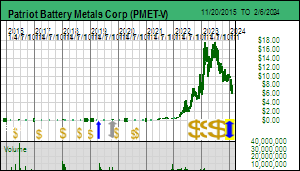

Patriot Battery Metals was halted on Tuesday to allow completion of a $50 million charity flow-through financing and did not resume until Thursday. The financing was done in the form of 2,215,000 shares at $22.57 and gives PMET working capital in the $60-$70 million range depending on how much has been spent at Corvette since the start of the year. The entire financing was actually bought by Australian entities. After Peartree stripped the flow-through benefits from the stock all of the shares were sold through Australian brokerage firms or the subsidiaries of Canadian firms to Australian investors in the form of 22,150,000 shares so called Chess depositary interests (CDI) at AUD $1.20. Just as British and Australian listed companies trade on North American exchanges on a 10:1 rollback basis (ie Piedmont Lithium), stocks with a primary listing on North American exchanges trade on a 10:1 split basis on the ASX. So whenever you see the PMT price on the ASX, multiply by 10 and adjust by the AUD-CAD exchange rate to calculate what the TSXV equivalent price will be. The stock is down from its $14-$15 range during PDAC week in part due to overall market weakness as the banking crisis began to emerge, but also to reflect the discount needed to place the stock in Australia.

The big question is whether or not PMET will bounce back after loading its treasury with an extra $50 million. The timing of the halt during a week when conservative investors watched the banking sector lose nearly a half trillion dollars in equity value, stocks that are supposed to be safe and boring, has injected a new dynamic into the PMET market structure. The stock will likely come under pressure from the exercise of 4,038,409 warrants at $0.25 that expire June 30, 2023, and 26,850,727 warrants at $0.75 that expire mostly at the end of the year. Normally a warrant overhang is a problem for a junior when the exercise price is above the market price because the holders will short against the warrants every time the stock rallies through the exercise price. An then cover the stock in the market when the stock price sags, sucking up incoming new risk capital. PMET has a different problem in the $0.75 warrants represent a paper gain of $286 million at, say, $11.41 per share where it was trading mid day Friday. If the holders wanted to collect their profit by exercising and selling their stock, the market would need to eat about $300 million worth of stock. That is not chump change.

The warrant holders may until last week have been happy to wait for a potential buyout later this year, but during the two days while the stock was halted to complete the financing and the general market was shuddering from the bank run crisis, they probably experienced a considerable amount of fear that their paper profits might evaporate. The premise behind PMET's recent $2 billion valuation is the idea that the world is determined to go through with the energy transition in order to ensure an inhabitable future for the children and grandchildren of the Boomers. One plank in the energy transition strategy involves electric vehicle replacement of internal combustion engine vehicles. The IEA projects that the for the 2030 EV goals to be achieved the world will need to expand its lithium supply by 600%. But none of that will happen if the world descends into an apocalyptic End Times mentality. So what happens on the global stage matters to shareholders of PMET.

Then there is also the recent financing reality in the resource sector where major financings are done at major discounts to the market. Nobody knew what the term structure would be for a financing most knew was coming, so existing shareholders likely weren't happy to see in effect a bought deal at AUD $1.20 or $12 which, because $1.00 AUD is worth about $0.91 CAD, implied a $10.92 CAD price for PMET. During the past year we have seen a spate of bought deals at 20% or more discounts to the market price, which resulted in an instant haircut for existing shareholders that was not rewarded with a rebound after the financing was completed. So although PMET post-financing has $60-$70 million working capital to finish delineating the CV5 lithium deposit and proceed with an economic study, spooked warrant holders will likely start exercising the warrants and banking the profit.

The good news about the Australian purchase is that the stock went into strong hands which apparently included Mineral Resources and Pilbara Minerals, two $14-$16 billion market cap ASX listed lithium producers with apparent ambitions to dominate a future $100-$200 billion market while established majors like Rio Tinto, BHP, Vale and Anglo American pick their noses. Earlier this year there were unconfirmed rumors that Mineral Resources was accumulating PMET in the open market, which raised hopes that it might launch a hostile bid for PMET, perhaps ahead of a maiden resource estimate expected in late Q2. Since nobody has disclosed passing the 9.9% insider threshold, all this is largely rumor, though the paperwork for the Australian purchase would make clear who bought what in the current financing. If it is true that Mineral Resources and Pilbara bought toeholds, this bodes well for the stability of the PMET market as it digests stock from the warrant exericse.

Changing the subject, while updating the PMET financials for my KRO database I noticed a peculiar entry in the balance sheet of a kind I had noticed last year in the case of another junior whose CEO suggested I talk to the CFO for an explanation. The Dec 31, 2022 balance sheet shows current assets of $20,990,581 and current liabilities of $10,537,259. A standard measure of a junior's financial health is working capital, which is current assets minus current liabilities. On this metric PMET had only $10.6 million working capital at the end of 2022. But one of the current liabilities items is called "flow-through premium liability" and it is $8,553,172. This is an accounting fiction which new regulations now require companies to include in current liabilities. The amount represents what the company would be liable for to Canada Revenue Agency (ie the Canadian equivalent of the IRS) if an audit determines that the flow-thru funds were not spent properly. There have been cases in the past were flakey life-style juniors raised flow-through money and failed to spend it on qualifying exploration, which resulted in the flow-thru benefits of the placees being reversed by CRA. This resulted in a huge mess for the junior and the investors, especially for the investors if the junior has effectively blown all its capital and the pump and dumpers behind the junior have walked away.

While the intent is to alert investors that the company has an obligation to spend flow-thru money properly, it does cause the working capital number to understate the financial health of a company that has flow-thru funds in the bank. When it is confirmed that the money has been spent properly, this line item vanishes via "amortization" recorded as an inflow rather than outflow. Of course the cash by then has also vanished because it needs to be spent by the end of the year subsequent to the one in which it was raised. In the case of PMET's Dec 31 financials the FT premium liability is linked to the $20 million charity FT financing PMET did in September at $13.27 when the stock was trading at half the price. If you trust the junior as being run by competent management trying to create real value through exploration, this line item is not necessary, and potentially misleading. We will have to watch for this distortion of a junior's financial health, just as we have to do with an expense line item called stock option compensation which is also an accounting fiction that must be stripped out to reveal the true burn rate of a junior. It is unfortunate that the more regulators try to achieve transparency, the more they achieve obfuscation. |