Hello Guest User, You are visiting this website from a computer with an IP address of 108.162.216.153 with the name of '?' since Sat Apr 20, 2024 at 7:56:38 AM PT for approx. 0 minutes now.

Kaiser Research Online is an information portal featuring all resource companies listed on the ASX, TSX, TSXV and CSE. New individual registrations will be temporarily suspended January 1, 2020 while we build a new web site though individuals already registered at KRO can subscribe for the USD $450 annual individual KRO membership during the transition. The USD $1,000 annual multi-user Corporate Membership will continue to be available in 2020 to new members. KRO will continue to operate in its current form with the difference that some Trackers will become unrestricted to non-members after a short period. Use your Email to retrieve your login credentials. See Membership Details for an overview of KRO.

The KRO Summary lists all Trackers and Blogs published during the designated weekly or monthly period so that so readers can easily catch up on what they may have missed. We no longer notify KRO members by email about new material except in special circumstances. When a Tracker is posted at KRO we notify members through the KaiserResearchOnline Slack Workspace. If you are an active KRO member and not registered on Slack, please let us know and we will send the invite. We will email the link to the KRO Summary to all KRO members when it is published. We will also Tweet the link so that Twitter followers can catch up at their leisure. The title links to the Tracker or Blog, the charts in the Discovery Watch Blog link to the YuoTube audio segment for that company, and the Tracker charts link to the free Corporate Profile. On occasion we may include commentary on the state of the market. Blog content is unrestricted but Trackers are always restricted to KRO members unless one has been tagged to become unrestricted. Check the General Release Schedule to see which Trackers are already unrestricted or scheduled for general viewing.

New Decade off to a good start for Resource Juniors, but will it last?

The new decade continued the resource junior uptrend that began in mid-December as investors began to embrace the idea that the gold uptrend which began in May 2019 has staying power. The disconnect between the gold uptrend and the malaise among resource juniors was very discouraging but there were signs that with the cannabis bubble deflating the 8 year resource junior bear market was turning around. The daily in and outflow of gold into the SPDR GLD ETF shows that there was a strong period of investor accumulation from May until late September, since which there have been more outflow than inflow days. So far the GLD ETF has acquired 320,235 ounces since the start of 2020, but most of that was due to a 621,348 ounce jump on January 17. Gold received a short term price boost over $1,600 in the wake of the surprise American drone assassination of the Iranian general Qassem Suleimani in early January as the world braced for an Iranian retaliation that would disrupt oil production in the Middle East. The bombing of two American bases in Iraq caused no casualties though reports have since emerged that 50 servicemen suffered traumatic brain injury. The killing of Suleimani initially united the Iranian people behind the Shiite theocracy that has controlled Iran since 1979, but the same night of the official retaliation Iranian air defence managed to shoot down by accident a passenger plane leaving a Tehran airport, killing all onboard who except for the crew were all Iranians or Iranian-Canadians. By the time the theocrats finally admitted it was their fault the public's anger over the oppressive regime had returned and the theocrats lost their mandate to stir up the Middle East. This defused another problem created by Trump's failure to warn America's European allies about the attack, about whose justification with regard to an "imminent threat" we no longer hear anything, and his subsequent cajoling that the Europeans need to get ready to clean up any resulting mess in the Middle East whose roots lie in the unilateral US withdrawal from the 2015 Iran nuclear treaty. The Europeans weren't going to rally behind the United States, which would have given fuel to Trump's agenda to escalate a trade war with Europe now that the China trade war had achieved a truce. Fortunately Iran decided to keep its head down and China stepped into the spotlight with its bungled handling of the "novel coronavirus" about which we started to hear peeps in December.

In the third week of January we learned that nCoV was very transmissible among humans, that it was a version of SARS which terrorized the world with pandemic fear in 2003, that the incubation period was 7-14 days during which there are no symptoms but the infected person is contagious, that its mortality rate was much lower than SARS but much higher than ordinary influenza for which most people get annual flu shots, and that mortality favored older people with health issues. On top of that, China failed to recognize these features and take timely containment measures before the Lunar New Year holiday began, that period when the Chinese travel from their urban workplaces on the coastal plain to be with family in the hinterland. This massive mixing of people is a perfect storm for contagion. Although China has now imposed lockdowns on tens of million people, the horse has left the barn. As of February 3 China had reported 20,438 confirmed cases, and 160 cases have been confirmed in 2 dozen other countries, including 11 in the United States. SARS in contrast recorded 5,327 cases and 349 deaths over a much longer period before it subsided. Given the lag between infection and symptoms, we can expect the statistics to keep climbing throughout February, not just in China, but also in the rest of the world. The reason is simple. For most people the nCoV flu just causes the usual flu symptoms and unless that person returned from China during the past month or had knowing contact with somebody who did, they will unwittingly spread it to others. Fortunately once the Chinese authorities woke up to the threat and worked out the genetic code for nCoV they immediately shared it with the rest of the world whose experts are now working on fast diagnostic tests, a vaccine and treatments. Unfortunately rapid contagion enables a virus to undergo mutation, invoking metaphors like "whack a mole" and "catch me if you can". The reluctance of the World Health Organization to declare a world health emergency right away reflects the reality that fear over an epidemic evolving into a pandemic can have far-reaching economic and social repercussions.

We are already witnessing xenophobia toward the Chinese in the Asian nations bordering China. Within China there is growing social rage over Xi Jinping's authoritarianism that censors all criticism of state policies with the help of hyper-surveillance technology. China cannot blame nCoV on external causes. The transmissibility of nCoV was not recognized during the first two weeks of January because Beijing wanted a "zero infection" status on pain of hospital heads being fired. So when health workers treating infected patients started getting sick, self-censorship kicked in, preventing recognition of the transmissibility and the associated incubation. Now all of China is paying a huge price as entire regions grind to an economic halt as movement quarantines get imposed. At 16% China is the world's second largest economy compared to 4% in 2003 when SARS broke out. Manufacturing around the world relies on a global supply chain to which China is a major contributor. US Commerce Secretary Wilbur Ross recently opined that China's coronavirus problem will be good for America because it will force manufacturers to reshore all aspects of the supply chain. That cannot happen overnight because it is physically impossible and because manufacturers will simply wait for the "pandemic" to go away. China's temporary inability to keep its economy humming as it struggles to contain the NCoV epidemic will unleash domestic strife that in turn may threaten the Communist Party's control which in turn will spawn repressive actions in a vicious spiral that could make China a very dysfunctional economy. That will ripple through the rest of the global economy, especially countries like Germany which depend on exports to China. A global economic downturn will further fuel the populist rage of people "left behind" by the modern economy which manifests itself in exclusionary nationalism. Trump's push for deglobalization through trade war may be undergoing a hijacking by processes the United States is unable to control, something a May 31, 2017 tweet may have prophesied: "Despite the constant negative press covfefe".

After a sharp drop on January 31 the big equity markets have rebounded, which seems counter-intuitive in that commodity prices are sliding, in particular oil but also base metals. The spread between short and long term treasury yields which went negative last year, historically a recession signal, widened in Q4 of 2019, suggesting that an economic downturn would be avoided. The amount of European negative yielding sovereign debt retreated from its $17 trillion peak to $12 trillion. But since word of the severity of the coronavirus epidemic broke during the third week of January the T-Bill spread has started to shrink and the amount of negative yielding Euro-debt climb.

It is too soon for any economic data to manifest a downturn arising from the disruption of global supply chains, and at this stage the fears outlined are simply fears that need not become reality. But if you assume that the rising gold price has been driven more by general uncertainty than inflation and fiat currency debasement fears, making it serve more as a safe haven than an inflation hedge, the coronavirus only adds to the uncertainty. On a day-to-day basis the price of gold is inversely related to the direction of US equity markets, but on a longer term scale the trend for a repricing into the $2,000-$3,000 range driven by rising uncertainty remains intact.

The enthusiasm at the Metals Investor Forum in Vancouver on January 17-18 was the strongest observed since these conferences began during the past decade, but a big question is whether the apparent turnaround in sentiment is just a manifestation of the January Effect, the tendency to flush away the disappointments of the prior year and greet the new year with optimism, or the real thing. Last year there was no observable January Effect, with the KRO 2019 Favorites Index achieving a maximum gain of 9.7% in late February. Although two-thirds of the KRO 2020 Favorites Index are the same companies as last year, it peaked at 18.4% on January 22 and as of February 3 was up 16.8%, a considerably better start to the year than in 2019. The TSXV Index is lagging the KRO 2020 Favorites Index, most likely due to deflating market interest in the cannabis sector, in particular the also-ran juniors which never migrated to the TSX. You can see this in the graphic below which shows a modest increase in the valued traded by TSXV resource sector listings since the start of 2020 with the percentage of all value traded creeping above 50% during the second half of January.

We cannot yet declare that the 8 year bear market for resource juniors which began in 2011 has turned into a bull cycle. While the growing uncertainty about where the world is headed economically and historically continues to be a case for a rising real gold price that will have a leveraged impact on ounce in the ground stories and even discovery plays because a higher price lowers the bar for what counts as a gold discovery, the resource juniors still face a head wind in the form of weakening commodity prices, in particular base metals such as copper and zinc. If one is inclined to believe the pessimistic outcome for the global economy as a result of China's disruption as both consumer and supplier due to the coronavirus, keep in mind that the resulting deglobalization of commodity markets could have surprising effects on metal prices and even a positive effect on juniors with non-gold projects in reasonably secure jurisdictions. Even if a general market decline accompanied by an economic slow-down sweeps the United States, the resulting Fortress America psychology will be good for resource juniors focused on projects in North America and maybe some parts of Latin America. There is also the possibility that economic stress will spur a popular call for infrastructure spending which traverses the entire political spectrum and could become the healing mechanism for a deeply polarized country. We could end up with a scenario where gold continues to rise because deficit spending will be the key to infrastructure renewal and no longer of any concern to either party, while the very act of shaking off the End Times mentality could pull the global economy out of a China induced funk. With regard to the resource junior sentiment cycle we are transitioning from the depression to hope stage.

FPX Nickel Corp reported on January 7, 2020 that test work by Sherritt Technologies on its 65% nickel concentrate from the Decar project in British Columbia was successful in demonstrating that pressure leaching will deliver a high purity chemical solution with 98.8%-99.5% recovery to which conventional solvent extraction can be applied to yield a nickel sulphate product suitable for the battery market. Although the testing was bench scale and would require larger scale confirmation, its results...

Yorbeau Resources Inc is a Bottom-Fish Spec Value rated Favorite because it is an orphaned junior with an undervalued portfolio of advanced and exploration projects in Quebec that would quickly attract market interest if the resource junior bear market turned bullish. Founded in 1984 and listed on the TSX Yorbeau has never done a rollback and as of early 2020 had 340.1 million issued and 349.2 fully diluted with no warrants. A good part of the stock is held by Quebec institutions, and the weak p...

Azimut Exploration Inc reported drill results for the 100% owned Elmer project in the James Bay region of Quebec on January 14, 2020 which caused the stock to triple on heavy volume, spurred market interest in several juniors with existing properties in the vicinity, and even prompted prospect-generator Midland Exploration Inc to map-stake a large 30 km land package south of Azimut's Elmer-Duxbury package. Based on 64.4 million shares fully diluted and a $1.48 price the Elmer project has achieve...

Golden Goliath Resources Ltd has a Bottom-Fish Spec Value rating effective January 28, 2020 based on its recent pivot from Mexico into the Red Lake district where it acquired strategic claims in late 2018 covering two faults believed to tap deeper plumbing in the manner now recognized for the LP fault to the north which is now part of the Dixie project on which Great Bear Resources Ltd has 4 rigs turning. In 2004 the Ontario government commissioned lithoprobe studies in western Ontario as part o...

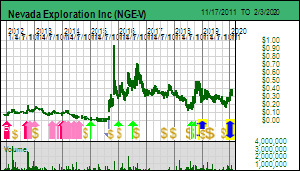

Nevada Exploration Inc provided the first of planned monthly updates on January 30, 2020 for the 2020 RC drill program at the 100% owned South Grass Valley project in Nevada. Drilling started on January 6 at the Freddie target to the west of the northern core holes drilled in 2018-19, with a second smaller rig starting a week later at the southern end on the Golden Gorge and Waterfall targets. Although the update consists mainly of descriptions of rock types encountered in each of the 5 holes so...

Namibia Critical Metals Inc made a major announcement on January 27, 2020 to which the market had a misguided negative reaction. NMI has done a deal which will allow JOGMEC to earn up to 74% of the Lofdal rare earth project in Namibia by funding it through production. NMI was a Bottom-Fish Spec Value rated Favorite in 2019 based on exploration plans for the project portfolio acquired from Gecko, the South African company that turned NMI into its Namibian exploration arm. The Lofdal rare earth de...