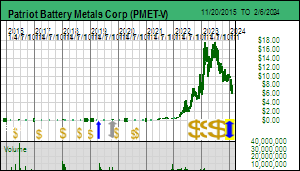

On July 6, 2023 an outfit called Night Market Research that specializes in identifying short selling opportunities published a length report title: Patriot Battery Metals: Aggressive Vancouver Promotion with Multiple MRE Delays and Fake Buyout Rumors Running Headfirst into Wall of Risk (and Warrants). This caused the stock price to decline on July 7 and the ASX requested PMET to provide a response which the company did on Monday July 10 when it also published the final assays for the winter drill program. The ASX will allow a stock to be halted for a number of days while material news is disseminated, but the remaining assays are not material because they are all within the CV5 pegmatite body and do not really change the market's perception of the extent and grade of CV5 for which a resource estimate is anticipated in a "few weeks". The TSXV allowed the stock to trade on Monday while the ASX allowed trading to resume on July 11, enabling the Canadian market for the first time in a long time to set the tone for PMET. The stock recovered into the $15-$16 range as the market shrugged off the Night Market Research report's allegations which fall into two categories.

The first is that in fundamental terms the Corvette project is over-valued and is destined to correct downwards as the project proceeds into the feasibility demonstration stages of the 9 stage exploration-development cycle that starts with grassroots exploration and finishes with commercial production. In terms of my rational speculation model this is true, for the stock is in S-curve territory, the initial valuation surge of what is commonly called the Lassonde Curve, namely the discovery delineation stage where the sky is the limit as to how big the discovery can become until a maiden resource is delivered, after which the market sees the limits and focuses on cost discovery which forms the basis for a discounted cash flow model valuation expressed as a net present value (NPV) accompanied by an internal rate of return (IRR). (Nicholas LePan of the Visual Capitalist has done an excellent job Visualizing the Life Cycle of a Mineral Discovery.) I have observed that the peak valuation frequently matches that of what the project ends up being worth in DCF valuation model terms years later when the project is ready to go into production. The valley in between while the company engages in cost discovery after deposit discovery has been completed is called the "value trough" from the perspective of those who don't already own the stock. Whatever back of the napkin valuations are done during the transition usually shrink as flow-sheets and permitting requirements are sorted out. An additional source of outcome value shrinkage can be the future metal prices, though sometimes they end up higher, the perennial hope for gold projects.

An example of the Lassonde Curve in action is Dia Met Minerals whose Ekati diamond discovery reached a peak $2 billion valuation in 1993, two years after the initial discovery announcement. Three years after Ekati went into production in 1998 BHP acquired Dia Met and its 29% interest for cash at an implied value of $2.3 billion on a 100% basis. Why did Ekati hit a $2 billion value during the discovery stage before we had any numbers for tonnage, grade and carat value? Because this was a brand new diamondiferous kimberlite field outside of Africa where it was legitimate to dream that world class monsters like Jwaneng or Orapa in Botswana might emerge within the Slave Craton of Canada. This did not happen, but the collection of pipes selected for production did end up having a world class value.

Completely missing from the Night Market Research short attack is any discussion of the "district scale" implications of the Corvette property which covers 45 km of the La Grande Shear Structure of which the CV5 resource will represent only a portion. NMR is making the assumption that the CV5 maiden resource estimate will be the culmination of what the Corvette property has to offer, something which the Australian and Canadian brokerage analysts think will be comparable to what Liontown accomplished with Kathleen Valley, which earlier this year attracted a conditional bid from Albemarle that priced the project at about AUD $5 billion (see KW Episode Mar 29, 2023 for background on Liontown's 8 year journey from grassroots lithium exploration in 2015 to the current status of mine construction). Liontown rejected the conditional bid but the stock has since then consistently traded above the proposed Albemarle buyout price. NMR correctly points out that Liontown has pushed Kathleen Valley through 5 years of feasibility demonstration to get the current valuation, as a result of which it has 2.2 billion shares issued, but what it ignores is that Kathleen Valley is now an optimized mining scenario for that project. This project is as good as it is going to get.

PMET's situation at this stage is equivalent to owning the entire 40 km long Carlin Trend in Nevada, and CV5 is the equivalent of finding Goldstrike as the first Carlin-type gold discovery within this trend. And we know a lot more such gold deposits were subsequently found. How many more CV5 deposits might be found within the Corvette property that could be developed as standalone open-pit mines? Perhaps 3-5 more, perhaps none. The point is we don't know yet because the first order lithium discovery boom in the James Bay region is only 2 years old; all the other advanced lithium deposits (Galaxy-Cyr, Wabouchi, Moblan, Rose) were discovered decades ago and are valuable today only because of the climate change crisis and the electric vehicle as a partial solution to achieving the goal of net zero emissions by 2050. How many Kathleen Valley deposits are left for Liontown to find on its property? If there were any more would they not have been found during the past 5 years while the main pegmatite plodded through the feasibility demonstration stages? If the big producers knew that CV5 is all that will ever be found and developed within the Corvette property, there is no way they would consider paying $2-$3 billion to own PMET.

The IEA has projected that the world will need 600% more lithium supply if 2030 EV rollout goals are to be met. That is with existing lithium ion battery technology. Rio Tinto has made even more aggressive predictions. If the EV sales goals are met, the lithium market will be worth $100-$200 billion in 2030-2040 assuming current battery technology remains unchanged. During the past few weeks Toyota, which was in the vanguard with its Prius hybrid model but has been a laggard with full plug-in electric vehicles while it focused on leapfrogging lithium ion battery technology through hydrogen fuel cell technology, made the stunning announcement that it had solved the processing cost problem for a solid state electrolyte which allows lithium metal to substitute for graphite in the anode. Toyota predicts that by 2027 it will be selling a high end model that has a range of 1,200 km and a charge time of 10 minutes. Neither the IEA nor Rio Tinto forecasts allow for this greater usage of lithium in future electric vehicles.

Since you are probably not going to achieve the required lithium supply if the price of lithium crbonate tanks back below $5/lb, what we are facing is a massive scramble to find and harvest the low hanging LCT-pegmatite fruit that is suddenly in the money, and which faces a 5-10 times demand expansion. Australia has already been through this low hanging fruit cycle which I call Lithium Mania 1.0; the second phase targeting stable regions such as Brazil and Canada is Lithium Mania 2.0 for which PMET is the poster child. Rio Tinto has said the world needs 60 Jadar scale lithium mines; the James Bay region has the capacity to deliver a couple dozen Jadar equivalent mines.

The timing of this report just ahead of PMET's plan to publish a maiden resource estimate appears designed to force a stock price retreat if the resource proves lower than the lofty conceptual estimates published by various Australian and Canadian brokerage firms. I have speculated the resource will come out within the range of 50-100 million tonnes grading between 1%-2% Li2O, but Night Market Research has presented a range of estimates from 90-160 million tonnes with grades ranging 1.12%-1.35% Li2O. It offers its own prediction of 73 million tonnes of 1.28%, whose grade is near the upper range of the analyst predictions, though its tonnage is lower than the 90 million tonnes at 1.35% Li2O it attributes to National Bank. NMR claims that PMET CEO Blair Way has been encouraging the market to think in terms of at least 100 million tonnes, which has supposedly set up the market for disappointment. NMR is predicting that the CV5 resource will be similar to the 68.5 million tonnes of 1.34% Li2O proven and probable reserve Liontown is putting into production.

The reality is that we do not know what cutoff grade PMET plans to use. If it uses a higher grade cutoff the tonnage will be lower but the grade higher. Initial development could focus on the higher grade Nova zone within the CV5 deposit. NMR has in fact created a straw man to knock down the market if we see a resource closer to its number. The reason it thinks the analysts are over-estimating the resource is that PMET stopped publishing sections along with its holes last year. However, PMET has an excel spreadsheet with all the drill hole data which includes the azimuth direction and dip angle for each hole, plus all mineralized intervals greater than 2 metres. Combine that with the drill plan and an analyst can construct a 3D model, especially if they have Leapfrog software at their disposal. What the company has not published is the assay interval breakdown which would allow analysts more granularity in defining the geometry of their choice using their own cutoff grades. NMR argues that the implied project value of about CAD $2 billion on a fully diluted basis is excessive if the estimate is more in line with its own prediction, but it does not provide a quantitative basis for this view which requires one to visualize an operating mine and calculate a net present value from the resulting cash flow.

Once we have a 43-101 resource estimate the market will be in a position to create an outcome visualization in the form of a DCF model which depletes the resource within 15 years. For example, NMR's resource would be mined at about 13,000 tpd to be depleted within 15 years. The economic value of that scenario will depend on CapEx and OpEx as well as the long term price of lithium carbonate. Suppose the DCF model does generate a future target outcome of CAD $5 billion. Under my rational speculation model fair speculative value should be 2.5%-5.0% for a project that has delivered a resource estimate but not yet done cost discovery in the form of a PEA. So we are talking a fair value range of $2.50-$5.00, well below the current valuation. However, if the project moves to PFS stage the FSV should be 50%-75% of the target outcome, which would be $25-$38 per share. What NMR is arguing is that the current valuation is an S-Curve peak which will follow the Lassonde Curve downwards once the project enters feasibility demonstration stage and follows into the value trough.

This can be expected to happen if PMET stays in charge of moving the project through the feasibility demonstration stages, but a likelier outcome is that a major producer will buy out PMET and do it properly. The most obvious candidate is Rio Tinto which has been optioning nearby properties from Azimut and Midland in what amounts to an effort to tie up as much of a new district as possible. NMR seems to be trying to talk down the price of PMET in order to help a third party get a better deal. But this may not work because we are talking about an emerging world class lithium district serving a market that by 2030 will be worth $100-$200 billion, more if Rio Tinto's own predictions are to be believed, and even bigger if Toyota is not bullshitting us. CV5 represents only a fraction of an LCT-pegmatite mineralized trend. There may be multiple CV5 deposits present, each of which could be developed as a standalone mine. It is conceivable that Rio Tinto, Albemarle or Pilbara Minerals would be willing to pay an S-curve valuation based on the strategic district value. Far from making a case that PMET's stock price will be a lot lower once the maiden resource estimate is published, Nigh Market Research has in fact boosted the credibility of PMET's discovery.

NMR's other angle of attack is to slag the history of Patriot Battery Metals, such as the sordid 18 month marketing deal PMET did at USD $500,000 per 6 month term with some obscure entity based in an ordinary Vancouver residential neighborhood. This deal was made just before the company announced an RTO of a private rare earth company that was canceled a couple months later when Blair Way became CEO and steered PMET back to the Corvette lithium project. I abhor these awful and expensive marketing deals Canadian juniors do to pump their stock, and sometimes I wonder if these deals are just ways for hidden insiders to steal their private placement money back into their pockets. In the ASX requested response to the short attack Blair Way stated the marketing deal was terminated after 6 months when PMET had a market capitalization of only $20 million, a hundredth of what it is today. Regardless how sleazy the marketing deals a junior may have done, none of that matters if the company has delivered a fundamental success. One thing I keep repeating is that the nature of Lithium Mania 2.0 is such that even juniors with horrible management practices can achieve a huge fundamental success, provided they spend money on competent exploration. Whatever questionable marketing deals PMET management has done, it did let Darren Smith's competent exploration team do their stuff.

NMR also tries to scare PMET shareholders by pointing out that Ken Brinsden, who played a key role in the success of Pilbara Minerals during Lithium Mania 1.0, was previously involved with an iron company that failed. Who cares? That is like arguing that Robert Friedland's Mongolian Turquoise Hills copper-gold discovery in Ivanhoe One, after he delivered a $4 billion buyout for the Voisey's Bay nickel-copper discovery by Diamond Fields, is doomed to fail because Friedland's earlier company, Galactic, crashed and burned. Not every Friedland effort is a winner (Kaizen and Cordoba come to mind), but Ivanhoe Two's Kamoa-Kakula grassroots copper discovery in the DRC is a monumental fundamental success. This complaint is the most feeble one NMR makes.

NMR does make a valid point when it frets that PMET has a large overhang of unexercised warrants that are very much in the money. Many of the holders will already have dumped the long positions from those private placements done in 2021 and are sitting on huge paper profits. Frankly I do not understand why so many cheap warrants remain unexercised. I pointed out this problem in KW Episode March 17, 2023 and it is still a problem. NMR's main strategy is to prime the market for a sell-off after the maiden resource estimate is released by predicting it will be lower than analysts are projecting. During the past year there have been several rumors about possible takeover bids for PMET, none of which are credible because no producer is going to pay a "strategic" premium without at least a resource estimate in view to explain its reasoning. The market risk is that even if the resource estimate come in within the analyst predicted range, there may not be a quick follow through. The attitude of the warrant holders is that they will exercise when they have to, such as in the event of a takeover bid. But if that does not promptly happen because Pilbara, Mineral Resources, Albemarle and Rio Tinto are all disciplined and reluctant to start a bidding war, the stock could stall. At Friday's $15.70 closing price the 24,330,190 warrants that expire between December 21, 2023 to March 21, 2025 have an implicit profit of $365 million, which to collect would require $382 million worth of buying at $15.70. Psychologically this type of warrant based paper profit is more unstable than if the holders exercised them a long time ago without selling any. NMR is in effect reminding all the warrant holders of their prisoner's dilemma situation and setting up a selling cascade after the resource estimate is released. The potential bidders for PMET are right now chortling with glee at the predicament of the warrant holders.

NMR also worries about the permitting regime in Quebec which is fairly detailed and could benefit from streamlining. It also mentions a lake sturgeon that supposedly lives in the lake which would be disrupted by open-pit mining CV5. The Canadian and Quebec governments are going to have to do a cost-benefit analysis. Billions are being shoveled at downstream fabricators serving the EV market to encourage them to set up their operations in Canada. One reason to do so is they can all see the potential lithium supply coming from Canadian pegmatites. But if the government is going to take a purist stance that there must never be a local loser, at the expense of net zero emission goals, there is a surprise coming. This year is shaping up to deliver a new round of extreme weather records, as Quebec's forest fire debacle has already shown. It is time to become pragmatic about all aspects of the various climate change mitigation solutions, in particular the discovery and mining of critical minerals.

NMR also invokes Goldman Sachs which has been predicting that Chinese and Latin American lithium supply will meet all demand growth, and mentions a GS prediction of $34,000/tonne for lithium carbonate in 2024. That is equivalent to $15.42/lb. If lithium carbonate is at that level rather than $10/lb as I assume, what is there to worry about? In fact $10/lb will be hugely profitable for pegmatites grading 1% Li2O or better. Demand will probably grew faster than supply, which NMR dwells on but treats it as a negative for PMET along the lines of "your project will take a lot longer to permit than anybody else's project, so by the time you are producing the market will be in oversupply and the lithium carbonate price will be a lot lower". Understanding the discovery exploration game is not something Goldman Sachs has much experience with because it is such a small space; its revenue generating strategy will involve helping downstream raw material consumers secure their supply. So of course GS is trying to talk down the prices of the lithium developers. And Night Market Research appears to have volunteered itself as foot soldier in this process. But in fact it has helped fulfill the requirement that no major new discovery is real until it has attracted a major short attack. |