| Kaiser Watch December 6, 2023: If not a Peanut or a PMET then what? |

| Jim (0:00:00): Why did the market not like Brunswick's Mirage update? |

Brunswick Exploration Inc finally published an update for its Mirage project on December 5, 2023, and, not surprisingly, the market decided it was not good enough. It did not help that the spot price of lithium carbonate dropped below $8.00/lb, and that the hedge fund short attack against lithium producers has helped lithium producers drop to their lowest price in a year. Brunswick last provided an update on October 3 when it reported that it had completed 15 holes at Mirage of which 12 intersected spodumene bearing pegmatite intervals up to 52 metres. The company provided no information about drill hole locations nor what additional prospecting had turned up within the 5 km by 20 km northeast trending Mirage property. What the market wanted was a sense of the scale of the Mirage potential, especially in light of the 3 km by 500 m wide field of spodumene boulders as big as 6 metres identified down ice from a 2.7 km corridor of outcrops to the northeast. The update provided this week, however, was confined to a 2 km by 1 km area where the company has completed 36 core holes totaling 5,080 metres. These are shallow holes to a maximum vertical depth of 150 metres. A winterized camp has been established and Brunswick plans to return by mid January to conduct a 15,000 m program during Q1 of 2024.

Assays published for 14 holes indicate that Mirage has three northeast trending dyke sets which the company has labeled the North, Central and South zones (the North zone appears to have 2 dykes). The drilling strategy seems to have involved starting the initial hole under the three main outcrops in this 2 km by 1 km area. Brunswick has published a drill plan outlining the drill hole traces and highlighting spodumene pegmatite intervals. All but 3 holes intersected spodumene bearing pegmatite. It is disappointing that the company decided not to publish azimuth, angle and total hole length information, even for the assayed holes, supposedly because they are afraid potential predators might figure out what Brunswick has at Mirage. The company provided one section for each zone.

Of the first 14 holes all but #13 intersected spodumene bearing pegmatite (the first hole drilled in the South Zone was drilled in the wrong direction but map have nipped some pegmatite and assays are still pending- hole #14 intersected 16.2 m of 2.75% Li2O. Only about 100 m strike of the North Zone was tested with holes 1-4 of which #1 and #2 delivered 24.5 m at 2.18% and 25.8 m of 2.57%, with grades spiking to 3.08%. True width is estimated at 90%. The MR-1 dyke dips to the northwest. Holes 3 and 4 intersected a narrower dyke to the southeast which they call the MR-2 dyke.

Holes 5-12 were drilled along a 300 m segment of the MR-3 dyke and yielded intervals up to 50.6 m grading 1%-2%. MR-3 also strikes northeast but dips to the southeast. Toward the end of the program Brunswick stepped about 500 m northeast close to the boundary of the inlier claims optioned 75% from Osisko Development Corp and drilled holes #28-30 from what appears to be a single drill pad. The map shows spodumene was intersected where you might expect the MR-3 dyke to be, giving it a strike of 750 metres. Hole 35 returned to the main part of MR-3, but the surface projection of the spodumene interval suggests a separate parallel dyke has been intersected.

Assays were reported only for #14 of holes #13-27 drilled into the South Zone which call the MR-4 dyke. This hole yielded 16.2 m of 2.75% Li2O. The MR-4 dyke has been encountered along a strike of 750 m and dips southeast at 45 degrees. Brunswick makes the important statement that similar bonanza grade mineralization has been seen in all the MR-4 dyke holes.

After hole #27 they drilled the #28-30 holes stepping out northeast of the MR-3 dyke for which assays were reported, and then stepped back to the southeast to drill holes 31-32 which intersected spodumene of what looks like a separate dyke that lines up with the dyke encountered by hole #35. But things got really interesting with hole 33 and 36 which have a much greater extent of surface projected spodumene intervals than any of the other 34 holes. They have included these holes in the Central zone, but, thanks to hole #34 which intersected spodumene half way between #33 and the southwestern limit of the South Zone, it looks like #33 and #36 are the continuation of the 2%-3% grading MR-4 dyke.

What does this mean? Is it a Peanut or a PMET? The company states that it has intersected a combined strike length of 1,500 metres, but if you connect some dots it is at least 2,000 m. Just to get a sense of the scale, one can imagine 2,000 m strike by 25 m thickness by 300 m down-dip and 2.6 specific gravity. That gives you a tonnage footprint of 39 million tonnes. That is a lot more than a Peanut, but it also is not close to being a PMET whose CV5 zone yielded 109 million tonnes of 1.42% Li2O based on 163 drill holes representing 56,000 m. Brunswick has only drilled 36 holes for 5,080 metres. The market saw the small area footprint, realized that the 15,000 m program in Q1 of 2024 would be focused on delineating the dyke sets within this area, and while the average grade might prove better than CV5, the tonnage would remain below 50 million tonnes, which the market thinks is Mickey Mouse. In an earlier KW episode I had joked that when Brunswick reveals what it has at Mirage Gina Rinehart would come and eat up Brunswick. But in the KRO Slack Forum we ended up joking that in light of this update Gina would just send her cat to take care of Mickey Mouse.

But one thing puzzled me, namely this statement by Bob Wares: "I believe the distribution of the first four mineralized dikes at Mirage does not explain the three-kilometre-long trend of rich spodumene-bearing boulders that occurs to the southwest. With more outcropping spodumene-bearing dikes located another three kilometres to the northeast, we have considerable exploration work and drilling to do to unlock the full potential of this promising property."

I asked Bob on what basis he made that statement and he explained that the MR 1-4 dykes have high levels of tourmaline and low levels of muscovite, whereas the boulder field that stretches 3 km to the southwest has lots of muscovite and almost no tourmaline. He also pointed out that the abundance and size range of the spodumene crystals in the boulders is very similar to what they are seeing in the core of the MR1 and MR-4 dykes which is running 2%-3%. The difference between the mineralogy of the boulders and the bedrock hosted pegmatites makes it impossible for the MR 1-4 dykes to have been the bedrock source. I then queried him on why he was looking for more potential 3 km to the northeast where apparently they have outcrops? The company's boulder distribution map shows that boots on the ground found the boulders largely concentrated in what appear to be two linear trends within the 3,000 m by 500 m corridor that has the same orientation as the ice direction.

The important news in the Mirage update is that the MR 1-4 dykes have a northeast orientation which happens to be the same as the ice direction. Because the boulder train had the same orientation everybody assumed glacial transport dropped them where they ended up and that the roundedness was due to abrasion as the ice sheet entrains loose boulders and drags them along the bedrock. If the boulder gets into the ice sheet it can be transported hundreds of kilometers. When the ice sheet stops flowing and melts, these boulders called glacial erratics end up sitting on bedrock with completely unrelated geology. AntarcticGlaciers.org has a good publication on Glacial Erratics.

The problem with the ice sheet transport explanation is that the Mirage boulder collection is too uniform and concentrated to have been plucked from bedrock and dragged 5-10 km from their location. I asked Bob if there is any outcrop in the vicinity of the boulders and his response was that this area is completely covered by overburden in which these boulders sit. So the lack of outcropping pegmatite doesn't mean there is no pegmatite in this area. I suggested maybe these boulders are sitting on top of a big pegmatite, one with Greenbushes scale. This pegmatite may have been a ridge which over time got broken up through fractures and then underwent "chemical" weathering courtesy of the freeze-thaw cycle in the James Bay region which would cause the boulders to end up somewhat rounded without ever having been tumbled as happens in shoreline or river systems, or from extensive dragging when stuck in the base of an ice sheet. For an idea of how this in situ weathering happens, check out this Formation of Rounded Boulders Video which one my KRO Slack Forum members tracked down while we were having a discussion about the origin of the Mirage boulder field.

Bob Wares did concede that this was a possibility, and that a glacial expert on their team has suggested the displacement is less than 500 m. He does not like the idea of drilling a fence of scout holes to prospect the bedrock and hope to spear a blind pegmatite, especially given that a key talking point during the past two years has been that Brunswick is only chasing after outcropping pegmatites. But in light of the bonanza grades in the North and South Zone dykes, the similar spodumene crystal distribution within the boulders, the mineralogical difference of the boulders, and the scale of the boulder field, lining up with what appears to be an important structural trend suitable for pegmatite emplacement, it is plausible that the boulder field is sitting on top of its bedrock source. In 2012 when Talison Lithium Ltd owned Greenbushes it reported a resource estimate of 118.4 million tonnes of 2.4% Li2O within a pegmatite body roughly 2,000 m long, 250 m wide and at least 500 m deep. Over the next week or so the company will decide if it will include some boulder field scout holes with the 15,000 m winter program. If neither "Mickey Mouse" nor anything up ice plausibly explains the boulder field, perhaps it is sitting on top of a Green Giant. As it now stands, the market thinks all that will change over the next 6 months is that a resource estimate will emerge for the small North-Central-South area, and that for an outcome of this size the Mirage play is already fully priced. Hopefully they decide to test the Greenbushes in situ hypothesis this winter. |

Brunswick Exploration Inc (BRW-V)

Favorite

Fair Spec Value |

|

|

| Mirage |

Canada - Quebec |

2-Target Drilling |

Li |

Price Charts for Lithium Producers and Advanced Juniors |

Lithium Rock Value Matrix and Price Chart |

Peanut, Mickey Mouse, PMET or Green Giant? |

Mirage Assay Results |

Where did that Boulder Field Come From? |

| Jim (0:14:02): Why did Vanstar settle for a $0.69 buyout offer from IAMGOLD? |

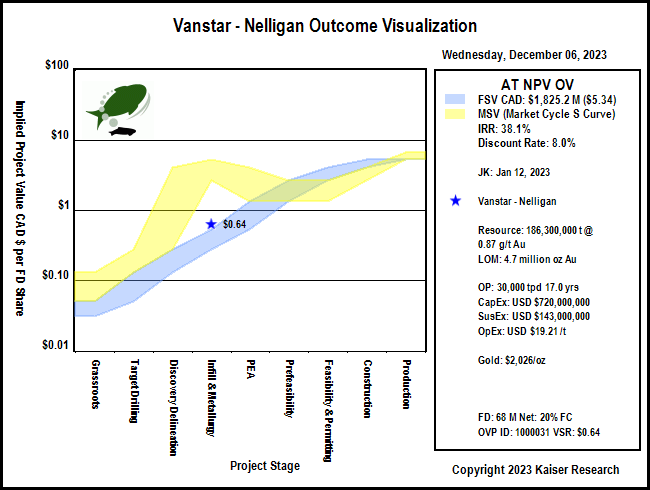

On December 5, 2023 Vanstar Mining Resources Inc announced a friendly buyout deal whereby IAMGold would issue 0.208 IAMGold share per Vanstar share which was valued at $0.69 at Monday's closing price. This disappointed some shareholders who were hoping for a higher price. In KW Episode November 10, 2023 I discussed the company's predicament as the minority stakeholder in the 5.2 million ounce Nelligan gold deposit in Quebec. However, I pointed out that by optioning the Amanda project in the James Bay region to Mosaic Minerals Corp Vanstar could perhaps attract some interim upside if Cygnus Metals Ltd continues to have lithium pegmatite success at its Auclair project which surrounds Amanda, and Mosaic discovers enough LCT-type pegmatite to eventually get Amanda acquired by Cygnus. This farmout deal is now a bad deal for Mosaic because IMG will inherit the Amanda project, and, if it becomes valuable, will decide to keep 50% when Mosaic vests rather than let it earn 80% by delivering a resource estimate before 2030. Since apart from JD Moore Vanstar management does not own much stock, there could be a problem getting shareholder approval for the plan of arrangement, which CEO JC St-Amour thinks could be completed by the end of January 2024. Since there is some overlap between the shareholders of Vanstar and Mosaic, maybe IMG will let Vanstar renegotiate the Amanda deal.

At first I was dismayed by the buyout terms, but on further reflection I have decided it does make sense. The uncertainty about when IMG would push Nelligan into the feasibility demonstration stage qualified Vanstar as part of the 2023 Bottom-Fish Collection and I had confirmed it for the 2024 Collection. IMG has been focused on getting its Cote gold project into production, but when it got wind of Vanstar management's effort to market itself as a buyout target for a royalty company, it initiated discussions. Since 2019 when IMG vested for 75% by delivering a resource estimate it has had the option to carry Vanstar until delivery of a bankable feasibility, at which point IMG's stake would increase to 80% and trigger a right to purchase the 20% interest at fair value based on the BFS numbers. Vanstar would retain an uncapped 2% NSR. So a royalty company had the potential to get a payout for the 20% carried stake plus retain a 2% NSR for the life of the mine whose gold resource is currently 5.2 million ounces and will probably grow over time.

In terms of the rational speculation model, if you accept my outcome visualization for a 30,000 tpd OP mine, the project would be worth CAD $1.8 billion on a 100% basis when ready to start production, which is $5.32 per share for Vanstar based on 20% and 68 million shares fully diluted. But a project stuck at the infill drilling stage has a fair value range of only 5%-10% of the expected outcome value, or $0.27-$0.53 per share. So the deal in rational terms is slightly better than fair value. The risk for Vanstar shareholders is that as Nelligan plods through the feasibility demonstration and permitting trough management might end up diluting the stock to pay the bills and stave off boredom by taking on other projects such as Amanda to generate interim upside. That would not be an issue for a royalty company. But there was a hitch.

The hitch is that at any time IMG could decide to form a 75:25 JV which would kill the option to buy the 20% for fair value and a 2% NSR. CEO JC St-Amour tells me that IMG never threatened to do this, but, given the endless bear market, it makes a lot of sense for a producer to embark on a 5 year economic study cycle, make all the decisions and control the disclosure timeline, and send monthly 25% cash calls to the poor junior partner stuck in the value trough. This risk would also have discouraged a royalty company from buying Vanstar. It is what management had to consider when IMG proposed negotiating an early buyout.

There is an outside chance a royalty company may make a hostile bid at a somewhat higher price, but I would discount that path. IMG has been through a development ordeal at Cote thanks to cost overruns and has had to sell off other projects to keep the development on track. It expects to pour gold in Q1 of 2024. Unless gold soars to the moon IMG will have a hard time recreating itself as a multi-mine producer. In 2024 we may see gold establish $2,000 as a floor rather than a ceiling, and that would boost IMG's price as Cote comes on stream. It would also boost the price of established producers who may move quickly to acquire IMG. The bet Vanstar management is making today is that while an implied $0.69 buyout price is disappointing, by the time the special meeting for the plan of arrangement is held in January and the acquisition is confirmed, possibly by late January, IMG's stock price could be trending higher. Furthermore, the change from dead money Vanstar paper into IMG paper is without capital gain consequences. If the status quo were maintained the risk is that Vanstar stays dead money while producers slug it out for control of IMG, and perhaps take even longer to turn their attention to Nelligan, or worse, declare a 75:25 joint venture where Vanstar's upside gets squashed through dilution funding its 25% stake which nobody but the 75% opertator will ever want to acquire. With this deal Vanstar's destiny has been hitched to IAMGold's destiny. |

Vanstar Mining Resources Inc (VSR-V)

Bottom-Fish Spec Value |

|

|

| Nelligan |

Canada - Quebec |

4-Infill & Metallurgy |

Au |

Rational Spoeculation Model Fair Value Ranges for Vanstar |

Implied Project Value Chart for Total Value |

Implied Project Value Chart on per Vanstar Share Basis |

| Disclosure: JK owns shares of Brunswick; Brunswick is a Fair Spec Value rated Favorite; Vanstar is Bottom-Fish Spec Value rated |