Hello Guest User, You are visiting this website from a computer with an IP address of 172.70.100.182 with the name of '?' since Sat Apr 20, 2024 at 7:33:00 AM PT for approx. 0 minutes now.

Kaiser Media Watch Blog - June 1, 2021 to June 30, 2021

KRO Blog Overview

The KRO Blog is where unrestricted content of a time sensitive nature is posted. It includes the Kaiser Media Watch Blog which features content involving John Kaiser produced by third parties such as the Discovery Watch series by HoweStreet.com, interviews by outfits such as Investing News Network, SDLRC related commentary, the KRO Monthly Summaries, and just about anything else John writes that is not intended exclusively for the fee based KRO Membership.

Discovery Watch is a weekly 15-30 minute audio show produced by HoweStreet.com where Jim Goddard interviews John Kaiser about resource juniors with projects that have caught John's attention. The projects will not be limited to companies he has covered through the Spec Value Rating System. Jim and John will periodically circle back to review the projects and if necessary close them out as no longer worth watching. Check out the catalog of KRO Free Stuff. KRO offers a USD $450 Annual Individual Membership. This Discovery Watch session is available via YouTube or Podcast.

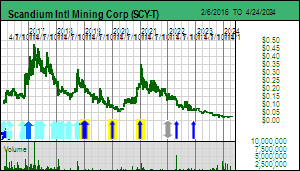

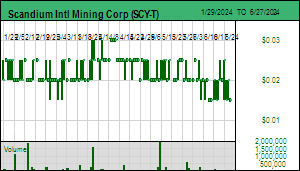

The shareholders who own 55% of Scandium International's 316.3 million issued shares and who do not have a seat at the boardroom table, and thus rely on bread crumbs the CEO drops inside the company's 10K and 10Q filings, of which the next one is not due until August 16, have been treated to fresh bread crumbs by Rio Tinto and Barrick to keep their hopes alive. On June 17, 2021 Rio Tinto announced that it has started operations at a new commercial scale demonstration plant at its Rio Tinto Fer et Titane facility in Sorel-Tracy in Quebec. The plant, which will produce 3 tpa of scandium oxide, was built at a cost of $6 million in less than 6 months. It has a modular design and Rio Tinto is already contemplating expansion of capacity. Rio Tinto revealed its scandium recovery plan in May 2021 a week after SCY put out a press release about its plan recover critical metals from the raffinate generated by SXEW copper oxide mines. Apart from grudgingly conceding that the US Patent Office granted a patent on April 27, 2021 for recovering scandium with its CMR method (an application covering a much bigger list of metals is still pending), SCY has published no further news about its efforts to secure a hosting site for its CMR plan. The Rio Tinto news that it is now in the scandium production business is very good news for SCY even if it never gets its CMR plan off the ground, for Rio Tinto's upside output limit from Lac Tio ore processed at Sorel-Tracy is about 50 tpa scandium oxide. And that means if Rio Tinto cracks the scandium offtake market chicken-egg problem by incrementally ramping up scandium supply, it had better start thinking soon about from where it can secure primary, scalable scandium supply before sleepy Alcoa wakes up and buys out SCY. Nyngan already has a mining lease for a 35 tpa output and can be scaled up to 125 tpa.

SCY's 2014 press release about its Honeybugle discovery south of Nyngan included enough bread crumbs to allow one to do a rough back of the napkin resource estimate which suggests Honeybugle could be bigger and richer than Nyngan. I've done a speculative DCF analysis of a 1,000 tpd Honeybugle scenario that borrows the Nyngan expansion scenario cost structure and it is safe to say that for SCY shareholders it is a good thing a more swift-footed junior willing to promote its story does not own Honeybugle. The Rio Tinto bread crumbs suggest that SCY should just stop wasting money pretending to be working on a CMR hosting deal and simply spend a few dollars on producing a resource estimate for Honeybugle and a metallurgical study to confirm that it is the same laterite ore as Nyngan. And wait for the buyout auction to begin. But Barrick provided some bread crumbs on its May 25, 2021 Nevada Gold Mines Investor Day which strongly indicate that SCY's CMR plan has made huge progress. Listen to the 8:47 minute Phoenix Video. Barrick first mentioned a critical metals recovery study with a "local partner" in its Q1 2021 presentation but did not mention the target metals nor the partner's name. That allowed the SCY CEO during the junior's AGM to answer a question by a member of the 55-percenter shareholder class with a dismissal that the partner could be anybody. Yet in the video Megan states that the Phoenix CMR study has identified zinc, nickel, cobalt and scandium as recoverable from the SXEW circuit's raffinate. Not only does that rule out any party but SCY, for who else would bother to recover a metal with an annual market of less than 25 tonnes worth only $50 million? It is very unlikely that Barrick's CEO Mark Bristow wants to compete with Rio Tinto in developing the Al-Sc alloy offtake market, but doing so incrementally with the help of its own master alloy proficiency is most certainly SCY's goal. But the really tasty bread crumb in this news is that the study is far enough along for Barrick and SCY to have identified zinc, nickel and cobalt as key target metals. Each deposit has a unique composition for which a leaching agent has been optimized, which means each mine's raffinate will have a unique collection of other metals unintentionally dissolved. The purpose of the study is to establish what SCY's ion exchange method can commercially recover from the raffinate, and that takes time, which obvious has already taken place or Megan wouldn't be talking specific metals. But why would Bristow publicly talk about this if a hosting deal still has to be negotiated with the SCY CEO who is a notorious over-optimizer and who just might play hardball with Bristow, potentially leaving him exposed to accusations by Barrick shareholders that he is fishing for fake ESG credits? My guess is that Barrick and SCY already have a deal in principle that both see as a win-win, and when the timing is right it will be inked and disclosed. So while SCY may have other reasons for feeding its 55-percenters tiny bits scraped off a stale Christmas cookie, Barrick is quite comfortable handing out an entire loaf of fresh baked bread. The graphics above show what Honeybugle is potentially worth, while the one below shows what the Nyngan expansion scenario is worth. Obviously Honeybugle would be developed many years later as scandium demand ramps toward 1,000 tpa Sc2O3, so you cannot stack these valuations, but if scandium demand reaches a tipping point where it can start going exponential, the market will start telescoping future value into a current, much higher stock price.

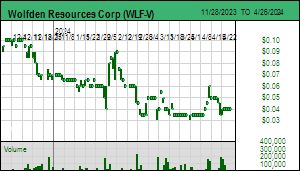

Disclosure: JK owns Scandium Intl and Wolfden; Scandium Intl is a Bottom-Fish Spec Value rated Favorite, Wolfden is a Good Spec Value rated Favorite; Eskay Mining is Fair Spec Value rated.

Discovery Watch is a weekly 15-30 minute audio show produced by HoweStreet.com where Jim Goddard interviews John Kaiser about resource juniors with projects that have caught John's attention. The projects will not be limited to companies he has covered through the Spec Value Rating System. Jim and John will periodically circle back to review the projects and if necessary close them out as no longer worth watching. Check out the catalog of KRO Free Stuff. KRO offers a USD $450 Annual Individual Membership. This Discovery Watch session is available via YouTube or Podcast.

Discovery Watch is a weekly 15-30 minute audio show produced by HoweStreet.com where Jim Goddard interviews John Kaiser about resource juniors with projects that have caught John's attention. The projects will not be limited to companies he has covered through the Spec Value Rating System. Jim and John will periodically circle back to review the projects and if necessary close them out as no longer worth watching. Check out the catalog of KRO Free Stuff. KRO offers a USD $450 Annual Individual Membership. This Discovery Watch session is available via YouTube or Podcast.

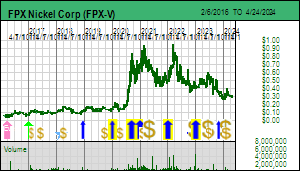

FPX Nickel is a wonderful opportunity for retail investors to learn how to value resource plays because the ability of the stock to move into a fair speculative value range of $1.50-$3.00 based on the economic value projected at the base case price of $7.75/lb nickel by the 2020 PEA requires an institutional audience to embrace the company. That has not yet happened because FPX proposes to mine the lowest grade nickel deposit in history and is targeting a natural stainless steel mineral that has never before been mined. What keeps the institutions on the sidelines is the fact that the viability of Decar hinges on the metallurgy behind the flow-sheet which has only been tested at a bench scale for a project that has world class scale. FPX is conducting larger scale tests of the flow-sheet as part of the $15 million PFS expected to be done by the end of 2022. These metallurgical results are expected in August 2021. If they support the PEA assumptions, we can expect institutions to take a much closer look at FPX, especially in light of the carbon sequestration work FPX is doing on the tailings which may make this project carbon neutral. The value upside and the ESG credentials will bring institutions into FPX Nickel and drive the stock into the $1.50-$3.00 range where the stock will trade ahead of a buyout in the $5-$10 range if the PFS delivers an outcome similar to that of the PEA. The graphics above and below are variations of the same thing, the after-tax net present value calculated at 5% and 10% discount rates at different nickel prices. The chart above expresses the outcomes in CAD per share terms (228 million fully diluted is a stable number because with $21 million working capital FPX has more than it needs to deliver the PFS), while the one below expresses it in USD absolute numbers.

Disclosure: JK owns FPX Nickel and Scandium Intl; FPX Nickel is a Good Spec Value rated Favorite, Scandium Intl and P2 Gold are Bottom-Fish Spec Value rated Favorites

Discovery Watch is a weekly 15-30 minute audio show produced by HoweStreet.com where Jim Goddard interviews John Kaiser about resource juniors with projects that have caught John's attention. The projects will not be limited to companies he has covered through the Spec Value Rating System. Jim and John will periodically circle back to review the projects and if necessary close them out as no longer worth watching. Check out the catalog of KRO Free Stuff. KRO offers a USD $450 Annual Individual Membership. This Discovery Watch session is available via YouTube or Podcast.

The big news for Scandium International Mining Corp is that Barrick in its Q1 2021 results presentation on slide 20 declared that with regard to its gold-copper Phoenix mine in Nevada (61.5% Barrick, 38.5% Newmont) it stated that it has "Initiated a study on the potential recovery of selected critical metals from the SXEW raffinate, in partnership with a local third party". The slide in the Q4 2020 results presentation dealing with Phoenx and Long Canyon made no such statement. The fact that Barrick would include the reference to the CMR study in a corporate presentation that will be reviewed by its huge institutional shareholder base suggests that this study is well advanced and is showing a lot of promise. Who could that local third party be? Scandium International held its AGM on the morning of June 3, 2021. Maybe 5 shareholders were on the Zoom call and asked questions. One brought up the Barrick slide comment with the suggestion that the partner is unlikely to be anybody but SCY. The CEO's response, rather than just plead "no comment, all our CMR dealings are under non-disclosure agreements", insisted that it is possible Barrick is dealing with another party. That would truly be amazing if somebody else based in Nevada has managed to get Barrick to participate in a study about recovering certain critical metals from a copper SXEW raffinate. I feel so sorry for SCY's CTO Willem Duyvesteyn who is the driving force behind SCY's CMR strategy if Barrick is indeed referring to another group. But the CEO is only correct in a logical sense; in probability terms his response is an arrogant dismissal of the shareholder question. In response to another question about better disclosures, the CEO pronounced that "shareholders can follow the bread crumbs by reading the 10K and 10Q filings". Well I have been doing that, but the need to do that presents a strong case for a change in corporate culture at SCY.

For whatever reason the SCY management is doing its best to discourage the market about the company's future. It still has not updated its March 2020 corporate presentation to reflect the shift to the CMR strategy and the pursuit of HPA production. Neither has the company said anything about Rio Tinto's breakthrough at Sorel-Tracy in recovering scandium while upgrading its 80% titanium slag to the 95% rutile equivalent TiO2 grade now required by pigment makers. No discussion that Rio Tinto now has an incremental scandium supply growth strategy that can spawn scandium demand gradually, overcoming the chicken-egg problem without a huge risky upfront CapEx investment. SCY's CMR strategy, for whose scandium recovery it already has a patent, can deliver the same incremental growth. Once SCY gets a CMR hosting deal, it and Rio Tinto can build out the offtake market for scandium which has a long term potential to grow to 1,000 tpa Sc2O3. If either is successful, building global supply into the 50-100 tpa range with offsetting demand, that will be the tipping point for rapid demand growth which can only be served by developing larger scale primary supply, for which role SCY's Nyngan project is ready. In late 2019 the scandium chicken-egg problem looked hopeless and Nyngan had become worthless because there was no plausible timeline for its development. But copper SXEW CMR and Sorel-Tracy changes everything. The Nyngan asset now has a future, maybe being developed 3-5 years from now when scandium demand takes off.

It has an optionality value that should be reflected in the SCY stock price ahead of any progress on the CMR or HPA fronts. Not just as a 35 tpa output project as defined by the 2016 DFS, which exploits only a fraction of the resource, but one that expands operating capacity in cash flow funded stages to 4 times the initial capacity. To see what this expansion might be worth to Rio Tinto if it has success with its Sorel-Tracy plan, I have done a discounted cash flow model of this expansion scenario. Assuming the $2,000/kg price for Sc2O3, the expansion scenario has an after tax NPV value of USD $762 million at 5% discount rate and $414 million at 10% which translates into a stock price range of CAD $1.43-$2.64 at current exchange rates and 349 million fully diluted. That is the range one might expect Rio Tinto to pay down the road when it needs to expand its scandium supply beyond the 50 tpa limit from Lac Tio ore at Sorel-Tracy. But we don't know how far down the road that will be, and with a project stuck at the completed feasibility study stage with no funding to move on to construction, the fair speculative value range for this future outcome is 50%-75%. Thus at the 10% discount range SCY should have an optionality value range of $0.72-$1.07, and if you push it to a 5% discount rate, the range is $1.32-$1.98. SCY should be trading between $0.50-$1.00 just on the optionality value of Nyngan alone, before any value is added for the CMR and HPA plans. In fact when you consider the future development potential for Keviniemi and Honeybugle, the value should be even higher. When you consider that SCY has mastered downstream master-alloy capability, and can branch into recovering critical metals other than scandium from various waste streams in premium commanding high purity forms, the company is a candidate for a bubble stock. The corporate culture should include promoting all this potential, not demoting it.

Disclosure: JK owns Endurance Gold, Namibia Critical Metals and Scandium Intl; Endurance is a Good Spec Value rated Favorite, Namibia Critical Metals and Scandium Intl are Bottom-Fish Spec Value rated Favorites