Hello Guest User, You are visiting this website from a computer with an IP address of 172.70.178.48 with the name of '?' since Fri Apr 19, 2024 at 3:33:15 PM PT for approx. 0 minutes now.

Kaiser Media Watch Blog - May 1, 2023 to May 31, 2023

KRO Blog Overview

The KRO Blog is where unrestricted content of a time sensitive nature is posted. It includes the Kaiser Media Watch Blog which features content involving John Kaiser produced by third parties such as the Discovery Watch series by HoweStreet.com, interviews by outfits such as Investing News Network, SDLRC related commentary, the KRO Monthly Summaries, and just about anything else John writes that is not intended exclusively for the fee based KRO Membership.

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch May 24, 2023: What two global crises mean for resource juniors

Jim (0:00:00): What will be the topic of your presentation at the upcoming Metals Investor Forum in Vancouver this weekend?

The Metals Investor Forum will take place in Vancouver at the Rosewood Hotel on Friday May 26 and Saturday May 27. Participation is free to the public but one must register online ahead of time. My session is on Saturday in the afternoon at 1:50 pm. My topic will be "Two Global Crises: what they mean for resource juniors". I will play on the theme Yellow, Red and White Gold reflecting the three metals I believe will be most important for the junior resource sector over the next couple years. I will also refer to Iridescent Gold as a catchall for metals whose supply will be disrupted if the geopolitical conflict between China and the United States turns hot.

Yellow gold, of course, is the regular gold whose price trend seems to have a permanent grip on the mood of the audience for resource juniors. Gold this past month has been struggling to establish $2,000 as its new base rather than a ceiling which it stopped short of in 2011, and briefly broke through in 2020 during the covid pandemic and again in 2022 when Russia invaded Ukraine. This year, despite interest rates having been jacked to the highest level since 2007, gold has clawed its way above $2,000. The current reason seems to be anxiety about what will happen if the US debt ceiling is not lifted and the United States defaults on its obligation to pay its debts. When the Republican Party first launched a debt ceiling extortion attack in 2011 the capitulation by the Obama administration was followed by an 8 year bear market for gold that did not turn around until 2020 when the world was blindsided by the covid pandemic which prompted extraordinary measures that cranked up the US debt and bestowed on Trump the honor of seeing the national debt increase during his term by a greater amount than accomplished by any predecessor. Biden is on track to becoming the new debt increase champion by the end of 2024 and this is supposedly what the Republican Party is upset about now.

What is different today from a decade ago is the geopolitical context. A decade ago China was still a fast growing economy with quite a ways to go before catching up with the United States. Although America's financial sector engineered the global financial crisis, the United States was still resting on its laurels as the leader of a globalized economy. But a lot has changed in the past decade, starting with the emergence of Xi Jinping as China's new leader. At the time the hope of the "liberal" world order was that growing prosperity would cause China's hybrid communist-capitalist system to become westernized and the country to become a huge market for western corporations. Xi, however, decided to re-establish China as a Communist autocracy with ever tighter control over corporate activity with a bias toward domestic entities. At the same time he used technology to impose hyper-surveillance on the Chinese people so that Beijing could make sure nothing could be heard or spoken that was at odds with Beijing's desired messaging. He also launched the Belt and Road Initiative as a way to reach into emerging countries that could supply China with the raw materials it cannot produce domestically.

Along the way Vladimir Putin, whose Russia was a fading economic power relative to the United States and China because he allowed crony capitalism parasitic on Russia's resource base to be the basis of its economy, decided it was time to re-establish the Soviet Union, starting with Ukraine, first with Crimea in 2014 and then with a full-blown invasion of Ukraine in 2022. China decided to align itself with Russia because it had a similar goal of annexing Taiwan whose existence is a democratic rebuke of China's autocracy. This accelerated the geopolitical power conflict between China and the United States which has been brewing for the past decade.

The Biden administration has packaged the conflict as one between autocracy and democracy, but it is not as simple as the Cold War conflict between Communism and capitalism. Alexander Stubb, former prime minister of Finland, recently provided a much better description of the conflict in a Financial Times opinion piece on May 10. (The west must learn from its mistakes if it wants to shape the new world order. He describes the conflict as a triangle involving the global west, which includes the United States, Europe and their allies, the global east which includes China, Russia, Iran and about 20 other outright autocracies, and the global south, which includes the non-autocratic members of the so-called BRICS nations, India, Brazil, and South Africa, plus most countries in Latin America, Africa and Asia.

This group of 125 countries that make up the global south has refused to condemn Russia's invasion of Ukraine in a UN resolution, and has been reluctant to participate in the sanctions imposed by the United States on Russia. The global south consists of countries which Freedom House would classify as "partly free" based on its civil liberties and political rights scoring system, whereas the global east would be "not free" while the global west is "free". The global south's primary goal is a better economic future. It is on the sidelines watching the struggle between the competing systems of the United States and China play out.

Unlike the Cold War where the Soviet Union had the goal of establishing global Communism run by Russians, China has no such agenda for the countries it wants as part of its trading network. Countries in the global south can shift to left or right wing autocracies, China would not care so long as it can secure some degree of economic leverage over the prevailing regime. During the Cold War the United States aligned itself with right wing autocracies whose leadership was happy for support against left wing opposition. Now that Russia is a right wing autocracy there is no distinction between left or right wing autocracy within the global east. It is really a struggle between China and the United States for domination of the global economy, and the global south's primary question is, how will we benefit?

Since the US dollar is the primary exchange medium for global trade and also provides price discovery, the underlying desire within the global west and global south nations is to keep using the US dollar for trade, both to price the exchange of goods and services and to park the proceeds of a consummated transaction. The very fact that the losers of a democratic election can use a meaningless concept like a debt ceiling to threaten a US default unless the winners to the bidding of the losers has already harmed the credibility of the United States. Should a default actually happen, it will stigmitize the United States as an unreliable foundation of the global dollar system. Because no other currency is as ubiquitous as the dollar, none is an ideal immediate replacement. A debt ceiling default would push the global south into a closer economic embrace with China. And even if a deal is struck, it only punts the extortion problem down the road. Gold as a fungible asset class stands to benefit as a bridge when the dollar dominated global transaction system begins to fragment. My presentation will outline how the various paths of this geopolitical conflict can allow $2,000 to become the new base for gold from which it can launch real price gains as this new world order sorts itself out. Such a development underpinned by a general understanding of the irreversible drive of a real price uptrend will create a bull market for gold exploration and development juniors. The most likely path, namely a world partitioned into separate economic zones defined by the global west and global east, with members of the global south choosing whatever zone serves their interests best, will also create a bull market for juniors chasing Iridescent Gold, namely metals such as rare earths whose supply is concentrated in the countries of the global east.

The other part of my talk will be mostly about red gold (copper) and white gold (lithium), both of which are key metals for energy transition goals. Global warming and the resulting climate change is the other global crisis for which a solution is desired by most nations except Russia whose vast land mass overlapping the Arctic stands to benefit from global warming caused by greenhouse gas emissions. It is entirely possible for the global economy to split into two isolated zones headed by China and the United States with limited trade between them while all nations remain committed to achieving the energy transition. Copper demand is projected to increase 50% by 2030 to facilitate net zero emission related goals, while the IEA projects a 500%-600% demand increase for lithium. The latter can only be accomplished if lithium carbonate establishes a floor price around $10/lb. This means that by 2030 yellow, red and white gold will have annual supply markets worth $100-$300 billion. There is insufficient copper in the development pipeline to meet this 2030 NZE goal so for it to happen the real price of copper will need to rise so that lower grade deposits are dragged into the money. The supply of copper is globally diversified, so the higher real price will promote exploration and development around the world, though many of these regions will be off limits to resource juniors because many of their countries already are global east autocracies and many of the global south are drifting into autocracy, left wing style in Latin American and right wing style in Africa and parts of Asia beyond China's influence. Members of the global west, especially if they remain interested in ESG criteria, will look for new copper supply from secure jurisdictions such as Canada and Australia where open-pittable grade tends to be lower than in other parts of the world.

Lithium, which just over two decades ago in 2005 was a tiny $200 million annual market, was worth $20-$40 billion in 2022 depending on what one uses as an average lithium price. A five-fold supply expansion by 2030 would make lithium a $100-$200 billion market, putting it in a league with yellow and red gold beyond nickel and zinc. Half of that future supply will come from Australian pegmatites and brines in China and the Lithium Triangle of South America. The other half will come from Archean cratons in Canada, Brazil, Africa and Europe. There is a vast abundance of outcropping pegmatites documented as a by-product of precious and base metals exploration. The obvious ones visible from Google Earth were grabbed a long time ago; the smaller outcrops whose sub-surface extent and lithium content is unknown are the target of Lithium Mania 2.0. Lithium enriched pegmatite exploration will unfold as the greatest exploration boom ever and it will be dominated by resource juniors.

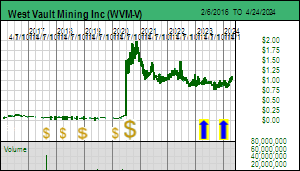

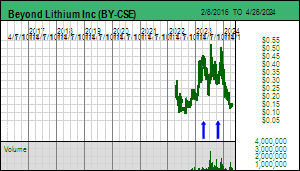

My past two MIF presentations in Vancouver and Toronto focused on the importance of lithium for the energy transition and why Lithium Mania 2.0, the hunt for pegmatite deposits beyond Australia in secure jurisdictions like Canada, will dominate resource junior speculation over the next couple years. I have only two companies in my May MIF session. The first is West Vault Mining Inc which is a gold optionality play I adopted as a Good Spec Value rated KRO Favorite in Tracker April 13, 2023 based on its Hasbrouck project in Nevada. The second is Beyond Lithium Inc which has acquired an extensive portfolio of known pegmatite showings in Ontario from a prospector group which in early 2022 assembled the claims groups using an archival research approach resembling that deployed by Brunswick Exploration Ltd last year. I did invite a copper junior to which I recently assigned a Bottom-Fish Spec Value rating but the company decided not to be part of my session, so red gold is not represented in my session.

NPV Sensitivity to Gold Price for Hasbrouck Project

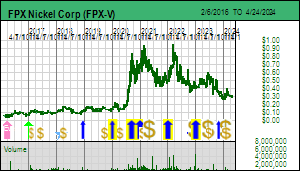

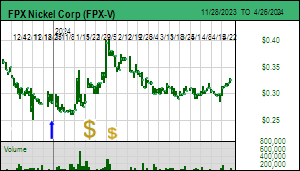

Jim (0:12:45): How important is the latest metallurgy press release for FPX Nickel?

On May 17, 2023 FPX Nickel Corp published the results of a hydrometallurgical study for the production of battery grade nickel and cobalt sulphate from the 60%-66% ferro-nickel concentrate it plans to produce from its 120,000 tpd Decar nickel project in central British Columbia. The study by Sherritt Technologies built on a scoping study published in September 2022 using a concentrate sample produced by the PFS calibre study done on the primary flowsheet for the awaruite mineralized ore in the Baptiste deposit. The work improved upon the scoping study flowsheet by adding an atmospheric leaching stage for the discharge from an initial pressure oxidation stage which allowed the recovery of a minor copper by-product and which neutralized the acid in the discharge courtesy of a reactive property of the partially leached awaruite so that the discharge could be sent back through the autoclave.

The change created three benefits: 1) removing the copper impurity in a form that has resale value, 2) reducing the amount of reagent needed to neutralize the acidity of the autoclave's discharge, and, 3) reducing the size of the required autoclave. This part of the flowsheet also removed the iron impurity which previously required a subsequent stage. Solvent extraction was then used on the pregnant liquor solution to remove the cobalt and precipitate it as a cobalt hydroxide with 99% cobalt recovery, and then applied to the nickel to precipitate nickel sulphate crystals. The optimized flowsheet demonstrated that the nickel sulphate crystals had a minimum 22% nickel content and impurity levels well below maximum specifications. The market not surprisingly yawned at this confirmation that battery grade nickel sulphate can be made from Decar's ferro-nickel concentrate which would otherwise be destined as a direct feedstock for stainless steel mills.

The nickel sulphate flowsheet will be incorporated into the PFS which is still projected for delivery in September 2023. The significance of this development is not that the nickel sulphate will add economic value to the Decar project, though this may be possible if the nickel sulphate premium above LME refined nickel is high enough. However, that outcome has two variables: the future price of LME nickel and the future premium for nickel sulphate. The real importance of this news is that it demonstrates the technical achievement of making battery grade nickel sulphate and establishes the cost of doing so. Quite likely the cost will be similar to what a battery maker may be able to pay for nickel sulphate from Indonesia, but it is the source and associated carbon footprint that matters. This is important because it expands the end-user audience for Decar's ferro-nickel concentrate beyond stainless steel makers. Currently nickel sulphate is made from dissolution of LME grade nickel briquette (matte) created by smelting of sulphide concentrates or mixed sulphide precipitates from laterite ores. Both these sources have more stages than FPX Nickel's flowsheet and have higher carbon footprints, especially in the case of Indonesia's nickel output which is mainly processed with coal powered electricity. Decar's nickel sulphate output is thus of great potential interest to North American and European carmakers, as described in a May 21, 2023 NYT article, The US Needs Minerals for Electric Cars. Everybody Else Wants them Too..

There has been plenty of head-scratching as to why none of this positive PFS related news budges FPX Nickel out of its $0.40-$0.50 trading range. I've done a 20% cost escalation for the 2020 PEA and the project still clears key development hurdles for a project of its scale and longevity. The PFS will reveal how much cost escalation has affected economics, but it will also reveal benefits from optimizations such as better recoveries. Retail audiences are generally not motivated to buy a junior whose project is at the feasibility demonstration stage, but will chase one that is trending up. Stocks at this development stage generally cannot develop an uptrend without the inflow of institutional capital. But institutions are currently avoiding the resource sector while they eye the weak post zero-covid rebound of China's economy and fret about a potential North American recession caused by persistent or even higher interest rates driven by the refusal of inflation to subside or perhaps even by a debt ceiling related default. Resource sector investors are hunkered down in the trenches.

The next fact based trigger for a repricing of FPX Nickel will be publication of the PFS in September, but that carries the risk that the numbers will disappoint the market, or nickel prices may have temporarily swooned as a result of new Indonesian supply not being matched by an increase in Chinese demand. It is possible that the revealed identity of the 9.9% strategic investor who paid $12 million at $0.50 last year would inspire an upwards repricing of FPX Nickel, but the identity of the investor would need to be a special surprise that turns heads. A mining company like Vale or BHP would inspire a shoulder shrug.

When I pressed CEO Martin Turenne on this topic he insisted that the revealed identity would have a big impact on the market's perception. That suggests it is a downstream entity. If it is a battery maker such as LG or CATL that would want an ESG qualified feedstock the strategic investment makes sense and the nickel sulphate news would be vindication even if it turns out be an economic wash. But I think a battery maker waiting to offtake nickel sulphate would hardly stir the market, even less so a more upstream chemical company with a name ordinary people never heard of. And a carmaker like Tesla also would induce a yawn because Tesla has not insisted on secrecy in other deals and having done so with FPX would just induce puzzlement. Maybe one of the other American, Japanese or European carmaker giants might excite the market, but secrecy tantalizes for only so long; when we finally find out the identity the only thing that will make jaws drop is if it turns out to be a giant, very well known brand that isn't supposed to be interested in battery feedstocks, something on the scale of an Apple or Google.

With regard to the Van deposit within the Decar property which grades similar to Baptiste and in some parts has better grades, FPX Nickel has decided not to conduct a followup drill program this year. Turenne estimates it would cost $4-$5 million to achieve the density required for a maiden inferred resource estimate. Spending less than needed to deliver a resource estimate would have no market impact other than have shareholders worry that another financing will be needed sooner than later. If FPX delivered a resource for Van similar to Baptiste the market would then ask, what is the NPV of a 40 year mine life that begins 45 years from now? Not much. What about if a parallel operation was started 15 years from now? Still don't care because the market isn't assigning a fair value to Baptiste that reflects confidence Baptiste will ever be put into production on the terms outlined in the PEA. So what difference would two birds in the bush make? Van's existence backed by a resource estimate would only matter if it could serve as a bargaining chip when majors get serious about acquiring and developing Decar. Then the threat of spinning out Van as a separate property could ratchet up the bid or the competition. So I think it is wise not to spend more money on Van for now. Does this mean there is an internal assumption no producer will come knocking until 2025? Not necessarily, because any potential bidder for FPX Nickel would understand the nature of the Baptiste and Van mineralization, would secure access to core logs through a non-disclosure agreement, and would know how to approximate a 43-101 resource estimate.

Awaruite, sulphide and laterite ore paths to nickel sulphate

Nickel Sulphate Flowsheet before and after PFS Optimization Study

Technical Specifications for Battery Grade Nickel Sulphate

Long Term Chart for Nickel Prices and Warehouse Stocks

2022 Supply Breakdown for Nickel

NPV Nickel Price Sensitivity for 2020 Decar PEA with 20% Cost Escalation

Timelines for the Advancement of Baptiste and Van deposits to Production

Van's location on other side of the mountain makes future spinout plausible

Jim (0:24:44): How do you think Lithium Mania 2.0 will play out over the next quarter?

The bungee plunge in lithium carbonate prices reached a limit of $11-$12/lb a couple weeks ago and has since rebounded into the $19-$20/lb range as battery makers restock lithium feedstock. We avoided a kersplatt for the lithium producers and explorers where the price dropped past $10 into the $3-$5/lb range reached in 2018-2020 when new supply mobilized from Australian pegmatites overwhelmed demand from the EV sector until 2021 when the reverse happened. I don't expect lithium carbonate to get back to the $30+ level but I would not be surprised to see it oscillate between $10-$20 during the rest of the year. This is the ideal scenario because within this range a 1% Li2O grade represents a rock value of $273 to $1,090 per tonne. Lithium Mania 2.0 is about finding near surface pegmatites in Canada that are open pittable. As long as a junior is finding pegmatites with a 1% or better grade and the lithium carbonate price stays above $10/lb that will be the equivalent of having an open-pittable gold discovery grading 8.5 g/t or better, or an open-pittable copper discovery grading 6.2% or better. I've created a graphic to depict the gold and copper grade equivalencies for the rock values indicated by a Li2O 1%-2% grade range and $10-$20/lb lithium carbonate price range. When you consider that these pegmatites can achieve 100 million plus tonnes, you realize there never was anything like that lucrative available for at or near surface copper or gold deposits. The only reason this opportunity exists is because of the extraordinarily short timeline for when the energy transition needs a 600% expansion of lithium supply. The key for the juniors is to demonstrate that there is lateral extent for an outcropping pegmatite grading 1% Li2O or better.

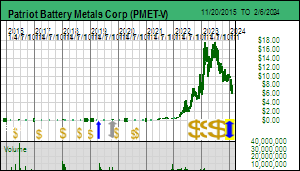

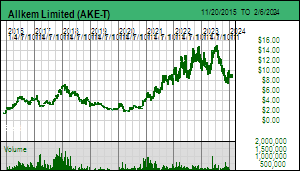

An unprecedented discovery frontier is unfolding for resource juniors focused on pegmatite exploration, in particular in Canada where pegmatites were documented during the past 70 years as a by-product of gold and base metals exploration. Now that investors long lithium juniors have shaken off the bungee plunger's sickening mid-flight question about the reliability of the weight and cord stretch calculations, the marked is poised to resume an uptrend, as soon as the debt ceiling Damocles sword as been taken away or done what it has to do. Patriot Battery Metals has rebounded from the $12-$14 range it settled into after a $17.70 peak in early February which it appears ready to challenge. The latest round of drill results continued to be in the 1.5%-2.0% range. The recently announced Allkem/Livent merger creates a new Quebec lithium champion which could prod Albemarle, Wesfarmers or SQM to make a move on PMET before it becomes too expensive. BHP and Rio Tinto have apparently sniffed that the early winners are too expensive, which leaves the field open to producers Pilbara Minerals or Mineral Resources to make premium-priced paper bids for PMET that establish a world class beachhead in Quebec's James Bay region. By July PMET hopes to have published a maiden inferred resource estimate for the CV5 pegmatite which the market expects to come in at 50-100 million tonnes of 1%-2% Li2O with some brokerage firm analysts offering estimates within the upper end of that range.

With regard to the Canadian resource juniors participating in Lithium Mania 2.0 few of them have drill programs underway, especially not in the James Bay region. Brunswick has reported partial drill results for its Anatacau West property in the southern half of the James Bay region where it has confirmed that Allkem's Cyr pegmatite system does extend onto Brunswick's property with grades of 1% or better. Brunswick started a small drill program on the Hearst pegmatite showing in Ontario in late April which should be due for a "visuals" update. But for Brunswick and nearly all Lithium Mania 2.0 juniors, including, Beyond Lithium Inc, the next big exploration stage involves putting boots on the ground to walk their properties, inspect the locations of documented pegmatites, use a LIPS or XRF gun to shoot outcropping pegmatite for lithium fertility (the XRF gun can only detect heavy element lithium pathfinders such as rubidium, which the LIPS gun is specialized to detect the presence of light elements such as lithium), try to identify spodumene in the field, and at a minimum collect samples for lab confirmation. A key part of this prospecting wave, which will unfold across Canada and I predict will be the biggest such prospecting wave in the history of Canadian exploration, will be to assess the lateral extent of pegmatite outcrops which may have only limited exposure.

Regions such as the southern half of James Bay where big outcropping pegmatites such as Cyr, Wabouchi, Rose and Moblan were found many decades ago will be the focus of "second order" exploration where indicators such as geology, lake bottom sediments and glacial dispersion history will be applied to focus prospectors into areas where pegmatite outcrops may be too subtle or small to have attracted attention in prior decades when lithium was still a smallish market. Some of these areas are more accessible than others which is why Brunswick will shortly be back on the Anatacau West and the much larger main Anatacau block 22 km to the east for boots on the ground inspection. The rumor mills in social media networks will be buzzing this summer with "reports from the field", especially for properties in minimally explored areas like the northern half of James Bay where PMET's Corvette pegmatites sit and where "first order" outcrop discoveries with considerable exposed size are entirely possible. While we may get LIPS or XRF readings indicating high Li2O grades these numbers will not be representative. Trench samples will take 2-3 months for assays to arrive.

With most companies heading into the field this June the earliest wave of surface values will be August, setting the stage for drill programs in September. Most companies will not be able to mobilize a drill program until Q1 of 2024, but the market will be watching the fall drilling juniors very closely for confirmation of another CV5 scale discovery. For by then Patriot Battery Metals may already have disappeared through a buyout by a bigger company. And because the PMET shareholders understand that Corvette is only an incremental solution to the projected 2030 supply requirements, much of the proceeds of a PMET buyout will be recycled into other Lithium Mania 2.0 juniors. But most importantly, the large retail and institutional audience on the sidelines will have seen the rapid wealth creation cycle of PMET, and will finally understand that lithium is evolving into a $100-$200 billion market that puts it in a league with yellow and red gold, but with open pittable rock values that are no longer possible to find at surface for gold and copper anywhere in Canada. By Q4 of 2023 there will be an unprecedented inflow of speculative risk capital into lithium focused resource juniors, and pudgy Jabbas like Rio Tinto and BHP will enter the fray in a big way, in fact in a much bigger way than they did in the 1990s when diamonds were discovered in Canada.

Lithium Carbonate Price Chart with AuEq and CuEq Grades for 1%-2% Li2O at $10-$20/lb lithium carbonate

James Bay Map showing 1st and 2nd Order Pegmatite Targeting Regions

Ontario Map showing distribution of Beyond Lithium's 66 properties with 500+ pegmatite showings

Disclosure: JK owns FPX Nickel and Brunswick; FPX Nickel and West Vault are Good Spec Value rated KRO Favorites, Brunswick is a Fair Spec Value rated Favorite; Beyond is Bottom-Fish Spec Value rated;

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch May 19, 2023: When losers are winners everybody losers

Jim (0:00:00): How is the debt ceiling affecting resource juniors and what might we expect if a default happens?

The resource juniors, which had a strong start during the first couple months of 2023, already faltered in March as it became apparent that China's post zero-covid rebound was not happening as vigorously as predicted, in contrast to the rebound in the United States during 2021 when the vaccine rollout began. The Chinese government target is 5% GDP growth while the IMF in its April 2023 World Economic Outlook optimistically projects 7.0% growth for China. The Federal Reserve's effort to subdue persistent inflation through interest rate hikes, even at the risk of destabilizing regional banks and triggering bank runs as depositors seek the safety of "too big to fail banks" or short term money market funds offering 4% plus yields that haven't been seen since the 2008 financial crisis, has had a dampening effect on metal prices as if a hard economic landing was inevitable in 2023. In some cases like lithium carbonate the steep decline was a consequence of the unsustainable level in 2022 courtesy of a severe supply-demand imbalance. But commodity prices, both metals and energy, have seen the gains of Q4 2022 reversed. General equity markets which on average lost 20% in 2022 when the interest rate hikes began mid year, have held their 2023 gains remarkably well, ignoring the debt ceiling crisis even as the projected June 1 date looms when the United States can no longer print new money to pay its bills. Even the US economy has ignored the approaching debt limit, continuing to add lots of jobs each month despite widespread layoffs in the technology sector. The resource juniors, however, have witnessed a distinct loss of market appetite during the past two months, despite gold spending a couple weeks above $2,000, poised to benefit on the upside if a default is actually allowed to happen.

The debt ceiling was created in 1939 as a compromise to give the United States greater flexibility in issuing new debt to pay for the war effort. It represents an arbitrary limit which Congress must increase when the national debt approaches this limit. Historically this has been a rubber stamp event with both parties agreeing to periodic increases because the growing debt represents obligations already created by legislation passed by Congress. In 2011 after the Republicans gained control of the House in the 2010 mid-terms this ritual debt ceiling was politicized when the Republican Party threatened to withhold approval of a debt ceiling increase. Failure to increase the debt ceiling would trigger a default which is predicted to have catastrophic consequences. Ostensibly the Republican Party was concerned about America's rising debt, and wanted the Obama administration to curtail spending plans. The timing was in the years following the 2008 financial crisis which unfolded under the watch of a two-term Republican administration.

Obama wanted to rebuild the American economy through fiscal stimulus aimed at infrastructure renewal with a climate change twist which today is called the "energy transition". Since the losers of the 2008 election really had nothing to lose since the president gets blamed for anything bad that happens on his or her watch, Obama decided not to call their bluff and capitulated to an agreement that limited fiscal stimulus. The task to rebuilding the American economy defaulted to the Federal Reserve which engaged in "quantitative easing" to restore liquidity to America's paper assets. Demand growth for raw materials ended up depending on China which embarked on an infrastructure building binge which ran out of steam in 2017. The result was an extraordinary bull market for bonds and equities which the resource sector sat out.

The Republicans lost the 2020 election and the Democrats managed to get razor thin majorities in the House and Senate which enabled Biden to pass the Chips and IRA bill which are focused on reshoring or friend-shoring manufacturing in the case of the Chips bill and promoting the energy transition in the case of the poorly named Inflation Reduction Act. I say "poorly named" because shifting from cheap fossil fuel sourced energy to renewables and rewiring the electricity transmission grid was never going to reduce inflation during the transition. If the measures encouraged by IRA work they significantly reduce the inflation risk that unmitigated global warming will cause down the road. But in 2022 the inflation that started to show up in 2021 during the American post-Covid rebound, which was partly caused by supply-chain bottlenecks in China where Xi Jinping had turned a zero-covid policy into a symbol of the superiority of Communist style autocracy over democracy, not only proved persistent but accelerated. Most people have a hard time imagining the value of current pain justified by the future pain that will never happen thanks to the current pain. But everybody who looks at a grocery store shelf and sees an $8 box of sugary cereal or $5 bag of potato chips that used to cost $2-$3 will know exactly what that means to them. They will probably not see the inflation caused by energy transition policies but they cannot help thinking that something called the "Inflation Reduction Act" is clearly not working for them.

The Republicans should have gained control of both the House and Senate during the 2022 mid-terms just on the back of voter unhappiness over visible inflation but because the Supreme Court tossed precedent out the window to reverse Roe and allow Republican controlled states to ban abortion, plus the party nominated Trump poodles as candidates, they failed to regain the Senate and just barely won control of the House. With the debt ceiling approaching in 2023 the Republican Party decided it was time to worry about the national debt. That worry is an absolute lie because no Republican president has ever failed to increase the national debt by a greater amount than any predecessor's term, regardless the party. The bill the House passed strives to undo the Inflation Reduction Act, in effect put the brakes on energy transition policies. This is tantamount to the loser declaring itself the winner and using a suicide vest to bully the winner into granting the loser policy making rights.

The House Bill has zero chance of being passed by the Democrat controlled Senate but serves as a starting point for negotiating the surrender of the Biden administration to the losers of the 2020 election. Whatever concession Biden makes will only hurt his party's election chances in 2024. The federal revenues for 2023 are projected by the Office of Management & Budget to be $4.8 trillion while outlays are estimated at $6.5 trillion, meaning about $1.7 trillion must be issued as new debt to cover the deficit. The debt at the end of 2022 was $30.9 trillion and is projected to be $32.7 trillion by the end of 2023. The current statutory debt ceiling is $31.4 trillion. The 2024 federal outlays are projected at $6.9 trillion while revenues are projected at $5.0 trillion, implying another $1.9 trillion deficit. The OMB projects the national debt to stand at $34.8 trillion by the end of 2024. The current Republican strategy is to approve a debt ceiling increase that does not shift the need to raise the ceiling again into 2025 after the 2024 election outcome is known. A half dozen Republican House members could decide to join the Democrats in approving a debt ceiling increase, but that would be political suicide for them, so not likely to happen. At the same time if the Democrats make concessions that allow the debt ceiling extortion to be launched again during an election year, that would be political suicide for the entire party.

The problem the Republican Party faces if it does boost the debt ceiling so that it potentially becomes its problem in 2025, assuming the Democrats retain control of the House or Senate, is that they will have to explain to voters where it will cut spending if put in charge of America's destiny. During Trump's term they cut revenues with the bogus claim that a trickle down effect will generate overall more tax revenues. Covid came along in 2020 as a major cause of new government spending, leaving Donald Trump with a record $5.1 trillion national debt expansion for his term. Biden is on track for scoring a new record with a $9.8 trillion expansion during his term.

The elephant in the room is the money spent on American retirees. Social Security and Medicare represent 33.4% of federal spending or $2.2 trillion compared to the $1.7 trillion that workers cough up through social security and Medicare deductions from their pay checks. By 2030 the entire Boomer generation will be 65 or older. The categories of "health" and "income security" which presumably is spent on non-retirees and will include welfare, food stamps and Medicaid is 25.8% of federal spending in 2023 or $1.7 trillion. The Republicans would like less money to be spent on people under the age of 65. But when you look at the chart showing the growth of the different spending categories it is Social Security and Medicare that are the national debt growth engine. The other key categories ate national defense which represents 12.5% or $815 billion, and interest on the national debt, which is 10.1% or $661 billion in 2023. Spending in these categories will rise if a default is allowed to happen because it will allow China and its autocratic allies to become more aggressive on the global stage.

Currently the United States enjoys an unusual advantage because the US dollar is the world's reserve currency. This allows the United States to use sanctions to squeeze nations it feels are misbehaving, such as Iran, North Korea and Russia. China would like its renminbi to become a reserve currency but nations are reluctant to embrace it because of China's capital controls. Since coming to power China's Xi Jinping has reversed China's drift into a more open society and returned China to a full blown autocracy exploiting hyper-surveillance technology that would turn Hitler's Nazis green with envy. Vladimir Putin has done the same with Russia. The difference between the two is that China claims to be a communist society striving for prosperity for all whereas Russia is focused on enriching an oligarchic elite while peddling nationalist fantasies to the rest of Russia. China is the second largest economy today and the gap between it and the United States is shrinking. When Russia invaded Ukraine in February 2022 as an explicit assault on democracy, China chose to declare its allegiance with Russia. The expectation was that Ukraine would be a pushover for Russia, the United States and Europe would huff and puff for a while, but then shrug their shoulders and get on with life. This would set the stage for China annexing Taiwan, a democracy in its backyard which is economically unimportant to China but stands as a refutation of China's autocratic political structure.

Russia and China were blind-sided by two developments. First, the Ukrainian president Volodomyr Zelensky, whose prior career was that of a comedian, proved to be anything but a pushover clown. Secondly, the United States and Europe rallied to support Ukraine against Putin's invasion. More than a year later the siege of Ukraine continues with no clear end in sight, which is a problem for the United States, a segment of whose voting population favors autocracies which promote religion, homophobia, and a subordinate role for women. Allocating part of America's defense budget to support Ukraine as a way of supporting democracy and freedom does not sit well with Putin Poodles.

The world has divided into three groups over the Russian invasion. The full-blown autocracies all support Russia for self-preservation reasons. Democracies such as the countries of Europe, Australia, United States, Canada, parts of South America and southern Africa have supported Ukraine and the sanction regime imposed on Russia. But another third which includes India have declined to support the sanction regime. The Biden administration has packaged the geopolitical conflict as a showdown between democracy and autocracy, but there is an excluded middle that is thinking hard about its economic goals, is watching America as a terrible example of a democracy where the losers claim they are the winners and are able and willing to push the United States into a default that likely has immediate negative repercussions for all nations. Such abdication of responsibility becomes a Humpty Dumpty event where it will be difficult to restore the credibility of the United States.

I've created a number of graphics to illustrate the geopolitical problem looming for the United States if there is an outright revolt against the United States where countries like India, Brazil and South Africa align themselves with China, which in turn is exploiting Russia's weakened hand to pull central Asia, former involuntary members of the Soviet Union, into its fold, and will likely out-compete Russia's Wagner mercenary group in Africa. I have created several heat map graphics to show the balance between the China-America great power conflict now underway. One is a population heat map which shows the concentration of people in Asia, primarily India and China. Others include heat maps of GDP and defense spending, which shows the geographical balance between China and the United States. There is also an official gold reserve heat map, but I believe it understates China's true gold holdings which need not be inside its central bank. I've created a graphic to show that if Chinese state owned entities have been buying gold, the actual holdings at Xi Jinping's disposal nearly match of those of the United States.

I've also created two heat map versions of political and civil freedom data compiled by Freedom House. Freedom House has a political rights and civil liberties scoring system that generates two scores which are added to create a "total freedom" score where 100 is the top freedom score. That graphic shows darker colors in areas with more freedom. Freedom House also has a matrix which allows it to combine the separate scores for civil and political liberty into three groups of "free", partly free", and "not free" to which I have assigned numbers 1, 2 and 3 so that the heat map color is darkest where least free. I've also provided the graphic which shows what percentage of each metal comes from China and Russia combined to illustrate what I see as a major looming problem if this widening geopolitical split demolishes globalized trade.

Whether or not the United States lets the debt ceiling problem cause it to default on its obligations, this over-arching geopolitical conflict can only worsen. It is just a matter of how quickly the actions of American politics accelerate the division of the world's economies into China aligned or America aligned. While the United States can inflict serious wounds upon itself, it will take a long time for it to become just one of many high GDP countries with little influence on affairs elsewhere in a world which currently is itching to migrate away from reliance on the US dollar as a trade currency vulnerable. The immediate affect of this trend should be higher demand for gold, which would benefit Canadian resource juniors. Despite gold trying to establish $2,000 as a new base for future upside price moves rather than a ceiling it cannot definitively break through, investors have not shown much interest in accumulating ETF gold such as the World Gold Council backed GLD. So who is buying physical gold that kept it above $2,000 for much of May until the past week? One explanation has been that central banks from the partly free and not free nations have been buying gold as a way to diversify away from the US dollar as a reserve currency. In terms of total official sector gold holding the gain in 2022 was actually smaller than for much of the past decade which shows consistent central bank accumulation of gold. The lower net growth is due to some nations being forced to sell gold to deal with their financial problems which offset a demand surge by other nations. If the United States defaults on its debt and yields for US treasuries soar, we can likely expect more central banks to increase their gold holdings. Once that becomes a visible and sustained trend we can expect broader audiences to buy gold and create a real price uptrend.

For the resource juniors an even more important benefit than a gold price rising well beyond $2,000 will be the collective realization that Canada is well endowed with many of the critical minerals needed for energy transition related technologies (as well as metals with more mundane applications) of which lithium is the most pressing metal today. While the focus is generally on how Canadian mine production can supply America's future needs, one should not forget that Europe, in so far that it resists alignment with the China-Russia axis, could be an important source of demand for responsibly mined metals. By Q3 of 2023 we should know the outcome of the debt ceiling debacle. Either a default has happened and we see what damage to the economy and markets it has caused, or it will have resolved itself without a catastrophic outcome. In either case the dread of what might happen will be gone and markets can adapt to a new reality.

TSXV listed resource junior traded value has declined since April

Metal and Energy Prices have declined thanks to weak China post zero-covid rebound

Interest rates still rising as inflation rate slowly eases

US Non-Farm Jobs at Record High

IMF projected distribution of 2023 Global GDP

General Equity Market seems unconcerned by Debt Ceiling Problem

A Visual History of National Debt Growth

Federal Revenue Estimate for 2023

Federal Spending Estimate for 2023

2023 Spending Amounts for each Federal Category

Federal Spending Projection through 2028

The Global Geographical Balance between United States and China

Global Distribution of Freedom

The China-United States Collision Trajectories

The Metal Supply Problem facing Democracies if Globalized Trade Collapses

China is the world's biggest gold producer: where did its domestic gold supply end up?

A History of Annual Official Sector Gold Holdings Changes

Daily Changes in the GLD Gold Holdings

Jim (0:11:23): What are the implications of the recent Mexican mining law changes for juniors like Sonoro Gold?

On April 29 the Mexican Senate jammed through a couple constitutional changes unrelated to the mining sector and a new mining law. This was accomplished by members of the ruling Morena party secretly gathering in another chamber to put the proposals to a vote while the opposition was gathered in the main chamber to protest the proposed rule changes. Last year Mexico's president nationalized the mining of lithium, effectively stripping owners of mining concessions with lithium potential from having the right to develop and mine lithium. The result has been that exploration for lithium in the form of claystones, brines or pegmatites simply stopped. Now the government is trying to come up with a system that will attract exploration and development capital of the sort juniors typically bring to the table. Chile's leader Gabriel Boric recently proposed a change which would give Chile a major stake in all new brine projects. The Chilean system was already messed up due to the government's excessive role in granting production leases. Some juniors have claimed that greater clarity will get things moving for the Chilean portion of the Lithium Triangle, but for now Chile's state copper mining entity has been instructed to study how to best take a higher stake in existing brine operations and figure out what the investment and title regime will be for undeveloped lithium projects. However, because the proposed Chilean change must get approval from another government branch, it may be quite some time before anything is formalized. In the meantime, all Chilean brine projects not already in production are in limbo. This has helped spotlight why Argentina is a better jurisdiction for developing brine projects and it has given brine producers like Albemarle, SQM and Wesfarmers extra reason to look at supply expansion through pegmatite lithium projects. Chile's foolishness may turn out to be of great benefit to Canadian juniors engaged in Lithium Mania 2.0 exploration in Canada. The Mexican mining law change may also boost the fortunes of resource juniors with a focus on Canadian projects.

The first implication of this Mexican mining law change is to create a period of limbo. Because of the manner in which the laws were passed it will be challenged to the Mexican Supreme Court which has resisted Andres Manuel Lopez Obrador's efforts to undermine Mexico's democratic institutions. Amlo is a populist like Trump but chases left wing goals such as more state control of everything. His term ends in 2024 so he will not be in a position to claim the election was stolen. But like Vladimir Putin and Xi Jinping he will do his best to get the rules changed so that he can stay in power beyond the current 6 year term limit. Because of the urgency of the matter a court decision could be in hand within a couple months.

Amlo has been pushing for mining law reform for some time, arguing that the existing mining concession system is too generous. In countries like Canada mineral title is established by staking open claims, online in most provinces through map-staking. There are staking fees and assessment work reporting requirements to keep the claims alive. Countries like Mexico have a claim application system where a company or individual must file a request for a land package. Once the application has been made nobody else can apply for those claims which are either confirmed as a mining concession or not. These mining concessions have a 50 year term. As a result Mexico is checkered with existing concessions covering most prospective geology. Canadian companies have typically done deals on these claims so that they can explore and develop them if an orebody is outlined.

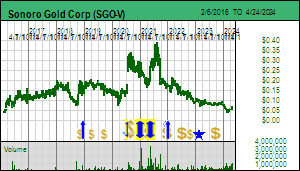

Sonoro Gold is an example of such a junior which has done deals with the mining concession title holders in the area of the Cerro Caliche project in Sonora State. These deals require Sonoro to pay USD $4.9 million by March 2024 of which $3.5 million has already been paid since 2018. Over 57,000 m have been drilled to delineate an indicated and inferred resource of 30,450,000 tonnes of 0.43 g/t gold which at $2,007 gold represents a rock value of $31 per tonne. That's just over 400,000 ounces gold. Sonoro delivered a PEA in September 2021 for a 15,000 tpd open-pit heap leach operation which it updated in May 2022. The mining plan involves several shallow open pits which represent only a portion of the known mineralized zones on the property. The resource supports only a 6-7 year mine life, which is normally a deal-breaker because nearby communities, when they support a mine in their backyard, want a longer mine life to sustain the local economy. However, Cerro Caliche is within an established mining district, there are no nearby communities, and the mineral title has been secured from the local surface rights holders. This has allowed Sonoro to adopt a strategy of designing for a larger scale operation with the goal of using cash flow to fund delineation drilling of additional zones to extend the mine life. For example, I've done an outcome visualization for 75 million tonnes of ore that would yield about 700,000 ounces over 14 years.

This is a low sulphidation epithermal system with gold smoke all over the place, and which, while it has yielded some high grade ore shoots, has not yet yielded deeper higher grade veins such as the Mercedes vein being mined next door by Bear Creek Mining after acquiring it from I-80 Gold. The problem for a junior is that it cannot afford to drill off a 20 year mine life backed by a feasibility study, especially during a bear market and with a gold system whose average grade is at the lower end of what is generally put into production. Sonoro has chosen to seek debt financing supported by a PEA with the argument that at current gold prices not only will lenders be paid back, but there will be sufficient cash flow for reinvestment in expansion drilling and scaling up production down the road with a 1-2 million ounce scenario a plausible outcome. With that goal in mind Sonoro submitted a mine permit application in May 2022.

Since 2018 when Amlo was elected no new mining concessions have been granted. Back in late 2021 Sonoro was confident it could have a mining permit in hand within 6-8 months of application. It is 18 months later and there still is no indication when a mining permit will be granted. Sonoro cannot secure project financing until mine approval is in hand. The COO Jorge Diaz who has put numerous Mexican mines into production has observed a distinct slowdown in the approval process from what he was accustomed to. Part of the problem is that during the covid pandemic bureaucracies such as Semarnat (Scretaria de Medio Ambiente y Recursos Naturales) slowed down activities substantially and lost competent personnel.

At the other end of the regulatory system no new mining concessions have been granted because Amlo wanted to reduce the concession term from 50 years to 15 years. That was a non-starter for the mining industry because any new concession application will be of a grassroots, generative nature where you can spend at least 5 years to be in a position to make a production decision, if you are lucky with exploration early on, at least another year to get mine approval, and then a couple years to build and commission the mine assuming you don't have to sit out a metal price bear market before you can secure CapEx funding. Nobody is going to bother with grassroots exploration if the best outcome is a 7 year mine life. As a result of industry feedback Amlo agreed to a 30 year concession term with a 15 year renewal.

Since Sonoro is paying to acquire existing concessions whose terms are grandfathered, the new concession rules are irrelevant to this Canadian junior with an advanced project in Mexico. But they are deadly to the type of junior that styles itself as a prospect-generator-farmout type. An important change to the concession granting process is the first come first serve principle has been abolished. Any concession application submitted by a party will be made available for anybody under an auction system where the highest bidder is awarded the concession. This makes sense when a land package within a government mineral reserve is being offered for exploration and development to third parties, but not when somebody has applied geological creativity to identify an area as prospective. An earlier version of the mining law reform included a requirement to describe what metals one hoped to find and how much. There was even a plan for the concessions to be metal specific. So if you have an idea for a carbonate replacement type deposit, which would be rich in silver, lead and zinc, you would need 3 concessions to be able to profit from mining all three. Common sense prevailed and these requirements were scrapped. But if this new mineral concession system is adopted, grassroots exploration will be limited to existing mineral concessions.

The big mining companies like Gruppo Mexico, Penoles and Fresnillo have indicated there are no implications for their existing mines, and their landholdings are large enough to offer plenty of greenfields and brownfields exploration potential. Furthermore, when Canadian resource juniors lose interest in Mexico the existing mineral concession holders with grandfathered rights will be easier to deal with. The new mining law does include tougher water usage scrutiny. Until now if a mining company secured water rights from an existing holder it would simply start using them. Now the plan to use water for a mining operation must undergo a study in terms of its impact on the basin from which it will be drawn. Since most mines use a relatively small portion of the water available in a basin the thresholds that would trigger a denial are unlikely to be hit. But the permitting cycle now has an additional study and approval layer. In the case of Sonoro it has secured water rights so this simply means extra studies. The main negative implication of this mining law reform for Sonoro is the uncertainty about when it will become law. The permitting department is not going to speed up processing until clarity has been achieved. If the Supreme Court strikes the mining law down on procedural grounds, Amlo will simply try to change the mining law in another manner. That means further sluggishness in the permitting department.

Sonoro Gold Corp is dealing with the situation by doing a private placement of 30 million units at $0.10 with a full 2 year warrant at $0.15. Insiders will take down a third of the financing to help pay loans Sonoro secured to make property payments due earlier this year and accumulated exploration expenses. Enough money will be set aside to take care of remaining payments this year, though more will have to be raised for the final Q1 2024 payments that secure title, something project lenders will insist on. A portion of the financing will be spent on drilling the western trend defined by the Cabeza Blanca, Guadalupe and El Colorado Zones where more recent drilling has intersected high grade shoots whose grades SRK Consulting capped at 3 g/t gold. The goal is to better flesh out these zones so that the resource grade can be boosted for the starter pits in the proposed mine life. So even if the mining law uncertainty drags on in Mexico Sonoro will be in a position to improve the Cerro Caliche project from the perspective of the project lenders waiting in the wings.

The financing does add 60 million shares of dilution, boosting fully diluted from 232 million shares to 292 million shares. However, 55.6 million warrants at $0.30 expire by the end of 2023, 38.6 million on August 12 and 16.9 million on Dec 20. The first batch was done in September 2020 when the covid response launched gold above $2,000 for the first time. A major participant was Pallisades which embraced a strategy of clipping the warrant and flipping the stock as soon as it became free trading. It did this with most of the juniors it bankrolled during that frenzied financing period. In another 7 months the free-lunchers will have no stake left in Sonoro and the overhang that remains will be in the hands of shareholders who invested in 2021 when the gold market had cooled and who were investing in the Sonoro team's plan to fast-track develop a gold mine that would benefit from a rising gold price. Sonoro will have 236 million shares fully diluted with the dilution held mainly by parties who understand the development dynamics of this story which will become much easier to appreciate when $2,000 becomes the base for gold's future price rather than its ceiling.

Chart showing what percentage of each metal's global supply Mexico provides

Chart showing what percentage of each metal's global supply Chile provides

Sonoro Gold's Cerro Caliche Resource

Sonoro is led by a very tenacious, experienced team

Current grade expansion focus and future expansion target area

Sections showing the high grade potential of the western trend

Sonoro's Cerro Caliche Timeline plus warrant and property payment details

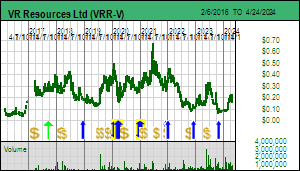

Jim (0:28:03): How important is the latest news from the Northway diamond project of VR Resources?

VR Resources Ltd announced on May 18 2023 that the second hole drilled at its Northway project encountered 117 m of diatreme breccia between 240 and 357 metres. The hole had to be stopped because of excessive caving at the unconformity between the kimberlite and the mudstones that filled the hole excavated when the kimberlite erupted 400-450 million years ago. Hole #2 was spotted dead center of a 1.2 km wide magnetic low anomaly 450 m to the northwest of hole #1 drilled last year and reported on February 22, 2023. KW Episode March 10, 2023 provides background about the potential implications of this discovery. Northway was a large untested magnetic low anomaly in the James Bay Lowlands of Ontario where a 400 million year old limestone platform covers the 2 billion plus year old basement rocks. Hole #1 yielded only 40 m of what has been described as kimberlitic material and was spotted near the edge of the circular anomaly because the initial model was that this was a carbonatite like Hecla-Kilmer or some other alkaline intrusive complex with IOCG potential such as Roanoke that was prospective for copper and gold. Typically the outer ring of such intrusions has the best chance for copper mineralization.

VR's Mike Gunning and Justin Daley were quite surprised by what they intersected last year and eventually decided it was a kimberlite though petrographic studies confirming the origin depth of the magma were not done, nor was any of the initial hole submitted for caustic fusion to recover micro diamonds because the sample was so small. VR quietly staked a couple dozen other untested magnetic low anomalies within a 30 km radius management realized that the Northway diatreme was a magnetic low because during its emplacement the earths magnetic poles were reversed relative to the Precambrian basement rocks (when a magma cools the magnetite crystals will align according to the polarity of the poles at the time, which doesn't mean they are more magnetic than the country rock, but simply end up a reversed polarity that shows up as circular anomalies in a magnetic survey). The exciting hypothesis was that after the limestone was laid down about 450 million years ago something triggered a wave of magmatic intrusions which burst through the limestone creating a cluster of kimberlite pipes. All those other magnetic lows could be a cluster of kimberlite pipes which avoided detection because they erupted into a marine environment. The craters were subsequently filled with marine sediments. As a result no kimberlite outcropped anywhere and was exposed to glacial activity which gouges out the softer kimberlite and creates the indicator mineral trains explorers track back to their origin through till sampling.

VR was able to raise $1.9 million through a private placement that closed in April, attracting some investors intrigued by the potential for a new diamond field in Canada. The market reacted strongly to the news despite an overall lacklustre market because the intersection confirmed that the geophysical interpretation was not an illusion, that the anomaly represented a 1.2 km wide intrusive body with a footprint of 500 million to 1 billion tonnes to a depth of 300 metres. It is unlikely that this is a single kimberlite intrusion, but rather multiple intrusions such as is the case with the world class Jwaneng pipe in Botswana. It is disappointing the hole could not be drilled deeper, but it is very positive that it obtained fresh rock beneath the altered crater facies material at the unconformity. VR has published core photos which certainly support the interpretation that this is a kimberlite. The sample is also large enough to allow a characterization study to be done that establishes the origin depth of the magma and the garnet bearing xenolith entrained during the ascent. The next important step is confirmation that the magma originated beneath the diamond stability field between 150-200 km where diamonds would have formed.

The sample is also large enough to allow part of it to be submitted to SRC for caustic fusion to recover micro-diamonds. The diamond bearing potential remains a critical obstacle because Northway occurs within the Kapuskasing Structural Zone which developed between 2-1 billion years ago. The resulting thermal event spawned the carbonatite and IOCG style intrusions in the James Bay Lowlands, but it would also have wiped out the diamond stability field, converting any diamonds that formed during the older Archean period into graphite. For the Northway cluster to be diamondiferous conditions would have had to be right to allow diamond populations to form after the thermal event subsided. The diamond population of the depleted Victor Pipe to the northwest several hundred kilometres is an example that is less than 1 billion years old. Micro diamond results with a coarse distribution supporting prediction of a macro grade will be an important next step, though not necessarily a death blow for Northway because the Victor pipe almost never became a mine because the micro diamond portion of the population was not observed in early drill core. Furthermore, with such a large intrusive complex there may be multiple phases representing a broad range of diamond content. VR will need to test a lot more than one drill hole pin-prick into Northway before it can conclude that it is a diamond bust. But if we get early confirmation that Northway is a true kimberlite, that the xenoliths contain garnets exclusively associated with the pressure-temperature regime of the diamond stability field, and ideally that a coarse micro diamond distribution is present, it would create the basis for testing all the other blind magnetic low anomalies. We will likely have to wait 2-4 months to get the petrography and micro diamond results. Meanwhile VR is moving the drill back to Hecla-Kilmer to delineate more of the rare earth zone, and in the fall it hopes to be in a position to drill the New Boston copper-molybdenum prospect in Nevada.

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch May 12, 2023: James Bay gets a Lithium Champion

Jim (0:00:00): What are the implications of the proposed Allkem-Livent merger for the James Bay region?

On May 10, 2023 Allkem Ltd and Livent Corp announced a merger of equals whereby Livent shareholders will get 2.406 Allkem shares with the resulting company trading on the NYSE and the ASX. The TSX listing will disappear. The combined company had a value of USD $10.6 billion when the deal was announced, which has since risen because both stocks responded positively to the news. Pro-forma 2022 revenues would be USD $1.9 billion and EBITDA would be $1.2 billion. This merger combines the Argentine brine operations of both companies and the Australian Mt Cattlin pegmatite mine of Allkem. The Argentine portfolio has expansion potential and includes one project under construction. But the real synergy comes from the Quebec James Bay project of Allkem and the 50% owned Nemaska project of Livent.

The Nemaska project consists of the Whabouchi deposit which was developed during Lithium Mania 1.0 but ended up in bankruptcy in December 2019 when lithium carbonate prices had crashed below $5/lb. In October 2020 Orion Mine Finance and The Pallinghurst Group acquired 50% of the asset and a government agency called Investissment Quebec acquired the other half. Livent acquired a partial stake on Dec 1, 2020 and on June 6, 2022 Livent issued 17,500,000 shares to acquire the other 25% to hold 50%. Livent and IQ are working to bring Wabouchi on stream and are building a lithium hydroxide facility at Becancour on the St Lawrence River half-way between Montreal and Quebec City. Livent, which was part of the FMC Corporation, went public on the NYSE by IPO in 2018 with the Hombre Muerto brine project in Argentina.

Allkem went public in 2007 as Orocobre and by 2015 had put the Olaroz brine project into production. In August 2021 it diversified into pegmatite sourced production by acquiring Galaxy Resources. Galaxy had put the Mt Cattlin deposit into production in 2010 and in 2012 acquired Lithium One which gave it ownership of the Sal de Vida brine project in Argentina and the Cyr pegmatite project in the James Bay region of Quebec. Allkem published a feasibility study in December 2021 for the Cyr project which it now calls the James Bay project. Last week Allkem published partial results of drilling it has been doing at James Bay which revealed the discovery of the NW Sector. It is an under-cover jog to the northwest for the existing Cyr deposit which has a Li2O grade in the 1.5%-2.0 % compared to the 1.3% grade of the largely outcropping main deposit. It also reported extensive drilling activity to the east right up to the boundary of Brunswick's Anatacau West project but did not report any assays. Brunswick has traced the pegmatite system at least 300 m onto its property and is awaiting assays.

The merger between Allkem and Livent is important for the James Bay region because future spodumene concentrates from both James Bay and Wabouchi can be shipped to the Becancour lithium hydroxide refinery which in turn can supply battery makers based in North America. Allkem-Livent, or whatever the merged company ends up being called, will be a potential aggregator of new lithium discoveries in the southern half of the James Bay region if another major lithium producer does not show up. The James Bay region can be divided into a southern half south of the Eleonore Gold Mine and the northern half where Patriot Battery Metalsis drilling off the Corvette lithium deposit whose results so far indicate a world class resource potential in the 50-100 million tonne range grading 1.5%-2.0%. That puts it in the league of deposits such as Liontown's Kathleen Valley which are currently priced in the $4-$6 billion range.

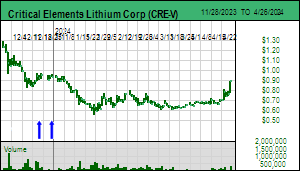

The lithium pegmatite deposits in the southern half of James Bay such as Cyr, Rose, which is owned by Critical Elements Lithioum Corp, and Whabouchi were found 3-5 decades ago because these pegmatites outcrop to such a degree you can see them from Google Earth satellite imagery. Simply walking the ground and looking for outcropping pegmatites that are lithium enriched is what I call "first order" exploration. The southern half is now regarded as an old exploration frontier because it is assumed that the best pegmatites are those that are sticking out of the ground. The exciting new exploration frontier is the northern half where outcropping pegmatites such as within the Corvette trend were observed during the past couple decades, but because of the remoteness they were never delineated. Plus the global lithium market was tiny and dominated by production from Greenbushes and the Chilean brines. Lithium Mania 1.0 kicked off in 2015 when Tesla EV sales took off and the world realized that electric vehicles powered by lithium ion batteries were becoming a reality. Lithium Mania 2.0 is based on projections by groups such as the IEA that lithium supply will need to undergo a 600% expansion by 2030 to make EV rollout projections reality. James Bay is turning into a Great Canadian Area Play because it is a prime candidate in a secure and stable jurisdiction to deliver the second half of the required supply expansion.

While the exploration glamour resides in the northern half of James Bay where simply first order walking the ground with an XRF gun this summer could lead to high success potential drill programs in the fall and certainly by Q1 of 2024, the southern half has been viewed until recently as an also ran. But the realization has started to set in that the known deposits may simply be the result of local topographical coincidences which created a tunnel-visioned exploration focus. The Allkem feasibility study at James Bay should have had a pit centered on the higher grade NW Sector, but the past delineation drilling focused on what was visible. This old frontier is undergoing a renewal in the form of "second order" exploration which seeks to home in on pegmatites close to surface but obscured by swamp, bush and overburden. Lake bottom sediment data, glacial history reconstruction, and geology are the keys to second order exploration. An early example of a second order discovery was the Pontax pegmatite system now being explored by Cygnus Metals and Stria Lithium. It was discovered a couple decades ago by Sirios Resources as a by-product of regional till sampling for diamond indicator minerals spawned by Ashton's discovery of the Renard kimberlite cluster.