Hello Guest User, You are visiting this website from a computer with an IP address of 172.70.126.49 with the name of '?' since Tue Apr 16, 2024 at 2:55:14 PM PT for approx. 0 minutes now.

SV Rating: Bottom-Fish Spec Value - as of December 21, 2023

What's Next?

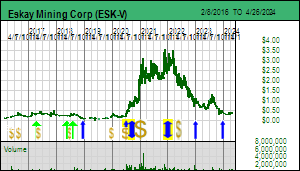

Updated September 18, 2020: Eskay Mining Corp was made a Bottom-Fish Spec Value rated Favorite at $0.215 on June 29, 2020 after CEO Mac Balkam cleaned up the balance sheet and raised $2.4 million to fund a major rethink of the SIB-Corey project in the Golden Triangle where efforts to find Eskay Creek 2 have been frustrated for decades (see Tracker June 29, 2020). The rethink initiative was launched in Q4 of 2019 when ESK brought Quinton Hennigh on board. He in turn recruited VMS experts John Monecke and John Dedecker to assist with a reinterpretation of the 25 km long property in the middle of a very prolific part of the Golden Triangle. This was a year after SSR dropped its 60% option on the SIB-Lulu portion after spending $8 million on a new approach based on the idea that the Coulter Creek Thrust fault coming from the east had decapitated the gold-silver enriched Lulu mudstone from the tilted VMS prospective Salmon River stratigraphy and displaced it westwards, an approach proposed earlier by Hennigh. Dedecker took a detailed look at the SSR drill data, confirmed that the subtle alteration on the SIB claim is indeed related to VMS style hydrothermal processes, and made the startling discovery that the Coulter Creek Thrust was backwards, rising from the west rather than the east and pushing younger Bowser Lake rocks over the Salmon River Formation. The past exploration goal was to find the Contact Mudstone which hosts the extremely rich 2.5 million tonne Eskay Creek deposit, but under the new Coulter Creek Thrust hypothesis this unit would be under the Bowser Lake sediments west of where all the drilling was done. The Lulu Zone mineralization was hosted by a "lower" carbonaceous mudstone unit into which fluids from a VMS feeder had bled laterally on their way to a seafloor vent at the Contact Mudstone unit (it is called "Contact" because it was buried by a post-mineral basalt flow) where something like the Eskay Creek deposit might have formed. So the potential for another Eskay Creek style deposit in the SIB-Lulu area just south of Skeena's property effectively remains untested. Once Dedecker figured this out, the question arose, how much else of the past exploration strategy was based on a misunderstanding of the geology? So in July 2020 Dedecker embarked on a program to relog and re-assay samples of the historic core stored in a warehouse, and then spent much of the summer at the SIB-Corey project visiting the known showings and remapping the geology. It turns out past exploration programs did not have a coherent understanding of the geology, and that the entire SIB-Corey project needed to be re-assessed, not just the SIB-Lulu area. This enabled ESK to raise an additional $3.4 million during the summer at $0.45 for hard and at $0.645 for flow-thru dollars. A decision was also made to fly a Skytem Mag-EM survey over the northern part of the property whose conductors were supposed to be the basis for a drill program, but bad weather prolonged this survey so that its final interpreted results will not be available until early October. IP surveys have also been done over selected targets but are only finishing now. Dedecker's digital compilation of the 30 holes drilled in 1995-96 on the Jeff and TV targets, gold bearing VMS style mineralized showings about 2 km apart, revealed that the past drill holes did not properly assess what appear to be stacked, east dipping lenses within a carbonaceous mudstone unit. A 3,000 m plus drill program began on August 21; a second rig was added in mid September when about 1,000 m had been drilled. The program is currently in a race against the weather with mid October projected to be the end of the season. Because the geophysical surveys took so long to complete Dedecker has designed a program of very small stepouts from the Jeff and TV zones in an attempt to establish their geometry and the geology of the area, which in turn will be used to calibrate the geophysical data for assessment in 2021 of new targets revealed by the Skytem survey. The company is not talking about the drilling program which will include some more aggressive holes in the 2 km segment between Jeff and TV, and, given the slow assay lab turnaround, we may not get a drill results report until late November. The north-south oriented footprint of the Jeff-TV zone is bigger than that of Eskay Creek, so there is room for a discovery hole during the 2020 season. But this summer's work will lay the foundation for a substantially bigger program in 2021 which may include deeper drilling in the SIB-Lulu area to test the revamped Coulter Creek Thrust hypothesis. Dedecker has also pointed out that field work highlighted other showings such as Spearhead, Tet, Cumberland and the intriguing C10 area which has a significant gold footprint that is not related to a VMS style hydrothermal system. Following the recent financing Eskay Mining Corp has 168.3 million fully diluted, which at $0.84 implies a $141 million value for the 100% owned portion, and $177 million for the 80% owned portion. An Eskay Creek clone would be worth CAD $4.7 billion today and under the rational speculation model that valuation is above the fair value channel for such an outcome, though for the 100% owned ground it is within the fair spec value range. Since Eskay Mining Corp has a meaningful exploration program underway at SIB-Corey, which will not exhaust the capital raised this summer, a Bottom-Fish Spec Value rating no longer applies. Accordingly effective September 18, 2020 Eskay Mining Corp is converted to a Fair Spec Value rated Favorite at $0.84. The Jeff-TV drilling has the potential to deliver a discovery hole, and will most certainly deliver a better understanding of the mineralization in this area. In the absence of flashy drill results the stock will be subject to end of year seasonal pressure. The degree that the stock price remains resilient will hinge on the new exploration potential that this summer's "rethink" grunt work has unveiled.

Corporate Change History

#Old for New

Last Price

Prior Name

Subsequent Name

Details

Nov 19, 2001

Name Change

3:1

$0.03

Kenrich Mining Corp (KRC-V)

Kenrich-Eskay Mining Corp (KRE-V)

Nov 3, 2009

Name Change

1:1

$0.20

Kenrich-Eskay Mining (KRE-V)

Eskay Mining Corp (ESK-V)

Recommendation History

Edition

Date

Price

Recommendation

Gain

BF2016

4/12/2017

$0.31

New BF Buy $0.30-$0.49

-37%

BF2016

5/15/2018

$0.23

Confirm BF Buy $0.30-$0.49

-53%

BF2016

7/30/2018

$0.25

Confirm BF Buy $0.30-$0.49

-49%

BF2016

12/13/2018

$0.10

BF Technical Closeout 100%

-80%

SVF2020

6/29/2020

$0.22

Bottom-Fish Spec Value Favorite

0%

SVF2020

9/18/2020

$0.84

Fair Spec Value Favorite

282%

SVF2020

12/31/2020

$2.20

Fair Spec Value

900%

SVF2022

12/31/2021

$2.77

Fair Spec Value Favorite

0%

SVF2022

12/30/2022

$1.12

SV Technical Closeout 100%

-60%

Charts & Financing Activity

Most recent 43-101 resource estimate Prior resource estimate PEA PFS FS/BFS/DFS

Private Placement Key

less than $500,000

$1,000,000 - $2,000,000

$5,000,000 - $10,000,000

$20,000,000 - $50,000,000

$500,000 - $1,000,000

$2,000,000 - $5,000,000

$10,000,000 - $20,000,000

over $50,000,000

Private placement financing dates and value ranges are based on transactions reported by the TSXV Monthly Review.

Past Insiders and Reported Shareholders - Current Ownership Status unknown - positions may be pre-rollback

Related Party

Occupation

Related Since

Insider Ended

Director Ended

Capacity

Ownership

Jerry D. Blackwell

Geologist

9/21/2009

12/2/2009

12/2/2009

Director

0

Wally E. Boguski

Businessperson

8/31/1997

12/15/2009

12/15/2009

Director

389,666

Doug Chalmers

7/28/2010

9/12/2011

9/12/2011

Director

1,839,000

Art D. Ettlinger

Deceased

12/21/2010

1/1/2011

Advisory Board

0

David Hodge

Businessperson

12/21/2010

Advisory Board

0

Chet Idziszek

Geologist

3/1/2010

Advisory Board

0

David Mallo

Geologist

3/1/2010

Advisory Board

0

Robert A. Michor

Businessperson

4/26/1991

10/4/2010

10/4/2010

Director

225,441

Thal S. Poonian

Businessperson

10/8/2002

10/20/2009

10/20/2009

Director

0

Larry Riggin

Broker

6/1/2012

Placee

200,000

John Wilson

Broker

10/12/2011

Placee

500,000

Share positions of current insiders based on last AGM circular, ownership % based on current Issued. Share positions of past insiders and shareholders have not been adjusted for rollbacks or splits.

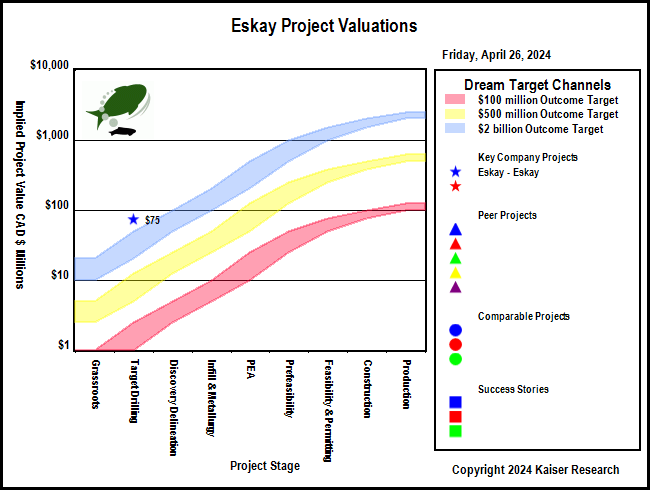

A Spec Value Hunter table allows speculators to identify which projects offer poor, fair or good speculative value according to the rational speculation model. The speculative value depends on the project stage, the project's implied value as calculated by the company's fully diluted, stock price and net project interest, and the dream target deemed appropriate for the project. A dream target is what a project would be worth in discounted cash flow terms once in production.

Poor Speculative Value -

Fair Speculative Value -

Good Speculative Value -

Note: narrow arrows indicate IPV is outside the fair value channel but within 25% of the fair value limits

Color Key for Target Outcome Achievability Ranges in millions ranked from most to least achievable

below $25

Should be Private: Artisanal, Placer, Mom & Pop Shop

$25-$50

Tiny Scale: underground mine or quarry - not worth the bother

$50-$100

Small Scale: junior needs to self-develop

$100-$250

Buyout Target: by Lower Tier Producers

$250-$500

Buyout Target: by Mid-Tier Producers

$500-$1,000

Ideal Target for Junior: Buckhorn, Sleeper

$1,000-$2,000

Almost World Class: Ekati, Red Chris, Brucejack, Juanicipio, Stibnite

$2,000-$5,000

World Class: Eskay Creek, Hemlo, Hermosa-Taylor, Oyu Tolgoi, LaRonde, McArthur

$5,000-$10,000

Giants: Escondida, Sullivan, Carlin Trend, Kidd Creek, Orapa, Kamoa-Kakula

above $10,000

Off the Scale District: Wits 1.0, Araxa, Sudbury Basin, Bayan Obo

The target outcome range required for the current implied project value to represent fair speculative value is based on the upper and lower certainty limits associated with the project stage. The color coding is based on the target outcome using the mid-point of the certainty range.

Active Company Projects

Project

Location

Net Interest

Stage

IPV $ MM

Fair Spec Value Required Target Outcome Range

$100

UPV $500

$2000

Target Metals

Deposit Style

Eskay

Canada - British Columbia - Golden Triangle

100% WI

2-Target Drilling

$74

$2,943 - $7,357

Gold Silver Copper Lead Zinc

VMS

North Mitchell

Canada - British Columbia - Golden Triangle

80% WI

2-Target Drilling

$92

$3,678 - $9,196

Gold

Epithermal Vein

Project Stage

Flagship

Secondary

Active

Grassroots (1) & Target Testing (2)

Discovery Delineation (3)

Infill Drilling & Metallurgy (4)

PEA (5) or PFS (6)

Feasibility & Permitting (7)

Construction (8) or Production (9)

Clicking on the project icon will display a popup identifying the company project, its stage and target metals, basic facts, a chart, a link to that project within that company's KRO Profile, a link to the most recent news release, and a link to the most recent KRO comment if one exists.

Net Interest: 100% WI Vested: Yes Uncapped NSR/GOR: 1.00%

Ownership Terms: Formerly called SIB-Lulu, combined with Corey project after ESK increased 80% interest to 100%. Option May 8, 2008 to earn 80% from St. Andrew's Goldfields (now Kirkland Gold) for $4 million exploration as well as 1,750,000 shares and $200,000 by May 7, 2012. Eskay vested on Jan 23, 2013. On Jan 26, 2017 Eskay optioned a net 60% to Silver Standard which can earn 51% by spending $11.7 million over 3 years, with $3.7 million in Y1, $4 million in each of Y2 and Y3. If the price of gold does not meet a minimum threshold in an option year the required spend is $2 million and the term is extended a year. Upon vesting for 51% Silver Standard can go to 60% by delivering a PEA or drilling 23,000 m. Kirkland Gold must fund its 20% share of expendeitures or dilute. If Kirkland dilutes to 10% its working interest converts to a 2% NSR. On Nov 9, 2018 SSR dropped the option after spending $7.7 million. Agreement Mar 25, 2021 whereby Kirkland Lake exchanged its 20% interest for a 2% NSR of which ESK can buy 1% for $3 million and has a right of first refusal on the remaining 1%.

Target Metals: Gold Silver Copper Lead Zinc

Model: VMS

Stage: 2-Target Drilling

Notes on Eskay Project

This property encompasses 33,000 Hectares immediately adjacent to the prolific Eskay Creek mine owned by Barrick Gold.

Visualized Outcome: Eskay Mining - Eskay as Eskay Creek II

The SIB-Lulu property starts about 4 km southwest of the former Eskay Creek mine-site and covers the strike extension of the Eskay Rift stratigraphy. The Lulu Zone was intersected in 1991 about 3 km from the claim boundary and yielded 14 m of 14.4 g/t gold and 1,059.5 g/t silver within a siliceous carbonaceous mudstone similar to that which hosts the Eskay Creek deposit (2.5 million tonnes @ 43 g/t gold, 2,208 g/t silver, 5%-6% zinc and 0.7%-0.8% copper). Followup drilling failed to establish any strike or downdip extent to the LuLu Zone. Further work led to the conclusion that the Lulu Zone is within the hanging wall of the Coulter Creek thrust fault which detached this tip from a possible iceberg within the footwall. This model drove SSR's $8 million drill program in 2017-2018 before it dropped the option in early 2019. The latest interpretation driven by John Dedecker, brought on board by Quinton Hennigh, is that the thrust fault is backwards, that in fact it is Bowser Lake rocks that have been thrust from the west over the tilted stratigraphy and that the Lulu zone is a feeder zone in the footwall of the contact mudstone that hosts Eskay Creek, whose projection under Bowser rocks is untested. The mudstone host of the Lulu mineralization has been a red herring because it is an older horizon that would be beneath the mudstone that evolved a VMS system similar to Eskay Creek. The rethink QH's team launched in 2020 now posits a previously unrecognized 25 km strike of prospective VMS stratigraphy reaching all the way to the Cumberland-Tet targets which are on the 100% owned Corey claims. A key focus in 2020 will be the Jeff-TV area which is on the 80:20 JV with Kirkland Lake. The Eskay Creek stratigraphy has been fault displaced eastward in this area. The purpose of this OV is to demonstrate what the discovery of another Eskay Creek deposit would be worth.

Source Note: The Eskay OV is based entirely on the Eskay Creek deposit discovered in 1989 and turned into an underground mine in 1995 which initially direct shipped ore to smelters in BC and Japan. The mine operated until Barrick shut it down in 2008. It produced 3.5 million oz gold and 180 million oz silver. The cost assumptions are based on historical data Barrick provided in 2004 when the mine was operating at about 700 tpd.

Visualized Outcome Summary: Eskay Mining - Eskay as Eskay Creek II

LOM Payable: 3.2 million oz gold, 165.0 million oz silver, 249.0 million lb zinc, 38.9 million lb copper

Economic Outcome (USD): Revenue Model at OV designated Metal Prices

Annual Average

Life of Mine (LOM)

LOM Stats

Recoverable Revenue:

$1,332,613,060

$13,039,266,729

$5,216/t ore Recoverable Value:

Smelter/Transport Costs:

($31,677,601)

($309,956,953)

2.4% of Recoverable Revenue

Gross Payable Revenue:

$1,300,935,459

$12,729,309,775

97.6% of Recoverable Revenue

Royalties:

($13,009,355)

($127,293,098)

1.0% of Gross Payable Revenue

Net Payable Revenue:

$1,287,926,104

$12,602,016,677

96.6% of Recoverable Revenue

Mining Cost:

($35,770,000)

($350,000,000)

24% of OpEx - $140.00/t ore

Processing Cost:

($105,010,500)

($1,027,500,000)

70% of OpEx - $411.00/t ore

Other Cost:

($6,643,000)

($65,000,000)

4% of OpEx - $26.00/t ore

Sustaining Cost:

($2,500,000)

($25,000,000)

2% of OpEx - $10.00/t ore

Total Operating Cost:

($149,923,500)

($1,467,500,000)

12% of Net Payable Revenue - OpEx - $587.00/t ore

Pre-Tax Cash Flow:

$1,138,002,604

$11,134,516,677

88% of Net Payable Revenue - $4,453.81/t ore

Taxes:

($394,412,023)

($3,862,080,837)

35% of Pre-Tax Cash Flow - $1,544.83/t ore

After-Tax Cash Flow:

$743,590,582

$7,272,435,840

58% of Net Payable Revenue - $2,908.97/t ore

Note: Concentrate transport costs, smelter treatment costs and retention are subtracted from recoverable revenue to get gross payable revenue to which the uncapped royalty rate for the project is applied. The annual average of LOM sustaining cost is expensed as an annual operating cost. Annual average figures reflect full production years.

Economic Outcome (USD): Royalty Model for 1% NSR at OV designated Metal Prices

Mine Life:

10 years

Startup

NPV 5%

NPV 10%

NPV 15%

Annual Avg NSR:

$12,879,261

Now

$93,093,524

$70,971,442

$55,611,066

LOM NSR:

$126,020,167

2021

$107,767,390

$94,462,990

$84,577,480

Economic Outcome - Discount Rate: 9.5% - CAD AT NPV: $5.7 billion - Fair Speculative Value

Gross Rock Value (USD/t):

$5,494

Recoverable Rock Value:

$5,216

Payable Rock Value:

$5,092

LOM Net Payable Revenue (USD):

$12,602,016,677

LOM PT Cash Flow (USD):

$11,134,516,677

LOM AT Cash Flow (USD):

$7,272,435,840

USD Pre-Tax NPV:

$6,343,581,738

Pre-Tax IRR:

1,138.0%

Pre-Tax Payback:

0.1

USD After-Tax NPV:

$4,114,260,065

After-Tax IRR:

746.7%

After-Tax Payback:

0.1

CAD Fair Spec Value Low:

$56,628,676

CAD Fair Spec Value High:

$141,571,689

CAD Implied Project Value:

$73,565,008

Price Target if Visualized Outcome delivered by Expl-Dev Cycle without dilution: CAD $28.48

Fair Speculative Value Stock Price Range: CAD $0.28 - $0.71

MSV (Market Cycle S Curve): Market Speculative Value represents the typical market pricing pattern of a new discovery as it moves through its exploration-development cycle. The irrational pricing behavior of the yellow channel contrasts with the fair speculative value of the blue channel as defined by the rational speculation model because during the pre-economic study stages there is great uncertainty about how big the discovery will turn out.

Fair Speculative Value Ladder

USD OV NPV

CAD OV NPV

Exch Rate

Diluted

Net Interest

$4,114,260,065

$5,662,867,553

1.3764

198,824,346

100.00%

Project Stage

Uncertainty Range

CAD FSV Range

CAD FSV per Share Range

CAD MSV per Share Range

Grassroots

0.5% - 1.0%

$28,314,338 - $56,628,676

$0.14 - $0.28

$0.28 - $0.71

Target Drilling

1.0% - 2.5%

$56,628,676 - $141,571,689

$0.28 - $0.71

$0.71 - $1.42

Discovery Delineation

2.5% - 5.0%

$141,571,689 - $283,143,378

$0.71 - $1.42

$1.42 - $21.36

Infill & Metallurgy

5% - 10%

$283,143,378 - $566,286,755

$1.42 - $2.85

$14.24 - $28.48

PEA

10% - 25%

$566,286,755 - $1,415,716,888

$2.85 - $7.12

$7.12 - $21.36

Prefeasibility

25% - 50%

$1,415,716,888 - $2,831,433,777

$7.12 - $14.24

$7.12 - $14.24

Permitting & Feasibility

50% - 75%

$2,831,433,777 - $4,247,150,665

$14.24 - $21.36

$7.12 - $14.24

Construction

75% - 100%

$4,247,150,665 - $5,662,867,553

$21.36 - $28.48

$14.24 - $21.36

Production

100%

$5,662,867,553

$28.48

$28.48 - $35.60

Market Speculative Value Stock Price Range: CAD $0.71 - $1.42

Warning: while the market spec value (S-Curve) and fair spec value channels presented in project value terms track the evolving expected ultimate outcome value, when presented in stock price terms the expected stock prices are subject to dilution through future equity financings or project interest farmouts.

Alternative Metal Price Scenarios

Metal 1

Metal 2

Metal 3

Metal 4

Gold

Silver

Zinc

Copper

Spot:

$2,344 /oz

$28.44 /oz

$1.29 /lb

$4.26 /lb

OV Assigned:

$2,344 /oz

$28.44 /oz

$1.29 /lb

$4.26 /lb

Pessimistic:

$1,300 /oz

$28.44 /oz

$1.29 /lb

$4.26 /lb

Optimistic:

$2,300 /oz

$28.44 /oz

$1.29 /lb

$4.26 /lb

Fantasy:

$3,000 /oz

$28.44 /oz

$1.29 /lb

$4.26 /lb

Note: for Metal 1 pessimistic, optimistic and fantasy price scenarios, OV assigned prices are used for Metals 2-4

Economic Outcomes with Alternative Metal Price Scenarios

USD PT NPV

USD PT IRR

USD AT NPV

USD AT IRR

AT Payback yrs

Spot:

$6,343,581,738

1,138.0%

$4,114,260,065

746.7%

0.1

OV Assigned:

$6,343,581,738

1,138.0%

$4,114,260,065

746.7%

0.1

Pessimistic:

$4,421,221,650

798.0%

$2,864,726,007

525.6%

0.2

Optimistic:

$6,262,210,051

1,123.6%

$4,061,368,468

737.3%

0.1

Fantasy:

$7,550,901,932

1,351.5%

$4,899,018,191

885.5%

0.1

Fair Speculative Value for Alternative Metal Price Scenarios

Stage: Target Drilling - 1.0% - 2.5%

CAD AT NPV

CAD Target Price

CAD FSV Range

CAD FSV per Share Range

CAD MSV per Share Range

Spot:

$5,662,867,553

$28.48

$56,628,676 - $141,571,689

$0.28 - $0.71

$0.71 - $1.42

OV Assigned:

$5,662,867,553

$28.48

$56,628,676 - $141,571,689

$0.28 - $0.71

$0.71 - $1.42

Pessimistic:

$3,943,008,877

$19.83

$39,430,089 - $98,575,222

$0.20 - $0.50

$0.50 - $0.99

Optimistic:

$5,590,067,560

$28.12

$55,900,676 - $139,751,689

$0.28 - $0.70

$0.70 - $1.41

Fantasy:

$6,743,008,638

$33.91

$67,430,086 - $168,575,216

$0.34 - $0.85

$0.85 - $1.70

Disclaimer: A visualized outcome is one of many possible outcomes for an exploration project as it moves through the 9 stages of the exploration-development cycle from grassroots to a producing mine with failure as an outcome at any point along the way. The range of possible outcomes for the physical nature of a deposit shrinks after delivery of an initial 43-101 resource estimate. While the nature of the deposit constrains the range of mining scenarios, the cost assumptions will vary as the project moves through the feasibility demonstration stages of the cycle, which affects the economic value of the final outcome. This economic value will also vary according to the prices of the metals targeted for extraction which may change during the years it takes for a project to become a mine. An outcome visualization is thus a compilation of best guess assumptions for the key variables that drive the discounted cash flow model, the basis for assigning an economic value to a mine. An OV is not intended as a prediction, but rather as a framework that allows the incorporation of new information generated by the exploration-development cycle for the project into a valuation model on an ongoing, dynamic basis.

Net Interest: 80% WI Vested: Yes Uncapped NSR/GOR: 0.00%

Ownership Terms: Option May 8, 2008 to earn 80% from St. Andrew's Goldfields (now Kirkland Gold) for $4 million exploration as well as 1,750,000 shares and $200,000 by May 7, 2012. Eskay vested on Jan 23, 2013. On Jan 26, 2017 Eskay optioned a 4,400 ha portion of the 80:20 JV to Silver Standard which can earn 51% by spending $11.7 million over 3 years, with $3.7 million in Y1, $4 million in each of Y2 and Y3. If the price of gold does not meet a minimum threshold in an option year the required spend is $2 million and the term is extended a year. Upon vesting for 51% Silver Standard can go to 60% by delivering a PEA or drilling 23,000 m. Kirkland Gold must fund its 20% share of expendeitures or dilute. If Kirkland dilutes to 10% its working interest converts to a 2% NSR. The remaining 28,600 ha are owned 80:20 by Eskay Mining and Kirkland Lake. To avoid confusion this group has been named SIB-Mitchell and the SSO farmout group is called SUB-Lulu.

Target Metals: Gold

Model: Epithermal Vein

Stage: 2-Target Drilling

Notes on North Mitchell Project

This property encompasses 33,000 Hectares immediately adjacent to the prolific Eskay Creek mine owned by Barrick Gold.