| Kaiser Watch October 13, 2023: What is Gina's Liontown Plan? |

| Jim (0:00:00): What is new in the world of lithium? |

Lithium carbonate prices, which hit $10.42/lb on Sept 26, have started to bounce off a bottom, reducing fears that the price would crash into the $5-$10 range. It does not appear that there has been a substantial boost in demand, for the reason behind the uptick seems to be that refineries whose lithium concentrate feed is purchased under long term contracts are now starting to lose money converting the concentrate into battery grade lithium carbonate not sold to battery makers at long term contract prices. So they are cutting back on production which is reversing the lithium carbonate price decline. The spot price for 6% lithium spodumene concentrate, which ranged $5,000-$6,000 per tonne in 2022 until starting to decline in March 2023, is now at $2,325 per tonne and not yet showing signs of a reversal. In fact, if it is true the refineries are cutting back on concentrate conversion, the concentrate spot price will continue to weaken. So far the hopes that China's Golden Week celebration would stimulate domestic consumption have not yet turned into reality.

Meanwhile, the rest of the world, in addition to worrying about the economic impact of persistent high interest rates chasing a 2% inflation target which encourages hunkering down in 5% plus risk free instruments, be they short term treasuries or term deposits at the bank, is now fretting about what the Israeli response to the Hamas terrorist attack will do to disrupt global supply chains and further fuel inflation. These are concerns that discourage consumption and help explain why Chinese caution is spreading globally. But they are irrelevant to the energy transition, which in the Global West is being pushed to restrain greenhouse gas fueled climate change, and, in the oil supply deficient parts of the Global East and South, is being pushed to help escape the tyranny of the world's biggest old producers: the United States, Saudi Arabia and Russia.

Dialing back from this big picture hand-wringing, the recent focus of lithium stock investors has been the optics of lithium carbonate prices bouncing off $10/lb, possibly back to $20/lb, rather than crashing into the $5-$10/lb range and spawning fears of another 2018-2020 style lithium winter when it crashed below $5/lb. My counsel is to ignore the lithium carbonate spot price. I continue to be of the view that exploration for LCT-type pegmatites should seek 1%+ Li2O deposits which can be profitably mined in the $5-$10/lb range. No new discovery will be in production before 2030, so the focus should be on finding 1% plus Li2O deposits and, if you want to be religious, praying that a Direct Lithium Extraction (DLE) technology breakthrough with unlimited scalability that drops the unit cost well below $5/lb lithium carbonate never happens. That scenario is the bugbear of Lithium Mania 2.0, which is the focus on LCT-type pegmatites to supply the bulk of the world's future lithium needs.

The first week of October, which was also Golden Week in China, was pretty grim for lithium companies in general, but Liontown Resources Corp was an exception. This week we found out why. After Albemarle presented Liontown with a revised AUD $3.00 per share offer on September 4 conditional only on due diligence, Hancock Prospecting, a private company owned by Gina Rinehart that specializes in iron ore mining but is diversified into a lot of other areas, filed a notice of becoming a substantial Liontown shareholder on September 11, following a purchase of 59,281,147 shares on September 7 at an average $2.98 price. On September 11 Hancock owned 169,914,764 shares or 7.72%. While other lithium companies retreated since then, Liontown has held up well because Hancock has continued to buy in the open market.

On October 11 Hancock reported that it had reached 19.9% with 438,248,862 shares. A day later on October 12 Liontown announced that it had granted a 7 day due diligence extension to Albemarle which presumably now has until the middle of next week to make a decision. So you might ask, why, with lithium carbonate prices finally bouncing off a bottom, and Gina Rinehart owning 19.9% of Liontown at close to a $3 average price, has Liontown's share price sagged to $2.79 in the past couple days? One explanation could be market concern that next week we will find out that Albemarle has decided to walk away from acquiring Kathleen Valley, which would be definitive because the recent proposal indicated the $3 offer would be the final offer, which means Albermarle cannot manipulate the Liontown stock price by playing games. Such an outcome would make Australia's richest woman look like a doofus.

Since it is hard to imagine that the woman who expanded her father's iron mining business into a colossus is a doofus, there is an alternative explanation with interesting implications. Under Australian rules if a third party acquires 20% or more of a company it is required to make an offer for 100% of the company (according to a recent FT LEX comment). The market expectation is that Hancock will not exceed 19.9% but will instead vote against the plan of arrangement if Albermarle decides to go ahead with acquiring Liontown at AUD $3 per share. For the acquisition to become reality it must receive 75% of votes cast, and, while Hancock doesn't have the 25.1% stake needed to prevent approval, the reality is that most shareholders don't bother voting their shares, so if just under 80% of Liontown's 2.2 billion shares are voted in favor of the deal, Hancock can still kill the deal with its 19.9% stake. Albemarle's extension request is ostensibly about needing just a little bit more time, but in reality it is so that it can work out a deal with Hancock to secure a yes vote, and since the stake was bought close to the offer price, such a deal would require a better offer.

The two main potential outcomes are that Albermarle increases its offer to a level that secures the vote of Hancock, or Albemarle has to walk away. That would pave the way for Hancock to make its own bid for Liontown, not necessarily at a higher price, but one that is unconditional and perhaps done in conjunction with a partner. The slightly sagging price of Liontown reflects market uncertainty about how this will play out. The most important question right now is, "What is Gina's plan?" The big picture implication, however, is that deep-pocketed players are valuing Kathleen Valley at minimum USD $4 billion, despite the recent lithium carbonate price declines. |

Liontown Resources Ltd (LTR-ASX)

Unrated Spec Value |

|

|

| Kathleen Valley |

Australia - Western Australia |

8-Construction |

Li Ta |

Albemarle Corp (ALB-N)

Unrated Spec Value |

|

|

| Greenbushes |

Australia - Western Australia |

9-Production |

Li |

Price Charts for Lithium Carbonate, Hydroxide and Concentrate |

Pie Chart for Sources of 2022 Oil Supply |

Liontown Purchase History by Gina Rinehart's Hancock Prospecting Group |

| Jim (0:10:35): What are the implications of the various Liontown outcomes for the James Bay Lithium Area Play? |

Albemarle has a 49% stake in Greenbushes with Tianqi holding the other 51%, and it has a 60:40 JV with Mineral Resources Ltd in Wodgina, both producing mines, so Albemarle already has meaningful pegmatite sourced lithium supply in Australia. Not to be taken lightly, Albemarle is an American company, not like Rio Tinto which is sort of Australian but has no meaningful pegmatite based lithium stake. A big question is whether Hancock is merely trying to squeeze Albemarle into offering a higher price so that the binge buying during the past month turns into a nice short-term profit (Gina messing with the big boys), or if Hancock it is in fact trying to muscle Albemarle aside and turn itself into a major lithium supplier by acquiring Liontown and its Kathleen Valley project which will be in production in mid 2024?

The preferable outcome for Lithium Mania 2.0 is that Hancock expands from iron mining to include mining pegmatite deposits for lithium. I believe the IEA projection of a 600% lithium supply expansion needed by 2030 to fulfill the EV deployment part of the 2050 net zero emissions goal will happen regardless what people thing about the efficacy of global warming mitigation measures. I also believe that Toyota's solid state lithium ion battery breakthrough is commercial not just for the high end models it plans to sell by 2027, but ultimately also cheap enough for its affordable and popular Camry and Corolla models. If a solid state lithium ion battery becomes reality, it will be because of manufacturing efficiencies, not a decline in the price of the critical mineral inputs. In that case we may need 12 times as much lithium supply by 2035 compared to the 130,000 tonnes of lithium metal equivalent produced in 2022.

Unless there is a miracle breakthrough in direct lithium extraction that opens up an unlimited supply with a cost well below $5/lb lithium carbonate, that future lithium supply market will be worth $100-$200 billion, the same league of aluminum, gold and copper, though not as big as iron whose output was worth $312 billion in 2022. Barring the DLE miracle, the bulk of future lithium supply will come from pegmatite deposits. Rio Tinto has already recognized the future importance of lithium, but other major western mining companies have not. If Hancock were to acquire Kathleen Valley it would be just the start of the miner expanding into lithium production while biggies like BHP and Anglo American pick rust out of their noses, one more major with lithium supply growth ambitions. The more majors looking for a serious chunk of a future $200 billion annual lithium market, the better for the juniors looking for LCT-type pegmatites in the James Bay region.

If Hancock's strategy is merely to grind some chump change out of Albemarle, then the only implication for the James Bay region is that Liontown shareholders will end up with over AUD $6 billion cash to redeploy elsewhere, and the best emerging destination is the James Bay region of Quebec where Albemarle already has a 4.9% equity stake in Patriot Battery Metals Corp, owner of the world class CV5 deposit. Regardless how the Liontown story plays out, it should send a new flood of money and interest into the James Bay region to which ASX-listed companies are already flocking.

The James Bay region suffered a serious setback this year thanks to the forest fire closures which prevented access to most of the region during June through August, a key prospecting season for boots on the ground. Some areas such as the Mia and Radis projects of Q2 Metals Corp and Ophir Gold Corp had even less time because they were off limits during the moose hunting season that runs September 15 to October 15. Those companies got in only a couple weeks in the field before having to leave. Logistics, however, was a problem even for those juniors with properties in areas that opened early andf were not impacted by moose hunting season. As a result very few companies will be in a position to drill meaningful targets in Q4, and even Q1 will not see anywhere near the number of drill programs that a full 2023 summer prospecting season would have made possible. For those of us who embraced Lithium Mania 2.0 last year, this is an annoying delay, but for those on the sidelines, perhaps wondering if they missed the boats, the sight of boats returning to the dock is a joy to behold. I was not wrong, just early and only because I was blindsided by the forest fire closure, which only the dumbest bag of hammers refuses to link to climate change.

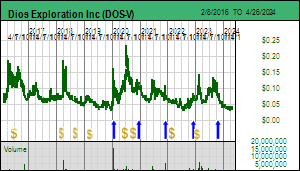

Take the example of Dios Exploration Inc which this week provided an update about its Lecaron project which left the market cold. The junior's third party contractor was able to visit four of the five property groups, but spent only 14-21 days in the field. At Lecaron this resulted in a 50% expansion of the claim package after the geologist led team observed prospective geology not indicated by the government maps. But there were no reports of spodumene observed in outcrop at Lecaron. Samples were collected and sent for assaying, but there was no mention about using a LIBS or XRF to determine the LCT-type nature of outcrops. Dios won't have the assays until November though by then it will be too late to go back into the field, especially if this year's prediction of an early winter proves correct. The press release didn't mention the number of samples, but management told me that about 200 outcrop samples have been shipped for assaying, which is an impressive number, though management did not know how many outcrops these came from. Management also told me that much of the area prospected turned out to have heavy bush cover and there simply wasn't enough time to assess the scale and continuity of pegmatite outcrops, which of course you don't want to waste time on before you know it is an LCT-type pegmatite. The bush cover problem is not a surprise, because the Dios properties are what I call "second order", meaning that they are being generated by a combination of datasets, including a proprietary database from the diamond indicator mineral till sampling days of Dios in the 2000's which the company has used to vector into prospective areas. These are not geologically obvious areas which have seen intense exploration for precious or base metal deposits, and while pegmatite showings have been documented, they are not highly visible in satellite imagery. To assess these second order prospects requires a full summer prospecting season, which Dios was not able to undertake. After enduring the lost summer of 2023, the market has no patience for so-so descriptions about boots on the ground efforts.

The glum reaction among KRO members who are Dios shareholders was "oh, dead money until the summer of 2024". That isn't a fair reaction, because once Dios has assembled and published everything it has learned about its 5 claim groups, there will probably be a positive market reaction, especially if drilling activity by some juniors has confirmed significant new discoveries. My James Bay Lithium Index membership is now up to 69 companies, with new additions mainly by ASX listings which acquired claims or options during the past 5 months. The Australian resource junior interest in James Bay keeps growing; Dios CEO Marie-Josie Girard tells she is getting plenty of inquiries from ASX listings seeking to option a property. But until she has a better understanding of the potential based on the short sampling season in September, she is not considering farmouts at this stage.

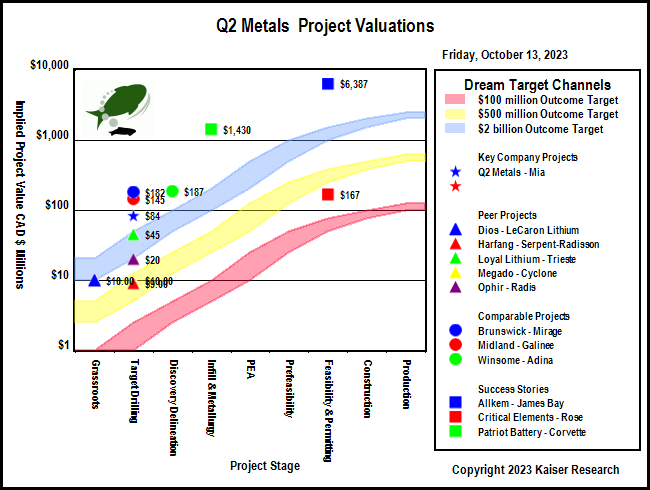

Without question, however, the market's attention is shifting towards drill intersection based confirmation of grade and scale of an LCT-type pegmatite outcrop. Who is on track to deliver the next PMET CV5 discovery over the next year? All eyes are now on Brunswick Exploration Inc which is busy drilling within its 850 m by 2,700 m corridor of spodumene bearing outcrop at Mirage with preparations already underway for a winterized camp that will allow drilling to resume in January 2024.

With regard to drilling expectations, consider the plight of Ophir Gold Corp whose Radis project I discussed in KW Episode September 1, 2023. Ophir and its neighbor Q2 Metals Corp got in only a few weeks of prospecting before they had to quit for First Nation moose hunting season. The Mia project of Q2 Metals is more advanced, so the targets were already sufficiently developed to allow a meaningful drill program. Q2's stock price has held up because on October 16, the day after the end of moose hunting season, it will mobilize a drill rig to the property. Ophir, which last week published an Update about its brief sampling efforts at Radis which continued to support the potential for meaningful LCT-type pegmatites, and certainly read more promising than the sparse Dios news release about Lecaron, saw its stock get hammered from the $0.30 plus level below $0.20 when the market realized that there would be no drill program in 2023. However, CEO Shawn Westcott tells me that their target is sufficiently developed to justify a drill program in late January 2024 which will stage out of the winterized camp Q2 Metals is preparing at Mia. And Ophir has a $5 million treasury so that it doesn't have to go begging to the brokerage sector later this year when it is recommending dumping all its former picks for tax loss purposes.

The challenge at Q@ Metals' Mia is the same challenge Brunswick has at Mirage. What is the sub-surface orientation of the outcrops, is it an en echelon series of parallel dykes like at Allkem's Galaxy-Cyr project, or elongated bodies like with PMET's CV5 pegmatite? And what is the dip so that one can convert the outcrop's surface width into true width and start estimating tonnages? Ophir will benefit from whatever Q2 learns drilling at Mia in October-November, and if Q2 delivers confirmation of a discovery, the market will no doubt turn its attention to Ophir Gold because right now the market is assigning an $84 million value to Mia but only a $20 million value to Radis. The Q4 bottom-fishing season for James Bay Lithium Index juniors could be very lucrative this year, especially given the capitulation mood in the market.

With the recent filing of financial statements for the period ending June 30 it is time to start researching my 2024 Bottom-Fish Collection. The slump in financing this year has made my job easier, so long as I insist on working capital being $500,000 or more when I look at three criteria - money, people and story. (I used to focus on structure, namely how much of the stock was controlled by management and its allies, but these days a thumbs up on this count usually implies vulnerability to a pump and dump operation - much more interesting is a meaningful management stake in a sea of liquidity.)

A tougher question than bottom-fishing strategy is what to do about the 2024 Favorites Collection which are supposed to be graduates from the Bottom-Fish Collection. The 16 juniors in my 2023 Favorites collection are down 17.2% this year, with only 3 showing gains, of which the winner is Brunswick Exploration Inc, among a handful that don't deserve to be demoted to the 2024 Bottom-Fish Collection. The missing piece for many of 2023 Favorites is a positive outlook for their target metal and a return of investor interest in the resource sector. But with 5% risk free interest rates being threatened by central banks well into 2026 in pursuit of their 2% inflation targets, the more likelier outcome is a major economic downturn that does not boost metal prices, and leaves most juniors gasping for air.

I recently used the KRO Search Engine to do a quick survey of resource juniors with at least $500,000 working capital among which I spotted about a hundred bottom-fish candidates, many of which have yet to form a bottoming chart pattern. What was truly awful, however, was the large number of prominent companies that normally do not qualify as bottom-fish because they are well promoted and financed by Bay Street, but which now have ski slope charts turning into cliffs. This is a sign of collective capitulation, and, with tax loss selling usually not kicking in until December, Q4 of 2023 looks awful. But not if you are today doing your homework and preparing a bottom-fish watch list to load up in December's tax loss selling season (don't worry about the tax losses being taken earlier, the optics and threat of the resource junior ecosystem approaching an extinction threshold will generate capitulation selling by shareholders who aren't underwater, just fearing the opportunity cost posed by dead money and risk free 5% plus interest bearing deposits. But while I am rubbing my bottom-fishing hands, coming up with the 2024 Favorites Collection is going to be a challenge unless it becomes a collection of my favorite bottom-fish.

A major focus of Kaiser Watch in 2024 will be the James Bay Lithium Index because its macro story is intact and does not require a higher metal price to boost the value of resource juniors. The individual company story will be grassroots discovery exploration, the simplest kind that takes me back to the 1980s when making money on resource juniors required a grassroots discovery and a wave of "me too" juniors. As part of my bottom-fish research I will pay particular attention to the JBLI members, of whom I recently confirmed Midland Exploration Ltd and Ophir Gold Corp as part of my 2024 Bottom-Fish Collection. To encourage new subscribers to sign up for a USD $450 annual individual KRO membership I am extending the term of all new signups to the end of 2024. You may not be in hurry to buy anything yet, but you ought to be building your watch list now for later this year. |

Liontown Resources Ltd (LTR-ASX)

Unrated Spec Value |

|

|

| Kathleen Valley |

Australia - Western Australia |

8-Construction |

Li Ta |

Q2 Metals Corp (QTWO-V)

Fair Spec Value |

|

|

| Mia |

Canada - Quebec |

2-Target Drilling |

Li |

Ophir Gold Corp (OPHR-V)

Bottom-Fish Spec Value |

|

|

| Radis |

Canada - Quebec |

2-Target Drilling |

Li |

Dios Exploration Inc (DOS-V)

Bottom-Fish Spec Value |

|

|

| LeCaron Lithium |

Canada - Quebec |

1-Grassroots |

Li |

Albemarle Corp (ALB-N)

Unrated Spec Value |

|

|

| Greenbushes |

Australia - Western Australia |

9-Production |

Li |

Bar Chart displaying value of 2022 Metal and Fossil Fuel Production |

Graphics from Ophir's recent Radis Update |

Graphic from Q2's recent Mia Update |

Graphic from Dios' recent Lecaron Update |

IPV Chart for Q2 Metals showing relative valuations of James Bay projects |

Snapshot of 2023 KRO Favorites |

| Disclosure: JK owns shares of Brunswick and Dios; Brunswick is a Fair Spec Value rated Favorite; Q2 Metals is Fair Spec Value rated; Dios and Ophir Gold are Bottom-Fish Spec Value rated |