Hello Guest User, You are visiting this website from a computer with an IP address of 172.70.178.2 with the name of '?' since Fri Apr 26, 2024 at 4:00:58 PM PT for approx. 0 minutes now.

Spec Value Rating Overview Updated January 3, 2023

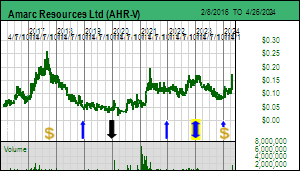

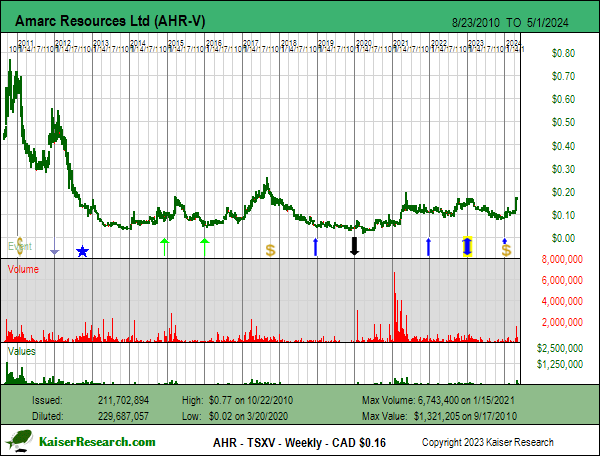

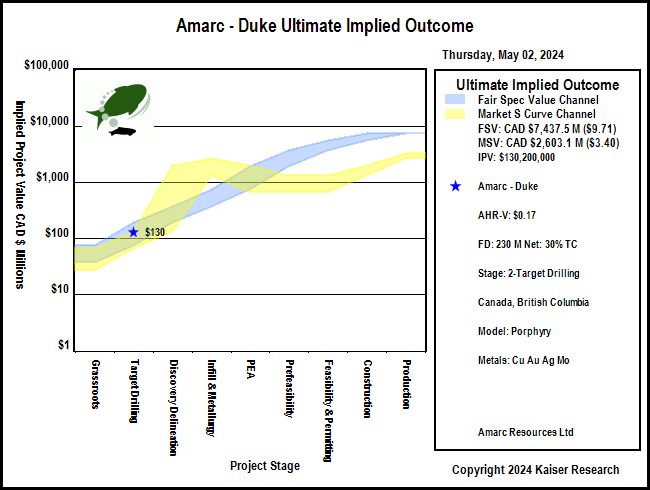

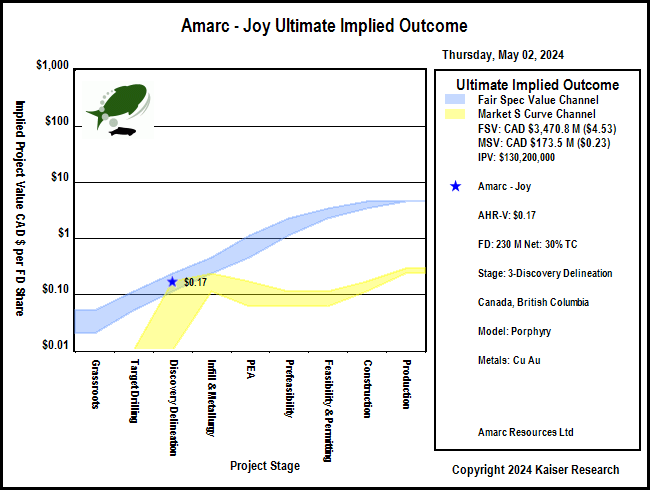

SV Rating: Bottom-Fish Spec Value - as of December 29, 2023: Amarc Resources Ltd was made a Fair Spec Value rated 2023 Favorite at $0.15 on December 30, 2022 based partly on its British Columbia focused copper exploration plays, two of which, Joy and Duke, are funded by majors Freeport McMoran and Boliden who can earn up to 70% by spending $105 million and $90 million respectively. Freeport optioned the Joy copper-gold porphyry project in May 2021 and has spent about $20 million to the end of 2022. The 48,200 ha Joy project adjoins to the north of the Kemess Mine now operated by Centerra Gold. Freeport, which drilled 15,427 m in 2022 for which results were still pending at the start of 2023, is delineating the Pine copper-gold system and testing district wide targets. Boliden optioned the 67,800 ha Duke project in November 2022 and immediately initiated a winter drill program. Duke, located 50 km north of the former Bell and Granisle copper mines in the Babine Lake region, is an emerging copper-molybdenum-silver discovery Amarc made in 2017. Amarc is operator of both projects. The company is headed by CEO Diane Nicolson and Chairman Bob Dickinson who with 29 million shares representing 16% is Amarc's largest shareholder. Amarc has for two decades been focused on grassroots exploration in British Columbia during a period when Northern Dynasty's now beleaguered Pebble copper-gold project in Alaska dominated the attention of the HDI group. Amarc appeared on track for a major emerging discovery in 2014 when it assembled the IKE copper-molybdenum-silver district located in southwestern British Columbia between Taseko's stalled New Prosperity copper-gold project and the Bralorne gold project to the south. IKE, which does not yet have a resource estimate, was first optioned to Thompson Creek in 2015 which dropped out after Centerra Gold acquired Thompson in 2017. In mid 2017 Hudbay optioned both IKE and Joy, but dropped out in early 2019 after spending nearly $10 million when Waterton launched a proxy battle. Amarc, which had a weak treasury supported by loans from Dickinson, spent the next two years bottom-crawling below $0.10 until the Joy farmout in 2021 woke up the company. Market interest strengthened with the Duke farmout because one never knows when a major like Freeport might suddenly lose interest, but it will take at least a year before Boliden is in any danger of losing interest. In May 2022 Amarc also quietly optioned the Hearne Hill project for $1 million in the form of $100,000 annual payments. Hearne Hill is south of Duke and southeast of Pacific Booker's Morrison copper-gold porphyry project which is stalled because of proximity to Morrison Lake. Hearne Hill is inland and hosts a copper breccia pipe system that underwent small scale mining but which Amarc plans to rethink as a bulk tonnage copper system. The main reason, however, for making Amarc a 2023 Favorite is its plan to revisit the Empress area at the northern end of the 100% owned IKE project. The Empress area represents a gold enriched copper replacement system within older volcanics and sediments off-board the northern boundary of the Coast Plutonic Complex. Amarc would also like to do enough drilling of IKE to allow a maiden resource estimate. Working capital as of September 30, 2022 was about $3 million, not enough to mount a major program. But with 199 million shares fully diluted and the last financing done in 2017 there is no market overhang if Bob Dickinson comes through with his threat to emerge from semi-retirement and turn Amarc into the success story that has eluded it for two decades.

Recommendation History

Edition

Date

Price

Recommendation

Gain

BF1998

12/1/1997

$0.62

New BF MP Buy $0.50-$0.75

0%

BF1998

12/11/1998

$0.60

Confirm BF TP Buy $0.50-$0.75

-20%

BF1998

1/5/2000

$0.70

Confirm BF TP Buy $0.50-$0.75

-7%

BF1998

12/30/2005

$0.29

BF Cycle Closeout Sell 100%

-61%

BF2009

12/24/2008

$0.10

New BF MP Buy $0.10-$0.19

-47%

BF2009

12/30/2011

$0.41

BF Technical Closeout Hold 0%

116%

BF2014

12/4/2014

$0.07

New BF Buy below $0.10

-30%

BF2014

12/31/2015

$0.06

BF Technical Closeout 100%

-40%

BF2016

12/31/2015

$0.06

New BF Buy below $0.10

-40%

BF2016

12/13/2018

$0.06

BF Technical Closeout 100%

-45%

SVF2023

12/30/2022

$0.15

Fair Spec Value Favorite

0%

SVF2023

12/29/2023

$0.10

SV Technical Closeout 100%

-33%

Charts & Financing Activity

Most recent 43-101 resource estimate Prior resource estimate PEA PFS FS/BFS/DFS

Private Placement Key

less than $500,000

$1,000,000 - $2,000,000

$5,000,000 - $10,000,000

$20,000,000 - $50,000,000

$500,000 - $1,000,000

$2,000,000 - $5,000,000

$10,000,000 - $20,000,000

over $50,000,000

Private placement financing dates and value ranges are based on transactions reported by the TSXV Monthly Review.

Past Insiders and Reported Shareholders - Current Ownership Status unknown - positions may be pre-rollback

Related Party

Occupation

Related Since

Insider Ended

Director Ended

Capacity

Ownership

Rene G. Carrier

Administrator

9/29/2008

11/22/2018

11/22/2018

Director

400,000

David J. Copeland

Engineer

9/1/1995

9/17/2015

9/17/2015

Director

1,249,500

Colin Gibson

Broker

1/24/2011

Placee

125,000

Roy Greig

Geologist

1/31/2022

3/11/2024

VP Exploration

0

Harold Hodgson

Broker

1/24/2011

Placee

312,500

Greg Johnson

Broker

1/24/2011

Placee

31,250

Jeffrey R. Mason

Accountant

9/1/1995

11/22/2018

11/22/2018

Director

2,878,500

Peter Ross

Broker

1/24/2011

Placee

62,500

John Rybinski

Broker

1/24/2011

Placee

312,500

Philip Smith

Broker

1/24/2011

Placee

62,500

Sun Valley Gold LLC

Institution

3/16/2012

Insider

14,615,384

Ronald W. Thiessen

Accountant

9/1/1995

11/21/2019

11/21/2019

CEO

3,109,992

John Welch

Broker

1/24/2011

Placee

12,500

Share positions of current insiders based on last AGM circular, ownership % based on current Issued. Share positions of past insiders and shareholders have not been adjusted for rollbacks or splits.

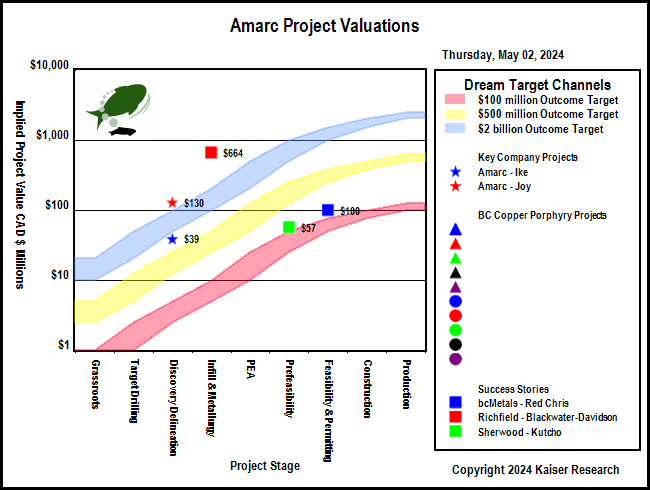

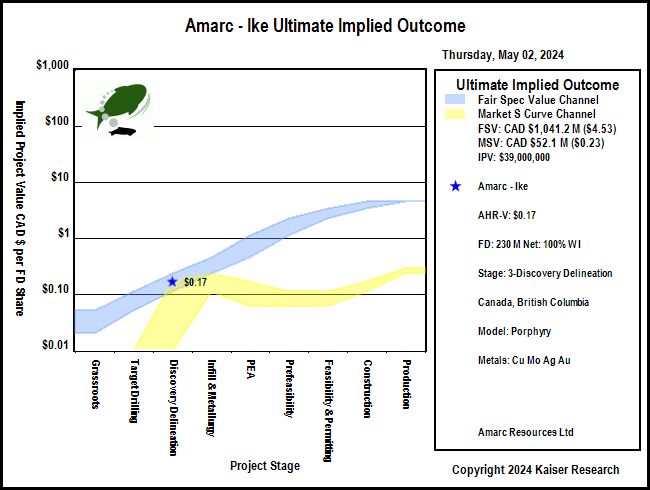

A Spec Value Hunter table allows speculators to identify which projects offer poor, fair or good speculative value according to the rational speculation model. The speculative value depends on the project stage, the project's implied value as calculated by the company's fully diluted, stock price and net project interest, and the dream target deemed appropriate for the project. A dream target is what a project would be worth in discounted cash flow terms once in production.

Poor Speculative Value -

Fair Speculative Value -

Good Speculative Value -

Note: narrow arrows indicate IPV is outside the fair value channel but within 25% of the fair value limits

Color Key for Target Outcome Achievability Ranges in millions ranked from most to least achievable

below $25

Should be Private: Artisanal, Placer, Mom & Pop Shop

$25-$50

Tiny Scale: underground mine or quarry - not worth the bother

$50-$100

Small Scale: junior needs to self-develop

$100-$250

Buyout Target: by Lower Tier Producers

$250-$500

Buyout Target: by Mid-Tier Producers

$500-$1,000

Ideal Target for Junior: Buckhorn, Sleeper

$1,000-$2,000

Almost World Class: Ekati, Red Chris, Brucejack, Juanicipio, Stibnite

$2,000-$5,000

World Class: Eskay Creek, Hemlo, Hermosa-Taylor, Oyu Tolgoi, LaRonde, McArthur

$5,000-$10,000

Giants: Escondida, Sullivan, Carlin Trend, Kidd Creek, Orapa, Kamoa-Kakula

above $10,000

Off the Scale District: Wits 1.0, Araxa, Sudbury Basin, Bayan Obo

The target outcome range required for the current implied project value to represent fair speculative value is based on the upper and lower certainty limits associated with the project stage. The color coding is based on the target outcome using the mid-point of the certainty range.

Active Company Projects

Project

Location

Net Interest

Stage

IPV $ MM

Fair Spec Value Required Target Outcome Range

$100

UPV $500

$2000

Target Metals

Deposit Style

Ike

Canada - British Columbia - Southwest BC

100% WI

3-Discovery Delineation

$38

$758 - $1,516

Copper Molybdenum Silver Gold

Porphyry

Duke

Canada - British Columbia - Central BC

30% TC

2-Target Drilling

$126

$5,053 - $12,633

Copper Gold Silver Molybdenum

Porphyry

Joy

Canada - British Columbia - Toodoggone

30% TC

3-Discovery Delineation

$126

$2,527 - $5,053

Copper Gold

Porphyry

Hearne

Canada - British Columbia - Northern BC

100% WI

2-Target Drilling

$38

$1,516 - $3,790

Copper

Porphyry

Project Stage

Flagship

Secondary

Active

Grassroots (1) & Target Testing (2)

Discovery Delineation (3)

Infill Drilling & Metallurgy (4)

PEA (5) or PFS (6)

Feasibility & Permitting (7)

Construction (8) or Production (9)

Clicking on the project icon will display a popup identifying the company project, its stage and target metals, basic facts, a chart, a link to that project within that company's KRO Profile, a link to the most recent news release, and a link to the most recent KRO comment if one exists.

Net Interest: 100% WI Vested: No Uncapped NSR/GOR: 0.00%

Ownership Terms: December 2013 option to acquire 80% from Oxford Resources Inc. Amarc can acquire 80% by making cash payments totaling $125,000, issuing 300,000 shares, and by incurring approximately $1,860,000 in exploration expenditures on or before November 30, 2015. In July 2014 the Ike Agreement was amended and Oxford assigned all of its interest property, and the underlying option agreement with respect to the Ike property, to Amarc and

converted its ownership interest in the Ike property to a 1% Net Smelter Return (NSR) royalty in

consideration of a $40,000 cash payment. The 1% NSR royalty can be purchased at any time for

$2,000,000 less any amount of royalty already paid. Underying vendor holds a 2% NSR. 1% can be bought for $2 million any time before commercial production and the other 1% can be bought for $2 million before Nov 30, 2015. On Sept 3, 2015 optioned up to 50% to Thompson Creek Metals which dropped the option after earning 10% which it agreed to convert into a 1% NSR capped at $5 million. Agreement July 18, 2017 whereby Hudbay Minerals Inc can earn an initial 49% ownership interest in the IKE Project under a Stage 1 Farm-in Right by funding $25 million of expenditures before December 31, 2020, of which $3.3 million is committed for 2017. Provided its Stage 1 Farm-in Right is exercised, Hudbay can, pursuant to a Stage 2 Farm-in Right, elect to earn an additional 1% interest in the Project (for a total 50% interest), by funding $15 million of expenditures (for a total of $40 million), also before December 31, 2020. Stage 1 and Stage 2 Farm-in expenditures can be accelerated by Hudbay at its discretion. Amarc will be the operator during the Stage 1 and Stage 2 periods. A Joint Venture ("JV") will be formed when Hudbay has acquired a 49% interest in the Project. Provided that Hudbay has exercised its Stage 2 Farm-in Right and acquired a 50% interest in the IKE Project, it can then elect to go forward via one of two paths. First, Hudbay can replace Amarc as operator of the JV after it funds all project expenditures and completes a Feasibility Study for the IKE Project by December 31, 2025. Having gained operatorship, Hudbay can then choose to either go forward with Amarc in a 50/50 participating JV, or can instead elect to continue with its Farm-in (the 'Stage 3 Farm-in Right") to acquire an additional 10% interest in the IKE Project (for a total 60% interest). To exercise its Stage 3 Farm-in Right, Hudbay must fund all expenditures required to submit a British Columbia Environment Assessment ("EA") application for the IKE Project and, if applicable, a Canadian EA application, with the application(s) being accepted for review by December 31, 2026. In addition, Hudbay must also continue to fund all project expenditures until the necessary EA Certificate(s) are received. Following receipt of the EA Certificate(s), all IKE Project expenditures going forward will be shared by Hudbay and Amarc on a pro rata basis (Hudbay 60%/Amarc 40%) under the JV. As a second alternative path Hudbay can elect, after exercising its Stage 2 Farm-in Right, to proceed directly to the Stage 3 Farm-in Right, so immediately becoming the operator, and acquire a further 10% interest (for a total 60% interest) by, as above, submitting and having accepted for review a British Columbia EA application and, if applicable, a Canadian EA application, by December 31, 2026. Again in this instance, Hudbay must also fund all project expenditures until receipt of the necessary EA Certificate(s). As with the first path, following receipt of the EA Certificate(s), all IKE Project expenditures going forward will be shared by Hudbay and Amarc on a pro rata basis (Hudbay 60%/Amarc 40%) under the JV. HudBay dropped option on Jan 21, 2019.

Initial Amarc drill program begins, with nine holes planned for 5,400m, designed as an initial test to confirm if Ike is an important porphyry system, deserving of more detailed exploration work going forward.

Target Testing

2014 Q4 Late November

2014 Q4 Late November

Reported results from 9 hole 5,400 m drill program started in mid September 2014 that confirm the presence of a potentially economic Cu-Mo-Ag porphyry system.

Net Interest: 30% TC Vested: Yes Uncapped NSR/GOR: 0.00%

Ownership Terms: Agreement Nov 22, 2022 where Boliden can earn up to 70% by spending CAD $30 million within 4 years to earn 60%, of which $5 million is committed in late 2022 and early 2023, after which Boliden can elect to earn 70% by spending $60 million over 6 years with $10 million minimum per year. Amarc will operate until Bolden vests for 60% at which point Bolden can elect to become operator.

Net Interest: 30% TC Vested: Yes Uncapped NSR/GOR: 0.00%

Ownership Terms: Part by staking, other by option from Cascadero and Gold Fields where Cascadero gets $1 million cash in stages by Oct 31, 2018 and $950,000 in Amarc stock by Oct 31, 2018 for its 49%. Amarc can over 4 years acquire Gold Fields' 51% by creating a new company in which Gold Fields will receive 15% on a fully diluted basis. Option Aug 22, 2017 whereby HudBay can earn 49% by spending $15 million by Dec 31, 2020, of which $1.9 million was committed for 2017. On vesting for 49%, Hudbay can earn 50% by spending an extra $5 million, also by Dec 31, 2020. Amarc operates during these stages. If Hydbay vests for 50%, it can elect to earn 60% by funding all costs needed to deliver an EA by Dec 31, 2026. HudBay dropped option on Jan 21, 2019. On Dec 10, 2019 Amarc acquired Gold Fiels' 51% by issuing 5 million shares and a future 2 million contingent on unspecified expenditures. Gold Fields retains a 2.5% NPI on 86% of property and 1% NSR on the rest. The NPI can be reduced to 1.25% for $2.5 million in cash or stock. Agreement May 12, 2021 to option 70% to Freeport McMoran for $35 million exploration over 5 years to earn 60%, after which it can earn 70% by spending $75 million over 5 years.

Net Interest: 100% WI Vested: Yes Uncapped NSR/GOR: 2.00%

Ownership Terms: Agreement May 16, 2022 to acquire 100% for $1 million payable $100,000 up front and $100,000 annually. Vendor retains a 2% NSR of which 1.5% is capped at 0.5%.