Hello Guest User, You are visiting this website from a computer with an IP address of 172.69.6.93 with the name of '?' since Sat Apr 20, 2024 at 9:15:49 AM PT for approx. 0 minutes now.

Kaiser Media Watch Blog - September 1, 2020 to September 30, 2020

KRO Blog Overview

The KRO Blog is where unrestricted content of a time sensitive nature is posted. It includes the Kaiser Media Watch Blog which features content involving John Kaiser produced by third parties such as the Discovery Watch series by HoweStreet.com, interviews by outfits such as Investing News Network, SDLRC related commentary, the KRO Monthly Summaries, and just about anything else John writes that is not intended exclusively for the fee based KRO Membership.

Discovery Watch is a weekly 15-30 minute audio show produced by HoweStreet.com where Jim Goddard interviews John Kaiser about resource juniors with projects that have caught John's attention. The projects will not be limited to companies he has covered through the Spec Value Rating System. Jim and John will periodically circle back to review the projects and if necessary close them out as no longer worth watching. Check out the catalog of KRO Free Stuff. We currently have a USD $275 Membership Special which grants full access to the end of 2020. Discovery Watch is available via YouTube or Podcast..

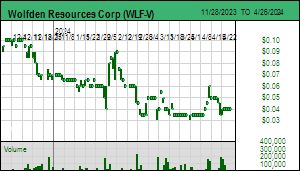

Wolfden Resources Corp was introduced to DW in August 2018 based on the intriguing story of Maine reforming its mining code and re-opening itsef to exploration after more than a decade of no trespassing signs. Wolfden was a first mover to do a deal on the Pickett Mtn VMS system which Getty found and explored during the 1980's. Since then we have been watching to see if Wolfden can expand the existing resource. This was accomplished with the January 2019 resource estimate for the West-East lenses after drilling pushed the West Lens deeper. 2019 was supposed to be the year Wolfden discovered new lenses in the Footwall Zone and in fold limbs parallel to the West-East lens limb. But technical drilling problems turned the campaign into a bust except for a teaser stringer zone in which the last hole was lost. But during 2019 Wolfden flew geophysical surveys, not just on the property, but also on a 30 km by 10 km grid covering geology similar to that which hosts the Bathurst Camp in New Brunswick and Buchans in Newfoundland. To avoid equity dilution Wolfden raised USD $3.5 million January 2020 by selling timber rights. It also filed for land use rezoning from logging to industrial for a 500 acre parcel that would be the site for mining infrastructure. This rezoning is necesaary for a mining permit application and they hope to get it by Q1 of 2021. In early Q3 2020 Wolfden will publish a PEA for a 1,000 tpd UG mine which was the basis for the rezoning application. I created a SC 1,000 tpd scenario OV in the ShareCollective which yields a USD $135 million after-tax NPV that implies a future CAD $1.24 stock price, but that is a worst case scenario. Much more interesting is the exploration potential to boost the existing resource to 10 million tonnes at the same grade so as to support a 2,000 tpd scenario with a 10 year mine life. The SC 2,000 tpd scenario is much more interesting at USD $464 million NPV with a corresponding CAD $4.26 stock price. Wolfden began a 5,000 m drill program in July 2020 designed to test multiple new targets at Pickett Mtn whose EM conductors represent potential tonnage footprints of 15-20 million tonnes. The DW hope is that Wolfen turns one or more of these targets into satellite massive sulphide zones that boost the resource towards 10 million tonnes. Failing that, Wolfden is negotiating with landowners for deals on some of the sourrounding area it flew in 2019. If successful, the play turns into a regional quest for Buchans scale VMS clusters. On July 13, 2020 John Kaiser conducted a Zoom Interview with CEO Ron Little and Expl VP Don Dudeck. (Jul 15, 2020)

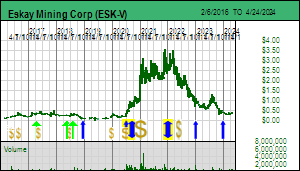

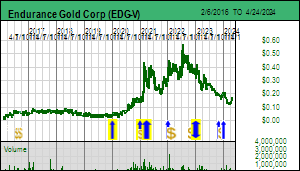

Disclosure: JK owns Endurance Gold and Wolfden; Eskay Mining is a Fair Spec Value rated Favorite, Wolfden is a Good Spec Value rated Favorite, Endurance is a Bottom-Fish Spec Value rated Favorite

Discovery Watch is a weekly 15-30 minute audio show produced by HoweStreet.com where Jim Goddard interviews John Kaiser about resource juniors with projects that have caught John's attention. The projects will not be limited to companies he has covered through the Spec Value Rating System. Jim and John will periodically circle back to review the projects and if necessary close them out as no longer worth watching. Check out the catalog of KRO Free Stuff. We currently have a USD $275 Membership Special which grants full access to the end of 2020. Discovery Watch is available via YouTube or Podcast..

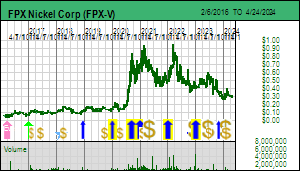

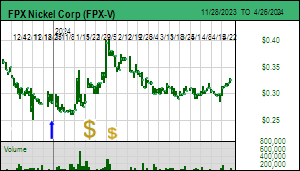

FPX Nickel Corp has had a Bottom-Fish Spec Value rating since 2017 while the junior worked on over-coming the limitations embedded in the PEA Cliffs delivered in March 2013 for a 114,000 tpd open-pit nickel mine at Decar which required a $9/lb plus nickel price to be viable. Most of this work has been completed and 2020 promises to be a relaunch of the Decar nickel story with an updated PEA expected in September 2020. FPX was introduced to Discovery watch in November 2016 as a different type of discovery in the sense that the Decar deposit, recognized in 2009, is unusual in having a very low 0.12% nickel grade as defined by a Davis Tube assay which only measures nickel recoverable through crushing and magnetic separation. This is different from a fire assay which will yield a similar grade for almost every ultramafic body that is economically worthless because it reflects nickel trapped in an olivine lattice. The Decar nickel is different because it occurs as awaruite, a nickel-iron alloy that is in effect natural stainless steel. The result is a very homogenous 1 billion tonne deposit that can be large scale open pit mined for 40 years without any sulphide related acid drainage and which, thanks to the magnesium content that ends in the tailings, could operate as a carbon sink which could bring Decar close to the holy grail of a carbon neutral mine. The key changes achieved by FPX management headed by Peter Bradshaw and Martin Turenne since buying back 100% ownership from Cliffs in 2015 are 1) replacing gravity separation with a flotation stage that generates a concentrate with 65% nickel that can be fed directly into stainless steel mills, delineation of the SE Baptiste zone that allows front-loading the ore schedule with higher grade ore, and preliminary studies that indicate that the concentrate can be converted directly into nickel sulphate, the form required by the EV battery market. FPX is unusual in that it has been funded by insiders and close associates through private placements that did not include warrants, a sign of strong internal belief that Decar is a winner. A key question the PEA will answer is the cost structure of Decar using the new flowsheet, which will make it easier to assess the potential economic value of developing Decar, expected to have a CapEx of $2 billion or more. The wild card is the future price of nickel which during the past decade has suffered from a glut of low grade laterite ore mined in Indonesia and the Phillipines and shipped as whole rock to Chinise blast furnaces where it is converted into nickel-pig-iron, a feedstock for lower quality stainless steel that meets China's standards. Indonesia no longer allows direct shipping of ore, and the Philippines is rapidly depleting the laterite resources suitable for this NPI market. The FPX PEA will show what nickel price is needed to achieve an NPV at least 50% of CapEx. Given that it will take another $40-$50 million to push Decar through feasibility to a permitted production decision, the speculative question is who might pay what percentage of the NPV at what stage for the privilege of investing another $2 billion to develop Decar as a 40 year mine in a secure jurisdiction that threatens little variation during the life of the mine. A decade ago the FPX team scoured the world in search of similar deposits, but concluded that Decar is pretty much unique. (Jul 22, 2020)

Disclosure: JK owns FPX Nickel & Scandium Intl; FPX Nickel is a Good Spec Value rated Favorite, Scandium Intl is a Bottom-Fish Spec Value rated Favorite; Golden Goliath is Bottom-Fish Spec Value rated.

Discovery Watch is a weekly 15-30 minute audio show produced by HoweStreet.com where Jim Goddard interviews John Kaiser about resource juniors with projects that have caught John's attention. The projects will not be limited to companies he has covered through the Spec Value Rating System. Jim and John will periodically circle back to review the projects and if necessary close them out as no longer worth watching. Check out the catalog of KRO Free Stuff. We currently have a USD $275 Membership Special which grants full access to the end of 2020. Discovery Watch is available via YouTube or Podcast..

Azimut Exploration In was introduced to Discovery Watch in September 2016 due to its minority stake in the Eleonore South project in the James Bay region of Quebec which covers the southern half of the Cheechoo intrusion where Sirios Resources Inc caught the market's imagination in early 2016 by rethinking a low grade bulk tonnage gold optionality into a potential high grade underground mineable system. Sirios started drilling the intrusion with NE oriented holes instead of SW holes and while initially this seemed to deliver high grade intervals more consistently, after several years it became apparent that the Cheechoo intrusion did not host coherent high grade zones that would lend themselves to underground mining. Sirios has since reverted to a bulk tonnage model and published a resource estimate in late 2019. Azimut's CEO Jean-Marc Lulin became the champion for Eleonore South which it had staked during the early days of the Eleonore discovery by Virginia. Work by Goldcorp and Eastmain failed to deliver a discovery because it was focused on the margins of the Cheechoo intrusion. JML focused on potential high grade zones such as Moni, but that effort grounded out just like that of Sirios. Today it is clear that Eleonore South and Sirios' Cheechoo needs to be consolidated as one property with a large open pit operation which has the support of Newmont (after acquiring Goldcorp), which is also a major shareholder of Sirios. The stick in the mud resisting a win-win proposal has been Azimut, which stopped funding its share of Eleonore South in 2018 when it decided to violate the PGFO strategy by drilling the Chromaska chromite target with its own money. Chromaska died quietly, and it looked like Azimut was a DW bust on two fronts. But in early 2019 when Midland's Mythril copper discovery ignited hopes for a base metals area play in the James Bay region Azimut's Pikwa project to the west became a DW focus after Azimut was able to swing a deal with SOQUEM to earn back a 50% interest. Mythril fizzled in H2 of 2019 when it became apparent that the very high grade copper mineralization was restricted to thin margins of dykes that weren't spaced closely enough to deliver a bulk mineable resource similar to that of the Aitik copper mine in Sweden. During 2019 Azimut focused on mapping and sampling the 20 km Copperfield Trend which projects SWW from the 10 km trend on Midland's Mythril project and established that there were major copper anomalies in the western and eastern ends of the anomaly. The middle seemed to be a dead zone though it did contain 2 prominent EM conductors, the only such anomalies within this trend. The geochemical dead zone may be due to the presence of a giant esker of glacially transported debris that obscures the bedrock. An IP survey in the East Copperfield portion yielded chargeability highs similar to those on the Mythril property to the east, which raised the question of whether Pikwa hosted more of the same marginal copper mineralization. Azimut decided to extend the IP survey west to include the EM conductors, because these could be part of a "center of gravity" for the mineralizing system where bigger zones may have evolved in this Archean setting. We are still awaiting the outcome of this IP survey and what Azimut plans next for Pikwa. Since December 2019, however, the DW focus has been on the Elmer project in the James Bay region where Azimut has demonstrated that the small 200 m by 80 m Patwon outcrop hosts 3 sets of mineralized gold veins: a set of short NW oriented Riedel type dilational veins, a set of sub-horizontal veins, and a set of NE-SW oriented veins, all occurring within what appears to be a 7 km NE trending shear structure. The high grades within the Patwon zone attracted market attention in January 2020 and Elmer was shaping up as a Discovery Watch success story. The association of pyrite with the gold prompted Azimut to conduct an IP survey which generated multiple chargeability highs of the sort associated with sulphide mineralization. Drilling resumed in late May 2020 with the first update occurring in late June after 29 new holes were drilled. Although the market initially responded positively, driving the stock as high as $3.50, the cautious wording by Azimut and the shifts in the drill location sequences of the two rigs suggested that expansion drilling was not playing out as expected. On July 27 Azimut disclosed results for holes close to Patwon which extended the strike 350 m and confirmed mineralization persists to a depth of 200 m. But it is disrupted to the SW and in the NE direction where holes not discussed are pending and where the IP chargeability anomaly is low rather than high. In fact, early holes drilled in ELM-1 where the IP anomaly is strong were not prioritized for assaying. During July Azimut drilled only 7 more holes, most of them in the other ELM IP anomalies. 18 holes were still being logged and assays are unlikely before September. The DW premise was that the Patwon zone would repeat itself along the 7 km shear, most of which is covered by swamp or overburden, with IP anomalies highlighting targets. It now looks like IP is not highlighting gold zones, so until we learn more about the geology and gold controls, the Elmer play is focused on definition drilling of the Patwon zone for a possible open pit scenario and chasing this style of mineralization deeper for an underground scenario. Elmer qualifies as a discovery, but for now it is not a game changing development for the gold potential of the James Bay region. (Jul 29, 2020)

Disclosure: JK owns none; Serengeti is a Bottom-Fish Spec Value rated Favorite, Azimut is a Fair Spec Value rated Favorite.