Hello Guest User, You are visiting this website from a computer with an IP address of 172.70.126.222 with the name of '?' since Sat Apr 20, 2024 at 4:44:54 AM PT for approx. 0 minutes now.

Discovery Watch is a weekly 15-30 minute audio show produced by HoweStreet.com where Jim Goddard interviews John Kaiser about resource juniors with projects that have caught John's attention. The projects will not be limited to companies he has covered through the Spec Value Rating System. Jim and John will periodically circle back to review the projects and if necessary close them out as no longer worth watching. Check out the catalog of KRO Free Stuff. KRO offers a USD $450 Annual Individual Membership. This Discovery Watch session is available via YouTube or Podcast.

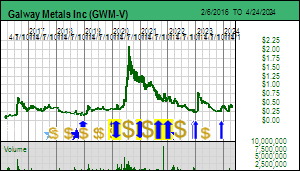

Galway Metals Inc management is the opposite of the "toiling geologist" Eastfield Group whose Cons Woodjam is featured in the second segment of this Discovery Watch episode. In fact they are so good I had to keep the company rated as a Fair Spec Value rated Favorite. In 2020 they raised lots of capital that allowed them to get serious about turning the new series of zones over a 4 km strike southwest of the Freewest discovered resource they purchased in 2016 into a resource estimate. But this resource estimate is still pending. We were supposed to see it in H1 of 2021, but then it was shifted to Q3 of 2021, which has one month left. So the market has become fatigued, and with gold no longer in an uptrend, the price has sagged, allowing me to upgrade Galway to a Good Spec Value rated Favorite. I haven't done an Outcome Visualization because I need to see the geometry of the new Jubilee etc Zone so that I can figure out what sort of mining scenario and operating costs are plausible. The upside resides in the exploration potential to repeat the North-South and Jubilee etc zones many times, feeding a central milling facility. The market wants to see the global resource clear the 1 million oz threshold, and those who know how to squeeze all those assays into a Leapfrog model are hoping for a resource in the 1.5-2.0 million ounce range. I can't wait for them to clear this hurdle because once it is done Galway has plenty of money left to reallocate its 6 rigs to start pounding all these other gold in soil anomalies they have developed near intrusions, for this is an intrusion related gold system which multiple intrusions within a district scale land package controlled by Galway. Although Clarence Stream is part of the Appalachian Gold Trend which includes the Fosterville fantasy playing out in Newfoundland, this is not a Bendigo style gold porn play that needs millions of metres of drilling to delineate a high grade resource. Tracker Aug 23, 2021 explains why I have made Galway a Good Spec Value rated Favorite but for now it is restricted to KRO members.

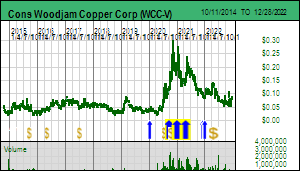

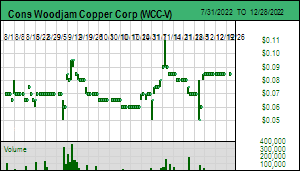

The Eastfield Group behind Cons Woodjam Copper Corp has created value for their backers for decades despite being notoriously obtuse when it comes to stock promotion. They were "toiling geologists" in the nineties when I launched the "bottom-fishing" concept as an independent analyst after leaving the brokerage sector in 1994, and they are still that today. Glory has escaped them because the value they have created through their Eastfield Resources Ltd mothership has been incremental. Glen and Bill are quintessential plodding tortoises who never win a gold medal but make it across the finish line. And you know what the fable says how this is supposed to turn out? WCC finally is a mechanical story in their hands that does not require a discovery to be turned into a mine. But they are addicted to discovery exploration and the current program is geared toward making Deerhorn bigger and proving that Megaton is more than a lower grade extension of the Southeast Zone. The market is pricing failure on the "extra" discovery front, and dismissing $4/lb plus copper as the new long term reality. I've done an Outcome Visualization for the Southeast Zone as it currently stands after Goldfields spent $30 million more than a decade ago and if my cost assumptions for a 30,000 tpd open pit scenario are correct, it deserves to be developed if you accept $4/lb plus as the new long term reality for copper. This doesn't even include blending gold enriched ore from Deerhorn into the SEZ flow-sheet. Now it is not yet for sure that Deerhorn is what it is and Megaton is a bust, but I am betting that this is the best outcome from the drill program currently underway because it would force Bill Morton and Glen Garratt to shift into feasibility demonstration mode. They have always farmed that out to others because that is not their style. So they are terrified about 2022 as the year when they have to shift Woodjam into feasibility demonstration mode, carrying on where Goldfields left off a decade ago. Maybe mother nature will bail them out by allowing the current Derrhorn hole to show there is a lot more size to Deerhorn than figured out by Goldfields, and that Megaton represents an extra 50% for the Southeast Zone. But mother nature seems to have a vendetta against my Favorites, so a pox on her, we don't need her to cooperate, we just need the Eastfield Group to embrace something they have avoided throughout their history.

Disclosure: JK owns Cons Woodjam; Galway Metals and Cons Woodjam are Good Spec Value rated Favorites