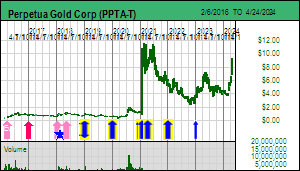

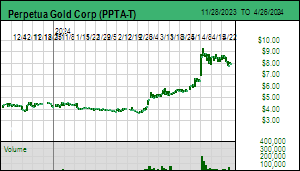

| The USFS has finally released a Supplemental Draft Environmental Impact Statement that reflects the modifications Perpetua Gold Corp made in response to the comments generated when the USFS released the original Draft EIS in August 2020. In Q1 of 2021 PPTA's largest shareholder John Paulson fired the Canadian team led by Stephen Quin and replaced them with Idahoes and his pals. Two years later we are where we were two years ago: waiting for a 75 day comment period to end on January 10, 2023 that finally results in a Final EIS in mid 2023 that kicks off application for dozens of other permits needed to begin mine construction. But it no longer matters.

When the Stibnite feasibility study was filed in late 2020 it used $1,600 gold as a base case price. Stibnite cleared the IRR hurdle and made the hurdle of after-tax NPV matching CapEx provided you used a 5% discount rate. But during the past year we have seen two bad things unfold: inflation has reached 3 decade highs and gold has retreated from the $2,000 level almost back to the base case level of $1,600. Perpetua was made a Good Spec Value rated KRO Favorite based on the feasibility study and the expectation that $1,600 gold was likely the low end of the gold price range going forward. I still believe that.

To understand the upside of Stibnite I created a DCF model that closely follows all the assumptions in the feasibility study. This allows me to see the impact on after tax NPV at both 5% and 10% discount rates as well as IRR at different gold prices. It also allows me to convert those absolute figures into per share figures in CAD using the latest exchange rate and fully diluted. The first two charts below illustrate this in NPV/share and aboslute NPV terms. The NPVsh chart shows that PPTA has a target range of $16-$26 at $1,600 gold, soaring to $31-$46 at $2,000 gold.

But gold has sunk back close to $1,600 as the Federal Reserve cranks up interest rate to fight inflation. So I did what I did the other week with FPX Nickel and its Decar PEA: I escalated all costs by 20% which is not unreasonable to do for a mining project whose costs were figured out for the 2020 FS. The result in the second set of charts is horrific. The NPV at $1,600 gold collapses to USD $377 million at 10% and $715 million at 5%, well below the new $1.6 billion CapEx. The per share target of CAD $8-$15 looks good for a current stock price below $3, but it is fictitious because the NPV is far below the CapEx, and with only a 15 year mine life this is not going to be built, which is different in a scenario like Decar with a 40 year mine life producing a metal the world can never do without (keep in mind that BitCoin is the new gold as pumped by the libertarian crowd which will continue to rely on stainless steel until Ray Kurzweil shows them how to migrate into quantum space as disembodied Q like beings). At $2,000 gold the hurdle gets cleared with a $1 billion NPV at 10% and $1.6 billion at 5%, though again only with the 5% discount rate just as was the case with the original FS assumption. The price target range would be $22-$34.

If the Stibnite permit is ever granted Perpetua will have to redo its feasibility study with current numbers. And if gold is not $2,000 plus by the end of next year, Stibnite will be just another gold optionality play. The juiciest rony would be if the government is forced to step in to bankroll CapEx so that Stibnite is not just a reclamation project funded by a gold mine, but antimony supply security funded by a gold mine. But I'm not sure what that triumph will be worth on a per share basis. To stay enthusiastic about Perpetua you have to be optimistic that the perpertual permitting cycle is coming to an end, that my cost inflation assumptions are excessive, and that gold will charge through $2,000 while inflation succumbs to a high interest rate induced recession. |