Hello Guest User, You are visiting this website from a computer with an IP address of 172.71.254.144 with the name of '?' since Sat Apr 27, 2024 at 7:45:12 AM PT for approx. 0 minutes now.

Kaiser Media Watch Blog - March 1, 2024 to March 31, 2024

KRO Blog Overview

The KRO Blog is where unrestricted content is posted such as Kaiser Watch, material produced by third parties such as the as Investing News Network, and Metal Investor Forum conference links.

Kaiser Watch is a weekly audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees which have changed for 2024 as a transition to a $200 per month auto renewal program in 2025. During 2024 individuals can register for a KRO membership at a non-refundable price of $450 for a term that expires December 31, 2024. All active KRO members will be grandfathered to renew annually at $450 on Dec 31, 2024. Sign up here for this limited $450 offer. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch March 29, 2024: Ys $2,000 finally the floor for gold?

Jim (0:00:00): How is the market responding to the recent gold uptrend that on Thursday achieved an all-time high of $2,214?

Gold achieved an all time high of $2,214 per oz on the LBMA on March 28, 2024, registering an 11.5% gain from its 2024 low achieved on February 14, 2024. Gold's uptrend has not been tracked by silver which for the past year has traded in a narrow range of $23-$25 per oz. This disconnect is evident in the uptrend of the gold-silver price ratio which now stands at 90.2. That there should be linkage between the price of gold and silver is a construct of the hard money crowd which forgets that gold is primarily produced as a store of value in the form of coins, bullion and jewelry that largely sit in vaults doing nothing, while most of the above ground silver stock is fabricated into some useful application. Most gold production is of a primary nature, while most silver is a by-product of base metal mines and some gold mines. As a result it gets produced regardless of the silver price and gets sold at whatever the market price is. The fact that there is no obvious new usage for gold, such as we see with solar technology for silver and EV batteries for lithium, makes the recent independent uptrend a very curious phenomenon.

The usual gold price drivers invoked by the hard money advocates are not offering explanatory reasons for the demand that is driving up the price of gold. Inflation has come down from its 9.1% peak in June 2022 and has bounced between 3%-4% since June 2023, which is still above the Federal Reserve's 2.0% target though Jerome Powell has signaled three federal rate cuts totaling 0.75% in the second half of 2024 on the assumption that the negative impact of high interest rates are still working their way through the economy (for example about $2 trillion worth of commercial real estate debt is coming due by 2026, much of whose value has been compromised by pandemic triggered shift to working from home). The US treasury yield curve is slightly inverted, offering 5.5% for 1 month terms down to 4.18% for 7 year terms rising to 4.45% for a 20 year term. After a decade during which retirees and other savers got almost zero interest for their savings, as one can see from the awful yield curve on January 6, 2021, gold ownership which yields no income but does incur storage costs if a meaningful amount is owned hardly seems a good asset allocation strategy today.

Another common suspect behind an uptrending gold price is the US dollar weakening against other currencies, but the Nominal Broad Currency Index has been tracking sideways near its multi-decade high for the past year (a downtrend in the index represents other currencies rising against the US dollar). In terms of official sector buying the reversal of a 35 year spree of net central bank liquidation which began in 2009 slowed during the past two years, though there are reasons to believe that state owned Chinese entities have been secretly buying China's gold production. In 2007 China became the world's biggest gold producer and has maintained that lead. At the end of 2000 China's official gold reserves were about 13 million ounces, growing to about 72 million ounces at the end of 2023. But since then China has produced 251 million ounces, raising the question, who bought the other 192 million ounces? During that same period The United States produced 172 million ounces but its official holdings have been unchanged, so we know US gold production was sold into the open market. However, if China has hoarded all its gold production at the state level, which would make its official reserves 264 million ounces, slightly more than the 262 million ounces held by the United States, it simply means that the private sector has not had to eat each year's new Chinese mine supply. If you believe the official holdings report from the World Gold Council central banks have accumulated only 13% of the 1.4 billion ounces produced since 2009. The upshot is that official sector buying has not been a meaningful factor in the gold market, and is unlikely to be the source of the uptrend since mid February.

Another common suspect is the gold ETFs of which the SPDR Gold Trust (GLD-NYSE) is the biggest since its creation in 2005 with the help of the WGC to make physical gold more accessible to fund managers and individual investors. The GLD ETF has a mechanism whereby it accumulates gold when there is net investor buying that creates an arbitrage opportunity for a designated group of bankers to sell GLD paper short while buying cheaper physical gold in the bullion market. The short is covered by delivering the physical gold to the Gold Trust in exchange for GLD paper. The GLD's gold holdings peaked at 45.3 million ounces on December 7, 2012, and as the price of gold plunged lost 23.3 million ounces until its nadir on December 17, 2015. The 2020 covid pandemic generated a surge in investor demand for the GLD whose holdings climbed 12.4 million ounces from the start of 2020 to a peak of 41.1 million ounces on October 14, 2020. But apart from a short-lived burst during H1 of 2022 during the Russian invasion of Ukraine, just before the Federal Reserve began to raise interest rates, the GLD ETF has been steadily losing gold ounces. In 2024 the GLD had lost just over 2 million ounces by March 11 before it began to recover ounces. As of March 28 the GLD was still down 1.5 million ounces since the start of 2024. When you look at a chart which plots the daily changes in GLD gold holdings it is clear that investors are abandoning gold as an investment asset class, not accumulating.

The siren song that is luring investors away from gold is the resurgence of demand for BitCoin created by Wall Street securing approval for a raft of ETFs which track the price in the Bitcoin blockchain. Investors no longer need to worry that their "wallet" will disappear with a hard disk failure, the failure of a crypto-currency exchange, or the disappearance of key passwords. Since bottoming in late 2022 BTC has rebounded to make a new high at $73,750 and as of March 29 the existing BTC "stock" of 19.67 million coins had a value of about $1.4 trillion at $69,875 per coin. What is the intrinsic value of a Bitcoin? That concept makes no sense because BTC refers only to itself as a digital number with a coded limit that is priced in US dollars. Its value will be whatever somebody else is willing to pay for it and Wall Street is busy pumping Bitcoin to suckers as a legitimate asset class. In fact, it should be understood as a liability class because the ability to unload your BTC depends on energy being consumed as Bitcoin miners race to guess the numerical key that allows a transaction to take place. Bitcoin's very success will be the architect of its demise as the corresponding energy consumption goes through the roof, energy spent to facilitate the laundering of criminal proceeds and unproductive gambling activity. Bitcoin has two threats on the horizon which will kill Bitcoin mining. One is the AI Dream which will have enormous energy requirements once it gets rolling and starts delivering benefits in the material world rather than just unemployment for white collar "knowledge" workers rendered useless by AI processes. The other is the rising electricity demand from air conditioners as everybody scrambles to escape the consequences of global warming. When AC and AI electricity demand start to generate brownouts, the first line of attack will be shutting down electricity consumption by Bitcoin miners.

Above ground gold, in contrast, represents stored energy, because it takes energy to extract gold from the ground and concentrate it as a bullion bar. And it is compact, with the above ground gold stock of 6.6 billion ounces (205,280 tonnes) physically occupying a 22 metre wide cube (205,280 t divided by 19.3 specific gravity root 3). Incidentally, the above ground stock of silver, about 57.4 billion ounces or 1,785,312 tonnes, would occupy a cube with a width of about 55 metres (silver's specific gravity is 10.5). The above ground gold stock is worth about $14.6 trillion at $2,214/oz price, about ten times the value of the digital Bitcoin stock, which is the same value as the silver stock at $24.54 per ounce. The problem with silver is that most of it is fabricated into something physical serving a purpose, so you cannot make a massive investment in silver which is also stored energy. The ratio of the gold to silver price is rising because somebody is moving a lot of money into physical gold through the LBMA which these days seems to be setting the gold price rather than reflecting what is going on in the North American ETF markets.

It is currently a mystery who is buying physical gold without worrying that this buying activity is driving up the price, something central banks are loathe to do. My own suspicion is that it is the tech bro community doing the buying. The general equity market, especially that comprised of the tech giants, does not seem to have much room for upside, and insider selling has recently outpaced insider buying. The tech bro community is also notoriously full of itself and early on celebrated Bitcoin as the salvation for libertarian principles. It would not surprise me at all if the tech bros are unloading their Bitcoin into the indirect hands of the suckers Wall Street is marshaling in line to buy this new asset class that needs to increase ten times in price to enjoy the current value of the above ground gold stock. Converting an intrinsically worthless asset class into a real asset is good enough in itself as a motivation, but there may be other things going on in the heads of the tech bros.

The tech bros likely have a far deeper understanding of the vulnerability of the digital worlds they have constructed than your ordinary person. In the past six months there has been an increase of articles in mainstream media reporting warnings from various government agencies about the vulnerability of infrastructure at all levels to cyber-attack. Chinese malware is said to have been inserted everywhere as a potential prelude to an invasion of Taiwan. The rationale is that when everything jams up in the United States it will be too distracted to mobilize a response. Russian, Iranian and North Korean hackers are also doing their best to make it possible to implode the Global West from within. Authorities have dismissed the mysterious crash of the Dali freighter into the Francis Key Scott bridge spanning Baltimore's port harbor as an act of terrorism. Was this just a case of bad luck where Murphy's Law conspired to neutralize all backup and safety systems designed to prevent a complete power outage? Or was this a test run for remotely shutting down infrastructure? Whichever it was, the Baltimore incident is an example of what a deliberate cyber-attack might accomplish. That fear is not going to go away. Whoever is buying physical gold is doing so to end up with ownership of an asset class that once delivered to its purchaser is not going to evaporate when all hell breaks out in the digital world. It could still be stolen but I'm sure somebody buying gold on that scale can afford the security to prevent that from happening.

In 2020 I created a Gold Producer Index consisting of companies producing at least 100,000 ounces gold annually. It is an equally weighted index based on the closing gold ($1,523) and stock prices on December 31, 2019. The panic that swept markets in March 2020 when the world realized that covid was a life-threatening virus dragged the index down 30.7%, but by July 2020 it had bounced back with a peak gain of 56.4% as gold surged through $2,000. The big disappointment has been that since then as gold struggled to turn $2,000 into a floor rather than a ceiling the KRO 2020 Gold Producer Index has performed poorly. Partly to blame is the inflation which erupted globally that would have boosted OpEx to a greater degree than the general CPI figure.

Another reason is the growing perception that gold is an obsolete asset class that cannot compete with digital asset classes such as Bitcoin. When Nixon released gold from its $35 per oz peg to the US dollar in 1972 during an inflationary period the price shot to a high of $850 before stabilizing at around $400 in 1980 where it traded plus or minus $50 for the next two decades while the hard money crowd brayed about $2,000 gold. More than four decades later we finally have $2,000 gold but it is a pyrrhic victory. $400 gold CPI inflation adjusted from 1980 to the present is $1,554, which means that $2,214 represents a 43% real gain for the price of gold. But during those 43 years the mining industry produced 3.4 billion ounces, more than double the 3.2 billion ounces estimated to be the above ground stock in 1980. Not only has the mining industry harvested all the low hanging fruit that gold's tenfold increase during the seventies made available, but the CPI inflation figures reflect the productivity gains achieved by the digital revolution as well as the effect of globalization on the cost of consumer goods and services. Not only does the mining industry face a future of high hanging fruit in the form of what is left in the ground to find and mine (ie lower grade, poor metallurgy, access restrictions), but the CapEx and Opex for doing so is a lot higher than you get applying CPI to those costs in 1980. The 43% real price gain represented by $2,214 gold is thus an illusion, and the market knows it. What matters for the market is the idea that gold could reprice upwards to the $4,000 level without a major resurgence of inflation that keeps projects marginal that are currently marginal at $2,000.

Global gold production peaked in 2017 and is doomed to decline if the price of gold merely tracks inflation unless there is a discovery miracle that reveals new gold endowments that work at current prices. So you would expect the prices of gold producers to do poorly and not really follow any uptrend in the price of gold, especially if the $2,000 ceiling keeps reasserting itself in the short term as it did this year with gold bottoming at $1,985 in mid February. Remarkably, although gold is up only 12% from this February low, gold producers that have not suffered bad news like mine accidents have started to track gold's uptrend. You can see that in the Daily Index Performance chart which displays what percentage the index was up or down each day. The top tier producers Barrick and Newmont are up 18% and 20% respectively, followed by Agnico-Eagle up 32%. The mid-tier producers are generally up in the 35%-65% range from their 2024 lows. The index as a whole, which is down to 41 members from 53 due to buyouts and a couple failures, is up 22.6% from its February 13 low, and up 44.2% from its inception at the start of 2020. But for this uptrend to be sustained we need to see that $2,000 is indeed the floor from which bigger gains, perhaps into the $3,000-$4,000 range, can be launched. For the first to be convincing we need to survive Q2 of 2024, but for a gold bull cycle to emerge we need to see further gold price gains.

KRO 2020 Gold Producer Index (100,000+ oz annual production)

Daily Up-Down Chart past 120 days for KRO 2020 Gold Producer Index

Gains from 2024 lows for a selection of top and mid tier producers

Long Term Chart for LMBA Gold closing price

Chart showing stable patterns for USD Index, Inflation and Interest Rates

US Treasury Bill Yield Curve - Jan 6, 2021 vs Mar 27, 2024

Chart showing inflation adjusted gold price from 1980 benchmarks $400 and $850

BitCoin Chart: $1.4 trillion BTC value vs $14.6 trillion Gold Stock Value

GLD ETF Chart with daily gold holdings and NYSE volume compared to gold price

GLD ETF Chart showing daily changes in gold holdings 2018-2024

GLD ETF Chart showing daily changes in gold holdings 2005-2024

Gold to Silver Ratio Chart - silver is not tracking gold's uptrend

Cumulative Chinese gold production 2020-2023 and Official Reserve growth

Long term chart of annual changes in US and ROW official gold holdings

Annual global gold mine supply 1970-2023

Growth of above ground gold stock 1845-2023

Growth of above ground silver stock 1970-2023

Jim (0:10:50): Which juniors in your KRO Favorites would you pick to bet on gold?

The gold juniors have so far not responded to the six week uptrend in the price of gold because it is too soon to tell if $2,000 is indeed the new floor for gold rather than its ceiling. Gold producers have responded but their ability to post further gains will require gold to establish $2,500 as a new trading level where the real price gain is 61%, not really a meaningful monetary difference, but it is the optics that count. I have two juniors in my 2024 collection which represent opposite extremes for how to play the non-producing juniors with exposure to gold.

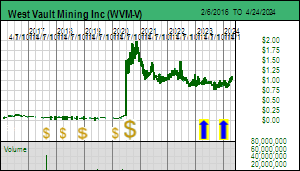

The first is West Vault Mining Inc which owns the Hasbrouck project in Nevada near Tonopah. Hasbrouck consists of two deposits that will be open-pit mined and heap leached at 17,000 tpd over an 8 year mine life during which it would produce 561,000 ounces. This project is shovel ready with all development permits in place, and the PFS was updated in January 2023 so the CapEx and OpEx numbers are reasonably reliable. At the base case price of $1,790 per oz gold the project has an after-tax IRR of 48% and net present value of USD $135.3 million at 10% discount rate and $192.6 million at 5%. Based on 59.5 million shares fully diluted and an exchange rate of 0.74 USD for 1 CAD this translates into an NPV per share range of CAD $3.09 to $4.37. The stock has been stuck in the $0.90-$1.00 range but managed to creep up to $1.03 on Thursday. The biggest shareholder is Sun Valley Gold LLC whose head Peter Palmedo has made a strategic decision to forego any further exploration activity or project diversification and just maintain West Vault as a target for a future buyout. This allows West Vault to serve as a leveraged proxy for the price of gold.

For example, at the current gold price of $2,214 the DCF model using the PFS costs generates a 79.5% after-tax IRR and a NPV per share range of CAD $5.52-$7.41. If you dare to dream of $4,000 gold without serious cost inflation, those numbers blossom to $15.75-$20.22 for 10% and 5% discount rates. The market is ignoring West Vault because it sees annual production potential of only 70,000 ounces gold, and is concerned that no producer will want to acquire and develop Hasbrouck. Given the recent mood about the future of gold and the gold mining sector compared to just gambling on a Bitcoin ETF, this aversion is understandable. But this is what gives West Vault Mining Good Speculative Value. The key development needed to turn West Vault into a $5-$10 buyout is a secular bull market for gold that fosters expectations for a higher real price for gold, and the decision by a producer to consolidate the region surrounding Tonopah and turn West Vault into the initial mine. West Vault is an example of an ounce-in-the-ground story whose feasibility has already been demonstrated and which is waiting for the right market conditions to attract a buyout in the $5-$10 range.

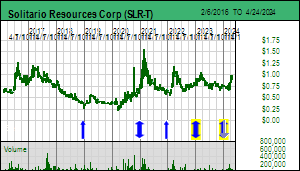

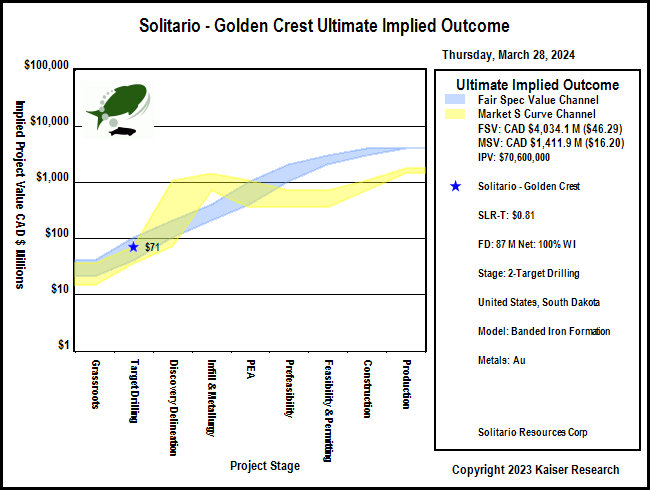

The other extreme is Solitario Resources Corp which is a gold exploration junior waiting for the USFS to approve a drill program for the Golden Crest project in the western part of the Black Hills area of South Dakota. The eastern part is home to the famous Homestake Mine which produced 65 million high grade ounces from basement hosted iron formation rocks, plus another 30 million ounces, some of them hosted in the much younger Deadwood formation sediments. For reasons I have described in prior KW episodes the western half of the Black Hills area received very limited exploration during the past century while the mining action was in the eastern half. One reason is that the cover rock is younger than the Deadwood Formation which hosts the Wharf gold system being mined by Coeur. Another is that the gold Solitario has found at surface is so fine grained it would not have shown up in the pans of early prospectors. So the western half of the Black Hills covered by Solitario's Golden Crest claims was stigmatized as unprospective. This is evident in a LIDAR survey over the entire Black Hills which reveals 150,000 prospect pits on the eastern half, but only 1,500 on the western half.

Solitario is an extraordinary discovery exploration play because since generating Golden Crest in 2020 the company has conducted extensive soil and rock sampling on the property which has yielded multiple areas with high grade gold values in the rocks at surface. The latest news has been on the Ponderosa block to the east of Spearfish Canyon near Hanna where the Geyser and Sleeping Beauty targets have now been recognized as a northeast trending area of interest 3 km by 2 km. The Ponderosa Plan of Operations was applied for in 2023 so these targets will not be permitted for drilling until 2025. For now Solitario is waiting for the final response by the USFS to the comment period objections made about the Golden Crest Plan of Operations. Approval is possible in the second half of April, though in a country haunted by permitting obstacles and anti-mining lifestyle NGOs no discovery is possible until a drill permit is granted.

Solitario has USD $8.3 million working capital and only 87 million shares fully diluted, which means that the implied value of Golden Crest is CAD $71 million at $0.81. If you assume that is fair speculative value for a project still at the target testing stage, the implied outcome is potentially worth CAD $4 billion if there is no further dilution bringing the project to the production stage. In per share terms that translates into a CAD $46.29 price target. Normally it would take 5-10 years to take a project from the discovery delineation stage into production, but resource junior market dynamics include something called an S-curve, also known as the Lassonde curve, which reflects the fact that during the excitement of a new discovery whose limits have not yet been delineated, the market can end up assigning a valuation during discovery delineation that matches what the project eventually ends up being worth when ready to go into production. Add in the fact that Solitario also trades on the NYSE with the symbol XPL, meaning it is eligible for Robinhooders to trade, this stock has the potential for mind-boggling gains. To be ultimately worth $4 billion Solitario will need to demonstrate 10 million plus medium grade ounces which would be quite an accomplishment. What makes Solitario so interesting is that thanks to circumstances created by mother nature Golden Crest could be sitting on a mirror image endowment of what has already been found in the eastern half of the Black Hills. This is what could drive crazy S-curve dynamics, even if the price of gold slumps back below $2,000. For West Vault to turn into a ten-bagger the price of gold needs to keep trending above $2,000; for Solitario to become a ten-bagger it needs to delivery a discovery with grade and size that works at whatever gold price we have.

DCF Model showing AT NPV of West Vault's Hasbrouck project at various gold prices

DCF Model showing AT NPV per share for West Vault's Hasbrouck project at various gold prices

Graphic showing location of Solitario's Ponderosa Plan of Operations

IPV Chart showing implied target outcome if current valuation for Golden Crest is fair

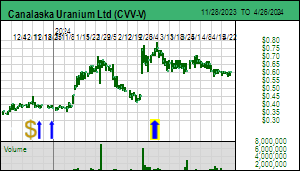

Jim (0:20:06): What do the latest Canalaska Uranium results for the Pike discovery mean?

Canalaska Uranium Ltd released radiometric assays on March 27, 2024 for two additional holes at its Pike discovery on the West McArthur property on the eastern flank of Saskatchewan's Athabasca Basin. The market had a lukewarm reaction to the news because the followup holes to WMA082-04 released on February 28 only stepped 20 metres across the graphitic pelite structure. The importance of hole #4 was that it intersected high grade mineralization at the unconformity between the overlying sandstone and the basement granite within the northeast oriented structural zone which is filled with graphitic pelite. The initial news did not include a section with the #4 hole but the latest news does and it is the combination of the plan and section presentation of the drilling so far which is the real importance of this update. This tells us that Canalaska is starting to understand the geometry of the Pike zone,

Hole #5 was a 20 m stepout to the north across the strike of the graphitic pelite filled structural corridor which yielded 4.5 m of 1.4% eU3O8 which included 2.0 m of 2.78%. As the section shows this hole intersected uranium only in sandstone before hitting basement, which is due to a local fault that downdropped the sandstone northwest of the main structural corridor. I suspect the mood was rather glum when they finished hole #5 - where is that graphitic pelite corridor? These are the sort of local geometry complexities encountered when delineating unconformity style deposits.

With hole #6 they tried only a 10 m stepout and this time did intersect high grade uranium of 11.5 m at 10.84% eU3O8 including 9.5 m as 12.99%. So they know the mineralized portion of the corridor is at least 20 m wide. What we do not yet have are stepouts along the strike of the structural corridor. We also do not have new information about how the uranium mineralization behaves deeper within the pelite zone, though the earlier #2 hole intersected the graphitic pelite at about 40 m beneath the unconformity and nipped 6.3 m of 1.03% U3O8. This hole intersected the pelite zone about 30 metres along strike to the northeast.

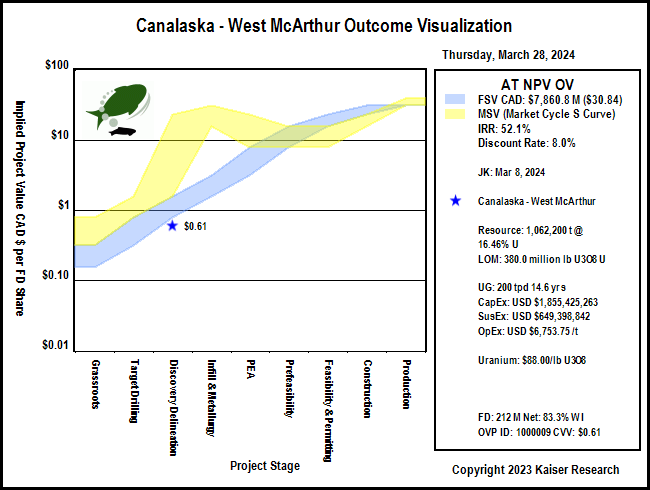

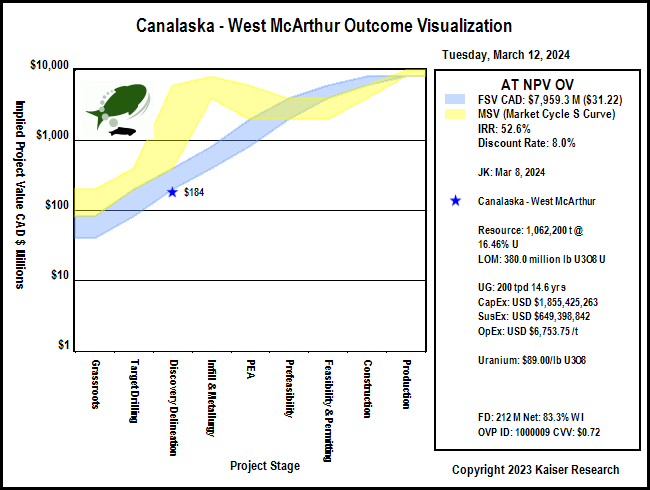

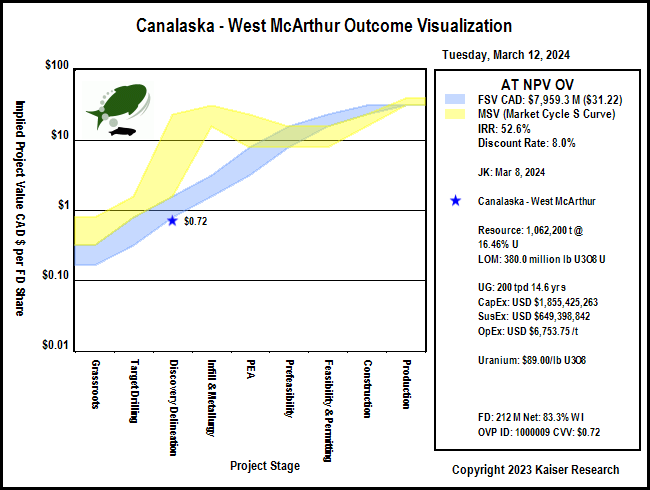

I have created an outcome visualization for a McArthur River clone discovery which imagines what 1,062,000 tonnes of 16.46% U3O8 might be worth at the scale McArthur was developed (200 tpd). Yes these high grade unconformity deposits are small; Pod 2 at 17.3% has a rock value of $33,563 per tonne at $88/lb U3O8. At $88/lb U3O8 price that outcome indicates an after-tax IRR of 52.1% and NPV of CAD $7.9 billion at an 8% discount rate. Based on Canalaska's 212 million fully diluted and 83.3% net interest that converts into an NPV per share price target of $30.84 per share. For that sort of future outcome the $0.61 stock price represents good speculative value, which means that S-curve action has not yet kicked in with the Pike zone.

To get a sense of how close we are to a tipping point for S-curve action I tracked down a paper Mining the high grade McArthur River uranium deposit written by B.W. Jamieson for Cameco. This paper has reserve estimates for Pods 1 and 2, of which Pod 2 is the larger at 577,000 tonnes of 17.3% U3O8. The paper describes Pod 2 as having a strike length of 100 m, height varying 30-90 m and width typically 20 m. The specific gravity of U3O8 is 8.3 but the ore will be lower. If we assume dimensions of 100 m x 20 m x 60 m = 120,000 cu m, and divide the 577,000 t Pod 2 by that number we get a specific gravity of 4.8. Pod 2 was delineated from underground (500-600 m depth). The paper includes a geology diagram showing the complexity of Pod 2.

To create some tonnage context for the Pike there is about 25 m along strike on both sides of this line of 3 holes across the corridor before earlier holes potentially limit the zone. This allows us to assume a scenario of 50 m of potential strike by 20 m width and say 50 m depth as a delineation target. Using 4.8 as a specific gravity that translates into a "pod" of 240,000 tonnes. If you use the McArthur grade of 16.46% U3O8 that translates into about 87 million lbs of U3O8, less than a quarter of McArthur's 380 million lb endowment. So we are not yet at McArthur tonnage scale, and, of course, the average grade remains to be determined.

It is important to keep in mind the intensity of the mineralization and alteration halo of the Pike Zone which is what allows us to dream about a McArthur clone outcome. While a drill is testing other targets at West McArthur until late April, Canalaska has stopped drilling the Pike zone while it awaits geochemical assays to confirm the eU3O8 readings. Canalaska plans to resume delineation drilling of the Pike zone in June. I've added green circles to the plan and section to illustrate the delineation focus for this summer. I've also added blue ovals to the plan view to show what Cory Belyk means when he talks about a "string of pearls" occurring at the unconformity within the graphitic pelite structural corridor. Maybe the roving drill still at West McArthur will hit another pearl, which would be an S-curve tipping point because it would eliminate concerns that the Pike zone is just "this little thing" at 815 m depth.

Canalaska West McArthur Section and Plan showing "string of pearls" potential

Graphic showing complexity of McArthur River Pod 2 (577,000 t @ 17.3% U3O8)

IPV Chart for McArthur River Clone Outcome Visualization

Disclosure: JK owns none of the stocks mentioned; Canalaska and West Vault are Good Spec Value rated Favorites; Solitario is a Fair Spec Value rated Favorite

Kaiser Watch is a weekly audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees which have changed for 2024 as a transition to a $200 per month auto renewal program in 2025. During 2024 individuals can register for a KRO membership at a non-refundable price of $450 for a term that expires December 31, 2024. All active KRO members will be grandfathered to renew annually at $450 on Dec 31, 2024. Sign up here for this limited $450 offer. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch March 22, 2024: Will James Bay Lithium thrive in 2024?

Jim (0:00:00): What is the status of the takeover bid for Azure Minerals and what will it mean for Patriot Battery Metals?

Despite the dampened sentiment with regard to the lithium sector the takeover of Azure Minerals Ltd by SQM and Hancock (Gina Reinhardt) is still proceeding with the shareholder vote taking place on April 8, and if the AUD $3.70 offer is approved, it will be implemented on April 18, 2024. Since drilling started in March 2023 Azure has drilled 248 core holes for 83,219 m and 97 RC holes for 19,267 m in three target areas within the the 9 km by 5 km pegmatite dyke swarm at the Andover project in the western Pilbara region of Australia. So far only 40% of the identified pegmatite targets have been drilled. Target Area 1 is estimated to have a tonnage range potential of 55-105 million tonnes of 1.0%-1.5% Li2O while the more recently tested Target Area 3 has a 25-75 million tonne potential at 1.0%-1.5% Li2O. Azure hopes to release a maiden resource estimate in Q2 of 2024 and a scoping study (PEA) in Q4 of 2024, though we may never see these documents, especially not the PEA, because Azure will have been privatized as a 50:50 JV between SQM and Hancock controlling 60% of Andover while the Mark Creasy group will have the other 40%.

If the acquisition closes at $3.70 per share cash it will value the Andover project at AUD $2.5 billion on a 100% basis, and will inject about AUD $945 million into the pockets of Azure shareholders excluding SQM and Hancock. At the current AUD:CAD exchange rate of about 1.116 that valuation amounts to CAD $2.2 billion compared to the CAD $1.2 billion valuation for Patriot Battery Metal's 100% owned Corvette project at CAD $8.30 per share. On July 31, 2023 PMET released a maiden resource estimate for the CV5 pegmatite in Quebec's James Bay region that came in at 109.2 million inferred tonnes at 1.42% Li2O, pretty much the upper end of the target range that Azure has projected for Target Area 1 of the Andover project. Combining Target Area 1 and 3 Azure is proposing a range of 80-180 million tonnes of 1.0%-1.5% Li2O.

PMET has potential to deliver an updated resource in the 150-200 million tonne range, partly by including a resource for the 4,400 m strike of CV5 of which the maiden resource estimate was based on only 3,750 m strike, marching CV5 another 3.1 km to the southwest where it is expected to join up with the CV13 pegmatite, and a maiden resource estimate for the CV13 pegmatite which has been traced for 2,300 m. This does not include the CV9 pegmatite discovered in late 2023 near the western end of the Corvette property 14 km from CV5 for which initial assays are still pending. And it does not include the CV8, 10, 11 and 12 pegmatite outcrops that will be drilled in 2024. PMET hopes to release an updated resource estimate in Q3 of 2024 and a PFS by the end of 2024.

The fact that SQM and Hancock have stood firm with their $3.70 per share bid for Azure Minerals despite the melt-down in lithium carbonate prices sends us a signal that SQM, a major lithium producer, and Hancock, a new entry in the lithium sector, firmly believe those IEA projections for a required 600% supply expansion by 2030 if the EV component of net zero emission goals are to be met. Those projections, by the way, exclude the possibility of a solid state lithium ion battery becoming reality. Toyota claimed in May 2023 that it had achieved a major manufacturing cost breakthrough for a solid state LIB where substitution of lithium metal for graphite in the anode could double demand. In fact, this doubling in demand is a necessary aspect of the EV future, because unless a carmaker like Toyota can offer an affordable Camry equivalent EV with 1,200 km range on a ten minute charge, the masses in at least North America will never adopt electric vehicles.

For PMET's Corvette project to have a valuation comparable to Azure's Andover project the stock would have to double to $16, just above the $15.29 price at which Albemarle was more than happy to invest $109 million within a week of the CV5 maiden resource estimate. Albemarle, which failed in its effort last year to take over Liontown and its Kathleen Valley project in Australia, has cooled its near term demand projections in light of the slowdown in EV sales, but remains confident about the long term growth of lithium demand. PMET bottomed at $5.77 on February 5 from which it has recovered to $8.30, and I believe it will make a new high ($17.74 was high on June 16) by the end of the year, provided that the rebound of lithium carbonate prices continues.

Map of pegmatite clusters in PMET's Corvette project

Timeline for PMET's Corvette project

IPV Chart for Patriot Battery Metals

Jim (0:10:30): When, if ever, will the James Bay Lithium Index develop an uptrend?

The James Bay Lithium Index was designed to include all companies with exposure to the James Bay region of Quebec on the premise that because of the novelty of the idea that LCT-type pegmatites could have a world class value any junior could make a major discovery simply by putting boots on the ground. The 2023 summer fire closure prevented the biggest prospecting boom in Canada's history from unfolding, with only a portion of the juniors getting any work done, often with only a few weeks in the field. Meanwhile the lithium carbonate price slump, slowing EV sales, and a general market aversion to the resource sector has vaporized market interest in the idea of Lithium Mania 2.0.

Only a handful of James Bay juniors mounted winter drill programs, including the three I made 2024 Favorites: Brunswick Exploration Ltd, Patriot Battery Metals Corp and Winsome Resources Ltd. All three suffered major declines in January when the market feared another coming lithium winter like 2018-2021 when lithium carbonate prices crashed below $3/lb. Winsome and PMET have recovered some of their declines, but Brunswick has yet to rebound. The winter drilling season ends at the end of April and no work will be done in May while the exploration sector pauses for the annual First Nations goose hunting season. The JBLI bottomed on February 13, 2024 when it was down 46% from its start on August 1, 2023. It has recovered modestly but is still down 40%.

I do not expect the JBLI as a whole to show any major improvement until perhaps September because it has 71 members and many of them are either lifestyle juniors who jumped onto the lithium bandwagon or are down and out toiling geologist type juniors like Dios Exploration Inc. We are in a very poor funding environment and we need leaders such as my three Favorites to develop sustained uptrends to breathe life back into the rest. The big question mark hanging over the market is whether or not Quebec and much of Canada will suffer another hot summer of forest fires that shuts down exploration. Many juniors have claims in areas where there is nothing left to burn, but if fires erupt elsewhere airplanes and helicopters will be requisitioned to fight those fires. There will thus not be an anticipatory buildup ahead of the summer exploration season.

PMET I believe can double because it has already demonstrated solid lithium assets that will support a $2 billion plus valuation once the market is comfortable lithium carbonate prices have stabilized. Winsome will benefit when we see the fruit of the winter drilling at Adina, helped out by the drilling efforts of others in this area - a big question mark about Winsome's Adina is whether it will achieve critical mass for standalone development or need to be consolidated with other pegmatites in the area.. Brunswick is the most important bellwether for the James Bay lithium area; it needs to show that drilling has made Mirage bigger and better, and ideally find the source of the spodumeme boulder field which is not explained by the current focus of their winter drill campaign. For the rest to get any upside movement the overall sentiment with regard to the future of pegmatite sourced lithium supply needs to improve.

There has been a lot of negative press about the slowing EV sales, and the Republican Party has made hostility toward electric vehicles and the energy transition a major talking point, but the shift is still happening. Toyota, which steered clear of electric vehicles while developing its hybrid fleet while quietly working on solving the problems needed to offer a truly desirable and affordable EV, is looking like a genius right now. President Biden's recent increase of emission reduction goals does not ban ICE car sales; it merely forces carmakers to lower their average emission footprint. The growing popularity of hybrids among consumers will help companies like Toyota achieve those lower emission goals while it races to deliver a Tesla killer EV for the masses.

On March 5, 2024 Toyota announced a decision to buy out Panasonic's 49% stake in their Prime Planet Energy & Solutions JV they have operated since 1996. This JV has made batteries for Toyota's hybrid and plug-in hybrid vehicles and is moving into making batteries for electric vehicles, a sector Toyota has so far largely shunned. Last October Toyota announced it would invest an additional $8 billion in its North Carolina battery manufacturing facility into which it had already invested $5.9 billion. Although Toyota is a Japanese company, it builds the cars it sells to American consumers in the United States. The American carmakers are going to have to roll up their sleeves over the next five years if they do not want Toyota and Tesla to eat their lunch.

Nissan and Honda, Japan's second and third largest carmakers after Toyota and normally rivals, have already read the writing on the wall and this week announced they are teaming up to develop an EV for the masses. Lithium Mania 2.0 has merely stalled, but the underlying logic that will drive it not only remains intact, but is becoming stronger as carmakers focus on delivering a solid state lithium ion battery powered EV by 2030. For the Canadian hardrock lithium explorers this is a welcome development, because it will take until 2030 to delineate, permit and construct the mines needed to meet demand set to skyrocket at the start of the next decade. PMET, which has $100 million working capital courtesy of Albemarle, will lead the turnaround.

Kaiser Watch is a weekly audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees which have changed for 2024 as a transition to a $200 per month auto renewal program in 2025. During 2024 individuals can register for a KRO membership at a non-refundable price of $450 for a term that expires December 31, 2024. All active KRO members will be grandfathered to renew annually at $450 on Dec 31, 2024. Sign up here for this limited $450 offer. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch March 15, 2024: A staking frenzy in America?

Jim (0:00:00): How is your 2024 Favorites Collection doing so far this year?

The KRO 2024 Favorites Collection was hit hard during January when the sell-off in the lithium sector accelerated in the midst of media handwringing about slowing electric vehicle sales and the crash in lithium carbonate spot prices toward $6/lb. The collection includes lithium juniors Brunswick Exploration Inc, Patriot Battery Metals Corp and Winsome Resources Ltd which slumped hard, dragging the Favorites Index down 19.3% as of February 26. Since then lithium carbonate spot prices have recovered to $7.22/lb, enabling the KRO Index to retrace half its losses so that as of March 15, 2024 it is only down 9.8%.

The relentless sell off this year any time a junior put out a news release, which made the January Effect essentially a no-show, has calmed down amid signs that nickel has bounced off a bottom, copper is threatening to claw its way back above $4/lb, and lithium so far at least has avoided the 2018-2020 lithium winter crash that took carbonate below $3/lb at which price the net zero emission goals for 2030 in so far that they depend on lithium ion battery powered electric vehicles has a near zero chance of being met.

Still drifting lower are the magnet rare earths such as neodymium which is caused by China's weaponization of its dominant supply situation. China has also indirectly weaponized nickel by bankrolling Indonesian smelting capacity fired by dirty coal. In the case of nickel western producers are now urging the LME to create a "green" category to distinguish nickel supply with a low carbon footprint. Uranium's sharp rise since mid 2023 has peaked, with the price falling into the $80-$90/lb range; if $80 can hold as a floor for uranium it will be good for uranium juniors.

Copper is starting to benefit from a growing realization that as the AI Dream cranks up in its pursuit of innovation breakthroughs the resulting surge in energy demand will exceed the existing capacity of energy infrastructure. Building new power plants and expanding the transmission grid would not sharply boost copper demand (high tension transmission wire is made of aluminum with a small copper core), but the projected AI data centre near term energy shortages is helping focus attention on the IEA's projection that if EV net zero emission goals for 2030 are to be met, the world will need 50% more copper supply. Copper, while not part of the EV battery, is a much bigger part of an EV than an ICE car. But what industrial policy has had its head in the sand about is that the existing energy infrastructure is woefully inadequate to meet the charging needs if carmakers like Toyota deliver an affordable EV whose range and charging times meet the needs of ordinary consumers (think a Camry EV with 1,200 km range and 10 minute charging time). This type of EV that appeals to the North American masses will not be available before 2030, and there are plenty of recent skeptics who think that is a pipedream. But if a serious push for energy infrastructure renewal and expansion gets underway to accommodate projected AIU Dream needs, it will also provide the charging foundation for mass adoption of EVs during the 2030s. So producers and the market are starting to think that now is a good time to explore for copper deposits, especially in jurisdictions that will remain secure, which cannot so easily be assumed for Latin America.

The big surprise during the past few weeks has been the steady rise in the price of gold to new records without any obvious explanation. The rise stalled the past week when US CPI came in at 3.2% for February, slightly higher than expected. The result has been a change in expectations that interest rates will begin to decline during 2024, which should have made gold which generates no income more attractive. Gold's price rise is not being driven by retail investors because so far this year the GLD ETF has managed to lose 2 million ounces, but on Friday March 15 the GLD ETF registered a very large single day gain of 481,494 ounces. It is assumed that retail investors have been selling their gold ETF holdings in order to chase into BitCoin which itself has made a record high courtesy of Wall Street getting approval for stock exchange listed BTC ETFs that spare momentum gamblers the anxiety of owning a crypto wallet and having to trade through one of those cryptocurrency exchanges. The fact that both gold and BitCoin are making new highs may seem to be a paradox until one considers that the buying is coming from two different audiences. There is the smart money which knows that BitCoin is a digital mirage that refers only to itself, is priced in US dollars, is mainly used to facilitate the transfer of criminal proceeds, and represents a usage energy liability that will in future compete with AI and EV electricity demand. This smart money also knows that above ground gold is stored energy, the real cost of extracting what remains in the ground is outpacing the price of gold, and if the election outcome results in the fragmentation of the world into everybody for themselves autocracies, the US dollar will see its status as the sole global reserve currency erode quickly. The dumb money is buying BitCoin because the trend is their friend and the idea that nobody will be MAGALand's friend just isn't a concept. However, it is too soon to assume that $2,000 has finally been established as a floor for gold rather than a ceiling it can never stay above for long.

The absence of a clear reason for gold's uptrend explains why the three gold related juniors in the 2024 Favorites Collection have not yet developed uptrends. Arizona Gold and Silver Corp is still waiting for a BLM permit that will allow it to test the bulk tonnage potential of its Philadelphia project in Arizona. West Vault Mining Corp, a shovel ready proxy for a higher real gold price is still treading water in the $0.90-$1.00 range. And Solitario Resoures Corp is still waiting for a permit that will allow it to drill its Golden Crest project in South Dakota. The longer gold can hold above $2,000 the more these gold-focused Favorites will attract attention, with two of them potentially benefiting from a near term event unrelated to the price of gold, a permit that lets them start drilling for a gold discovery that works at the existing gold price.

KRO 2024 Favorites Index

Table of 2024 KRO Favorites

Daily KRO 20245 Favorites Performance

GLD ETF Daily Changes in Ounce Holdings

Key Metal Price Charts

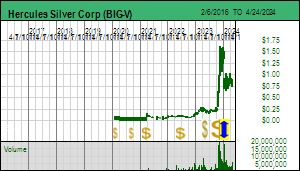

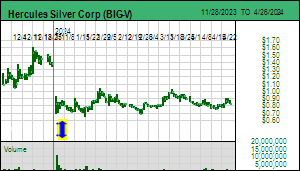

Jim (0:03:58): What are the implications of the final results Hercules Silver released for last year's drill program?

Hercules Silver Corp released the final results from the 2023 drilling on February 28, 2024 which the market liked for a couple days because it had fancy silver grades but then became disgruntled when it learned that drilling would not resume until May or later because of ground conditions. The stock has since recovered as the market began to appreciate that the meat in the final results news release was not the high grade silver-lead-zinc mineralization beneath the Hercules Adit near the contact between the "upper plate" rhyolite that hosts the silver-lead-zinc veins and the "lower plate" andesites that host the copper mineralization, but rather the geological discussion about a reinterpretation of the fault history of the area, much of which has been obscured by a thin veneer of much younger flood basalts.

An IP survey done in 2022 had revealed a substantial 1 km long IP chargeability anomaly beneath the known Hercules silver mineralization into which 400 hundred holes have been pumped since 1965, including some by Anne Mark's Anglo-Bomarc during the bull market of 1978-81. Hole 23-05 delivered in October 2023 confirmed a substantial copper porphyry system beneath the silver zones with high enough grades to support underground mining. This attracted a $23 million financing from Barrick Gold at a premium to the market (Hercules currently has $27 million working capital). But the followup holes drilled laterally and to the southeast of the IP anomaly had lower copper grades, and when released at the start of 2024 caused the stock to tank, enabling me to add Hercules Silver Corp (soon to be renamed Hercules Metals Corp) to the 2024 Favorites Collection. The company has since expanded the IP survey and stated that its footprint now extends several kilometres, but it has not published graphics for the new survey.

With the help of Barrick Chris Paul's team has done a lot scientific geology such as age dating and structural analysis, which has led to two important conclusions alluded to in the recent press release. One is that this porphyry system underwent multiple mineralizing phases, which is important for building big and rich deposits because successive fluid pulses remobilize mineralization from earlier phases and redeposit it in greater concentrations. The other is that the rhyolite "plate" that hosts the high grade silver was thrust from the northwest in a southeast direction over the andeslite "plate" that hosts the copper mineralization. This sort of high grade silver-lead-zinc mineralization one could expect at the peripheries of a porphyry system, but there is no zonation continuity between the rhyolite silver host and the underlying andesite copper host. The silver mineralization has been decapitated from the intrusive center that created it. Hercules had marched the drills along the length of the IP anomaly which turns out to have been the wrong direction. The proper direction appears to be in the northwest direction under cover rocks where no work has previously been done. Although Chris Paul would not spell out details, reading between the lines the IP anomaly extends beyond the Hercules Adit a couple kilometers.

So why the secrecy? The realization seems to have emerged among majors like Rio Tinto and Barrick that a 200 km trend of very fertile copper porphyry intrusions is located in western Idaho largely hidden by younger basalt cover rocks. Hercules has only a 2 km area of interest surrounding the existing property, beyond which Barrick is free to stake whatever it wants. And while Barrick may have seen the new IP survey data and perhaps even helped with the interpretation of the implications, there is no point in sharing those insights with other copper producers such as BHP, Rio Tinto and Freeport. Idaho, like the rest of the United State still requires old fashioned post staking so this is expensive and time consuming, plus those areas under state jurisdiction have different rules than BLM land. There is an old-fashioned copper focused staking frenzy unfolding in America!

Unlike in Arizona where major copper discoveries will be deep blind ones like Bell Copper Corp is chasing at Perseverance and Big Sandy in the hope of finding another Resolution scale deposit, these targets in Idaho, while likely still requiring underground mineable grades above 0.6% Cu, will be easier to discover and delineate if this trend hypothesis proves correct. The Hercules story is important because the big picture concept is that old mineralized systems which are typically dismissed as dead horse recycling plays can be evidence of something much bigger going on beneath the surface. All it takes is a fresh geological perspective, a willingness to think outside the box, and engage in extra data gathering that includes drilling geological scout holes. This is something the lifestyle juniors cannot accomplish, and when the resource juniors are pressed into service as the new heroes which will secure new metal supply in secure destinations, the lifestyle juniors will be left stranded at the dock as the serious boats put out to sea in search of whales.

Jim (0:10:13): What is the latest news from Solitario Resources Corp about its Golden Crest project in South Dakota?

Solitario Resources Corp provided an update on February 27, 2024 ahead of PDAC which highlighted a new gold zone called Wild Rose which appears to be part of a 4 km northeast trend extending from the Downpour showings first reported in 2021. Solitario applied to the USFS in 2022 for a plan of operations that would allow it to drill targets generated by surface sampling on the Golden Crest project in the western part of the Black Hills National Forest in South Dakota. The property boundary extends almost to the Wyoming border, and when I asked if there was a reason to avoid Wyoming, the answer was that there is a structural break in the rocks that happens to coincide with the Wyoming-South Dakota border, to the west of which the geology is not prospective for gold mineralization.

The 75 day comment period following the FONSI ruling by the USFS in December 2023 with regard to the first plan of operations application Solitario filed in 2022 has concluded and the USFS is preparing its responses to those comments that have standing. Solitario's COO Walt Hunt thinks the USFS may be finished by mid April, which is still a month ahead of when Solitario in terms of physical access could hope to start drilling at Golden Crest. The USFS has published a project location map which outlines the prospects for which drill permits are sought. On March 18, 2024 (after this KW episode was recorded) Solitario published an update about the Geyser Zone which it first reported on in February 2024. Once again surface sampling has yielded multi-ounce gold values.

What is intriguing is Solitario's announcement that it has filed the Ponderosa Plan of Operations which it describes as being a non-contiguous part of the Golden Crest project which the December 2023 presentation depicts as 3 distinct claim blocks. When I google Ponderosa POO I get a USFS splash page which contains no information other than the approximate location, which turns out to be east of Highway 85 which tracks Spearfish Canyon. Although Solitario's map shows 3 claim blocks, a medium sized one to the north, a small one to the northwest, and the main large one, the latter is in fact a couple blocks because Solitario had the wisdom not to stake claims over sensitive areas like Spearfish Canyon.

At PDAC I took a photo of a dull looking rock which assays just under 1 opt gold, a testament as to why this western part of the Black Hills has 1,500 prospect pits (based on LIDAR analysis) compared to a hundred times as many in the eastern half where Homestake yielded 60 million ounces out of a 90 million ounce endowment for the area. CEO Chris Herald tells me that no claims have been staked since the end of 2022, and admits they were surprised to discover the Geyser Zone and were obliged to expand the land package. It turns out that the new Wild Rose zone is outside both the original Golden Crest POO and the Ponderosa POO applied for in 2022. Based on the prospect pit locations in the original Golden Crest POO and the recently revealed location of the Ponderosa POO the impression is created that the middle of the land package is an unprospective doughnut hole. That, however, is an artifact of the permitting strategy which has limited Solitario's surface sampling focus to areas accessible by logging roads and where bedrock has been exposed thanks to logging.

Last year Solitario conducted an IP survey along two 11 km lines which yielded a weak, 2 km wide chargeability high projected around a depth of 400 m just above the Precambrian basement where the Lower Deadwood formation that hosts the Wharf gold system, a 10 million ounce system with high grade zones within a lower grade envelope whose high grade was plucked out 120 years ago, with the rest being open pit mined since the 1980s after heap-leaching technology was invented. If something similar is present within this doughnut hole ay Golden Crest it would have to be underground mined, but with the high grade intact such a system might run 2 g/t gold or better which is $129 rock at $2,000 gold. Both this deep IP target and Wildrose will have to wait for future plan of operation applications. If the permit is granted drilling would start at the Downpour target for which Solitario has provided a conceptual target cartoon which shows a laterally extensive Wharf style target within the Deadwood Formation just above the Precambrian basement, and gold mineralization within the feeder structures which they are tracing with high grade surface values. Oddly, during the past week Solitario came under selling pressure through its NYSE listing which may have been a forced liquidation by an institutional shareholder. Such liquidity on the bid side will be a thing of the past if the USFS decides to confirm the Golden Crest POO.

Kaiser Watch is a weekly audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees which have changed for 2024 as a transition to a $200 per month auto renewal program in 2025. During 2024 individuals can register for a KRO membership at a non-refundable price of $450 for a term that expires December 31, 2024. All active KRO members will be grandfathered to renew annually at $450 on Dec 31, 2024. Sign up here for this limited $450 offer. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch March 8, 2024: The California Gold Rush Metaphor

Jim (0:00:00): Why do you think the AI Dream will not suck the oxygen out of the resource junior room like the Dot-Com Bubble did in 2000?

At the Metals Investor Forum in Toronto on March 2, 2024 I gave a presentation called Geopolitics, Energy Transition and the AI Dream in which I argued that while my two key themes from the past couple years, the raw material supply dependency of the Global West on the Global East, and the additional critical metal supply requirements of the energy transition's net zero emission goals for 2030, were not lighting a fire under the resource sector, the massive energy consumption of the AI Dream when it really gets cranking over the next few years will spark a new secular bull market for the resource sector. If this starts to happen we will see a five-fold increase in most of my bottom-fish collection just to adapt to a new reality where the resource juniors are seen as the key to turning the AI startup dream into reality, and then be positioned to deliver further 5-10 baggers when they individually deliver a discovery. It will take a distributed collective of hundreds of serious juniors properly capitalized to deliver the dozens of new discoveries in secure jurisdictions like Australia, Canada, United States and Scandinavia which the majors buy out and turn into mines. But you put your finger on a reality which has become a millstone for the resource juniors, namely language like 10 bagger upside.

After my MIF presentation I was dwelling on my experience nearly a quarter century ago at PDAC 2000 when dot-com stocks were going to the moon while resource juniors lagged in the dumpster. The hope we had was that the dot-com bubble would be transformational for the global economy, which in turn would spur raw material demand and unleash an exploration boom that would drag the resource juniors out of their post-Bre-X bear market. In fact, the dot-com bubble peaked during March 2000 and the resource juniors remained in a bear market until mid-2003 when the world began to notice the rise of China which launched a raw material super cycle that lasted until 2011 despite the 2008 interruption caused by the financial crisis engineered by Wall Street.

The resulting resource junior bull market was very different from the ones that defined the Canadian resource juniors from 1970-2000, namely price gains due to a major discovery or anticipation of such a discovery (Hemlo, Eskay Creek, Ekati, Voisey's Bay). The winners of the 2003-2011 super cycle bull market were largely juniors which acquired deposits in the newly opened third world frontiers (emerging market countries) that were marginal at the time of discovery or compromised in some manner by the political situation. Ross Beaty had spent the 1997-2002 bear market tracking down such deposits in Latin America on speculation that the emergence of post-Mao China with the biggest population in the world in the context of globalized trade would increase raw material demand by an order of magnitude that would generate real price gains for metals after decades of real price decline. This prediction became reality and the approach of dusting off old deposits and demonstrating their feasibility in terms of new super-cycle driven real metal prices became known as the "Lumina Model". About 200 juniors ended up disappearing through buyouts worth about $100 billion as the majors, which did not acknowledge the super-cycle until 2006, scrambled to expand their mine portfolio.

Ironically, this feasibility demonstration based boom was based on the very reason the resource juniors could not compete against the dot-com startups back in 2000: the value of a discovery defined by the discounted cash flow model (DCF), namely the present value of the cash flow in each year of a mine's life. Institutional capital loved the China super-cycle because it could see the resulting higher metal prices, the tonnage and grade of those forgotten deposits was already roughly understood, and the cost of building and operating a mine were reasonably understood. The project still had to be marched through the various stages of the exploration-development cycle, but the size of the eventual price could be quantified. The China super-cycle bull market was driven much more by number-crunching than discovery exploration. Eventually the mining industry proved far more successful at mobilizing new supply than needed, the United States adopted a strategy of quantitative easing rather than fiscal stimulus driven infrastructure renewal, and global growth slowed. The result has been a bear market for resource juniors since 2011 with only a few short-lived rallies in 2016 (when gold looked like it was developing an uptrend), H2 of 2020 (when gold breached $2000 in view of pandemic largesse), and in early 2022 (when energy transition goals gained traction and Russia's invasion of Ukraine destabilized metal supply). In 2023 the energy transition faltered and Russia's ability to bypass sanctions cooled concern that the growing geopolitical conflict between Global West and East would come to hunt the Global West whose economy was 60% of global GDP in 2023.

The reason back in 2000 it felt like the dot-com bubble was sucking the oxygen out of the PDAC convention center was that the quantifiable upside limit of a junior's potential discovery could not compete with the unlimited upside of a dot-com startup in a winner take all dynamic where each contender is the potential Amazon style winner until proven otherwise. Every resource junior's discovery is a thing in itself with lots of things potentially blocking it from ever becoming a mine. That was the problem in 2000 and I wondered if it would be a problem again today as countless AI startups get launched, any one of which could deliver fabulous breakthrough discoveries and until it didn't could be priced by the market as if it could. Unlike an exploration play where fundamentals are always staring in your face declaring what is not yet there, you don't need to know anything about the quantitative or even qualitative fundamentals of an AI startup to make money. You just need to be a momentum gambler riding the uptrend.

The resource juniors cannot compete against this type of junior and they have been in a secular bear market for more than a decade as winner take all alternatives like crypto and cannabis came along. Despite resource juniors struggling to regain relevance since 2011, and a general glumness about the resource sector overall, PDAC was shockingly busy (26,925 attended). I am still puzzled by this disconnect and can only explain it by the paucity of delegates wearing the $25 Exhibit Day Pass and the abundance of All Access passes which cost $400 or more depending when you bought it. Investors, unless they are aged 65+ and qualify for a $75 All Access senior pass, buy the Exhibit Day pass, but even that is misleading because individuals flogging services to the exhibitors also buy the cheap day pass. The vast majority of delegates at PDAC are industry and government employees whose bosses paid for their All Access passes. The abundance of delegates is thus an illusion about the health of the resource sector. For me my three days at PDAC were extremely productive; of the hundred or so juniors I had flagged to visit, I managed to make contact with about half and have a notebook full of ideas to follow up on during the coming weeks.

Despite my cynicism about the basis for the PDAC attendance I did emerge with a sense that 2024 will prove to be a turning point. Currently I am still offering a $450 KRO membership expiring December 31, 2024 whose members will be grandfathered to renew at that rate. My plan is to shift to a $200 per month auto-renewal membership in 2025, but I may stop the $450 rate and start the new rate earlier if a resource sector bull cycle emerges this year. The basis for my new found bullishness is the realization that the resource juniors with their finite upside limit should not try to compete with the sky's the limit AI startups. The challenge is to teach the audience how open-eyed fundamental outcome gambling works compared to blind momentum gambling. The upside valuation limit curse of an economic deposit also is the basis for quantifying where a project is relative to a potential outcome and using the uncertainty ladder of my rational speculation model to price the junior based on the stage of the project and what the revealed fundamental results indicate. What changes in the news flow from an AI startup? Nothing except hyped up assertions of progress in the case of technology stories and bigger money losing revenues in the case of information based services. Momentum gambling in AI Startups is for the true believers who occupy the bottom of the Belief Horseshoe, whereas fundamental outcome gambling is for critical thinkers who occupy the upper half of the Belief Horseshoe.

After giving my MIF presentation on March 2 I had a conversation with somebody whose thinking about the resource sector was along similar lines as mine. Somehow our conversation caused me to think about the California gold rush as a metaphor for the AI Dream. The AI startups are the gold-seekers passing through San Francisco on their way to the American River where any one of them could become fabulously rich. Most won't but until they don't each is a contender. But to have a shot at being successful each forty-niner needed to buy a pick and shovel along with other gear in San Francisco. The amount of money the San Francisco outfitters could make was a function of how many forty-niners traveled to the gold fields and how long the gold fields yielded a gold bounty. There was quantifiable limit as to how rich the outfitters could get, which was never as high as the fabulous riches collected by the successful gold-seeker.

The resource junior industry needs to sell itself as the pick and shovel outfitters for the AI startups. This was hard to do with the dot-com startups because those didn't need anything the resource juniors could provide. The AI Dream, however, relies on computation, which, unlike information delivery via existing communications infrastructure, is extremely energy intensive, especially at the scale being proposed. But the AI Dream has a problem, and that problem was the essence of my MIF talk. Once AI really gets rolling, and starts crunching organic and inorganic molecules, reducing the infinite configurations to a manageable set of possibilities that are stable and have potential properties with measurable benefits in all aspects of the physical world (I'm assuming the mental is a function of the physical), and the physical prototyping to confirm those properties starts to deliver those benefits to humanity, the AI computation demand will go through the roof as AI startups start hunting down such possibilities. Forget about Chatgtp and the rest stealing all the jobs from white collar workers in the existing knowledge economy. The upside for humanity from AI resides in the generation of new knowledge. But the existing energy infrastructure cannot generate such a new demand nor deliver it. It needs to be expanded and upgraded. This requires raw material inputs, much of it metallic. In its Electricity Report January 2024 the IEA projected a doubling to tripling of electricity demand for 2026 by data centres (AI) and crypto-miners, but that is likely a major under-estimate if the AI Dream starts delivering that make the world more prosperous.

The energy transition goals have made it clear the world needs more of certain metals which will take at least 6 years to mobilize. But not much is being done to make this reality. Why not? One reason is that the boomers who control most of the capital are not excited about making the sacrifices required of the energy transition because most will not live long enough to find out if it made a difference. The other is that because energy transition strategies are staged (ie the EV adoption rate curve which I argue is not going to be linear but more like the S-curve in the exploration-development cycle), the need to do something about it can easily be postponed. Although the talking heads are brimming with urgency, those with capital not so much.

The geopolitical conflict between Global East and West is something everybody wants to ignore and assumes will disappear as everybody gets back to the globalization concept of making money wherever is best possible. Most people have no idea how dependent the Global West is on raw material supply from the Global East, and to a large degree the Global South which the Global West believes wants to become part of the Global West club. I do not see the autocracy basis of the Global East dissolving into the democracy basis that still underpins the Global West. I see a greater risk of the democracy basis dissolving into autocracy and the world splintering into competing thug nations (ie MAGA Land against everybody else). While I am optimistic that will not happen, I strongly fear the geopolitical conflict will get hot. And when that happens the Global West has a huge metal supply deficit which it will have to solve through domestic sources because in all likelihood the Global South will be either unstable or will align itself with the Global East. These two themes have been my core narrative for the past few years but its implications have not translated into a secular bull market for the resource juniors which I have been forced to acknowledge thanks to the severe slump in funding and market interest in the resource juniors, along with evidence that the Global East's weaponization of metal supply as a loss leader is undermining the profit foundation of Global West sourced metal supply.

My recent epiphany about how the AI Dream is not another Dot-Com bubble sucking the oxygen out of the resource junior room, but rather, thanks to its enormous future energy demands, an argument for mobilizing the resource junbiors as "picks and shovels" providers, has me excited. At any point in time a massive panic attack could jolt the Global West out of its stupor, perhaps driven by Russian nuke detonated in Ukraine, or people waking up to the energy consumption needs of the AI Dream which is no showing up in mainstream as a concern. When this happens there will be a public outcry to renew and expand America's energy infrastructure. That would crank the national debt into the stratosphere. Will the Boomers, lusting about AI innovations whose biomedical implications could extend their lives, or other innovations boost prosperity in the near term, object like they have about the energy transition related debt expansion?

No, it will be their children and grand-children who will object. They will argue, how dare you saddle us with all this debt while nothing serious is being done about net zero emission goals? Screw you! But hey, let's make a deal. We will buy in to this national debt expansion if you agree to make net zero emission goals part of the infrastructure renewal spending so that we will benefit if indeed it turns out to have made a difference in slowing global warming.