Hello Guest User, You are visiting this website from a computer with an IP address of 172.70.126.178 with the name of '?' since Thu Apr 25, 2024 at 9:10:49 AM PT for approx. 0 minutes now.

Kaiser Research Online is an information portal featuring all resource companies listed on the ASX, TSX, TSXV and CSE. Membership is available as an Individual Annual KRO Membership at USD $450 and as Multi-User Corporate Annual KRO Membership at USD $1,000. Use your Email to retrieve your login credentials if you have previously registered. See Membership Details for an overview of KRO.

The KRO Summary lists all Trackers and Blogs published during the designated weekly or monthly period so that so readers can easily catch up on what they may have missed. We no longer notify KRO members by email about new material except in special circumstances. When a Tracker is posted at KRO we notify members through the KaiserResearchOnline Slack Workspace. If you are an active KRO member and not registered on Slack, please let us know and we will send the invite. We will Tweet the link so that Twitter followers can catch up at their leisure. The title links to the Tracker or Blog, the charts in the Discovery Watch Blog link to the YouTube audio segment for that company, and the Tracker charts link to the free Corporate Profile. Blog content is unrestricted but Trackers are always restricted to KRO members unless one has been tagged to become unrestricted. Check the General Release Schedule to see which Trackers are already unrestricted or scheduled for general viewing.

Market says Clean Energy based Infrastructure Renewal Coming

October and November proved to be a difficult period for resource juniors with a precious metals focus as gold showed a greater bias toward a retreat than a definitive breakout beyond $2,000. Gold had peaked at $2,067 on August 6 and has been below $2,000 since August 18. On November 30 gold dropped to $1,762, testing the positive trendline which originates in late 2018, causing investors to fret that MacQuarie's $1,550 target rather than Goldman Sachs' $2,300 target would define gold during a Biden presidency. The market is haunted by the memory of the past decade.

During President George W. Bush's two terms US debt expanded by a record $6.1 trillion to stand at $12.1 trillion when President Barrack Obama took office, inheriting the fallout from the 2008 financial crisis. During Obama's two terms the debt expanded by a new record $7.9 trillion to $19.9 trillion when President Donald Trump took office, inheriting a strong economy that did not falter until early 2020 when he blew off the covid-19 virus as a hoax invented to make the stock market tank and steal his re-election for a second term. When Trump leaves office on January 20, 2021 the debt will stand at $25.1 trillion for a record single term $5.1 trillion increase. Even before President Elect Joe Biden takes office the White House Office of Management and Budget projects that the debt will expand another $3.4 trillion to $28.5 trillion during his term. Intuitively that should be good for a higher gold price, but when you look at a long term chart for gold, nothing is obvious about where gold is heading next.

The gold market has become wobbly because although the Democrats will control the House and Presidency in 2021, the Republicans will likely retain control of the Senate unless the Democrats win the Georgia run-off for 2 Senate seats. But even if they do, splitting the Senate with Vice-President Kamala Harris casting the deciding vote, there are enough fiscal conservatives among the Democrat senators that any major fiscal stimulus plan that would take the debt expansion well beyond what Trump has already carved into stone is unlikely to pass the Senate.

Gold investors have been pulling money out of the GLD and other gold ETFs since gold peaked in August. Given that gold jewelry consumption is down sharply in 2020 in places like India where celebrations such as weddings have been postponed by covid-19 restrictions, and official sector buying dried up in mid year when gold breached $2,000, it is surprising how well gold has held up in the face of a pending Biden presidency. The chart below depicts the cumulative above ground gold stock on an annual basis and the percentage held by the official sector at the end of each year. Official sector holdings tallied 49% in 1959 but stood at only 18.1% at the end of 2019.

Although the official sector has boosted its net gold holdings annually since 2009 following a lengthy net liquidation period from 1972-2008, adding 152.2 million ounces, as the chart below shows, but it has not been enough annually to increase its proportion of the above ground gold stock as the above chart shows.

We are potentially looking at a repeat of what followed the mid-term 2010 election when the Tea Party led Republicans gained control of the House and embraced a hard-line austerity stance which prevented Obama from launching infrastructure renewal to make America great again. In fact so hardnosed were the Republicans about fiscal conservatism that they were prepared to let the United States default on its debt my refusing to approve an increase in the statutory ceiling for federal debt, something that both political parties had historically rubber-stamped. Gold continued to trend up until peaking in August 2011, mainly in response to the monetary stimulus practiced by the Federal Reserve in the form of quantitative easing, effectively printing new money to buy illiquid debt paper from America's one-percenters and the pension funds that owned the retirement future of the 99 percenters. The GLD ETF gold holdings peaked at 43,511,415 ounces on December 7, 2012, but in 2013 both the price of gold and ETF holdings crashed when it became clear that the Tea Party debt ceiling extortion had killed any hope for Keynesian style fiscal stimulus by the Obama administration. Victory for the clarion call by gold bugs turned what was supposed to be the usual bear market of a few years for the resource juniors into a brutal decade long bear market that did not awaken into a bull cycle until 2020, though gold began its uptrend in early 2019.

A big mistake made by the likes of John Paulson of "Big Short" fame was to assume that the QE monetary stimulus as practiced by the Federal Reserve Congress would spawn inflation. But the reality was that annual inflation stayed between 0%-2% despite record low interest rates that in Europe even turned more than $15 trillion in sovereign debt into negative yielding Euro bonds. While debt, equity and real estate asset prices recovered during the past decade, the 99-percenters did not experience the second decade of the 21st century as the roaring teens, which became the basis for Trump's 2016 election victory. Ironically, his campaign platform included a promise to make America great again through infrastructure renewal, which is only possible through fiscal stimulus that creates long term debt, exactly what the Republicans had prevented Obama from doing, and which they gave Trump no leeway to make happen during the first two years of his term during which Republicans controlled all three branches of government.

When it is the Republicans in charge of spending, as they were during Trump's first two years when they controlled all three branches of government - the Presidency, House and Senate - the level of debt is not a problem. But when it is the Democrats, then Republicans rediscover their concern about rising debt. And they certainly will not be calling for higher taxes to bring down the debt, nor cuts to military spending and healthcare universal only for Boomers. They will push for cuts in all other areas and will absolutely refuse to support proposals for infrastructure renewal spending, especially any that benefits the Post-Boomer generations who are slated to inherit the consequences of climate change. They may even try out the debt ceiling extortion ploy again. Congress can suspend the debt ceiling, and has repeatedly done so on a temporary basis since February 4, 2013, including during Trump's term. The current suspension expires on July 31, 2021 when the debt ceiling will be defined as the level of debt on that date. However, given how the United States exploited the dollar's status as the single reserve currency to unilaterally impose sanctions on countries like Iran, and on companies working on the Nordstream II pipeline, giving the world extra reasons to find ways to avoid using the dollar might even cause the Republicans to think twice about pulling that stunt again.

When you consider that more than a third of federal spending goes exclusively to retirees whose ranks are swelling as the last Boomer marches into retirement in 2030, how can one avoid dreading a future clash between Boomers fighting any sacrifices during their End Times and Post-Boomers pushing back against the premature death of their future? In late 2019 I introduced the runaway tram problem as a way to depict this clash between the Post-Boomers personified by Greta Thunberg and the Boomers personified by Donald Trump, the first Boomer to hit retirement age. Trump's signature meme was that America had turned into a failure, that it was no longer great, that it needed to be made great again. But instead of pitching this idea to the Post Boomers, he harvested the End Times fear permeating the Boomers, and even packaged the climate change topic as a scam to inflict great sacrifice on the Boomers for the benefit of their Post-Boomer children and grand-children. Understanding this conflict is key to predicting how the future will unfold.

Donald Trump is a mean-spirited, cheating, lying, cynical, vindictive bully with a peculiar craven adoration of far more efficient thugs than himself, a sign of a destructive inferiority complex that would be merely sad if it was not that of the president of the United States. But clearly that did not bother just under half of the people who voted in the 2020 election. While a few may be just like him, and some simply viewed him as a necessary evil to advance their religious goals, many appreciate that he did hijack traditional "progressive" themes such as opposition to winner-take all free market principles applied at a global scale, military adventurism abroad, and neglect of social and economic resiliency that starts at home. The Democrats had ceased to be champions of these causes, making them rather indistinguishable from Republicans.

Had Trump paid attention to how China's autocrat Xi Jinping dealt with the virus once Beijing emerged from denial in January, and listened to America's medical experts about what was unfolding and how to deal responsibly with it, Trump might very well have been re-elected on November 3, 2020 even though the economy and market would have suffered during 2020 as he moved decisively to shut down the pandemic. Americans are not cry-babies. They can handle hardship if they understand that there is a purpose to it. And they will suspend their dogmas when it is time to assist each other against a common enemy. Instead we now have a situation where Christmas is being cancelled as the full October through April northern hemisphere flu season gets underway. He blew it and now he is behaving like a very un-American crybaby whose spell on his supporters will eventually dissipate as the United States and much of the rest of the world focuses on the great post-pandemic comeback. So even though it seems likely that the austerity history of the Obama period repeat will repeat itself during the Biden term and create another prolonged bear market for gold, is it possible that Americans may be ready to reject this false Clash of Generations? When you look at the graphic below which reveals that the vast majority of federal revenue is split between FICA taxes (green - social security) which is 7.65% of earned income up to $137,700 (employers pay half which for self-employed like myself means 100%), and individual income taxes, it becomes apparent that the employment future of Post-Boomers is expected to fund the twilight decades of the Boomers. If you are at the younger end of the Boomer age range like I am does not the runaway tram problem cause you some degree of discomfort?

The Spanish Flu, which originated from an American pig farm in early 1918 as migrating swallows dined on the overhead abundance of flies and shat into the swill troughs, killed only 675,000 Americans out of an estimated 50 million deaths globally out of 500 million people infected, or a third of the world population. According to John Hopkins University as of December 8, 2020 there have been 1,553,528 deaths out of 68,046,467 global cases of covid-19. Today the population is five times bigger, so covid-19 does not even come close to the devastation caused by the Spanish Flu. However, the Spanish flu went through two key mutation cycles. The first mutation made it more lethal, triggering outsized immune responses amongst robust individuals such as young people and pregnant women whose bodies were already primed to attack "invaders". Covid-19 is different in that its lethality exploits existing weaknesses such as poor health, obesity, age and having been immersed in the resource sector for way too long. Covid-19 has been described as a "Boomer Remover" that cascades concentrated wealth seemingly destined to make Boomers immortal into the hands of the Post-Boomers who have failed to flourish during the great neo-liberal backlash against Keynesian concepts of fiscal stimulus since 1980. As the super-spreader contagion created by the Sturgis biker rally in South Dakota rips through the Red States, there is a certain glee within the Post-Boomer generation whose members quite often asymptomatically blaze through a covid-19 infection. The second Spanish flu mutation made it less lethal, which helped end the pandemic and assured its remnant survival today. It is already known that the covid-19 strain currently infecting the world has a higher transmissibility than the original Wuhan strain. The fear that exploded in Q1 of 2020 was entirely justified when you consider the possibility of a mutation into a still very transmissible form whose lethality targets the young and healthy rather than the old and sickly. A smug sense of invincibility and schadenfreude is to be avoided. We are all in this together, whether or not for the moment we are high or low risk.

Covid-19 is not the new normal because now we have vaccines emerging to help us create synthetic herd immunity. Unfortunately it will not help us during the 2020-2021 flu season for large scale deployment is not possible before the summer of 2021. The markets seem to be looking beyond the 2020-2021 flu season, and embracing as an uptrend just about any theme (even uranium stocks are being pumped as a beneficiary of the post-covid green reality), but we are navigating a six month danger zone. The graphic above twins the DJIA of the roaring twenties with the past decade using a full calendar timeline and a normalized 100 index starting point. The uptrends leading to the September 1929 and March 2020 crashes have an eerie correlation, though by this point the 1929 Dow had begun the long term reversal of the post crash rebound while the 2020 Dow has made record highs during the past week. Is this time different? The greatest threat over the remaining five months of the flu season is that cases which require hospitalization will vastly exceed hospital capacity, with knock-on effects for people who require hospitalization for other reasons such as a car accident or heart attack. Vaccines will initially be deployed to health care and other front line workers who are most vulnerable to exposure and indispensable for helping the medical system deal with the covid-19 surge that will pound us through April. The potential for panic media headlines is very real, despite the claim of Canadian resource junior Trumpers that covid-19 will vanish as soon as Trump has vacated the White House. The joke question has been "do you know anybody who has caught covid-19, let alone died from it?" For most people the answer is no, but a yes answer is starting to proliferate. Furthermore, is anybody dumb enough to believe that when Trump is no longer in the White House his supporters in red states with ICU capacity full will continue to dismiss covid-19 as a liberal hoax? The market remains primed for a monster reversal like that of March 2020.

The fifth largest economy in the world, bigger than Canada and with a bigger population, encompassing a land mass smaller than British Columbia, has effectively cancelled Christmas. Everybody, including myself, is pissed. I spend the entire year in semi-isolation and now I can't have my children over for Christmas? But that's just me being a crybaby because I have done fine working from home rather than the office I continue to rent. The victims will once again be the Post-Boomers, the younger generations not squirreled away in a comfortable Zoom mediated home office. But this will be the proverbial "darkest before dawn" moment. When lockdown was imposed in March nobody had any idea how long and effective the sacrifice would be. The unemployment rate will skyrocket again, additional money will be doled out to keep the rental real estate debt market from collapsing due to non-payment of rents, and once Biden is the White House we will see what he comes up with for life after the covid pandemic. Survival is our focus while our hope is that covid-19 does not mutate into a far more lethal form that is "immune" to the current vaccines.

Maybe the markets will endure the misery of the next 5 months with a stiff upper lip. Mass vaccine deployment will begin during the summer and will establish close to herd immunity by the time the 2021-2022 flu season arrives. The economy, however, will take another massive lockdown hit over the next few months as sheer panic erupts. The graphic above depicts the value of the above ground gold stock as a percentage of USD denominated nominal global GDP. I treat that percentage as a measure of global anxiety about the future as sustained by the United States courtesy of the US dollar as the world's sole reserve currency. Under my "prosperity-anxiety" model I posit that the value of the gold stock will track global prosperity in terms of economic activity and the level of anxiety about the future. The percentage indicator peaked at 24.6% in 1980, compared to 14.1% in 2011 during the aftermath of the 2008 financial crisis when gold bugs were wringing their hands about imminent hyper-inflation. In 2020 it hit 16% and is currently at 13.6%, which implies elevated anxiety but nothing as extreme as 1980. The anxiety increase since early 2019 is attributable to concern that Trump's policies were turning the global order into a free-for-all with unpredictable outcomes rather than one managed by the United States from behind a facade of weakness.

The "prosperity-anxiety model for gold" graphic above presents the annual average gold price as well as the annual high and low. But in 2020 and beyond I present what the high and low would be based on the gold stock value percentage peak of 24.6% in 1980 and the low of 3.5% in 2000. The equivalent today would be $3,181 for the peak and $442 for the nadir. For the latter to become reality we would need to see a mass exodus from gold into some other "safe haven" asset class such as Bitcoin pretends to be. At $442 per oz gold there would be no new voluntary gold production. But $3,181 per oz is not inconceivable. I am on record as predicting that gold will establish a new range of $2,000-$3,000 before any meaningful inflation arrives. But to some degree that was premised on the possibility that Trump would secure a second term and continue policies that push the United States away from global hegemon to just a scrappy street fighter focused only on personal survival. Beyond 2020 the annual average gold price projection (red line) is based on the gold stock representing 10% of global GDP. If 10% became the new normal, based on IMF projections for global GDP through 2025 we would expect gold to retreat below $1,500 and gradually inch above $1,500 over the next few years. While that is better than the sub $1,300 misery of the past decade, it would be a rather bearish development for gold focused juniors.

The annual gold price graphic above shows that the $400 level gold stabilized at in 1980 after its surge to $850 would be $1,267 today in annual CPI inflation adjusted terms. At today's $1,868 gold price that represents a 47% real purchasing power gain for gold, meaning that gold has gone beyond functioning as a hedge against inflation (the gold bug story is that the price of gold is all about future fiat currency debasement and hyper-inflation, which can become a legitimate concern, but if that is what you think when you buy gold juniors it means you are either a charlatan or ignoramus). The long term annual gold production chart below shows that if you inflation adjust gold through 2019 from 1934 when FDR reset the price to $35 per oz the price of gold ought to be only $701 per oz.

In my "prosperity-anxiety" model for gold I assume that the value of the world's gold stock is related to nominal global GDP expressed as US dollars, and that the percentage of the gold stock value to that of global GDP reflects the overall degree of anxiety about the future. The current gold price is well above what you would expect as a long term inflation hedge, and during 2020 the prosperity-anxiety indicator has ranged 11.4% to 16.0% with the 13.6% average the highest since 1987. Gold is currently operating as a hedge against uncertainty, and the recent weakness reflects concern that the Biden presidency will manage to restore stability and normality for the role of the United States relative to the rest of the world.

While I concede that a hostile Republican Senate could sabotage America's post-covid economic rebound, Trump's legacy will continue to be good for gold. The geopolitical tension between the United States and China which Trump accelerated during his term is not going to disappear. The IMF projects that by 2024 the gap between the Chinese and American portions of the global economy will have shrunk to 3.4% compared to 24.4% in 2001 when the Chinese super cycle got underway. That is not because the US economy is shrinking (the 2020 pandemic year excluded) but rather because the Chinese economy keeps growing at a higher rate. Since Xi Jinping took charge in 2012 he has consolidated his power, turning himself into autocrat for life, and given his foreign ministry spokesperson Zhao "Wolf Warrior" Lijian the green light to trash talk other nations and their politicians rather than China quietly biding its time. The Trump administration has made clear its goal of stopping China from achieving military and technological equivalence with the United States. The Biden administration may dial back the bellicosity, but by now it also understands that China is determined to preserve itself as an autocracy and that any western hopes that China's expanding prosperity would bring about a shift to democracy is little more than wishful thinking.

Chinese defense spending is still only 36% of US defense spending but China's military budget is 3.7 times that of the next biggest spender, India, and 4 times that of Russia. China is expanding its military footprint in its backyard through the Spratly Island base building. It has pulled the plug on Hong Kong as an independent democracy and is stepping up its rhetoric about Taiwan being part of China. Taiwan is a huge problem for the United States because it is the location of semi-conductor production that supplies American technology needs. The elephant in the room is Australia, a major supplier of raw materials to China, which China has started to bully with import bans in retaliation for Australia failing to kow-tow to China's machinations.

The Obama administration launched the Trans Pacific Partnership to create a united front against China, which Trump promptly pulled out of, along with the Paris climate agreement and the Iran nuclear deal as part of his campaign to scrub Obama from the history books. He also attacked traditional allies and cozied up with autocrats like Putin, Kim Jong-Un, MBS, and even Xi Jinping to name a few. His "America First - Go it Alone" policy antagonized geopolitical rivals like China and alienated allies in the rest of the world. The United States became unpredictable and while Biden may try to reverse that perception, Humpty Dumpty has fallen off the wall. In 2024 there will be another presidential election, and although Trump is unlikely to be the Republican candidate, there may be a much more competent and efficient autocrat on the ballot who could win if the Republicans choose to sabotage America during the Biden term. The unfettered social media manipulation facilitated by big data technology companies is not going to disappear. Nor is the electoral system which makes a mockery of the popular vote going to change. Trust in America as the leader of the free world will be difficult to restore because in four years another Trump like president could enter the White House. Anxiety about the future will not lessen, and China will press its economic advantage in the rest of the world while the United States digs itself out of the covid-19 pandemic hole. The US dollar soared during the March market meltdown but is in a weakening trend against almost all currencies but in particular the Chinese RMB, and the Canadian and Australian dollars. (A downtrend in the charts indicates a weakening US dollar.)

Although gold has wobbled and gold producers have retreated sharply during the past few months, non-precious metals have not suffered any reversal of their uptrends and base metal producers have also done well. This conflicts with my analysis that the general equity market remains vulnerable to a second meltdown that may turn into an extended bear market just as happened in 1930 after a strong V-shaped recovery from the initial 1929 crash. In the current situation the second downturn would be linked to the 2020-2021 flu season surge of the covid-19 pandemic, another severe economic lockdown, and problems arising from the White House transition to Biden. The promise of a vaccine driven end to the covid-19 pandemic is causing markets to dismiss the risk of a second market retreat as a temporary nuisance at worst. H1 of 2021 may be clouded with uncertainty, but a clarity is emerging about H2 of 2021. Those consumers whose jobs were preserved have had limited opportunity to spend their income which has piled up as savings. Some of it has gone into market speculation, but a lot of it is pent up savings itching for an "all clear" signal. This situation is different from the aftermath of the 2008 financial crisis when nearly everybody in some way or other ended up over-extended or with diminished asset values. They just weren't in a great position to help the economy to recover, especially with the austerity policies imposed by the Tea Party. So employment growth was slow, adding to the perception of a lost decade for the majority of people, many of whom became Trump supporters. But this time nobody bore any responsibility for the artificially induced plunge in economic demand except the one person with the power to take charge who shirked that duty to become the Benedict Arnold of future history books.

The lockdown has also forced people to reconsider what their lives were really all about, and once freed from their lockdown prisons, what they might like to do differently in the future. Although Trump and his Boomers waged war on the topic of climate change, industry and the rest of the world took no heed. Oil producers and car makers are undergoing a shocking realization that electric vehicles are being embraced much faster than anticipated. The demand for "green" or "clean" energy solutions is going through the roof. Furthermore, the concept of ESG credentials, historically associated with the left, are being embraced by the financial sector. It is as though westerners have admitted that they cannot compete directly with jurisdictions like China which have allowed western capital to exploit weak ESG conditions (minimal environmental controls, exploitive social conditions, and corrupt governance), but now they intend to compete by insisting as consumers on goods and services criteria that may cost more but do enable a clean conscience. It is ironic that even as Trump labored to gut environmental standards in an effort to help American manufacturers become competitive with the China price, systems for measuring, certifying and verifying ESG credentials were evolving which China cannot possibly compete with. China is an autocracy far more advanced in hyper-surveillance and behavior control than the United States, a self-built trap from which China cannot escape without risking the collapse of the Chinese Communist Party. For an excellent example of this new ESG perspective, listen to the Smarter Markets Interview of Robert Friedland by Erik Townsend. Not only does Friedland spell out what the clean energy revolution implies for certain metals like aluminum, nickel, copper and scandium, but he also talks about the Abaxx Exchange, a blockchain based market system that will facilitate the exchange of raw materials on the basis of verifiable ESG credentials. If this technology or other versions work, they will enable raw material producers to define their output in terms of ESG credentials such as CO2 emissions per unit, and make it visible to manufacturers who can bid to purchase not just the physical metal but the associated ESG credentials they can incorporate into the total ESG footprint of their end-products. It is an intriguing response to Naomi Klein's 1999 "No Logo" critique of the branding giants.

As the charts above show, prices for the magnet related rare earths have risen sharply during H2 of 2020, partly as a result of dampened supply due to the covid-19 lockdown in China during H1, but also because electric vehicle production is ramping up in response to consumer demand. Neodymium is a light rare earth which is the main input for the NdFeB permanent magnets used in electric vehicles, while dysprosium and terbium are heavy rare earths which are used to dope the Neo magnets so that the magnetism does not decay under high operating temperatures. Light rare earths tend to occur in carbonatites with very little heavy rare earth content. There are many light rare earth deposits around the world, with China's Bayan Obo the biggest mine, one that competes with the Norlisk nickel-cobalt-palladium mine in terms of environmental devastation. The heavy rare earths come from ion adsorption clay deposits in southeastern China which are mined in a wasteful and highly polluting manner by small scale operators, many of whom are part of criminal networks. If you are a Tesla procurement officer, good luck getting any trustworthy ESG credentials with your Chinese rare earth purchases. But what if Tesla can get its rare earth inputs from a mine developed in a jurisdiction with tough permitting rules and a monitoring system that is not corruptible? Might Tesla be willing to pay an ESG premium over the cheap China price for a dirty product? Might Volkswagen, eager to move beyond Dieselgate, pay a little more than Elon Musk is willing to pay? As long as the world operates under the principles of unfettered capitalism in a setting of globalized free trade, only the richest rare earth deposits outside of China like Mt Weld and Mountain Pass will ever be developed because they cannot compete with the China price for generic rare earth supply. When you demand reliable ESG information with your purchase of a product, and you add in supply disruption risks due to great power geopolitical competition between China and the United States, globalization coupled with information technology evolves away from the "race to the bottom" defined by Milton Friedman's version of free market capitalism. It is still free market capitalism but one with accountability built into it. All this is good news for resource juniors hoping to develop a deposit that may not be the richest and biggest in the world, but for whose output a sophisticated market is emerging thanks to "smarter markets".

The resource juniors tracked sideways during October and November which is evident in the flat performance of the KRO Favorites 2020 Index which was up 71.8% as of December 8, 2020 after peaking up 102.2% in July. During this period the value percentage traded by TSXV resource listings slipped below 50% after dominating in the 50%-80% range from May through September which also delivered the biggest financing boom since Q2 of 2011. The problem with the resource juniors is that their fortune remains linked to the gold price trend, even though in a price range of $1,700-$1,900 any gold price is fabulous for a junior with an exploration or feasibility demonstration stage gold play. Their additional burden is that we are now in the window when the four month hold periods for financings done since May 2020 are coming free trading while gold tracks sideways. The KRO Private Placement Timebomb Report (members only) tracks in alphabetical order all the companies with private placements done in the prior 4 months. By now we should be seeing a tremendous bout of tax loss selling, but while prices are sagging, we are not seeing the washouts that create lucrative bottom-fishing opportunities. Most companies did not get exploration programs underway until July, and most are still awaiting exploration results because covid-19 related protocols coupled with the natural capacity attrition created by the decade long bear market has created such bad lab delays that some companies won't know what they accomplished until late January. The need to see results first has also prevented the acceleration of exploration and rapid depletion of treasuries. By mid December I will have all the financial data from the September 30 quarterlies updated which will show up in that TimeBomb Report.

The non-resource listings on the TSXV are benefiting from the dual news that Joe Biden will be the president for the next four years, and vaccines are now being readied for mass deployment in 2021 so that the pandemic disruption can be put behind the world and economic growth can resume. The uptrend in non-precious metals like iron, copper, nickel and even zinc has already pushed base metal producers like Freeport-McMoran, BHP, Teck and Vale up substantially, and we are starting to see market interest emerge for juniors focused on base metals. There is also growing interest in juniors with critical metal plays for the reasons I have outlined. I regard 2020 as the awakening of a multi-year bull cycle for the resource sector and the juniors in particular. The gold price trend, especially into new territory like the $2,000-$3,000 range, is always difficult to predict because it is usually linked to things unexpectedly going wrong. But I don't think anybody should complain if it manages to spend 2021 bouncing in a $1,500-$2,000 range because that represents a real gain for the price of gold that lowers the threshold for a gold discovery that excites retail and sophisticated speculators and makes the resumption of feasibility demonstration attractive to institutional capital. On December 31, 2020 I will close out some Favorites, maintain others for another year, and introduce a few new ideas. Covid-19 crashed my plan to develop a new web site this year, but I have also learned that reproducing the current version of KRO as an information portal on a newer platform is something that I simply cannot afford. So the tentative plan is to continue KaiserResearch.com for the current membership until the end of 2021 while I develop a simple web site called KaiserResearchOnline.com which only features the Favorites. When the new site is operational I will close the old site to new memberships and eventually convert it into an invitation only online workshop where we incubate bottom-fish for future adoption as a Favorite when they no longer have missing pieces. All active members will become members of the new site when it is ready. The Slack Workspace will remain available only to members of the current KRO site until that membership term expires. So if you wish to stay with the existing KRO system and Slack Workspace or rejoin for one last fling before I turn it into an elite membership system, renew your KRO membership sooner than later.

Sun Metals Corp was initially made a Fair Spec Value rated Favorite on December 31, 2018 at $0.30 for the 2019 Favorites Edition on the expectation that followup drilling of the spectacular #421 intersection at the Stardust project would outline a major polymetallic discovery (see Dec 28, 2018). A key milestone was resolving the convoluted nature of the original Startdust option agreement which was resolved in February 2019 when Sun Metals agreed to acquire Lorraine Copper Corp through a plan of...

Azimut Exploration Inc offered shareholders a glimmer of hope on Oct 6, 2020 when it announced that it had started a 2,000 m 12 hole drill at the Pikwa copper project in the James Bay region of Quebec where it is earning back a 50% interest from SOQUEM. On Sept 15, 2020 Azimut reported that it had drilled 61 holes (11,388 m) on the Elmer project since late 2019 with assays so far reported for 45 holes. The initial focus was on the Patwon outcrop where drilling along 100 m of strike yielded excel...

Serengeti Resources Inc sparked buying with its Oct 7, 2020 news release about the East Niv project which it had staked in Q1 of 2018 along with 7 other properties after the BC government released results on Jan 23, 2018 for its Geoscience BC Search III Program. This was an airborne magnetic and radiometric survey covering 9,600 sq km which CEO Dave Moore's team was quick to evaluate for new magnetic anomalies that past exploration had not explained away. They focused on targets in topographical...

Outcome Visualization Project as of Oct 20, 2020: James Bay Underground

Project:James BayLocation:CanadaStage:5-PEA & Metallurgy

Net Interest:100% WIUncapped NSR:2.0%Target Metals:Niobium

OV Project ID:1000020OVP Posted:4/10/2020OVP Retired:

Current OV ID:1000060Current OV Confirmed:10/20/2020Visualizer:JK

NioBay Metals Inc (NBY-V)

ProfileSearchWeb SiteTreeForumSEDARQuoteIPV

Issued52,344,580

Price$0.620

Working Capital$1,277,356

Key People: Claude Dufresne (CEO), Serge Savard...

Outcome Visualization Project as of Oct 20, 2020: James Bay Open Pit

Project:James BayLocation:CanadaStage:5-PEA & Metallurgy

Net Interest:100% WIUncapped NSR:2.0%Target Metals:Niobium

OV Project ID:1000028OVP Posted:10/20/2020OVP Retired:

Current OV ID:1000078Current OV Confirmed:10/20/2020Visualizer:JK

NioBay Metals Inc (NBY-V)

ProfileSearchWeb SiteTreeForumSEDARQuoteIPV

Issued52,344,580

Price$0.620

Working Capital$1,277,356

Key People: Claude Dufresne (CEO), Serge Savard (...

Yorbeau Resources Inc announced on Oct 22, 2020 that it has begun a 2,500 m 2 hole drill program to test two conductors to the west of the depleted Lemoine VMS deposit (758,000 tonnes 4.2% copper, 9.6% zinc, 4.2 g/t gold and 83 g/t silver). I put out a What's Next Tracker on Sept 25, 2020 which provided an update on Yorbeau's situation (the ousted CEO Amit Gupta who ceased to be a reporting insider on June 16, 2020 and at one point owned 31 million shares has apparently been liquidating into the...

Dios Explorations Inc was assigned a Bottom-Fish Spec Value rating on January 23, 2020 based on potential regional implications of the Patwon gold discovery by Azimut Exploration Inc on its Elmer project in the James Bay region of Quebec. Azimut has drilled 61 holes representing 11,388 m since November 2019 of which it has reported results for 46 holes. Initial optimism was based on the potential for the gold mineralized dilation zone at Patwon to repeat itself multiple times within a northeast ...

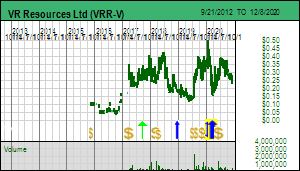

VR Resources Ltd was adopted as a Fair Spec Value rated Favorite at $0.38 in Tracker Feb 6, 2020 based on the drill program underway at the time on the Ranoke IOCG project in the James Bay Lowlands of Ontario and the Amsel gold-silver play in the Walker Lane of Nevada for which VR hoped to receive a plan of operations drill permit from the Forest Service by Q4 of 2020. Ranoke is a complex magnetic anomaly which VR first drilled in December 2019 with one hole that killed an IP target, leaving oth...

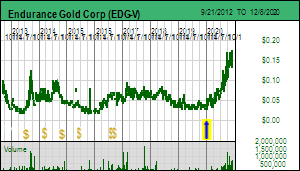

Endurance Gold Corp announced on Oct 22, 2020 that it has finally been granted a drill permit for the 100% owned Reliance project in southwestern British Columbia. It is too late in the season to mount a core drilling program but CEO Robert Boyd hopes to have a 60 hole "dry" RC drill program underway by mid November to assess the shallow gold grade potential along about 1 km of the Royal Shear structure at Reliance between the Imperial and new Eagle South zones. This is an important milestone be...

C3 Metals Inc was assigned a Bottom-Fish Spec Value rating on December 14, 2018 while it was still called Carube Copper Corp and focused on its portfolio of copper porphyry prospects in Jamaica. In August 2019 Carube sidelined its Jamaican copper portfolio and shifted its focus to Peru with the acquisition of the Jasperoide copper skarn project which changed the original rationale for the Bottom-Fish Spec Value rating. Thanks to the Covid-19 pandemic and Peru's strict lockdown response the deal ...

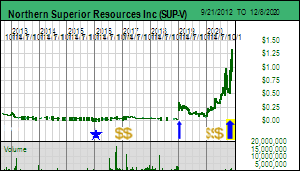

Northern Superior Resources Inc was initially assigned a Bottom-Fish Spec Value rating at $0.27 when the junior conducted a 10:1 rollback on January 7, 2019 based on its TPK gold project in northern Ontario which the junior had optioned 70% to Yamana in November 2018. Northern Superior operated a $2 million program on behalf of Yamana during 2019 but Yamana dropped the option at the end of 2019 despite promising drill results. TPK, which has the biggest gold in till dispersal anomaly in North Am...

Consolidated Woodjam Copper Corp reported assays on Nov 10, 2020 for the first hole drilled in 2020 on the Deerhorn system within the 100% owned Woodjam project in central British Columbia. Although technically an infill hole for the Deerhorn deposit for which Gold Fields reported an inferred resource of 32,800,000 tonnes of 0.22% copper and 0.49 g/t gold in May 2013, hole 20-71, drilled 50 m NW of hole 12-48, yielded 110 m of 2.57 g/t gold and 0.44% copper between 96-206 m, including 26 m of 5....

FPX Nickel Corp has started to attract market attention as multiple vaccine developers report positive trial results and the end of the Trump presidency inches ever closer to reality. Although large scale vaccine deployment will not kick in until the northern hemisphere's October through April flu season has run its dreadful course, it does allow the world to view 2021 as a year when economic life can start returning to normal. This is already happening in China where a harsh lockdown response i...