| Kaiser Watch October 21, 2022: Update on May 2022 MIF Picks |

| Jim (0:00:00): In May you presented 5 companies at the Metals Investor Forum in Vancouver. How have they fared in the current bear market for juniors? |

When we talk about TSXV juniors these days we have to distinguish between resource and non-resource listings. When I started working in the sector in 1983 resource juniors ruled, but that decade the VSE quickly became ruled by non-resource listings. By the 1990s regulatory reforms had shifted the balance back to resource listings, and, after the Bre-X debacle, the 43-101 reforms set the stage for resource juniors to benefit from the China super-cycle which shifted the focus from discovery exploration to feasibility demonstration. I have TSXV value traded data back to 2000, but I am only able to differentiate value traded between resource and non-resource listings from 2009 onwards. Thes TSXV Index created in 2001 initially reflected the resource listing skew of the TSXV, and in the first graphic below which depicts the traded value of all TSXV listings the performance of the TSXV Index you can see a strong correlation bwteeen the daily traded value and the performance of the index until about 2013 by when the resource listings had settled into a decade long bear market. When you look at this chart you see modest TSXV Index fluctuations since 2016 but two major value traded spikes in Q4-2017:Q1-2018 and Q1 2021.

The TSXV Index is a misleading indicator because it represents only 10% of listings, and their composition is constantly adjusted to reflect company market capitalization, with a selection mechanism that preserves the value of ousted members. At this stage the composition is roughly 50:50 between resource and non-resource listings. Given the completely different market dynamics, the TSXV Index is useless, not because its 50% decline from the peak in early 2021 exaggerates the performance, but rather because it understates how hideously negative TSXV listings as a group have performed. The second set of graphics keeps the TSXV Index but isolates the resource and non-resource listing traded value. The daily value traded scale on the left is the same for both charts, which allows you to see that since the 2009-2012 post crash rebound the TSXV non-resource listings have experienced two major capital inflow booms while the resource listings had a modest awakening in 2016-2018 and a somewhat better capital inflow in 2020-2022. It is important to understand how uninterested the market has become in non-resource TSXV listings this year. The third and fourth charts show on a long term and short term scale the relative percentage of traded value. The value traded value bars are stacked so it is not easy to see which is dominant, but the relative percentage line charts (red non-resource, yellow resource) clearly show which group was dominant.

The crossover to non-resource listing dominance began in 2012 and persisted except for a brief period in 2020 when gold charged through $2,000 in the wake of the Covid response. But a major crossover in favor of resource listings took place in December 2021 and it persists to this day. Both groups are suffering dwindling daily traded value, but the decline in non-resource listing traded value is much worse than for resource listings. Intuitively, when you consider that cannabis and and cryptocurrency related listings were dominant themes during the past decade, this reversal makes sense. KRO, however, only covers resource listings, so while it is nice to see cannabis and crypto stories fade away, the more important question is where are the resource juniors headed?

The final chart of this collection groups TSX and TSXV resource companies into price ranges, of which the most important one is the % of stocks trading below $0.10, a level which means nothing on the ASX, but which on the Canadian exchanges has historically represented companies headed for extinction as a defunct delisting or a rollback that wipes out existing shareholders. This graphic shows how hideous the decline was from mid 2011 until late 2015 when 66.1% of resource listings traded below a dime. There was a modest resource rally in 2016-2018, but that reversed in mid 2018 and hit a nadir at 53.7% in March 2020 during the Covid meltdown. The gold rally and general hysteria in early 2021 pulled up resource listings so that only 22% were left stranded in purgatory. Since then the trend has reversed, and has accelerated in 2022, with currently 41.5% trading below a dime. My prediction is that this percentage will be much, much worse by the end of 2022. In fact, we are facing a monster house-cleaning event in December as shareholders assess the resource juniors left in their portfolios and dump everything that does not reveal a committed management with a plausible long term story. The point of this KW Episode is to assess my five May 2022 MIF picks in terms of how they will be dealt with by the coming capitulation. |

Long Term Chart of TSXV Index and Daily Traded Value for All Listings |

Comparison of TSXV Value Traded between Resource and Non-Resource Listings |

Long Term Chart of Relative Traded Value of TSXV Resource and Non-Resource Listings |

Short Term Chart of TSXV Resource and Non Resource Realtive Traded Value |

Relative Performance of Cdn Resource Listings in terms of Price Ranges |

| Jim (0:06:17): Let's start with P2 Gold, one of your KRO Favorites which is working on the Gabbs copper-gold project in Nevada. What is needed to reverse its downtrend? |

At the end of 2021 I introduced a new concept where I would create a collection of KRO Favorites which weren't missing any pieces for success like those resource juniors I tag with a Bottom-Fish rating, and make them available on an unrestricted basis to the public. The 2022 Favorites featured only 8 companies, of which P2 Gold was one. The idea was that individuals would pay $450 per year to get access to the research platform and my collection of Bottom-Ftagged juniors which needed to secure some missing piece in order to develop an uptrend. As these pieces fell into place I would convert them into a KRO Favorite, ideally after the stock had risen several times from its bottom-fish equilibrium level. What a terrible year to launch this initiative!

At first it worked well, with the group gaining 32.8% by April, but since then it has been downhill, bottoming down 39.4% in September and currently limping along at down 33.9%. Worse, or perhaps fortunately so, I have not felt it necessary to add any bottom-fish graduates during 2022. Gold is down 9.7% so far this year, and the TSXV Index is down 36.8%, but it is no consolation that the 2022 KRO Favorites Index is down slightly less than a market index which is 50% polluted by non-resource juniors which we know have done much worse than resource juniors. The table below shows that only one KRO Favorite, Verde Agritech, is up for the year; the rest are down 31%-67%.

P2 Gold is down 59.6% thanks largely to how gold and copper have performed this year. Copper is understood as a proxy for the trend in the global economy, and despite all the talk about the demand boost required by the energy transition, a demand boost whose deliverability is not evident in the copper mine development pipeline, copper is not just signalling a macroeconomic downturn, but a failure of the energy transition dream. Or, more charitably, a disconnect between the market and projected reality. Gold is another matter because if Mr Goldfinger turned the 6.8 billion ounce above ground gold stock stored in vaults radioactive, it wouldn't change a thing in the way the real world operates, just as the flash evaporation of every Bitcoin wallet wouldn't. So what gold's price should be is anybody's guess, but in the case of copper it needs to be high enough to justify mining enough to make the energy transition a reality.

The flagship project of P2Gold is the Gabbs copper-gold project in Nevada for which the junior plans to deliver a PEA by the end of 2022. Early this year I created an outcome visualization which imagined a 20,000 tpd open-pit operation that simultaneously heap leached the higher gold grade oxide cap and milled the copper rich sulphide resource. At the time when gold was $1,900 and copper $4.50 the LOM DCF model just barely cleared development hurdles with the existing resource. But that didn't matter because what P2 Gold's Ken MacNaughton and Joe Ovsenek planned to do was create an optimized mining plan which heap leached the gold cap first and used the cash flow to fund the later CapEx to mill the the sulphides. Meantime the prices of gold and copper have declined sharply, such that my simplistic OV's outcomes are far below development hurdles. The question now is what have current prices done to the assumptions in the optimized PEA mining plan?

The market has given Gabbs a big thumbs down, which is only fair if you assume current metal pricing relative to costs represents the long term reality. But not if you consider that once the PEA is published, the clock starts ticking on a balloon payment to the vendor that is not in the bank. The vendor is Waterton, which as part of the Gabbs deal is the largest shareholder of P2 Gold. Ken and Joe have put serious personal money above the current market price into P2 Gold, so this is not an example of some deal where the principals got nearly free paper in a private company that was then folded into a shell. The value of the PEA will be that it establishes the optimal mining scenario for Gabbs and its underlying cost structure. It may not be viable at current gold and copper prices, but in the case of copper it is reasonable to assume that the future which depends on copper is not viable at the current copper price. Now if Waterton operates in the mold of the Carlsbad school where you always press your advantage, next year it will force a default, leaving it in control of a shell whose only asset is the Bam gold project in the Golden Triangle and a couple principals who put their money where their mouth was and upgraded the optionality value of the Gabbs project which Waterton scavanged during the bear market of the past decade.

The upside now hinges on Bam. During 2022 P2 Gold drilled 13,958 metres in 95 holes into the epthermal Monarch gold zone of which 59 holes are still pending. At the start of 2022 there was a plan to test the hypothesized feeder for this gold mineralization which required some deep holes. But weather delayed the geophysical surveys so the company has focused on shallower drilling designed to outline a near surface resource and provide zonation data which when correlated with the geophysical data will allow vectoring into the likely feeder target for testing in 2023. Bam has its own approaching vesting deadlines which may not be achievable if Waterton extracts Gabbs and tries to turn Ken and Joe into P2 Gold minions. So P2 Gold is in a sense a complex bet on how title to Gabbs will be established on a win-win basis. The wild card is that the remaining Bam results are so good that Gabbs becomes irrelevant as P2 Gold turns into a Golden Triangle gold discovery delineation story. |

P2 Gold Inc (PGLD-V)

Favorite

Fair Spec Value |

|

|

| Gabbs |

United States - Nevada |

4-Infill & Metallurgy |

Au Cu |

KRO 2022 Favorites Index |

KRO 2022 Favorites Performance |

P2 Gold Performance relative to KRO 2022 Favorites Index |

Long Term Charts for Copper and Gold |

Gabbs outcome Visualization Charts |

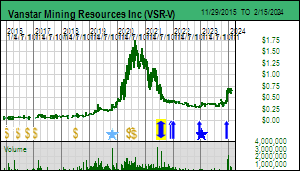

| Jim (0:10:24): Vanstar is an advanced gold resource junior that is trending lower. Is Vanstar's future still tied to that of partner IAMGOLD? |

Vanstar was invited to the May 2022 MIF because on the one hand it had a carried 20% interest in the Nelligan gold project in Quebec for which an open-pittable resource of 3.2 million oz had been established by IAMGOLD in 2019 at 1.02 g/t, and on the other hand it had secured an option on the Bosquet project near IMG's underutilized Doyon mill which allowed Vanstar to chase the down plunge potential for blossoming gold zones which IMG had ignored when it looked for a quick-fix open-pittable feed for its mill. Vanstar still has Bosquet assays pending, but there is no body language suggesting that anything special has been intersected at depth. The option commitments are such that Vanstar can think about Bosquet for much of 2023 while it waits to see what IMG does next with Nelligan. Since 2019 IMG has done a fair pit of drilling to extend the deposit to the west and it is planning an updated resource estimate by the end of 2022. The market would like to see the resource grind above 5 million ounces without too much decline in grade, but an increase to 4 million should be a more reasonable goal, especially given that there are still some drill density holes within the the mineralized footprint that may limit what IMG delivers later this year. In 2021 I created an outcome visualization based on the FS cost assumptions of the similar Springpole project of First Mining Gold. This 30,000 tpd open-pit scenario yields a 9 year mine life and CAD $914 million after-tax NPV at 8% using $1,643 gold, which implies a fuiture $2.82 price for Vanstar, a tenth the current valuation.

The problem is that IMG is a distressed company following a CapEx blowout this year at its Cote gold project in Ontario. However, during the past week it reached a deal to sell its Rosebel gold mine in Suriname to the Chinese miner Zijin for USD $360 million, which the creditors approved provided the money is allocated to Cote. On the one hand this means IMG lives to see another day, but on the other hand it means Nelligan sits on the sidelines. IMG still owns the Essakane gold mine in Burkina Faso, a country in the Sahel where the predations of jihadis have resulted in several recent military coups. Now there is talk of recruiting the Russian mercenary Wagner group to keep the peace, which really isn't a good scenario for western operators, but good for Chinese companies courtesy of the Russia-China axis Putin and Xi forged ahead of Putin's invasion of Ukraine. So my hope is that IMG also sells Essakane for a pretty penny which allows it to make complete a retreat to Canada as its primary operating jurisdiction. Its next best project is Nelligan, so if this were to happen, the market's doubts about the timeline for Nelligan's development and an eventual buyout of Vanstar's stake, possibly at ten times the current market price, would ease. Given that Vanstar is carried at Nelligan, I see this as a classic long term asset play. |

Vanstar Mining Resources Inc (VSR-V)

Bottom-Fish Spec Value |

|

|

| Nelligan |

Canada - Quebec |

4-Infill & Metallurgy |

Au |

Outcome Visualization Charts for Nelligan |

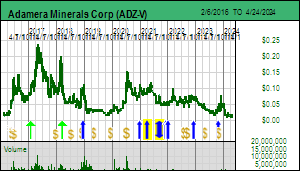

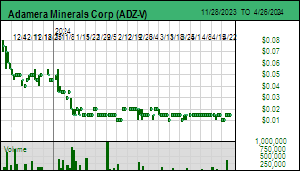

| Jim (0:15:49): Adamera Minerals is a gold discovery focused exploration junior. Is it any closer to making a discovery? |

Adamera Minerals has its origins as a diamond explorer in the Canadian Arctic which split itself to also engage in uranium exploration during the 2004-2008 bubble. But in 2012 Mark Kolebaba recombined the companies and changed the focus to gold exploration in northeastern Washington where high grade gold mines in the Republic Graben had shut down. This became the Cooke Mtn project which ADZ tackled with a new round of geophysical surveys designed to detect skarn hosted sulphide bodies overlooked by past exploration. While tidbits were intersected such as Oversight, nothing grew into a meaningful discovery. In 2020 the Peruvian high grade miner Hochschild optioned the project with the idea of applying a deeper form of IP surveys. This led to some promise on the Lamesfoot South claim, but Hochschild dropped out in 2022.

This year ADZ drilled several more holes which yielded high grade gold over short intervals less than 1 km from the depleted Lamefoot deposit from which Echo Bay underground mined 1 million oz at 8 g/t. The market has largely ignored this development, partly because it has been fooled before by such intervals, but also because it is hard to believe Echo Bay would have missed anything so shallow nearby. However, these zones are rod like and you need to get lucky to tag into one. We will have to wait to see if additional drilling fleshes out the zone or makes it disappear. So the100% owned Cooke Mtn story may undergo a revival.

But the real story is Buckhorn 2.0, the original land position Kinross assembled around its Buckhorn Mine lease. Crown Resources Corp discovered the Crown Jewel deposit in 1988 and initially tried to develop it with Battle Mtn as an open pit mine, but that went nowhere in Washington. Kinross acquired Crown in 2006 and developed Buckhorn as an underground mine whose ore it trucked to the 2,100 tpd Kettle River mill in the Republican Graben area where the Cooke Mtn claims are. Buckhorn produced 1.3 million oz at 13 g/t from 2008 until 2017 when it ran out of ore. Located in the Torodo Graben this skarn deposit was the only mine to emerge despite a century of groups poking around the gold teases at surface in the surrounding area.

Kinross assembled a 3,600 ha land package around the Buckhorn lease and drilled 281 shallow holes for 50,250 m mostly to the east. As Buckhorn's depletion approached Kinross filed a monster plan of operations with the USFS in what was going to be a massive search and destroy mission in the surrounding area. It hit a wall, Kinross gave up, and by 2020 had let all the claims lapse except the mining lease for whose reclamation it remains responsible. With Cooke Mtn optioned to Hochschild Kolebaba staked the entire former land package in 2020 and began to conduct geophysical surveys. In 2021 Adamera was able to strike a data deal with Kinross that gave ADZ access to all the historical data outside the lease. The company has been busy integrating these data sets and supplementing it with new data sets such as a Lidar survey which has helped reveal where prospectors ages ago beavered away. Buckhorn 2.0 straddles 3 permitting jurisdictions: State, BLM and USFS. Drill permits have been secured for the State and BLM portions and this summer ADZ began drilling geophysical targets on these claims. The best targets, however, sit on the USFS land and ADZ is still waiting for these permits which seem imminent but always slip into tomorrow.

This week ADZ announced that it has intersected sulphides in the first three targets, which the market liked somewhat because the gold in the Buckhorn skarn deposit is associated with sulphides, a necessary condition, but not a sufficient condition. The true significance of the news is that the geophysical targets are being validated by drilling and we can now hold our breath for assays. Buckhorn 2.0 will be a process of elimination drill strategy seeking a zone that has running room. I have created an outcome visualization of what Buckhorn 1.0 would be worth today if underground mined at 900 tpd with the ore trucked to the Kettle River mill which is mothballed. The AT NPV at 8% is CAD $920 million which translates into a future price target of $3.48. The size of this prize has not been negatively impacted by the recent decline in the price of gold, so Adamera Minerals remains a Bottom-Fish Spec Value rated junior with siginficant discovery exploration upside potential. What is important is that exploration is being done in the same geological context as Buckhorn 1.0, so if ADZ starts hitting a similar zone, the market is primed to understand the upside implications. It is also helpful that Crown alumni such as Mark Jones and Chris Herald have joined the board. |

Adamera Minerals Corp (ADZ-V)

Bottom-Fish Spec Value |

|

|

| Buckhorn 2.0 |

United States - Washington |

2-Target Drilling |

Au |

Relative Location of BUckhorn 2.0 and Cooke Mtn Project areas |

Graphic showing structural axis of new Lamefoot South Zone |

Google Earth shot of new Lamefoot South zone relative to depleted Lamefoot deposit |

Comparison of Buckhorn Drill History with Gold Geochemical Data |

Outcome Visualization of original Buckhorn Mine |

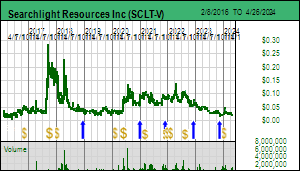

| Jim (0:20:42): Searchlight Resources is a Saskatchewan focused junior with exposure to a wide range of metals. Is it any closer to delivering a discovery? |

Searchlight Resources is a Saskatchewan focused junior headed by Stephen Wallace and Alf Stewart which started off assembling a gold district callled Bootleg Lake west of the Flin Flon VMS mining camp but has more recently branched into Saskatchewan's critical metals potential with Kulyk Lake as the current flagship. The idea at Bootleg Lake was to consolidate the fragmented ownership and start chasing the high grade orogenic veins down plunge to see if they blossom at depth. But market interest in such plays has stalled. Kulyk Lake has a high grade rare earth showing discovered decades ago and studied by academics but never drilled. During the 2009-2012 Rare Earth Mania 1.0 Eagle Plains staked it and cut a number of maximum 1 m wide trenches across the monazite showings. A table of the results is provided below. I have averaged the trench values and generated a REO distrbiution chart which also includes the in situ value distrbution based on current rare earth oxide prices.

The REO distribution is typical for monazite with 97.4% light rare earths. 85% of the $4,491/t rock value resides in neodymium and praseodymium, the light rare earths used for permanent magnets. The average grade of 16.59% TREO is meaningless - a 0.6 m trench averaged 45.1%. Kulyk Lake has never been drilled because the monazite appears to occur as narrow seams tracking Kulyk Lake. To turn this into a mine one needs to develop a multi-million tonne zone that can be open-pit mined. Such a deposit needs to grade 3%-6% to be worth developing, which translates into a rock value of $800-$1,000 of which only 85% in the form of Nd and Pr is worth recovering.

In 2021 Searchlight conducted a radiometric survey over the Kulyk Lake trend in an effort to use thorium to assess the potential scale of the monazite mineralization. The thorium data revealed a 6 km trend on the northwestern flank of Kulyk Lake which also repeats itself a km to the northwest. The survey also collected uranium data and revealed a sizable uranium anomaly to the southwest of the thorium anomaly. This got the company excited last year while the uranium bugs were flexing their muscles because it was large and unexpected. Field visits this summer have revealed that this is a pegmatite hosted system grading less than 0.1% U3O8 similar to the Rossing deposit in Namibia. This target will need a drill program to see if it represents a bulk mineable resource. The company has also done several sampling passes over the thorium anomaly and is still awaiting results.

The market question is whether or not a case can be made for drilling the rare earth target in 2023 to see if the monazite seams can average out into a mineable zone. As such Kulyk Lake does not yet qualify as an "emerging discovery" but it remains intact as a story. The Saskatchewan Research Council has created a pilot plant to process monazite samples as part of an initiative to develop rare earth expertise, so if there turns out to be size and grade at Kulyk Lake it could quickly become a big story.

The latest development that intrigues me is some staking SCLT did this week in an area north of Hanson Lake west of Flin Flon where SCLT owns claims covering a cluster of LCT pegmatites whose grade and size do not appear overly interesting. The junior optioned them to a private party earlier this year which was interested in the VMS potential. I grumbled about that to Stephen and Alf at the May MIF, and asked why does Manitoba have good lithium pegmatite potential and not Saskatchewan. Stephen mumbled that Hanson Lake seems to be the best documented, but did digest my argument that Lithium Mania 2.0 is based on the idea that the economic irrelevance of LCT pegmatites until the past decade discouraged exploration and that the documented showings were largely a result of prospectors doing a face-plant onto a whitish outcrop. Being GeoDataGeek he couldn't resist going through the data archives in search of potential pegmatite fields that were not recognized as such. An area north of Hanson Lake caught his interest, but it was already owned by parties looking for something else. These claims lapsed this year and the MARS system opened them as part of a monthly opening of lapsed claims. Wallace didn't have any competition so got what he wanted, and is now awaiting title confirmation before announcing the acquisition. He cautions that while he is confident a pegmatite field is present, he has no data indicating that they are LCT enriched because nobody appears to have bothered sampling antyhing in this area. At this point the Hanson Lake North pegmatite play is a longshot, but it is an example of the Great Lithium Rethink now underway which could be transformative for toiling geologist style juniors. |

Searchlight Resources Inc (SCLT-V)

Bottom-Fish Spec Value |

|

|

| Kulyk Lake |

Canada - Saskatchewan |

2-Target Drilling |

U REM |

Location map of Searchlight's Saskatchewan Projects |

Kulyk Lake Thorium Anomaly and Photo of Monazite Outcrop |

Table of Kulyk Lake Trench Results collected in 2009-2012 by Eagle Plains |

Rare Earth Content and Value Distribution of Monazite at Kulyk Lake |

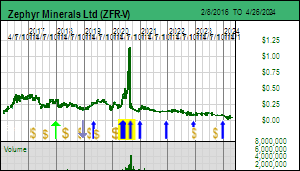

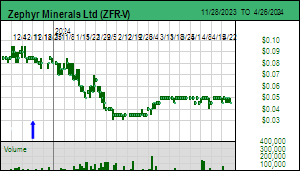

| Jim (0:26:28): Zephyr Minerals is trying to establish itself as a gold junior in Zimbabwe. Is it any closer to doing so? |

Zephyr Minerals was invited to my May 2022 MIF session because in 2021, building on management's international experience, the company decided to investigate the gold potential of Zimbabwe which after decades of misrule by Mugabe had transitioned from autocracy to democracy and reformed its mining law so that foreign countries can have majority ownership of future mines. Zimbabwe has a century long history as a gold producer thanks to the orogenic gold systems in its Archean craton's greenstone belts. But when Mugabe took control decades ago commercial gold mining dwindled and most of Zimbabwe's gold production came from artisanal workers chasing the high grade structures down to the water table. Consequently Zimbabwe missed the boat during the past two decades enjoyed by West Africa where mining companies acquired the near surface depleted workings of artisanal workers and evaluated the systems as lower grade open pit mining opportunities.When Zimbabwe changed is mining law in 2020 there was a rush of companies led by Australians to apply for "exclusive prospecting orders" or EPOs, most of which were granted by early 2022. Zephyr was part of the second application wave in mid 2021 and hoped to have its 2 EPOs granted by this summer. However, it is still waiting for approval but seems to think this may finally happen in November. The stock meanwhile has languished because until it has the EPOs granted it only has a pending story.

But something else is happening in Zimbabwe As juniors are discovering in Newfoundland, pegmatite trends often occur parallel to gold mineralization trends. Back in May Loren Komperdo wasn't much interested in lithium, but since then the idea of Lithium Mania 2.0 has gained momentum. In fact, there is a new wave of EPO applications in Zimbabwe targeting pegmatite fields. During the middle of the past century Zimbabwe was the biggest lithium producer in the world because its pegmatites tend to feature both petalite and spodumene lithium mineralogy. But only the petalite zones were mined because they have the purity required by the main users at the time, the glassware and ceramics industry. The spodumene was ignored. Lithium demand picked up in the 1990s thanks to lithium ion batteries in electronic equipment such as laptops and cell phones. But around 2015 Lithium Mania 1.0 kicked in as the market realized that the car industry was embracing electic vehicles in response to climate change policy and the example set by Tesla. In 1995 lithium supply was about 10,000 tonnes lithium metal equivalent but by 2021 it had increased ten-fold thanks to EV battery demand. Now the projection is that by 2030 demand will increase another five-fold and ten-fold by 2035-2040 when EV sales are mandated to replace ICE sales. The carmakers are busy investing in GigaFactories to make batteries, and are now investing in refinieries outside China to make battery grade lithium hydroxide or carbonate from concentrates. While these facilities can be built quickly, the EV sector is now waking up the reality of the hideous 5-8 year timelines for finding and developing a new mine.

The Australian pegmatites and Lithium Triangle brines may only supply half of future projected demand. The rest may have to come from pegmatites in other cratons such as eastern Canada, Brazil, Scandinavia and Africa. Lithium Mania 2.0 is premised on the reality that if these future mines are to become reality by 2030, they need to be identified right now. Lithium Mania 2.0 is not so much about the M&A sweeping the lithium supply identified by Lithium Mania 1.0 during 2015-2017 and now in or close to production, but rather about an exploration boom during the next 2-3 years which will lead to feasibility demonstration, permitting and construction in 2026-2030. This is the ideal arena for resource juniors which, starting with very low market capitalization bases, have the potential to undergo 100 fold price increases very quickly if they find a large pegmatite grading 1% Li2O or higher.

In the case of Zimbabwe, ASX listed Prospect Resources Ltd acquired the Arcadia deposit not far from Harare during Lithium Mania 1.0 and brought it to the stage of an optimized feasibility study. Then in December 2021 it received an offer from Huayou Cobalt to purchase its 87% stake for USD $377.8 million. This deal closed in April 2022 and Prospect distributed AUD $0.96 per share as a special dividend and kept about $35 million to continue exploring for lithium on its Step Aside project in Zimbabwe and the Omoruru prospect in Namibia. Although the total resource was 72.1 million tonnes of 1.06% Li2O, the proven and probable resource was 42.3 million tonnes of 1.19% Li2O. This deposit has both petalite and spodumene zones. Zephyr's management has taken note of this development and the subsequent application rush, taken a second look at its EPO applications, and realized that one of them has a footprint which straddles both the targeted gold structure and a parallel pegmatite trend. So if this EPO gets granted, Zephyr will end up with a major "frontier" style land position in Zimbabwe that has both bulk tonnage gold and lithium pegmatite potential. |

Zephyr Minerals Ltd (ZFR-V)

Bottom-Fish Spec Value |

|

|

| Nyanga North |

Zimbabwe - Other |

2-Target Drilling |

Au |

Historical Gold Production by Zimbabwe |

Historical Lithium Production by Zimbabwe |

Historical Global Lithium Production |

Lithium Production by Country in 2021 |

Zephr's Exclusive Prospecting Order Applications in Zimbabwe |

| Disclosure: JK owns Adamera; P2 Gold is a fair Spec Value rated KRO Favorite; Adamera, Searchlight, Vanstar and Zephyr are Bottom-Fish Spec Value rated |