Hello Guest User, You are visiting this website from a computer with an IP address of 172.70.100.56 with the name of '?' since Sat Apr 27, 2024 at 12:14:10 PM PT for approx. 0 minutes now.

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kauser Watch September 20, 2023: Rio Tinto success at Midland's Galinee

Jim (0:00:00): What do you plan to talk about at this weekend's Metals Investor Forum in Vancouver?

This KW Episode was recorded September 20, 2023 and was supposed to be posted ahead of the September 22-23, 2023 Metals Investor Forum in Vancouver but travel complications got in the way. I have consequently converted the written portion into a summary of the conference. Compared to the January MIF when a much larger speaker hall had only a few empty chairs and some of the audience was standing, turnout was considerably lower, though better than I had expected given the pall that has settled onto the junior resource sector. The speaker hall was typically two-thirds full. One thing that struck me as odd was the relative absence of industry people not involved with the presenting companies who usually remain in the exhibit area while investors flock to the talks. The videos of the presentations, panel discussions and backstage interviews are starting to show up on the MIF YouTube Channel.

I only had time to see Joe Mazumdar's presentation, Into Thin Air - Oxygen Required to Support Junior Companies which, as suggested by the title, dealt with the difficult financing environment for resource juniors. Joe tends to be more focused on juniors with advanced projects which are still able to do bought deals placed with institutional investors (these tend to be free trading right away), though almost always at a steep discount to prior trading levels to which the stock almost never recovers. As I watched his parade of charts, most of which had a closing price below the recent financing price like the stock was heading off a cliff, it struck me the message Joe was offering is that the better the junior, the more ordinary investors should avoid them in this market.

The difficult financing environment became clear to me when I processed the private placement data the TSXV publishes in its monthly review. Since 2009 I have had the ability to separate the resource listings from the rest. The resource listing only chart shows strong financing periods occurring in mid-2009 to 2012, 2016-2018, and mid-2020 until mid 2023. July's resource sector private placement activity of CAD $119 million was the lowest since April 2020 when the market was reeling from the eruption of the Covid pandemic. But I was shocked by August's surge to $328 million until I drilled into the data and realized that $109 million represented the financing Albemarle did in Patriot Battery Metals after it published its CV5 maiden resource estimate in Quebec's James Bay region, and $86 million was raised by NGX Minerals Ltd for its Los Helados and Lunahuasi copper-gold projects in Chile. Subtract these two financings linked to very strong exploration results and the total was $133 million, slightly better than July's total. But when you take away the $33 million raised by Jervois Global (623 million at $0.053 - Australian money) and $21.5 million by Electra Battery Materials, both of which are cobalt refinery stories, the total was only $79 million spread among only 45 TSXV resource listings. This is bad and I will be curious to see how September fared, usually a stronger "back to work" financing window.

I recently updated the financial status of the 1,160 TSXV resource listings which brings them up to date to the end of June 30 and the outlook is very dismal. There are 714 juniors (62%) with positive working capital totaling $4.5 billion while 446 (38%) have negative working capital totaling $3.2 billion. Of those with positive working capital about $2 billion is parked in juniors trading below $0.30. Next month I begin research for my 2024 Bottom-Fish Collection. The KRO Search Engine that is part of the annual USD $450 membership will save me a lot of effort. The only positive news from my TSXV financing charts is that TSXV resource listing traded value, which was substantially less than non-resource listing value from 2013-2021 except for that crazy gold window in H2 of 2020, has been higher than non-resource listing traded value since 2022. The numbers are in fact worse for the non-resource listings because these are artificially boosted by a few oddball listings like Topicus.com which are established foreign companies that don't belong on a venture exchange.

My September 23, 2023 MIF presentation, Exploring for Yellow and White Gold (PDF version of Powerpoint), continued the theme I kicked off at the January MIF, namely that the dominant big picture trends shaping the resource junior future are the geopolitical conflict between Global West and East and the energy transition. In the September talk I focused on gold and lithium to emphasize the entirely different narratives behind these two metals. The basic argument for gold is that a higher real price will emerge as the Global East works to reduce its reliance on the US dollar to settle international trade. A recent theme has been the emergence of a premium for Chinese domestic gold above the international price caused by a Chinese gold import ban to stop the outflow of US dollars. The optics of a domestic gold premium, however, is an affront to Xi Jinping's message that everything is wonderful in his autocratic China. He can censor just about everything else but not the fact that gold costs Chinese citizens more to buy than anybody else in the world and that isn't stopping them. The import ban has been lifted but the curious fact remains that China has not banned the purchase of gold by its citizens.

Gold seems stuck in the $1,800-$2,000 range, unable to convert $2,000 from a ceiling into a base for further gains. That is a problem because $400 gold in 1980 inflation adjusted to the present is $1,489, which means that at the current price gold has achieved a real price gain of only 29% during a period when mining doubled the above ground gold stock by harvesting all the low hanging fruit created by the gold's price move during the 1970s after it was liberated from its $35 per ounce prison. A common refrain these days is one of puzzlement, "why does the market not care that gold is at current levels?"

To explain this conundrum I created a gold rock value matrix where I show the in situ rock value for different combinations of grade and gold price. I then colored each cell in the matrix red where the rock value is too low even for open pit mining, yellow where only open pit mining is possible, and green where underground mining is also possible. I enclosed in a red box the rock values possible at the various gold grades between $1,800-$2,000 gold, and in a blue box between $2,000-$3,000. You have to look very hard to see the value difference a move by the gold price into the $2,000-$3,000 range makes. And yet, every time gold makes a surge toward the $2,000, and sometimes, as has happened twice now since 2020, breaches $2,000, risk capital flows into the resource juniors, whether or not their flagship project is focused on gold. The $2,000 gold price ceiling has become an optical obstacle for the resource juniors. If gold can definitively pass $2,000 so that $2,000 becomes the base, it would unleash a bull market for resource juniors, even though in value terms it would not make a huge difference.

The hesitation I have about this hope for gold establishing a new $2,000-$3,000 price range is that I am not sure what will cause such a move, and worry it will be something so catastrophic for investors in the Global West that there will be zero risk appetite for exploration and development resource juniors. During the May 2023 MIF I introduced West Vault Mining Inc as a leveraged proxy for a real price move beyond $2,000. West Vault is a Good Speculative Value rated KRO Favorite on the premise that a strong upward move in gold will not be of "end of the world as we know it" nature. In the September 2023 MIF I pivoted to the opposite end of the spectrum by introducing Silver Range Resources Ltd, a traditional prospect-generator-farmout junior focused on high grade gold-silver epithermal and carbonate replacement prospects in southwestern United States. The strategy here is that if we are stuck with $1,800-$2,000 gold as a tradeoff for geopolitical conflict not escalating into catastrophic territory, then we should be placing bets on juniors positioned to make high grade gold-silver discoveries in secure jurisdictions.

CEO Mike Power did an excellent job with his Silver Range Presentation, which included a simple slide explaining what sort of prospects he is seeking. Nevada has seen a lot of exploration for epithermal deposits in the nearly two centuries since Comstock was discovered, so the chance of face-planting into a mineralized outcrop is pretty much zero. However, after my June site visit to Nevada, described in KW Episode - Tonopah Adventure Tour Part I and KW Episode - Tonopah Adventure Tour Part II, I am convinced Nevada will undergo a revival of interest in high grade epithermal plays.

Mike presented 4 target scenarios: 1) another Comstock sticking out of the ground, 2) a tiny or weakly mineralized outcrop, 3) no outcrop but alteration at surface hinting at a hydrothermal system, and, 4) deep conceptual targets. Silver Range is only interested in the second type because these can be identified through archival research and prospecting in the field that looks for old workings where previous operators gave up. This is a tip of the iceberg exploration strategy where the focus is not so much the mineralized outcrop but what Silver Range can learn about the strength of the underlying system based on the geochemical nature of the alteration at surface. This involves new field instruments and deposit models not available to the prospectors of yore. It involves a lot of field work and geological knowledge, and it is not the sort of strategy a life-style junior can pursue. Because Silver Range is seeking to make discoveries grading 5 g/t gold equivalent or higher, all of which will likely have to be underground mined, a higher gold price is irrelevant to the success of this junior. It's all about applied method. On the other hand, the optics of gold trading in the $2,000-$3,000 range would stimulate strong farm-in interest, with Silver Range able to get increasingly stronger terms. So indirectly the success of Silver Range, thanks to the work it is doing now in Nevada, Arizona and soon also Utah, is positively leveraged to an upside move in the price of gold.

Silver Range Resources Ltd is Bottom-Fish Spec Value rated because it does not have a strong treasury, but that is something which could change when one of the private companies to which it vended property goes public. In the main presentation Mike Power mentioned that one of them has a pricing which implies a $19 million value for the 10% equity stake Silver Range acquired when it contributed its namesake Silver Range (Keg) project in Yukon's Faro silver-lead-zinc district to Broden Mining Ltd. He goes into greater detail in the Backstage Interview. If Broden goes public in 2024 as an advanced junior, Silver Range may be able to monetize its equity stake by selling it to an institution. Such a non-dilutive "financing" via an asset to which the market currently assigns zero value would be transformative for this junior.

With regard to the energy transition I focused on lithium, a white gold contrast to yellow gold because speculation about lithium plays has nothing to do with expectations for a higher lithium price. During 2022 the price of lithium carbonate was stuck in the obscenely elevated range of $30-$35/lb, a far cry from the price below $3/lb during the 2018-2020 lithium winter caused by the extremely successful mobilization of lithium supply by Australian companies during Lithium Mania 1.0 in 2015-1017 from Australia's strong endowment of LCT-type pegmatites. Below $3/lb the EV sector will never reach the car sales required for the 2050 net zero emission goal unless meanwhile there is a miraculous breakthrough in the cost and efficiency of direct lithium extraction (DLE) technology or a better and cheaper battery than lithium ion emerges. The lithium winter slowed supply development which resulted in a reversal of the imbalance in 2021 as EV sales took off, especially in China which has a non-climate change related strategic reason to shift transportation away from oil to electricity. The elevated spot prices of 2022 are not sustainable over the long run because at that price far more claystone and pegmatite lithium is in the money than the world will ever need. During 2023 the price of lithium carbonate has plunged into the $10-$20/lb range where it has gyrated and is currently threatening to drop through $10/lb, creating fear of another lithium winter.

The resource junior audience, trained by decades of obsessing about the need for a higher gold price, does not like the optics of a crashing metal price, so Lithium Mania 2.0 has been slow to get rolling. However, I like the lithium sector because I do expect the price of lithium carbonate long term to settle into the $5-$10/lb range, though during the rest of the decade we may see periodic surges back to the $30/lb level. But because lithium carbonate or hydroxide is sold under long term contracts, such spot price spikes will do little for the bottom line. I have done to my lithium rock value matrix the same as I did to the gold rock value matrix; colored red those grade-price cells where for hardrock deposits (claystone and pegmatite) production will never be profitable, yellow those where only open pit mining is possible, and green those where underground mining is feasible (note that the grade is lithium oxide - Li2O - claystone resources are usually reported as elemental lithium which you must multiply by 2.153 to get lithium oxide equivalent). I've also boxed in blue the $10-$20/lb price range prevailing this year and in red the $5-$10/lb price range I think will be the long term reality. Assuming your target is a 1% plus Li2O grade, the shift to the lower price range does not change the underground mineability of a pegmatite. Yes, the after-tax net present value will be lower, but most pegmatites that will be discovered will be outcropping or near surface and be at least partly open-pittable. What the general investing public not based in Australia does not quite yet understand is that exploration for LCT-type pegmatites in jurisdictions like Canada and Brazil has barely begun and there is an awful lot of low hanging fruit available for harvesting.

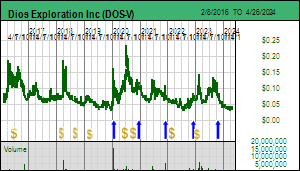

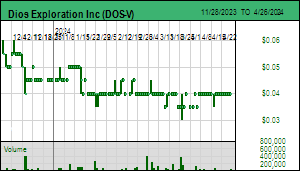

In my presentation I contrasted Silver Range Resources Ltd with Dios Exploration Inc which had indicated in Q2 that it would be ready to participate in the September 2023 Metals Investor Forum. I liked the contrast because both juniors are engaged in science based target generation. Many of the members of the James Bay Lithium Index are there simply because they owned land in the region for its gold and base metals potential whose prospective rocks happen to overlap with LCT-type pegmatite potential. Quite a few members own land optioned from armchair speculators who map-staked claims based on closeology and not so much on relevant geology or meaningful interpretation of lake bottom sediment data. But with the James Bay district only very recently being recognized for its world class LCT-type pegmatite potential, and with historical exploration laser-focused on gold and base metal related geology, which does not have a perfect overlap with LCT-type geology, the dumbest, most horrible resource junior could make a billion dollar discovery so long as it retains a competent exploration team and puts boots on the ground.

A small group of companies which includes Brunswick Exploration Inc and Dios started acquiring land in 2022 based exclusively on LCT-type pegmatite potential. In the case of Brunswick Bob Wares' team conducted archival research for documented pegmatite showings and analyzed commercial satellite imagery to stake land in James Bay where a pegmatite of some nature was outcropping. This is first order exploration because once boots land on a pegmatite the use of a handheld XRF or LIPS reader will quickly establish if the pegmatite is LCT-type. If spodumene crystals are present a visual assessment of the distribution within the pegmatite can give a rough idea of grade potential. Another type of first order exploration is being done by juniors like Champion Electric Metals Inc which have acquired large land positions covering rocks that have seen comparatively less field exploration because they are not as prospective for precious or base metals as trends like PMET's Corvette trend. The archives would have a much lower frequency of references to mapped pegmatite outcrops, which means grid-based prospecting will need to be done that could result in the discovery of a major LCT-type pegmatite peeking out from under the moss.

Dios did not start taking the LCT-type pegmatite potential of its James Bay backyard seriously until last September, so it was late to the game. But the tools it brought to the game included a detailed knowledge of the region's glacial history learned during its decades of till sampling activity, initially for diamond indicator minerals and later for precious and base metal indicators. Coupled with internal proprietary till sample data, Dios went after second order targets by analyzing lake bottom sediment chemistry in the context of glacial transport and relevant geology, leading it to areas where commercial satellite imagery revealed outcropping pegmatite and in some cases, even documented pegmatite when you dug deep enough into the archives. This science based approach to generating targets is similar to what Silver Range is doing in southwestern United States. The result is a collection of second order exploration generated claim blocks in the middle of nowhere within the James Bay region. The reason I am keen about this junior whose marketing budget in H1 of 2023 was only big enough to buy a bottle of two buck chuck is that its type of prospect could contain low hanging fruit nobody has ever seen because there wasn't a precious or base metals reason to walk the ground.

Unfortunately the forest fire closure of the James Bay region that began at the end of May robbed the industry of 3 critical summer months for boots on the ground prospecting. Dios thus declined to participate in my MIF session because it realized it needed to get as much done in September-October as possible to put it in a position to drill meaningful LCT-type pegmatite outcrops in Q1 of 2023. Many juniors will not get sufficient work done in the remainder of the prospecting season to have a good story to tell at the end of 2023, some because logistics has become scarce, some because their claims are in areas impacted by the September 15-October 15 moose hunting season, and some because James Bay may get an early winter onset. Once the ground is blanketed with snow, if you do not have a clearly outlined drill target, there will be nothing more to do until June of 2024.

This frustration may, however, be a blessing in disguise. During the May 2023 MIF conference I moderated a Panel Discussion. The bad fire closure news was still around the corner and I was pretty pumped about Lithium Mania 2.0 exploding during the summer, but dismayed that my peers were uniformly negative about lithium plays. Some of this negativity was due to being a Trumper stuck dismissing anything to do with climate change mitigation. Some of it was due to skepticism that EV adoption would ever go beyond society's economic elite. But most of it, I suspect, was due to a sense that they had missed the boat.

However, the bleak overall resource sector market decline after Q1, the forest fire closure of James Bay, and the nasty bungee plunge undertaken by lithium carbonate delayed lift-off, stranding most boats at the dock. At the same time since that May MIF panel discussion PMET delivered a world class resource at CV5, Allkem upgraded Galaxy-Cyr to world class status confirming the widespread nature of the lithium pegmatite endowment of the James Bay region, Albemarle came back to Liontown with a AUD $6 billion bid for Kathleen Valley accepted by management but subject to due diligence, and Toyota stunned the world with a boast that it had figured out how to cost effectively make a solid state lithium ion battery that is safe, the holy grail of the industry because it would allow lithium metal to substitute for graphite in the anode.

Toyota, which has sat out the EV boom by focusing on selling hybrids and working on hydrogen fuel cell technology, arguing that current battery technology is not good enough to scale to the sort of mass adoption required by net zero emission goals (one of the May panel's reasons for rejecting the EV story), claims it will be able to sell a high end model by 2027 which will get a range of 1,200 km on a 10 minute charge. But most important of all, it claims that it achieved this with a breakthrough in manufacturing cost which previously had made a conceptually viable solid state battery configuration prohibitively expensive to build. The reason lithium metal cannot be used in the anode with the conventional fluid electrolyte between the cathode and anode is that the ion flow causes lithium dendrites to grow. If these puncture the electrolyte wrapper the short will cause thermal runaway and turn the car into a fire bomb. So graphite became the compromise anode and remains the anode even for the lithium iron phosphate (LFP) batteries with which cheaper EV models are equipped but which come with the range and charging limitations that make a cheap EV of little appeal to consumers accustomed to refueling their ICE cars at a nearby gas station within 10 minutes. The beauty about a manufacturing breakthrough is that over time Toyota will make the process more efficient, just as happened with solar panels during the past decade. Thus by 2030 it is possible that Toyota relaunches its popular Camry and Corolla models as affordable EVs with a better range than the ICE versions and the same refueling time. Toyota, which was threatened with marginalization by its non-EV strategy, has positioned itself to become a Tesla killer.

Rio Tinto in 2021 predicted that the world will need 60 Jadar equivalent mines by 2035 if the EV contribution to the 2050 net zero emission goals is to become reality. This prediction was premised on the assumption that a solid state lithium ion battery will never become reality. But if what Toyota claims is true, the amount of lithium used in a battery will more than double, so the world will need at least 120 Jadars by 2035. And a Jadar is roughly equivalent to a Kathleen Valley or CV5 pegmatite deposit. And how did lithium stock prices respond amidst all this good news? They generally went down.

The Canadian attitude toward lithium, however, is changing. First, I was surprised to see Targa Exploration Corp be part of the September MIF show, one of Gwen Preston's picks. Targa has assembled lithium pegmatite plays in Saskatchewan, Manitoba, Ontario and Quebec. Among its first acquisitions was the Opinaca project it acquired from Zach Flood's Kenorland Minerals Ltd in late 2022 for stock and a 3% NSR. Kenorland is a Fair Spec Value rated KRO Favorite based on its status as a prospect-generator which develops large conceptual plays and farms them out to both majors and juniors. The Opinaca project is in the James Bay region in the middle of nowhere. Why? Because back in 2021 Kenorland looked at the James Bay region for its lithium potential, well before Brunswick's Bob Wares started looking, and conducted its own till sampling program in an effort to tighten the source of the lake bottom sediment anomalies visible in the government data set. The brains behind this strategy was Francis Macdonald who has since left to head Li-FT Power Ltd after it acquired 3 James Bay lithium prospects from Kenorland. Li-FT used the James Bay prospects to expand its market cap so that it could acquire a collection of known LCT-type pegmatites in the Northwest Territories east of Yellowknife which is now its primary focus. Kenorland in turn has managed to sell the Li-FT stock for about $14 million in proceeds. It holds a 9.9% stake in Targa which only recently finally put boots onto the Opinaca ground. This is a second order type of target similar to those Dios has generated, so it is entirely possible that overnight Targa becomes a discovery sensation.

Not only was I pleased to see a James Bay lithium junior at September MIF recommended by a newsletter peer, but I also observed a dramatic attitude change in the two panel discussions I was part of. On Saturday September 22 Joe Mazumdar moderated the Day 1 Panel Discussion: Making Money in the Current Resource Equity Markets. Whereas at January MIF neither he in his presentation nor Jean-Marc Lulin of his pick Azimut Exploration Inc could barely bring themselves to utter the word "lithium", on Saturday he was very much on top of the evolving lithium space and enthusiastic about the potential. On Sunday September 23 Gwen Preston moderated the Day 2 Panel Discussion: What Caused Excitement this Summer? And What's Next?. Again there was a brand new openness to the idea that a lithium exploration boom was a distinct possibility.

Yes, most people including me missed the PMET boat, and yes, the Brunswick boat I recommended in June 2022 at Toronto MIF has gone up five-fold since then, but most juniors, including those with projects in the James Bay region, have barely moved on the upside since getting into the pegmatite lithium sector. Meanwhile Brunswick's boots on the ground have established a substantial corridor of spodumene enriched pegmatite outcrops at the Mirage project which the market is pricing at just under $200 million, a tenth of the valuation of PMET at the price where Albemarle bought a 4.9% equity stake for $109 million after the CV5 resource estimate was released. Most investors do not understand that the EV future will not happen unless lithium grows into a $200 billion annual market by 2035. They do not understand that a lower lithium price is not a bad thing for the market because it ensures that only the better grade and size discoveries will undergo a rocket launch toward a $2 billion valuation. They do not understand that the future pegmatite lithium sourced supply hinges on the exploration efforts of juniors in jurisdictions like Canada and Brazil. But the pool of those who do is starting to expand beyond Australians, and the most important takeaway from the September 2023 Metals Investor Forum is that my peers are starting to understand and research their own favorites. Lithium Mania 2.0 may start lifting off in Q4 of 2023, but it will definitely be exploding on the upside in 2024 as it gains eyeball critical mass. The 2023 forest fire closures, bad as it was for James Bay juniors, has bought everybody else time to get positioned.

Two Global Crises as Key Drivers for Resource Juniors

TSXV Financing Activity 2009-2023: Resource and Non-Resource

TSXV Resource Sector Fianncing 2009-2023 by Financing Type

TSXV Resource Junior Working Capital Distribution

TSXV Positive & Negative Working Capital Distirbution by Stock Price Range

Comparing the Long Term Gold Price Trend to its Inflation Adjusted Price

Gold Grade vs Price Rock Value Matrix

Lithium Price vs Grade Rock Value Matrix

If Toyota's solid state Li ion battery is real there world will need 150 Jadars by 2035

China's embrace of Electric Vehicles is Irreversible

Silver Range and Dios have similar second order prospect generation strategies

Jim (0:08:29): Is the James Bay Lithium Index waking up yet?

The James Bay Lithium Index is still weakening as the price of lithium carbonate approaches $10/lb on the downside. As of September 26, 2023 it was down 14.1% from the August 1, 2023 initialization date. The optics of a declining metal price never makes the market happy, but as I argued in the MIF overview portion of this KW Episode the long term price range will be $5-$10/lb within which pegmatite deposits grading 1% Li2O or better still have rock values that allow profitable underground mining and where open pit mining is possible that brings tears of envy to gold explorer. There is also the index downward bias created by my decision to include all companies which have land in the James Bay region on the premise that the novelty of the pegmatite hunt makes it possible for even the dumbest, most horrible lifestyle juniors to get lucky so long as they mobilize a prospecting program run by a competent exploration team. JBLI is now colliding with the reality that the loss of three months of critical boots on the ground prospecting will limit the number of juniors that have drill ready targets for Q1 of 2024. This causes the penny dreadful members who were added to the index with the same value weighting as all the rest to register big percentage drops. But there is some discovery joy trickling through despite the curtailed season that will focus new money coming into the James Bay Great Canadian Area Play. The value of the JBLI is that it creates a monitoring framework and will reveal a rising tide when that begins to happen, possibly late 2023 but definitely in 2024.

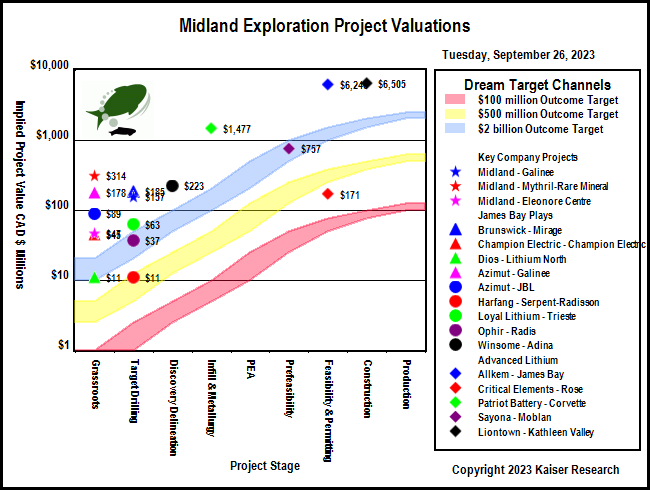

The most important development during the past week was news from Midland Exploration Ltd that Rio Tinto has discovered spodumene bearing pegmatite outcrop on the Galinee project optioned 70% from Midland. In KW Episode September 15, 2023 I made the case that Midland is so far the best way to bet on Rio Tinto's exploration efforts in the James Bay region and is also the best way for nervous speculators to have exposure to James Bay lithium discovery upside without the downside risk. This is due to the fact that Midland is a Quebec focused prospect-generator-farmout junior with numerous projects, some farmed out to majors, in other parts of Quebec such as the Abitibi and northern Quebec. In addition not all its James Bay projects have been farmed out to Brunswick or Rio Tinto and the junior is now reviewing them for their LCT-type pegmatite potential. Gino Roger may have let a good number of Midland's James Bay boats slip out to sea, but he is taking a hard look at those still moored at the dock. Needless to say, because Midland's net 30% stake in Galinee already implies a valuation of about $161 million, the market did not reward the stock with upside. That will happen when drilling reveals the scale and geometry of the Galinee discovery, and it is noteworthy that operator Rio Tinto is planning a 2023 fall drilling program.

Midland only revealed that outcropping spodumene bearing pegmatite had been identified along several hundred metres, with no indication of the lateral distribution of these outcrops. In contrast consider that Brunswick has now identified pegmatite outcrops within a corridor of 2,700 m by 850 m, and a solo outcrop 6 km to the northeast from the southwestern end of the outcrop corridor where a 3 km boulder train begins. Brunswick started a 5,000 m drill program on September 7 and will be in a position to tell us by mid October to what extent the Mirage outcrops hang together beneath the surface.

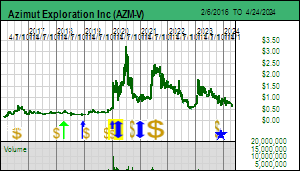

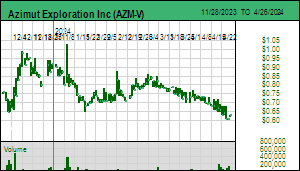

So, given the so far relatively puny outcrop area at Galinee, why is Rio Tinto already planning a drill program? The Galinee area is emerging as a focal district within James Bay created by the Adina discovery in late 2022 by Winsome Resources Ltd. The Adina LCT-type pegmatites are associated with the contact zone between the easterly trending amphibolite Trieste Formation and felsic intrusives to the north. Winsome has now traced LCT-type pegmatite along a 3.1 km trend with the best drill results at the Jamar showing whose pegmatite body dips to the southeast onto the Galinee 50:50 JV between Azimut Exploration Inc and SOQUEM.

Azimut recently reported that its boots on the ground had found spodumene bearing boulders on its side of the boundary from Winsome's Jamar Zone, but so far failed to find any outcrop on the rest of the property. The ice direction indicates that these boulders came from the Jamar Zone and Azimut's hope is that there is a meaningful downdip extension onto its property and possibly blind parallel bodies as it has hypothesized in a diagram. However, the combination of the lake bottom sediment lithium map and geology on Azimut's Galinee project suggests that if anything outcropping is present it will be in the southern part of the property where a narrower amphibolite trend is present.

The forest fire access closure has been particularly harmful for Winsome which planned a major discovery delineation drilling program this summer to stitch together the pegmatite zones at Adina, but this program was only recently able to get underway. Winsome's Adina project is carrying an implied value of AUD $223 million, another example of an emerging discovery in the James Bay region that could deliver 5-10 fold gains from current levels if drilling can deliver a deposit resembling PMET's CV5. Rio Tinto is being aggressive about Midland's Galinee because it sits between Winsome's Adina and the Trieste project of Loyal Lithium Inc which has discovered LCT-type pegmatite on the southern flank of the amphibolite trend. Loyal has an option to acquire most of its Trieste project from Osisko Development Corp whose Sean Roosen is apparently planning to spin out the remaining James Bay holdings into a new vehicle. Comet Lithium Corp's Liberty property to the north has a small segment of this trend between Adina and Galinee, but this junior has so far demonstrated itself as management challeneged.

I've patched together several maps to try and make it easier to understand who has what land where; the various companies tend not to outline and identify their neighbors unless they have a discovery worth pointing out, so we are stuck with a fragmented perspective of relative land positions. The reason I think Rio Tinto is being aggressive about Galinee is that it sees the potential to consolidate this district which doesn't really have a name so I will call it the Trieste Trend.

Not every junior is reporting spodumene-bearing pegmatite outcrop news. Champion Electric Metals Inc has assembled a large 53,000 ha land package it calls Champion Electric that parallels to the north the amphibolite trend of PMET's Corvette trend. This belt of rocks has seen less historical exploration from the likes of Virginia so will lack archival references to pegmatites observed while exploring for precious and base metal deposits. But because there is no genetic relationship between LCT-type pegmatite emplacement and the formation of precious and base metal deposits, Champion's land position has the potential to deliver first order surprises when prospected on a detailed grid.

During 2022 Champion completed a LIDAR survey over those portions mapped as "mafic volcanic rocks" (hard to tell what Champion means because its map assigns the same color to the amphibolite rocks of the Corvette Trend to the south while the dark green color it calls amphibolite are patches to the north of its land package). LIDAR surveys reveal topographical variation which is useful for homing in on ridges that may represent pegmatites whose harder rock than the country rock causes them to resist weathering and grinding away by ice sheets to a higher degree than the surrounding rock. (Geologists are now scratching their heads why the CV5 deposit of PMET recessively tracks a long lake.) Andre Gaumond during the Virginia exploration era famously forbade his field crews from sampling light colored bush and mosquito free ridges because those were worthless pegmatites with zero precious and base metal potential.

Champion announced on August 3 that it had sent boots onto the ground to prospect the areas of the 2022 LIDAR survey. The next update came on September 19 when CEO John Buick revealed that Champion had completed a LIDAR survey on the rest of the property and would soon be sending prospecting crews into the field. Given that a 7 week prospecting window had just passed, it was shocking not to hear an update about what was or wasn't found. Given the company spent $324,000 on investor relations during H1 of 2023, you would think that if there was anything positive to report, Champion would have done so. The glum conclusion is that the first boots on the ground pass turned up nothing interesting and the race is now on to prospect the rest of the property before snow blankets the region. Champion should still have about $5 million working capital left, so if it can generate targets worth drilling in Q1 of 2024 it will not have to go to the market. The main obstacle to upside is that Champion has an overhang of 54,536,266 warrants exercisable at $0.10-$0.25 which boost its fully diluted to 323 million shares and which implies a lofty valuation of $45 million for a project which so far has no evidence of LCT-type pegmatites.

James Bay Lithium Index Daily Performance Last 120 Days

Lithium Rock Value Matrix and LC Price Chart

Various Maps of Trieste Trend where Winsome's Adina Discovery is located

Winsome's Adina Discovery and Azimut's Geochem Map

Azimut's hopes for its Galinee Project

Lidar & geology Maps for Champion's Champion Electric Project

Vhampeion Electric Financial Snapshots

Midland IPV Chart

Disclosure: JK owns shares of Brunswick and Dios; Crtical Elements is a Fair Spec Value rated Favorite; Dios, Midland and Silver Range are Bottom-Fish Spec Value rated; Champion & Targa are not rated