Hello Guest User, You are visiting this website from a computer with an IP address of 172.71.254.18 with the name of '?' since Thu Apr 25, 2024 at 11:12:40 AM PT for approx. 0 minutes now.

Kaiser Media Watch Blog - June 1, 2023 to June 30, 2023

KRO Blog Overview

The KRO Blog is where unrestricted content of a time sensitive nature is posted. It includes the Kaiser Media Watch Blog which features content involving John Kaiser produced by third parties such as the Discovery Watch series by HoweStreet.com, interviews by outfits such as Investing News Network, SDLRC related commentary, the KRO Monthly Summaries, and just about anything else John writes that is not intended exclusively for the fee based KRO Membership.

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch June 23, 2023: Mirage a major Boots on the Ground discovery

Jim (0:00:00): What is the latest news for the James Bay region?

Last week I talked about how the forest fire closures in Quebec's James Bay region had been lifted thanks to the arrival of rain in southern Quebec, but on Monday June 19 came the bad news that the Quebec government had reinstated the closure all the way south to include the Abitibi region due to lack of rain. It is unclear when the James Bay area will reopen and many Quebec based service providers are preparing to offer their services elsewhere in Canada. Brunswick Exploration Inc has already given up on the James Bay region until the middle of July and is putting all its boots on the ground into other parts of Canada not yet hit by fire closures.

Brunswick apparently has good reason to hit its properties in other provinces hard while James Bay remains off limits. In last week's Kaiser Watch June 16, 2023 Episode I discussed the spodumene-bearing boulder field Brunswick reported on June 14 finding at its Mirage project in the eastern part of James Bay. I inferred from the news release that the 1.7 km long band of boulders was parallel to the ice direction which is roughly southwest. Brunswick emphasized that the boulder field was at the southern end of a land package that stretched 18 km up ice. This implied an up ice source which to be meaningful had to also be oriented in the ice direction. The downside risk was that the pegmatite body was either a narrow dyke or a short body with limited strike, neither of which had tonnage implications. If I had talked to Killian Charles last week I would not have gotten more than what was in the press release about Mirage which was deliberately vague because it turns out they have been scrambling to expand the land position based on a new understanding of the area's potential.

The team spent only 6 hours at Mirage and they had with them the geologist who found the spodumene boulder a couple decades ago to show them where to start looking. They were blown away by what they found. The 1.7 km long band of boulders is 200 m wide and its limits were not cut off because they had to leave the field. The boots on the ground were like kids in a candy store who just didn't want to leave. The stunning tidbit I gleaned from Killian was that the band of boulders is perpendicular to the ice direction. What they found so far straddles both the 100% optioned Globex ground and the BRW staked ground. The geologist who found the original boulder is actually a geomorphologist, an expert on how the physical landscape is shaped. He himself was surprised at the extent of the boulder field.

The situation is in fact much better than I assumed last week and I am now confident that Brunswick has a major "first order" discovery at Mirage. There is no way this boulder field can be described as a glacial train, and the abundance of sub-rounded and sub-angular boulders rules out the idea of glacial erratics from far away. If this narrow field of boulders stretching 1.7 km perpendicular to the ice direction were glacially transported it would have a fan like down ice dispersal pattern. The topography is flat, so it is not a case of boulders rolling off some mountain into a valley bottom. The source is very local and likely parallel to the strike of the 200 m wide band of boulders. The size and quality of the spodumene crystals, which needs verification by assays, suggests this is a major discovery. I have been grumbling about the lack of geology Brunswick includes with its disclosure graphics, but they have deliberately withheld geology about the Mirage property because it has implications for the potential of a wider region than initially staked by BRW. They are so optimistic about the Mirage discovery that they are initiating drill permitting with the goal of drilling by September. Quebec's permitting rules for drill holes are flexible enough to figure out later this summer where exactly to spot drill holes.

Killian Charles did attend the Fastmarkets Lithium Conference held in Las Vegas June 20-22. This conference focuses on lithium supply and demand but also included rare earth talks. Killian, who attended as a delegate, estimates about 1,000 delegates participated. Many of them were representatives of government agencies and downstream processors and fabricators, but in terms of the lithium supply side the conference was dominated by Australians who are aware of Canada's major lithium supply potential. They are shaking their heads at the lack of North American interest in Lithium Mania 2.0, namely the hunt for LCT-type pegmatites beyond Australia in secure jurisdictions like Canada. Why are Canadians and especially the financial community on Bay Street oblivious to this enormous potential in their own backyard? I think the answer is simply that they do not understand how to convert lithium grades into rock value and appreciate how pathetic Canadian precious and base metal plays are in comparison.

Canada Wide Fire Map and Quebec Forest Access Closure

Some Mirage geology from Globex web site

Matrix for converting Li2O grades into rock value at various lithium carbonate prices

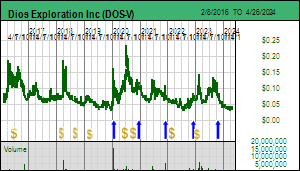

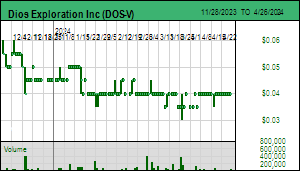

Jim (0:11:53): What do you make of the latest James Bay acquisitions announced by Dios Exploration?

On June 20, 2023 Dios Exploration Inc announced the acquisition of 3 new claim blocks called East Clarkie in an entirely new area to the east of its Lithium North and Lecaron areas. I've spliced together the new East Clarkie map with an older Lecaron geology map which does not include the Lithium Nord claims or the latest Lecaron addition. One of the frustrating things about the James Bay area is that companies tend to publish map fragments featuring only their projects, which makes it hard to see the big picture. To solve this I've tried to scale the spliced map to a Google Earth screenshot. The red box in the first graphic is supposed to be where the geology spliced map sits, with the yellow ovals representing the 4 groups in this area. I've also done a scan of the James Bay CEO.ca map published in December 2022 which only shows claims of companies that paid to be on it. I can't wait until a new one gets published.

It is now clear why Dios has been so secretive about its target generation strategy. Most of its target area is open to staking. In the third graphic is an update of my 1st versuss 2nd order regions which is interesting in terms of the absence of Brunswick claims in the Dios target generation area. The East Clarkie claims expand the focus about 100 km eastwards. Keep in mind that this area is closer to infrastructure than the northern Corvette trend area. What I also find interesting is that this is not a case of James Bay juniors focused on gold and base metal exploration waking up to the overlapping LCT type pegmatite potential like Azimut and Midland have largely done. There is no genetic relationship between precious/base metals deposits and LCT type pegmatites. Note the original Clarkie and Lecaron gold-related claim blocks in the middle of this area. If Dios is doing deep research based on a sophisticated understanding of glacial directions, a proprietary till sampling database, and studying high resolution satellite imagary, coupled with the lake bottom sediment data, in areas ignored for other metals, this would qualify as first order exploration when the boots hit the ground because nobody has ever had reason to look hard at these areas other than government geologists.

James Bay map showing focus area of Dios largely ignored by Brunswick

Key Dios lithium focus areas in southern half of James Bay region

Fragment of CEO.ca Dec 2022 James Bay showing how Dios focus area is largely open

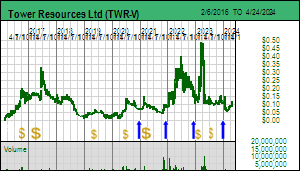

Jim (0:15:46): What is causing Tower Resources to perk up in recent days?

On June 22, 2023 Tower Resources Ltd announced that it had completed a ground magnetic survey at its 100% owned Rabbit North project in southern British Columbia which extends 2014 coverage to the area of recent focus, the Lightning and Thunder orogenic zones highlighted by the Dominic Lake and Centrain gold in till trains. As suggested by the recent drilling on the Thunder Zone the Chilcotin basalt flow is laterally more extensive than the band mapped at surface to the north. Although it is highly magnetic, it shows up as a magnetic low because of a polarity reversal at the time of eruption, which has the effect of partly masking what they see as a 250 m by 900 m magnetic high to the west of the Rainbow Cu-Au-Mo zone hit earlier this year while testing the Thunder gold target. The stock collapsed in April when Tower released the final results for the 4 holes drilled into the Thunder target.

In I pointed out that although the Thunder Zone has fallen short of expectations, the Rainbow zone intersected to the west of the Thunder Zone was an unexpected pleasant surprise that may be the edge of a blind copper-gold porphyry system to the west that is obscured by overburden and has never been drilled. Stu Averill believes the magnetic high to the west of the Rainbow intersection may be due to hydrothermal magnetite in conjunction with sulphides related to a porphyry system. There is no outcrop in this area and it looks like they plan to drill this Rainbow target.

Tower has also concluded that the gold grains in the Durand Creek train are associated with a copper-gold porphyry system, and not another younger shear controlled orogenic gold system. Furthermore, its head appears to be well to the north of the Rainbow target in a magnetic low area 1 km to the west of Western Magnetite Zone which in 2017 yielded 247 m of 0.51% copper and 0.34 g/t gold starting at a depth of 208 m, too deep for open pit mining. Stu does not attempt to explain why this area is a magnetic low, though from the graphic the Western Magnetite Zone also appears to be a magnetic low. Although for the moment I am not optimistic the orogenic Lightning and Thunder Zones will amount to meaningful gold deposits, the focus on them has helped reveal a hidden copper-gold porphyry aspect of Rabbit North that has not been tested by past exploration due to the absence of any encouraging outcrop. Tower has not indicated when it plans to drill the Rainbow target, but bottom-fishers appear to be willing to give the Rabbit North story another chance.

Exploration at Rabbit North shifting west into covered area

New magnetic survey with new targets highlighted

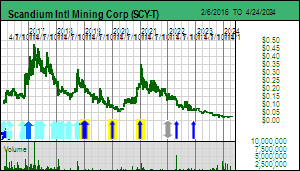

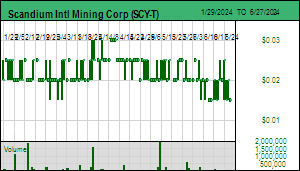

Jim (0:21:12): What do the Honeybugle drill results mean for Scandium International?

On June 20, 2023 Scandium International announced the results for a drill program completed on the Honeybugle project located 24 km southwest of the Nyngan scandium project in New South Wales. The market ignored the news, perhaps because it does not understand its meaning, perhaps it does understand what Rio Tinto's purchase of the Owendale deposit from Platina means for a future buyout of SCY, and perhaps because it knows that there remain four years of life for the 5 year warrants that accompanied last year's $3.5 million private placement at $0.09 when the Evensens kicked out Willem Duyvestyn and George Putnam.

The Honeybugle project emerged in 2014 when SCY was in danger of losing Nyngan to Till Capital which was calling its loans to the company. SCY ended up being bailed out by the Evensens when they loaned USD $2.5 million convertible into a 20% stake in Nyngan, which conversion would be triggered by SCY raising additional equity capital. The target amount was reached in the form of a private placement by Andy Greig who remains a major shareholder of SCY. They eventually converted the 20% project interest into a roughly 20% equity stake in SCY to become the largest shareholder.

The Honeybugle area was known to host 4 magnetic anomalies represented by ultramafic laterites which had previously been explored for nickel and platinum group metals without success, but were known to have scandium values at a time when nobody cared. SCY, eager to preserve its scandium "brand", drilled the Seaford target with 30 holes in April 2014 and confirmed that scandium values comparable to Nyngan were present, but did not publicly do any followup work when it had staved off the Nyngan default with the help of the Evensen financings. In Tracker June 7, 2021 I undertook a back of the napkin resource estimate based on the key results from Drill Area 1 of the Seaford anomaly which intersected good scandium values in both limonite and saprolite. The result was a speculative resource of 3,740,000 t @ 272 g/t Sc (ppm) for the Seaford zone which I used as the basis for an outcome visualization imagining a 1,000 tpd open-pit mining operation that would produce 127 tpa of scandium oxide, nearly 4 times what the proposed Nyngan mine would produce. I bugged former CEO George Putnam to spend a small amount on additional drilling to achieve the density needed for a resource estimate but he rejected that idea.

When I read the news release I was surprised to learn that work was done on Honeybugle in 2016 and 2018 which was never reported by SCY. The drill program of 32 air core holes done in Q1 of 2023 focused on a 300 m by 400 m area of the Woodlong anomaly and were disclosed as holes #76-#107. The news release included earlier drill resuls for holes #37-#60, and continued with holes #76-#107 from the 2023 program. This it was news to me that holes 37-60 were from drilling campaigns done in 2016 and 2018. The 2023 program runs from #76-107, which means there is another batch of holes #61-75 that must be on one of the other targets of which there are 4 defined by magnetic anomalies: Seaford, Woodlong, Yarran Park and Mallee Valley. In addition there must also be holes #31-#36 whose location is not disclosed. I am assuming the numbering sequence reflects holes drilled by SCY.

SCY provided a drill plan for all the holes drilled into the Woodlong target. The 2016-2018 drill sequence, which I have traced does not make a lot of sense with holes jumping all over the place with some yielding good values. But the 2023 drill sequence shows a determination to drill the Woodlong zone on a systematic grid that fills in the older holes and produces a grid with 50 m spacing between holes. The company also included a grade x thickness heat map on which I've circled all holes with a minimum 200 ppm grade. The holes are drilled on 50 m centers so I have assumed a 50 x 50 m block around each hole and multiplied the area by the mineralized interval and 1.88 as a specific gravity (assigned by the Nyngan DFS for the higher grade limonite ore that feeds the Nyngan mining plan), and then added the 26 holes that qualify to get the total tonnage which is 1,184,000 tonnes. Note that the southern part has some gaps, and given the nature of this type of laterite system, the back of the napkin resource can be rounded up to 1.4 million tonnes. The thickness of these 26 holes was 9.7 m with overburden ranging from 0-6 m but generally just1-2 m thick. For the average grade I multiplied the tonnage block of each hole by the grade, summed them, and divided by total tonnage to get an average grade of 394 ppm, which is better than I estimated for the Seaford mineralization.

But what is the potential economic value of this bak of the napkin resource estimate? Here is where the market runs in comprehension challenges, and the company cannot help out until it has converted the data into a 43-101 resource estimate. First you multiply the 394 ppm Sc grade by 1.534 to convert to Sc2O3, the form that gets marketed and to which a price is assigned. Then you multiply by $2,000/kg Sc2O3 (the price SCY used as a base case for Nyngan, Sunrise uses $1,500/kg, Niocorp $3,600/kg, and sneaky Imperial Mining uses $6,500/kg inside its master alloy) and divide by 1,000 (ppm means parts per million and is the same as g/t - there are 1 million grams per tonne) to get a rock value of USD $1,208/t. The Nyngan DFS assumed an 84% recovery, so the recoverable rock value is $1,015 per tonne for about 600 recoverable tonnes Sc2O3 worth USD $1.2 billion.

SCY mentions that a thinner horizon of saprolite sits below the limonite horizon, and while it is lower grade than the limonite, does run at least 200 ppm Sc. The Sunrise and Owendale deposits do not have a saprolite horizon. But what does it matter if the Seaford and Woodlong zones are richer and possibly bigger than the resource targeted for development at the nearby Nyngan deposit? In Kaiser Watch Episode May 5, 2023 I discussed the potential negative implications for SCY presented by Rio Tinto's decision to purchase the Owendale scandium deposit from Platina for USD $14 million. Owendale is substantially bigger and richer than Nyngan, so if Rio Tinto gets it into production, it will never need to develop SCY's Nyngan deposit. However, Owendale has a water rights problem and does not own the surface rights for a property in an area that is agriculturally more productive than in the Nyngan-Honeybugle area. At Nyngan SCY already owns the surface rights for the western half of the mining lease where all the infrastructure would be located and where the first ten years of mine production at 240 tpd would take place.

The new SCY management has talked about getting a partner to develop Nyngan, perhaps on a smaller scale, and Rio Tinto is the most likely party to be in need of additional scandium supply when its Sorel-Tracy facility hits its scandium by-product limit. But Rio Tinto would strike a hard bargain that is not beneficial to SCY, as we saw with the terrible deal it did on Midland's James Bay lithium project (Gino Roger wants everybody to know that the number of years Rio Tinto has to earn 70% is 10 rather than 12 years as I mistated last week!) However, having Rio Tinto spend the money to prove that the Nyngan flow-sheet works as predicted and possibly ruin the expansion potential of Nyngan would be very beneficial for Honeybugle because the mineralogy is likely to be similar. If SCY decides to deliver a JORC or 43-101 resource estimate for the Woodlong zone, even though it is small, combined with the Seaford zone it would be an attractive development target for another major eager to piggyback on any success Rio Tinto has had building scandium offtake demand to a tipping point where a lot of end users might want to use aluminum-scandium alloys for the lightweighting benefits in the transportation sector.

Today one also has to take into consideration potential demand from the defense sector; a decade ago when I first became enamored with scandium China was still expected to become more like the Global West thanks to the demands of a rising middle class. But under Xi Jinping China has defined itself as an autocracy aligned with other autocracies such as Russia, the Global East, which sees itself in economic competition with the United States led Global West. As a result today both American political parties support defense spending and even venture capital is investing in new military technology startups. When it comes to pushing materials to new functional limits, scandium, shunned for decades because as a dispersoid it does not concentrate into rich deposits like other metals, is a contender. While consumer applications are very sensitive to input costs, military applications are not. The chicken and egg problem that has plagued scandium forever could be solved quickly through "military intervention". That wasn't a plausible concept a decade ago. I think it is a wise decision by CEO Peter Evensen to make Honeybugle more visible as an asset, which allows Nyngan to be rapidly developed as a pilot plant facility with larger scale potential 24 km down the road at Honeybugle.

Honeybugle Drill Plan showing drilling sequence in 2016-18 compared to 2023

Woodlong drill results and back-of-the-napkin resourcer estimate

Disclosure: JK owns Brunswick, Dios & Scandium Intl; Brunswick is Fair Spec Value rated Favorite; Dios, Scandium Intl and Tower are Bottom-Fish Spec Value rated

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch June 16, 2023: Patriot rises as Rio Tinto enters James Bay

Jim (0:00:00): What is the status of fire restrictions in the James Bay region of Quebec?

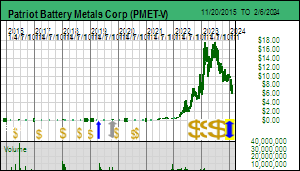

Although forest access restrictions remain in effect in southern Quebec they have been lifted in the James Bay region thanks to rain during the past week which has helped get fires in southern Quebec under control. Patriot Battery Metals, which announced more CV5 drill results earlier this week, is remobilizing all its crew and operations at the Corvette project. This week Dusan Berka who has been a director and CFO for more than a decade retired and was replaced by Pierre Boivin, a lawyer with McCarthy Tetreault. The company expects to have a maiden resource estimate out by the end of July which will include all results from the winter drill program that stopped in late April for spring thaw and the annual month long goose hunt. These holes encompass 3.7 km of strike for what is now called the CV5 zone. There remains another 1.5 km in the northeast direction to the CV4 pegmatite outcrop at the edge of the lake though the grade-thickness diminishes at the northeastern drill limit. The northeastern third called the Nova zone is a high grade 1,100 m segment assaying above 1.5% LiO. Assays for 12 holes are still pending but these are not going to make much difference about the size of the CV5 system. The company has 30,000 m of drilling planned for the summer season, much of it infill drilling to support a PFS for next summer, but also extending the CV5 in both a northeast and southwest direction.

The lifting of the forest access ban helped PMET make a new high today at $17.80, surpassing the $17.69 high made on February 6. At Friday's closing price of $17.53 the 100% owned Corvette project at 135.3 million shares fully diluted has an implied value of CAD $2.4 billion. Why is the stock making new highs? I doubt very much it has anything to do with the pending assays for CV5, nor is the market speculating that the resumption of drilling will make CV5 more valuable by making it bigger. The stock is making new highs because on June 14 Rio Tinto tipped its hand as a potential bidder for PMET by securing a deal that will allow it to earn 70% of Midland's remaining 100% owned James Bay projects by spending $64.5 million over 10 years. All the juniors who still have 100% were applauding Midland for allowing Rio Tinto to take Midland offline as a target for Lithium Mania 2.0 speculators.

Drilled and Undrilled Targets on Corvette Property

High Grade Nova Zone within CV5 Pegmatite

Jim (0:06:37): Why do you think the Rio Tinto-Midland deal is good for everybody except Midland?

The Rio Tinto farmout deal announced on June 14, 2023 by Midland Exploration Inc allows Rio Tinto to earn up to 70% by spending $64.5 million over 10 years. Rio Tinto can go to 50% by spending $14.5 million over 5 years, with $2 million a firm commitment over the next 18 months. It also includes cash payments of $500,000 upfront and $100,000 at the end of each of the first 5 years. Rio Tinto can elect to earn 70% by spending $50 million over another 5 years. The deal is a disappointment for Midland shareholders because Midland should have spent its own $2 million over the next 18 months to see if there is any low hanging LCT type pegmatite fruit for boots on the ground to stumble over. Midland had about $5 million working capital at the end of March 31, 2023. Given the extraordinary size of the potential prize - a 1% Li2O grade at $10/lb lithium carbonate is equivalent to a 8-9 g/t gold or 6% copper grade - CEO Gino Roger should have taken the 100% risk, especially after being asleep at the switch when on November 10, 2022 Bob Wares managed to convince Midland to option to Brunswick the lithium and rare metal rights to the original Mythril copper property adjoining the north side of Patriot's Corvette property (the deal also included the Elrond property located much farther to the west). Brunswick can earn 85% by paying $345,000, issuing $355,000 in stock and spending $3.5 million over 5 years. The only good part of that deal for Midland was that its 15% is a carried interest on which Brunswick retains a right of first refusal. When I asked Bob Wares why Midland did such an easy deal, he just shook his head, saying that climbing up the lithium learning curve just wasn't on their to do list.

By PDAC Midland had come to understand Lithium Mania 2.0 and the potential for James Bay to turn into a Great Canadian Area Play. It had staked additional claims and created excellent graphics for projects such as Komo to the west of Allkem's Galaxy-Cyr project and Galinee to the east of Winsome's Adina discovery. Since 2006 Midland has spent $80 million on projects in Quebec, of which $39 million was provided by farm-in partners. And remarkably Midland still has only 88.8 million shares fully diluted. I talked to exploration VP Mario Masson at PDAC and hoped out loud they would do a boots on the ground lithium first pass this summer on a 100% basis so that they could reap any first order discoveries. I was taken aback by the sad look on Mario's face and wondered if Gino was still shell-shocked from the failure of his Mythril copper keeper moment in 2018-2019 to deliver.

The Mythril copper play, which was generated by following up with boots on the ground a copper showing mapped by the government, stirred hopes that James Bay, which has largely failed as a gold district, might in fact host a major copper district. At the October 2018 AMEQ in Montreal Gino had button-holed me in the same manner Virginia Gold's Andre Gaumond did at the November 2004 Hard Assets show in San Francisco when he showed me a rock from Eleonore and insisted this was a keeper. That decision to buck the farmout rule drew a sell recommendation from a Carlsbad guardian at the start of a 100% funded play that resulted in Virginia disappearing at $14 in a $750 million buyout by Goldcorp a couple years later. When Midland mounted its own Mythril copper drilling play in 2019 the inexplicable selling was relentless. At the time Midland was too busy to accept my invite to MIF so I instead invited 92 Resources Corp which had optioned the adjacent Corvette property from Osisko for its lithium potential. But by 2019 lithium carbonate prices had tanked below $5/lb thanks to Australian pegmatite sourced supply, so the project was undrilled. 92 Resources did conduct a drill program in 2019 on what were gold targets which like most gold targets in James Bay failed to deliver much. That program was also accompanied by relentless selling, after which the junior did a 10:1 rollback to become Gaia, relisted on the CSE, and for good measure did another 3:1 rollback when it changed its name to Patriot Battery Metals. As it turned out, the high grade copper seams at Mythril were too narrow and widely spaced to deliver a bulk tonnage mineable ore grade and the play flopped. Azimut drilled its Pikwa extension in 2020 but was apparently so ashamed by the results that the Pikwa outcome was never reported.

The Rio Tinto farmout deal is terrible for Midland shareholders because Rio Tinto only needs to spend $2 million over 18 months which as operator it will do with its own boots on the ground. It's as if Rio Tinto has borrowed Midland's James Bay properties as a training school for its geologists. Rio Tinto will make quick work of the 10 properties to make sure nothing obvious is sticking out of the ground, but its real target will be to take out Patriot Battery Metals or any other junior that makes a major LCT-pegmatite discovery in the James Bay region over the next couple years. The Rio Tinto CEO is on record grumbling that lithium pegmatite projects are too expensive, though that did not stop Albemarle from making a conditional AUD $5 billion offer for Liontown's Kathleen Valley project which has a scale and grade similar to what the CV5 zone at Corvette may approach when the maiden resource estimate is delivered in late July.

Rio Tinto clearly understands that lithium could evolve into a $100-$200 billion annual market, putting this until recently obscure metal in the same league as copper and gold. In 2004 Rio Tinto discovered the Jadar deposit in Serbia which is a sediment hosted system similar to Nevada's claystones except the lithium grade within a mineral called jadarite is 10 times higher. By 2017 Rio Tinto had solved the metallurgical challenges and applied to develop a reserve of 118 million tonnes of 1.8% Li2O. This was met by opposition from the European anti-mining lobby which complained that mining would disrupt the pastoral setting of the project area. The Serbian government canceled the license and Jadar is going nowhere. In an October 2021 Investor Seminar Rio Tinto provided a slide which declared that the world will need 60 Jadar equivalent mines by 2040, and that did not include the possibility that a solid state lithium battery allowing lithium metal as the anode would become reality.

Back in the 1990's when Dia Met and BHP made the Ekati diamond discovery in the Northwest Territories of Canada Rio Tinto was quick to show up through its North American subsidiary Kennecott to option properties that Aber and the DHK group had staked south and east of the Ekati block. Kennecott was very aggressive because BHP owned 51% of Ekati and so there was opportunity to acquire Ekati. Kennecott discovered the DO27 kimberlite which was large with good grade but low value diamonds. It then went on to discover the high grade Diavik pipes on Aber's ground and developed them into mines. Patriot Battery owns 100% of Corvette and does not have any major shareholders who could block a hostile takeover bid. The Corvette property is also 2-3 years ahead of any other potential world class grassroots discoveries in the James Bay region. If Rio Tinto makes a successful bid for PMET, that will become its focus, while the Midland farm-in deal limps along for the next decade. If Rio Tinto is beaten out by another party, that would be construed as good news for Midland because then Rio Tinto will become very aggressive exploring the 10 properties. However, if a takeover battle for PMET emerges, it will send market interest in the James Bay Great Canadian Area Play through the roof, and other juniors like Champion Electric, Dios and Brunswick who have majority stakes in promising James Bay properties will become the target of speculators and the Bay Street financiers. Midland did not farm out all its James Bay projects; let's hope that wasn't because they have zero LCT-type pegmatite potential.

Jim (0:17:02): How significant is this week's news from Brunswick about its Mirage project?

Brunswick Exploration Inc announced on June 14, 2023 that during the 2 days it had boots on the ground at the Mirage project the team managed to identify 20 spodumene bearing boulders within a 1.7 km band aligned with the ice direction. A bedrock source has not been established, but the company did point out that the property stretches 18 km up ice from the boulder field. The largest boulder was 6 m by 5 m. Light grey spodumene crystals up to 50 cm representing 5% to 50% of the pegmatite were observed. The boulders vary from sub-angular to sub-rounded. As a rule the more angular a boulder the more local the source. When rocks end up in river beds they quickly become rounded. But they also become rounded when they get stuck in the base of an ice sheet and dragged along bedrock. This boulder field was first noticed by a prospector 25 years ago but nobody was interested. Bob Wares remembered the episode and tracked down the area. Part of it was staked by Jack Stoch's Globex Mining Enterprises Inc as the Lac Escale project for its precious metals potential. Brunswick staked the open ground it felt was relevant for LCT-pegmatite potential and then optioned Lac Escale on January 24, 2023 100% for $500,000 and $1 million exploration over 3 years.

This development is significant because such a large number of boulders with a distinct rock type within a constrained area aligned with the ice direction suggests an up ice source possibly oriented in the same direction as the ice sheet's movement. Large boulders can travel enormous distance from their source and are called "glacial erratics" because they have no relationship to nearby geology. Until Brunswick finds the bedrock source there will be questions about how far this field of boulders traveled, especially given the sub-rounded appearance of some of them. However, in climates where there are dramatic seasonal changes granitic rocks undergo exfoliation which gives then a rounded look despite being stationary.

I saw this first hand when I visited the Strange Lake site in September 2009. The original Strange Lake deposit had been found decades earlier by the Iron Ore Company on the Labrador side. The speculation with Quest Rare Minerals was that perhaps half of the Main Zone sat on the Quebec side of the boundary which is defined by the watershed divide. By the time we got there a survey had established that only 15% of the known deposit was on the Quebec side where Quest had staked claims (the Labrador side had been withdrawn into a provincial mineral reserve). But then management took us for a walk and showed us a field of boulders which were assaying up to 1.5% TREO with 45% represented by heavy rare earths. It turned out that these boulders emerged from their source through frost-heaving. By April 2010 Quest had delineated a resource of 114 million tones of 1% TREO for what became know as the BZone. Within the BZone a 20 million tonne enriched zone grading 1.44% TREO became the focus for economic studies. The problem with the Rare Earth Mania of 2009-2012 was that the rare earth market was dominated by China which has since managed to grow its supply 200% to keep pace with EV related demand growth. Lithium demand has a much bigger demand growth trajectory and no country has a near monopoly of supply as China does with rare earths. With the fire restrictions now lifted in the James Bay region the Brunswick teams top priority is to get those boots back on the ground, figure out the bedrock source, and establish enough understanding of its orientation to support permit applications for a drill program in the fall.

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch June 9, 2023: James Bay Waiting for the Summer Rain

Jim (0:00:00): How will the Quebec forest fires affect the lithium pegmatite hunt this summer in the James Bay region?

Last weekend Quebec exploration hit the wall when the provincial government suspended access to forests and ordered exploration companies to cease activities. The reason was that lightning strikes had started about 150 forest fires in southern Quebec which the province's forest fire fighting system had capacity to handle only about 25% (a June 9, 2023 NYT Article describes how budget cuts have diminished Canada's forest fire fighting capacity despite the country's official acceptance that global warming is a real trend that must be dealt with). All helicopters were requisitioned to support fighting fires in southern Quebec close to communities and infrastructure. By mid week Chibougamau was ordered to evacuate at 2 AM. The reason for the forest fire situation was an abrupt transition from spring thaw to record setting temperature and dry conditions.

Some have suggested that the fires were accelerated because the leaves from Quebec's deciduous trees (ie the maples responsible for spectacular fall color), preserved quickly by winter after falling last year, never had a chance to decay and quickly turned into flammable tinder. The trees in the northern part of Quebec which includes the James Bay region are conifers such as spruce. The smoke was so bad it reached as far as Florida, and New York at times matched the air quality of India's Delhi which has the worst air quality in the world. In 2020 California suffered major forest fires whose smoke traveled into the Bay Area resulting in one day that was like an all-day total eclipse (Sept 9, 2020 San Francisco Chronicle. But that was in September in the middle of a drought; summer hasn't even arrived yet in Quebec and we have a situation this bad already?

The fear experienced by everybody with exposure to Lithium Mania 2.0 juniors was that no boots would be allowed to pound the ground the entire summer, meaning there would be no targets to drill in the fall or early 2024. The whole point of Lithium Mania 2.0 is to find as soon as possible in places like Canada the second half of the 600% expansion in lithium supply that the IEA projects is needed to meet 2030 EV deployment goals to support net zero emissions by 2050 (limiting temperature rise to 1.5° C). Getting major new pegmatite deposits found over the next two years into production by 2030 is already a stretch of the imagination unless Canada figures out how to streamline its mine permitting system. Few missed the irony that greenhouse gas driven climate change would delay this mitigation effort because Canada was asleep at the firefighting switch.

Only a few fires were burning in the sparsely populated James Bay region and they are usually ignored unless they threaten hydro power facilities, exploration camps or get close to the few roads that connect this remote region. Natural Resources Canada provides an Interactive Map which allows one to track the fire danger and fires across Canada. When loading the interactive map the first time, use the "overlay" button to drop down a menu of settings to activate. I have provided a screenshot of the menu along with maps from June 5 and June 9. These show the dire situation last weekend moderating as rainy weather moves westward. A June 11 screenshot shows that although there still many active fires the fire danger is dropping in southern Ontario and Quebec thanks to wet weather. Eastern Canada does have wet weather during the summer, so the big hope is that the spring dry spell is over, the fire danger will diminish, and the restrictions on exploration will be lifted.

Quite a few juniors such as Brunswick Exploration Inc put out glum news releases that they had boots on the ground but had to pull out their crews. Although Brunswick has properties in other parts of Canada such as Manitoba, Ontario and Atlantic Canada where there are no restrictions, at least not yet, the indefinite closure of the James Bay region would be a major problem because Brunswick holds several strategic claim options from Osisko and Midland which have an escalating option payment structure. The plan was to hit hard the Plex and Mythril claims in the northern half of the James Bay region where Patriot Battery Metals is delineating the CV5 lithium pegmatite on its Corvette property. Patriot optioned Corvette from Osisko back in 2015 because this particular trend had visible pegmatite outcrops. But this northern half of James Bay has never been seriously investigated for LCT-pegmatites, and now there is a scramble afoot to take a close look at the areas parallel to the Corvette property as well as the continuation of the amphibolite trend to the west which in areas like Plex were targeted by Virginia Mines for their gold potential. Brunswick has now disclosed that the pegmatite encountered in holes testing the Orfee gold zone on the Plex property is not spodumene enriched. Killian Charles told me that the main encouragement his team got from visiting the Plex core shack was this was "evolved" pegmatite, just not to the extent needed to create an LCT-type pegmatite. Prospecting the numerous peripheral pegmatites, shooting them with an XRF or LIPS gun, and collecting channel samples is thus an essential task for this summer. This is "first order" exploration because pegmatites are known to exist, except nobody has ever bothered to classify them. In the case of the Mythril claims whose "rare mineral" potential Brunswick has optioned 85% from Midland the task is a little harder because of LCT-type pegmatites are present they will have more subtle exposure.

Although the prices of most James Bay lithium juniors sagged, Dios Exploration Inc managed to generate a modest uptick when it published an update about additional claims it had sticked with the LeCaron cluster. The press release included a large scale map showing the inland extent of the former Tyrell Sea and how it overlaps with the glacial moraine front of the last ice sheet. Dios' CEO Majire-Josie Girard explained to me that while the area covered by the Tyrell Sea has plenty of LCT-pegmatite potential, as is evidenced by the Galaxy-Cyr pegmatite Allkem is developing, the lake bottom sediment data in this area is largely useless for pinpointing nearby LCT pegmatites because of the sea floor reworking of sediments. The glacial moraine front shows the overlapping part where basal till sampling is useful.

This region saw all its major outcropping pegmatites like Cyr staked decades ago and is now target for "second order" exploration where secondary clues are used to track down locations for hidden or barely exposed LCT pegmatites. One technique being used by many companies involves studying high resolution government satellite imagery for "glimmers" of pegmatite. One of the properties Brunswick optioned from Osisko is the Anatacau group. Most of the attention has focused on the small Anatacau West claim where drilling by Brunswick this winter confirmed that the Galaxy-Cyr pegmatite systems trends at least 300 m onto Anatacau West. Brunswick plans to prospect the eastern extent of this property during the summer, but more important are its plans for the much larger main Anatacau block to the east. Brunswick has been rather penurious in publishing detailed graphics about its various properties, but it has indicated that pegmatite outcrops are present on Anatacau and that is a priority for boots on the ground because its is part of the expensive Osisko option, but it is also much closer to infrastructure than the "first order" targets in the northern half of James Bay. I've super-imposed a screenshot of the Anatacau property onto the map published by Dios to show the scale of Brunswick's property which also hearkens from the Virginia gold exploration days.

Nobody except Kenorland has done any recent till sampling in this region and Kenorland optioned 100% of the claims resulting from this till sampling to Li_FT Power whose attention has shifted to its collection of pegmaties in the Northwest Territories. However, about 15 years ago Sirios and Dios collaborated on a regional till sampling program done on a 2 km by 2 km grid with Sirios getting to stake any gold in till related targets while Dios got to stake diamond indicator mineral related targets. This till sampling program which extended somewhat beyond the glacial moraine front resulted in the discovery of the Pontax lithium system which Sirios and Dios spun out as a separate entity that became Stria Lithium which in turn has farmed out Pontax to ASX listed Cygnus. Sirios and Dios dissolved the till sampling JV but each kept a copy of the resulting proprietary database. The Dios exploration team has been quietly parsing the till database for more subtle LCT pegmatite clues and correlating them with lake bottom sediment data, satellite imagery, mapped geology, and archival research. The spice that Dios is adding to this secret sauce is the in-house experience with regard to the behavior of glacial transport that evolved during the two decades of futile diamond exploration trying to find another Renard cluster in the James Bay region.

Dios has plans to put boots on the ground in July, so the current disclosure has not disrupted any of its plans. But much will hinge on whether the summer rain dampens the fire risk in southern Quebec and the James Bay access closure is lifted. Dios managed to gain a few pennies this week, which still leaves it with less than a tenth of the valuation Brunswick is commanding. But it will likely continue to attract bottom-fishers while we wait for the summer rain, especially if Dios steps up its disclosures that help the market better understand its "second order" exploration strategy in the southern half of the James Bay region. In its recent MD&A quarterly filing which revealed that the marketing budget consisted of the equivalent of springing for a bottle of two buck chuck, Dios also included a shareholder pie chart including a "private investor" with an 8.5% stake. If my leg isn't being pulled by this investor, he is sitting on a windfall score in the form of over 1 million Patriot Battery Metals shares. Not every PMET investor below out his or her stock when it hit $2. Furthermore, given how many cheap warrants remain outstanding, there are plenty sitting on windfalls that will be turned into liquid cash or big company stock if PMET attracts a buyout later this year. Where to redeploy that windfall will depend on what boots on the ground in James Bay deliver this summer.

NRCAN's Canada Fire Map comparing June 5 to June 9

Updated NRCAN Fire Map for June 11, 2023

James Bay Map showing 1st and 2nd Order Pegmatite Potential

Map showing the overlap of Tyrell Sea and ice sheet moraine front

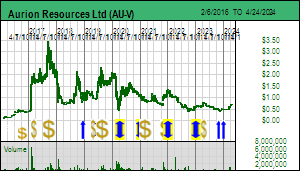

Jim (0:12:37): What has your KRO Favorite Aurion Resources planned for this summer?

I published Tracker June 8, 2023 which provides a detailed assessment of the district consolidation play brewing for the Central Lapland Greenstone Belt in Finland where Aurion Resources Ltd is the lynchpin. It also explains how the Savu acquisition news on May 23 not only provides Aurion shareholders with a meaningful Finland spinout if Rupert Resources Ltd reaches a plan of arrangement to merge with Aurion, but also exposes Aurion to a potential hallelujah event this summer if the boots CEO Matti Talikka puts on the ground at Savu stumble across a significant LCT enriched pegmatite. His secret sauce is a basal till sampling database which GTK, the Finnish geological survey, conducted on a 2 km by 2 km grind decades ago in the Savu region. It took some effort by Talikka to extract the database from the GTK archives, helped by the fact that he used to work for GTK and knew it existed. To his surprise the database included anomalous lithium values in the western part of the claim package he spent two years assembling. Unlike in the James Bay region where Dios is treating lithium in till as derivative of neary spodumene mineralized pegmatites, Talikka belives the lithium values are derived from precursor micas within granitoids. What makes the Savu play interesting is that nobody has every bothered to investigate rthe lithium potential of the Savu region which is best known for the Sokli carbonatite which hosts several hundred million tonnes of 12%-13% phosphate now owned by a government entity called Finnish Minerals Group. It turns out the southern part where there is a history of mineralized drill intersections was open so Aurion scooped it up. If the CLGB district consolidation does not rapidly unfold, a drill program by Aurion on the Kaares structural trend in the southern part of the 100% owned Risti property could deliver an Ikkari discovery scale surprise. Should that happen, B2Gold, which is the 70:30 partner with Aurion on the Kutovuoma property that is critical to optimal development of the 4.1 million ounce Ikkari gold deposit, would not waste time offering to buy out Aurion as a prelude to fighting Agnico-Eagle for control of Rupert. Although Aurion has not delineated a gold resource, a rising gold price would inject urgency into Rupert to approach Aurion, especially if a rising gold price pushes Rupert into an uptrend.

Map of Aurion holdings in Central Lapland Greenstone Belt

Cross section of PEA Mining Plan for Rupert's Ikkari deposit

Page 110 of PEA Technical Report has cluses for mine plan alternatives

Map of 70:30 Kutuvuoma JV with B2Gold

Comparison of Rock Sample Map and more recent Till Sample Map for Risti

Map of Savu Region Claim Blocks and Till derived Lithium Values

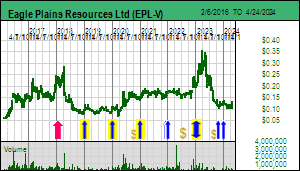

Jim (0:28:22): Why has Eagle Plains Resources, another KRO Favorite which did well earlier this year, recently seen its price decline?

Eagle Plains Resources Ltd was made a Fair Spec Value rated 2023 KRO Favorite based on its strategy as a prospect-generator-farmout junior focused on western Canada which also planned to drill its 100% owned Vulcan project in southern British Columbia. Vulcan is a candidate for the Sullivan Two Hunt that has bedeviled explorers since the 1970s, including Cominco, and later Ascot Resources for whom Eagle Plains CEO Tim Termuende worked as a junior geologist when Ascot drilled Vulcan. In recent years Eagle Plains has conducted two drill programs, the first one on the southern target area in 2020 to fulfill assessment requirements, and the second one last year in both the northern and southern target areas. The 2020 program was a bust in that the MT target turned out to be caused by graphite, but the two holes did answer a hypothesis about whether the assumed Sullivan Time Horizon, namely the contact between the Lower and Middle Aldrige formations, that guided past drilling was correct. It turned it was not, and Eagle Plans has been trying to develop a vectoring strategy to home in on a Sullivan scale zinc-lead-silver system based on this new understanding. The 2022 drilling on the southern and northern targets has turned EPL's attention to the northern Hilo-West Basin target where a 3,000 m 5 hole drill program is planned starting in mid June. This program will vector in on a new geophysical conductor which is likely pyrrhotite, but understanding it will give a clue where the less conductive zinc-lead mineralization is located. The drilling program is scheduled to begin by the third week of June.

By know I have been frustrated by so many failed Sullivan Two Hunts that my inclination is to just sit on my position and assume no discovery hole will be delivered. But it is always more fun to watch a game rather than wait to hear the outcome. EPL's Kerry Bates put together a 14 minute YouTube Video last year using a whiteboard and felt pens to explain the evolution of the original Sullivan deposit. It's worth watching to understand that Sullivan is actually a two stage system that starts with traditonal seafloor smokers that spew fluids into the water that form thin beds of mineralization interspersed with quiet period of sedimentation. The fluids come up the faults of a rift setting where blocks of rock are down-dropped to form "grabens". These traditional SEDEX deposits are not very interesting. in the case of southern British Columbia the stratigraphy was invaded by invaded gabbroic sills which did not introduce any mineralized fluids, but their heat convecting through the not yet consolidated sea floor bedding created mini explosions that fragmented the bending. In the case of Sullivan a later hydrothermal system found its way up the sides of a sub-basin filled this mess of mineralization, harvested the metals in it, and re-deposited them through a new sea-floor vent which in the case of Sullivan created a 150 million tonne monster. The work so far done in the Hilo area of Vulcan has delivered evidence that the first stage took place. Now they are looking for evidence that the second remobilization and enrichment phase took place. The final step will be to figure out where the resulting Sullivan 2 deposit ended up after post-deposition folding and faulting.

Eagle Plains, however, did not gain 50%-75% earlier this year because Sullivan 2 Hunt addicts were getting worked up the upcoming drill season. In January Eagle Plains announced a plan to put all its royalties into a subsidiary and spin it out on the basis of 1 Eagle Royalties share for every 3 Eagle Plains shares. As usual this process took longer than expected by May 18 was the day of record, which meant that with two day settlement May 16 was the last day to buy EPL to get the spinout. The deal was structured so that the subsidiary would merge with a private company that would conduct a $3 million financing before listing on the CSE. The terms implied a value of about $0.30 for Eagle Royalties share or about $0.10 of value created for each Eagle Plains share. Once the spinout happened there was a $0.10 drop in the price of Eagle Plains. Eagle Royalties began to trade on the CSE on May 24 but has been fairly illiquid because there was a delay getting the spinout shares into the EPL shareholder accounts. Also, the spinout stock will be escrowed with 20% released on listing and 20% each 3 months. For US residents such as myself I am happy to wait a year because the cost base is zero and I prefer to pay long term capital gains.

Eagle Royalties now owns royalties on 52 properties still owned by Eagle Plains. They generally consist of a 2% NSR of which Eagle Plains can buy back 1% any time for $1 million. The most important royalty is a group of 0.5%-2.0% covering parts of Banyan's Aurmac gold deposit. There is no buyback on that royalty which is Eagle Royalties' flagship royalty. When I added Eagle Royalties to KRO I was surprises how many there were. I assumed that Eagle Plains was spinning out the royalties it had retained when it farmed out properties. In fact, Eagle Plains invented a 2% NSR for every property not yet farmed out and retained an unrestricted right to buy back 1% from Eagle Royalties for $1 million. In other words, if any of these projects gets developed into a mine, a 1% NSR will be worth more than $1 million, which EPL can repatriate for the benefit of Eagle Plains shareholders. EPL is operator of these projects, most of which do not currently have active farmouts, and it is typically retained by the farm-in junior to operate the program. Now that the 2% NSR exists, Eagle Plains will not have to negotiate with a farm-in partner about keeping a royalty. All it needs to focus on is the combination of cash, stock and spending timeline the other party must fulfill to earn an interest. Eagle Plains has also retained about 5.2 million Eagle Royalties shares. I had not understood this aspect of the spinout deal. I thought Eagle Plains was giving away its collection of royalties and it would be Eagle Royalties shareholders who benefit from any future upside. I think Eagle Plains will soon recover the $0.10 drop is suffered after the spinout. It is a gift to Eagle Royalties that will keep giving back as long as Eagle Plains sticks to its prospect-generator-farmout strategy. If Eagle Plains gets lucky with a Vulcan homerun, the prospect portfolio would survive through a spinout.

Map showing how much of Aurmac Royalty overlaps with BBanyan's gold deposits

Disclosure: JK owns shares of Brunswick, Dios and Eagle Plains; Aurion, Brunswick a Eagle Plains are Fair Spec Value rated Favorites; Dios is Bottom-Fish Spec Value rated

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch June 2, 2023: Outokumpu funds FPX Nickel into 2025

Jim (0:00:00): What was the Metals Investor Forum show like this past weekend?

The attendance and mood at MIF May 26-27, 2023 was subdued in comparison to the MIF January 27-28, 2023 show in Vancouver when the speaker hall was full with some people standing in the back. Turnout was better on Friday than Saturday thanks in part to a gorgeous Vancouver weekend. The shift is not surprising. I used my KRO Search Engine this week to walk through all the TSX resource sector listings and was left with a distinct impression. Producers, whether focused on precious or base metals, were down 20%-40% from their March peaks. For the base metal producers this is understandable because China's weak post zero-covid rebound has sapped demand for metals, with copper in a conspicuous retreat and most metals following. With China not carrying the global economy onward the focus has been on the potential recession impact of rising interest rates, made worse by the prospect of a US default caused by the failure to lift the debt ceiling. The gold producer downtrend is puzzling because gold has spent the past couple months trying to convert $2,000 from a ceiling into a new base from which higher real price gains can be launched. The market clearly lacks confidence this will happen. Fortunately the risk of a debt ceiling related default has been pushed into 2025.

Another example of the subdued mood was the dinner MIF hosts on Friday evening for the speakers and exhibitors who can bring along a high net worth guest. This dinner is usually very popular and is held at an excellent restaurant, in this case Ophelia, a high end Mexican restaurant on the south side of False Creek. It's only a ten minute cab ride from downtown so the location was not an obstacle. Fewer people than expected showed up and those that did generally left early. This gave me an opportunity to get a crash course in mezcal from Ophelia's bar manager, Erik Mendoza, a forty-something who spent 15 years working in the New York bar scene and knows his stuff. Having done enough Mexican site visits I am reasonably familiar with the varieties of tequila, but my knowledge of mezcal was limited to a vague college memory of a type of tequila with a worm in the bottle, and a recent attempt to learn more which left me with the impression that mezcal is a tequila that tastes like burnt rubber tire. Erik introduced me to a range of mezcals that opened my eyes to what I think will be a growing trend. Unlike tequila which is made from blue agave plants grown in Jalisco state in what has become an industrialized process that allows tequila to be branded with celebrity names like George Clooney, mezcal is made from any variety of agave harvested and prepared in an artisanal manner that involves first roasting the agave heart in underground ovens. This gives mezcal the smoky flavor that distinguishes it from tequila. Most mezcal is produced in Oaxaca state though there is no legal restriction such as with tequila and Jalisco state. Not surprisingly, given the high degree of manual labor involved, bottles of mezcal tend to be more expensive than decent quality tequila. Erik has even imported the hand-painted half gourds that are the traditional way to drink mezcal. He admits that the Vancouver audience has been slow to embrace mezcal, but I think it is only a matter of time before people become intrigued by the complexity and variety that mezcal offers.

I have now assembled into a KRO Blog Comment all the YouTube links to my presentation, my companies' presentations and the Backstage Interviews as well as the MIF Panel Discussion that I moderated. I've also made available a link to the pdf for my powerpoint for those who want to see the graphics behind my talk: Two Global Crises: what they mean for resource juniors.

Sparse Speaker Dinner Turnout gives Ophelia's Erik Mendoza a chance to educate JK about Mezcal

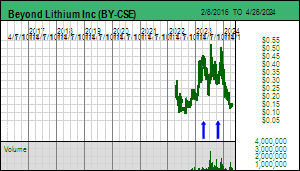

Jim (0:05:02): How were the two companies in your session, Beyond Lithium and West Vault Mining, received?

In terms of traffic experienced by the two companies in my session, Beyond Lithium Inc and West Vault Mining Inc, Al Frame and Sandy McVey indicated about 10%-20% of the conference delegates they spoke with were serious and knowledgeable. That wasn't a surprise in the case of West Vault which is a gold proxy buyout story, but Al Frame was surprised by the level of lithium knowledge, a relatively new concept for retail investors. There were no other lithium pegmatite companies presenting at MIF though there was one junior investigating direct lithium extraction of Saskatchewan brines. After my presentation Saturday afternoon and those of the two juniors in my session I moderated the Newsletter Writer Panel Discussion. I asked six questions of which the last two were about the energy transition and lithium. I first introduced the concept of Lithium Mania 2.0 a year ago at the MIF May 2022 conference and I was curious why I am still an outlier, so I asked, "To what extent do you have a lithium story in your portfolio of covered stocks, and, if none, what do you need to see to embrace Lithium Mania 2.0, namely the search for lithium pegmatites in places like Canada?"

The panelists were generally dismissive of lithium and it is worthwhile to listen to the responses just to appreciate how early we still are in the Canadian lithium boom which tried to get going during the 2015-2018 cycle, but unlike their Australian pegmatite counterparts, the Canadian pegmatite hunters were largely still born. In fact, in 2018 I had a predecessor of Patriot Battery Metals in my MIF session because its Corvette project, which it had acquired for the pegmatite lithium story, was next door to Midland's Mythril project which appeared to be a major new copper discovery for the James Bay region. There is currently a major mismatch between the perception of Australian investors with regard to Canada's lithium pegmatite potential and that of North American investors. Some of the panelists were dismissive because they are ideologically wedded to the claim that fossil fuel combustion as a primary driver of climate change is a hoax. Some think that electric vehicles are a passing fad and the world will never need a six-fold expansion of lithium supply by 2030. Some complain that lithium is an industrial mineral like feldspar or kaolin subject to end-user specifications when in fact it is a metal with final product purity requirements like any other "industrial" metal. Some complain that lithium enriched pegmatites are everywhere and that this will lead to massive over-supply, so why go exploring for it? Never mind that we first need an exploration boom that develops the best deposits before over-supply problems arrive five years down the road.

Some, who have seen stocks like Patriot Battery Metals and Sigma Lithium soar during the past couple years, feel they are too late, that they missed the boat. Sigma Lithium was a Brazilian version of the 2015-2018 Australian pegmatite boom, but Patriot is part of the second wave, equivalent to Dia Met in 1992 which boat nearly everybody missed. One geologist (not a panelist) who spun his wheels two decades chasing diamonds without success and recently refocused on gold and base metals declared that he is not an ambulance chaser.

What I think is missing is a proper understanding of the underlying dynamics of the energy transition, in particular the move by carmakers to shift to EV sales whether or not forced to do so by government climate change policies. Yes, most of us, including myself, missed the first lithium wave that began in 2015, stalled in 2018-2020, but came to life again in 2021 when EV sales caught up with the Australian over-supply. I was skeptical EVs would become more than a fad, and assumed the Lithium Triangle brines would provide whatever the world needed. Now I know better. Those first wave success stories will deliver the first half of the required 600% expansion. The second wave is about delivering the second half needed by 2030.

Patriot Battery Metals is the poster child for this second wave. Even if it delivers a 100 million tonne deposit in July grading 1%-2% Li2O, that solves only a fraction of the lithium supply needed. The EV sector needs a couple dozen such deposits. It is entirely plausible that Patriot Battery disappears in H2 of 2023 at $20 plus, a $2 billion plus buyout within three years of starting a drill program. This summer Canada will witness the biggest boots on the ground prospecting boom in its entire exploration history. Pegmatites are indeed everywhere, but they were not created equally. Only some will be 10 million tonnes plus and grade 1% Li2O or better with low iron and uranium impurities. You won't know until you look. Patriot will emerge as the case study of what happens when a junior finds a pegmatite that appears to have scale and grade.

It is interesting to hear from Al Frame that Beyond Lithium is receiving a lot of serious joint venture inquiries for its 60 plus Ontario lithium property portfolio from other juniors who do understand what Lithium Mania 2.0 will be all about. Beyond is in no hurry to do a farmout. During June-July exploration VP Lawrence Tsang will have prospecting teams checking out every property to see which ones have the best potential. During August-September a couple dozen of the most promising properties will receive closer examination with the goal of turning them into targets that can be drilled in the fall or early 2024. I expect Lithium Mania 2.0 begin to simmer during the summer when rumors leak from the field into local communities from where they propagate into social media networks. Now that the threat of a debt ceiling related default has disappeared, speculators will begin to move in from the sidelines. If Patriot turns into a liquidity event, much of the proceeds will be recycled into lithium pegmatite juniors just getting started. Even juniors with a two buck chuck marketing budget will be swept into the stratosphere. September will be the breakout; the MIF panelists have three months to do get their heads around the concept, do their homework, and come up with their own favorite picks. So long as the junior has a competent exploration team and sufficient funding to put boots on the ground this summer, it is unpredictable which one will emerge as the next Patriot.

JK Moderates MIF Discussion Panel featuring Eric Coffin, Peter Krauth, Greg McCoach & Robert Sinn

Jim (0:15:45): How important is the new strategic investor FPX Nickel announced this week?

FPX Nickel Corp surprised us on May 30 with news that it had closed a $16 million financing at $0.60 with Outokumpu, the Finland based stainless steel producer which specializes in ESG credentialed products. The stock had closed at $0.425 on Monday, so the $0.60 stock price represents a 41% premium above market. Last year the stock was at $0.39 when FPX announced a $12 million financing at $0.50 with a secret strategic investor. That was at a 28% premium to market. No warrants were included in either case. The financing boosts FPX's treasury to over $30 million, enough to carry permitting and feasibility study related work well into 2025.

Unlike last year's strategic investor, Outokumpu secured rights to offtake 60,000 tonnes of nickel over 8 years, or 7,500 tonnes per year which is only 17% of the 44,900 tonnes production projected by the 2020 PEA. But that offtake right does not come with any fixed nickel price or a specified discount like Elon Musk's Tesla has pursued. It will be based on LME market prices. Why has Outokumpu agreed to such an offtake deal? The stainless steel producer recognizes that ferro-nickel concentrate from Decar will have a high ESG rating, and in light of FPX Nickel's recent demonstration that battery grade nickel sulphate can be made from the concentrate, is worried that its own need for ESG credentialed nickel could experience competition from carmakers. Outokumpu once used to be a mining company but it sold off that business some time go. Now it is a global downstream stainless steel producer. This financing is important because it is the first evidence that a stainless steel producer is happy with the ferro-nickel concentrate Decar will produce.

Outokumpu now owns 9.9% of the 270.6 million shares issued (284.4 million fully diluted), while last year's secret investor drops to 8.9%. That investor has a 7 day window to decide if it will get back to 9.9% by also buying additional stock at $0.60. My suspicion is that the secret strategic investor is a downstream customer within the EV supply chain. I don't think it is a chemical company, a battery maker or a carmaker because none of these entities have any special reason to keep their identity secret, and even if the name were revealed, I don't think the market would care. Yet Martin Turenne insists the market would care. My bet is that the secret strategic investor is an entity that cares about ESG credentials, is not yet in the EV manufacturing business, but may one day become a carmaker that needs clean nickel for its battery. The secrecy is necessary because this may never happen. My prime suspects are Apple and Google, both of whom are working on self-driving cars whose future is probably 2030 and beyond. That twins well with the development timeline for Decar. And if Google or Apple were identified as the strategic investor, that would rock the market.

There has been whining from frustrated shareholders about the dilution at a price which seriously undervalues FPX based on the PEA and what metallurgical derisking has been since the PEA. In fact, the secret strategic investor may also be grumbling to itself because since it put up money at $0.50 FPX has validated the ferro-nickel concentrate flowsheet and optimized the nickel sulphate flowsheet. And now a stainless steel producer gets to buy 9.9% at $0.60? Tough luck secret strategic investor, it was your decision not to help reduce market skepticism about FPX Nickel's plan to produce nickel from awaruite, a natural stainless steel never before commercially exploited.

The next big milestone will be the PFS still expected in September. The market wants to see what inflation and revisions to the flow-sheet have done to CapEx and OpEx. I've applied a 20% cost escalation to the PEA assumptions and the project does not clear development hurdles at the $7.75/lb base case price used in 2020. But it does at the current $9.72/lb nickel price. What will be the base case price used for the PFS? There is concern about the nickel price due to recent expansion of Indonesian nickel supply bankrolled by Chinese entities. China's EV fleet is shifting away from nickel cathode batteries to LFP batteries. Its economic rebound after giving up on zero-covid has been weak. Economic studies at the PFS or higher level have a history of shocking shareholders with cost blowout, but the body language from FPX Nickel suggests there is no negative surprise coming. A rule of thumb is that the after-tax NPV should match or exceed CapEx which in my escalated PEA scenario is USD $2 billion or about CAD $2.7 billion. How close the NPV will come depends on the discount rate used. For long lived projects like Decar (35 years) the difference between 5% and 10% is huge. The potential duplication of Baptiste by Van on the other side of the mountain, which could be developed within ten years of bringing Baptiste on stream, may allow any shortfall to be made up as a "strategic premium" in the eye of a mining company like Vale considering a buyout. If the PFS clears this hurdle fair value should be 50%-75% of the NPV which is $4.75 to $7.12. What FPX management is willing to accept could be less after spinning out the Jogmec alliance and CO2 Lock, the carbon capture story. So investors get only 5-10 times the current price.

The key importance of the Outokumpu financing is that FPX Nickel is no longer in danger of being caught by a recession and needing to raise money at predatory prices while a producer like Vale plays a waiting game. Retail investors in advanced juniors have been shafted multiple times in the past year by deeply discounted Bay Street bought deals from whose levels the stock has not recovered. Nobody is going to take over FPX with a bid that doesn't approach fair value; existing shareholders have too large a position to make a hostile bid feasible. The low valuation is an obstacle to a takeover bid because a producer can only pay a modest market premium. FPX Nickel's biggest challenge is to secure a higher valuation so that a potential developer can make an offer FPX management can consider and which will not get the CEO of the bidder fired if accepted. The big uncertainty is the PFS, which will be resolved within another four months.