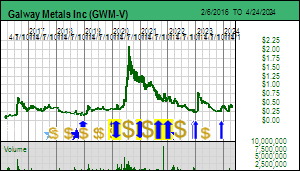

Galway Metals Inc was introduced to Discovery Watch in February 2020 based on its effort to demonstrate that the Clarence Stream gold project in New Brunswick is a multi-million ounce gold district with both open-pittable and high grade underground mining potential. It was a grassroots discovery in 1999 by Mac Watson's Freewest which along with successors never went much beyond the North and South zones for which a resource of 432,000 tonnes of 6.56 g/t gold was generated (about 100,000 ounces). Galway acquired Clarence Stream in 2016 and for the past 3 years has struggled to gain market respect for Mike Sutton's idea that it hosts a district of multiple intrusion related gold systems on both sides of the regional George Sawyer Fault which separates two ages of meta-sediments that have been intruded by younger granites which created the structural setting for gold deposition within veins along their flanks. Key to the optimism are widespread gold in till and soil anomalies north and south of the fault (the North and South zones are on opposite sides of the fault). In late 2017 Galway discovered the trend 7 km southwest of the original North-South Zones defined by the sequence of the George Murphy, Richard and Jublilee zones within a 4 km trend. Due to the complex nature of the vein sets the market has had a tough time connecting drill hole dots to visualize emerging ounce footprints, which was not helped by tight budgets during the past few years. But in 2020 a rising gold price prompted Galway to adopt a more aggressive strategy which now involves 5 drill rigs, 3 of them infill stitching together the Jubilee-Richard-GM segment with infill drilling which will become the basis for a resource estimate in Q1 of 2021, and 2 rigs "wildcatting" at the northern and southern limits of the infill focus. The open-endedness of this district play whose destiny Galway was controlling through geology smarts and drilling appealed to the market against the backdrop of a rising gold price, enabling Galway to raise $17 million in June 2020 at $0.44-$0.64 for common and flow-thru which boosted its treasury to $22 million, more than enough to carry its strategy well into 2021. On June 24 Galway reported 0.5 m of 186.5 g/t gold (6 opt) for hole #38 at the southern end where there seems to be a cross structure associated with a high gold in soil anomaly. On July 29 Galway reported that hole #65 drilled as an expansion hole to the NE of the George Murphy Zone unexpectedly intersected repeated visible gold over 14 m d=near the bottom of the hole. When you look at the geological context, #65 appears to have intersected a new zone parallel to the Jubilee-George Murphy trend which itself flanks the southeastern margin of a granite intrusive which is 400-500 m wide where it outcrops and about 2,000 m long. No holes have been drilled on the northern flank. So for the moment the market is wondering if hole 65's VG interval is evidence of a mirror trend on the other side of the granite intrusive. Although Galway describes its 2 rigs as "wildcatting", this is not the same as testing isolated targets elsewhere on the property, if which there are plenty with geochemical support. These wildcat rigs are groping beyond the known mineralization, which makes it unlikely that Galway will pull a job dropping discovery hole signaling a major new zone. That suits the current market fine, because despite the awakening bull, it remains fearful that all will soon enough end, so a district play undergoing a major rethink that incrementally keeps getting better suits the market just fine. (Jul 29, 2020)

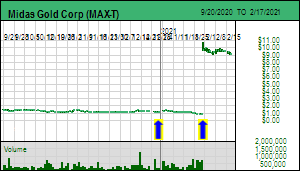

Midas Gold Corp has been a regular Discovery Watch feature since January 2017, not because there was any new mineralization to be discovered at the Stibnite gold-antimony project in Idaho, but rather because we were curious to discover if CEO Stephen Quin with John Paulson's financial backing in early 2016 could overcome the market's glum view that Idaho would never permit an open pit mine in an area that was turned into an environmental disaster zone by mining for antimony to support the World War II effort, and later by gold miners who were no longer around when Nixon invented the EPA in the 1970's. And boy oh boy, has it ever been a journey of discovery with regard to regulatory incompetence led by the Forest Service as the timeline for a draft Environmental Impact Statement kept slipping into the future like that Steve Miller song. Midas as of the end of 2019 has spent USD $53 million on permitting out of $210 million overall, and CEO Stephen Quin has suggested to me the total will be $70 million when a mining permit is finally granted. The last economic study was a PFS in December 2014 which was lousier than the 2012 PEA because certain parts of the deposits lacked the drill density needed to support a PFS calibre ore schedule, so half the antimony output disappeared, as did a good part of the high grade front loading of the ore mining schedule. The outcome of the PFS was not impressive because it used a $1,350 gold price as a base case to support an after tax NPV of US $832 million and 23.4% IRR using a 5% discount rate. The IRR was fine, but the NPV not so good because CapEX was $970 million thanks to a pressure oxidation unit needed to deal with the refractory sulphide ore. But even worse, gold was below $1,300 most of the time until mid 2019 when it finally began to rise as the world became uncertain about America's leadership role in a world where China under emperor for life Xi Jinping had since 2012 embarked on a course that clearly dashed any hope that China's prosperity would eventually make it "just like us", even as the US under its own leadership was setting America on a path to become just like "them". One reason the timeline for a draft EIS kept being extended was that the Forest Service simply lacked the processing infrastructure to permit a mine that would produce 350,000 ounces gold annually, turning this into a learning how to properly approve a mine on the fly experience. The other reason was that Trump's deregulatory zeal was undermined by strategic incompetence that inflicted an unnecessary government shutdown and which later enabled the Wuhan Virus to become the self-gutting America Virus. But it finally looks like a draft EIS is on track to be accepted in August 2020, which will be followed by a 45 day comment period during which objectors opposed to mining will try to demonstrate that the Forest Service and related agencies are too incompetent or corrupted to have done their job properly. Knowing the quality of the Midas team and the sincerity of the regulators to do the job properly to support a reclamation project bankrolled by a gold mine, these comments should not prove more than fodder for late night comedy, enabling Midas to publish a feasibility study in Q4 of 2020 which incorporates the cost of all the changes generated by the permitting process. A record of decision is expected in late 2021, namely a permit to proceed with construction of the Stibnite Mine whose antimony by-product will bail America out of a serious security of supply problem should the escalating "new cold war" with China disrupt the supply of raw materials in which China dominates. At $1,900 plus gold Stibnite will be very much in the money, even if CapEx expands 30%, and if you dare to dream $3,000 gold, you are looking at a $10-$15 future price target. (Jul 29, 2020)

Disclosure: JK does not own any of the companies mentioned; Azimut and Galway are Fair Spec Value rated Favorites, Midas is a Good Spec Value rated Favorite