Hello Guest User, You are visiting this website from a computer with an IP address of 172.69.7.184 with the name of '?' since Tue May 7, 2024 at 5:42:42 PM PT for approx. 0 minutes now.

The KRO Blog is where unrestricted content is posted such as Kaiser Watch, material produced by third parties such as the as Investing News Network, and Metal Investor Forum conference links.

Kaiser Watch is a weekly audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees which have changed for 2024 as a transition to a $200 per month auto renewal program in 2025. During 2024 individuals can register for a KRO membership at a non-refundable price of $450 for a term that expires December 31, 2024. All active KRO members will be grandfathered to renew annually at $450 on Dec 31, 2024. Sign up here for this limited $450 offer. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch April 26, 2024: Is a Colonial Coal buyout imminent?

Jim (0:00:00): Is Colonial Coal any closer to getting bought out for its metallurgical coal assets in northeastern British Columbia?

This is the third year in a row that I have had David Austin's Colonial Coal International Corp as a KRO Favorite based on the expectation that it will receive a buyout offer in the $5-$10 range based on its 100% owned Huguenot and Flatbed projects in northeastern British Columbia. Colonial Coal took these projects through the PEA stage of feasibility demonstration in 2018 and 2019 using 1.30:1 CAD-USD exchange rate and metallurgical coal base case prices of USD $172/t and $164.80/t for Huguenot and Flatbed respectively. At a 7.5% discount rate that generated an after-tax net present value of CAD $1,516 million for Huguenot and CAD $898 million for Flatbed. During 2023 Teck averaged USD $297/t for its metallurgical coal production, nearly double Colonial Coal's base case price. The cost assumptions of the PEAs will need to be updated to reflect the post-covid inflation, so if one trades off the higher cost with the higher price of metallurgical coal it is reasonable to take the combined PEA NPV of CAD $2.4 billion seriously, which, based on 194 million shares fully diluted, translates into $12.44 per share. Contemplating a buyout in the $5-$10 range is thus a reasonable speculation.

Since completing the PEAs Colonial Coal's chairman and CEO David Austin has been shopping the company around for a buyout by a steelmaker in need of security of supply. Coal is a dirty word these days and most people do not understand the difference between metallurgical and thermal coal, causing some metallurgical coal producers such as Teck to prefer calling it "steel-making coal" so as not to get tarnished by the anti-fossil fuel brush. Metallurgical coal is used in making steel from iron, and this process does generate carbon dioxide emissions just as does the burning of thermal coal to generate energy. In fact steelmaking contributes about 7%-8% of global CO2 emissions. There are alternative ways to make steel, but they are substantially more expensive and the world is not ready for higher steel costs, especially Global South nations such as India and Global East nations such as China. Steelmakers in jurisdictions where it matters deal with their CO2 emissions by purchasing carbon offsets.

There are, however, energy alternatives to thermal coal which have zero carbon dioxide emissions and are non-polluting such as renewables and nuclear. Even worse for thermal coal is the fact that natural gas which is non-polluting not only generates less carbon dioxide per energy unit than thermal coal, but in places like North America is cheaper than coal. Unfortunately there are countries like China and Indonesia which have abundant coal and little interest in the cost of mitigating CO2 emissions and other pollutants generated by burning coal (in steel-making whatever other elements are present in metallurgical coal either end up in the steel or the slag). The global nickel market is now under pressure because Indonesia is happy to burn dirty coal as its source of energy for extracting nickel from its laterite ore.

Even though there is a distinction between metallurgical and thermal coal, companies such as Teck which produce both base metals and metallurgical coal are penalized by investors who want their portfolio to exclude exposure to fossil fuels that generate carbon dioxide. In February 2023 Teck proposed to split itself into two companies, Teck Metals Corp which would hold all the base metal operations, and Elk Valley Resources Ltd which would hold its Canadaian metallurgical coal operations. In April 2023 Teck disclosed that it had received and rejected an unsolicited paper bid from Glencore which valued Teck at USD $22.5 billion. Glencore's plan was to combine Teck's metallurgical coal division with its own thermal coal division (26 mines) and split that off into a separate company so that Teck shareholders would end up with shares of Glencore holding the base metal and oil operations and shares of the coal spinout.

In December 2022 Glencore's effort to permit the Sukunka metallurgical coal project in northeastern BC was definitively rejected, which raised hopes that in 2023 Glencore might consider a bid for Colonial Coal's projects which do not have similar caribou habitat and First Nations issues. That hope faded when Glencore decided to go after a much bigger prize. A week after Teck's initial rejection Glencore came back with a revised bid that allowed Teck shareholders to opt for cash instead of stock in the coal spinout, which Teck management also rejected as undervaluing the company. Unfortunately for management a few weeks later its own shareholders rejected the proposal to split Teck into separate base metal and coal companies. In November 2023 Teck agreed to sell its coal division to Glencore for USD $6.9 billion. That transaction is expected to close in Q3 of 2024 if it receives regulatory approval.

Colonial Coal has traded in a $2.00-$2.50 range so far this year on daily volume ranging 50,000 to 150,000 shares but has not issued any meaningful press releases since December 2022 when the stock was being trashed in the wake of the negative Sukunka decision which the market interpreted as a thumbs down for all future metallurgical coal mines in northeastern British Columbia. I discussed the fallout from the Sukunka denial in KW Episode January 26, 2023. On Friday April 26 the stock jumped $0.52 to $2.69 on 459,300 shares, the biggest move and volume in more than a year. This prompted some KRO members who follow Colonial Coal to speculate in my Slack forum if somebody was front-running an imminent buyout offer.

Unlike the base and precious metals sector where a producer cannot offer too big a premium for a resource junior with an advanced project, which is a problem for many juniors trapped in this endless bear market lacking the sort of institutional audience which has the firepower to lift a stock into the desired buyout range, potential bidders for strategic assets involving less conventional metals and minerals do not have this problem. Is Colonial Coal any closer to a buyout?

Today's move was not caused by traders front-running inside information but rather by informal news that Citi Bank has agreed to become Colonial Coal's advisor with regard to a potential buyout. Citi Bank is the sort of entity that advises Glencore scale companies, not Canadian listed resource juniors. This does not mean a buyout is imminent, but it does mean that the expressions of interest David Austin has been receiving from tire kickers during the past few years may have become serious. Indian steelmakers have been a source of potential interest, but things like Trudeau's spat with Modi about Sikh assassinations chilled that potential last year. But now that Glencore's acquisition of Teck's metallurgical coal assets is plodding through regulatory approval, it may have dawned on potential bidders that Glencore itself might seek to expand its metallurgical coal production capacity in Teck's backyard. There could be a new sense of urgency to move sooner than later.

General Map showing locations of Huguenot and Flatbed projects in NE BC

Map showing locations of met coal mines in NE BC

Highlights of 2018 PEA for Huguenot

Highlights of 2018 PEA for Flatbed

Jim (0:12:40): What did Brunswick's first results for winter drilling at Mirage tell us?

When Brunswick Exploration Inc released initial drill results on April 25, 2024 for its winter drill program at Mirage I was taken aback by the nature of the disclosures which seemed to suggest that Mirage was shaping up to be little more than a mirage. What struck me as odd was that although Brunswick drilled 35 holes during the winter program, I could only count 22 holes on the drill plan the company provided. And except for the 4 holes for which assays were reported, none of the other new hole locations had numbers. Since the company follows the practice of numbering holes in the sequence drilled following the prior year's holes, which totaled 36 holes, I expected to see holes #37-#71 on the map. On the assumption that holes are logged and shipped for assaying in the order completed, I was surprised that the press release included assays for holes 49, 57, 58 and 60. What were the results for 37-48, 50-56 and 59? Were they blanks or very short intervals or low grades, with the result that Brunswick only reported 4 holes, of which #57 and #58 were not exciting at all? Fortunately Brunswick's CEO Killian Charles did return my call and provided plausible explanations for the strange appearance which has left me bullish that when the final results arrive over the next month or so the scale of Mirage will have increased from last year, with plenty of further growth left when drilling resumes in July.

First off, the 22 drill holes marked on the drill plan map are actually drill pad locations, some of which had several holes drilled at different angles but in the same direction. This makes it impossible to show the traces since they stack on top of each, which is why we saw only one drill hole trace per "pad". They did not number the holes not yet assayed because it would have made the drill plan far too busy. The "hole" pattern we see is complete.

They also had two rigs until the end of March, and although they are following last year's numbering sequence (ie last hole is #71), we could not infer anything from the numbering in terms of what they were seeing in the field and responding to as far as which pad the rig goes to next. A rig may have problems with a hole while the other rig has none, and since they are drilling in different areas the numbering sequence reveals no information as would be the case when a company is using a single rig as a vectoring tool probing the third dimension and deciding on that basis where to drill next.

With regard to why assays were reported first for holes 49, 57, 58 and 60, they had some logistical issues with the shipping order, so that it is not a case of first drilled first assayed. However, #60 which steps 250 m northeast of last year's MR6 dyke limit at the boundary of the inlier claims optioned 75% from Electric Elements and for which Brunswick recently bought out the 0.5% royalty Sirios Resources Inc acquired when it sold those claims to Virginia Mines, was important and I believe was given priority. The reason it was important is that they wanted to chase the MR6 dyke northeast by drilling through the ice. There is a narrow northeast oriented lake which has bulges at the southwestern and northeastern ends which makes it look like a barbell. As it turned out, winter was warmer than expected, and the drill crew's efforts at ice thickening never achieved a comfort zone.

The 6 holes within the area I have highlighted with a blue circle are within the inlier claims and ended up being drilled from shore. This batch of holes are the most important in terms of expanding the scale of the discovery because it extends the strike of the "central" zone (MR3 & MR6) 1 km to the northeast. Killian resisted my efforts to tease out confirmation that drilling in this direction was successful beyond #60 which had two intervals of 18.4 m at 1.03% Li2O and 31.6 m of 1.71% Li2O, but in the next sentence he was talking about the outcrop 3 km to the northeast on 100% owned ground which is on dry land that can be drilled during the summer. If the dyke is confirmed under the lake they will consider barge drilling this summer.

He has also confirmed my conclusion that they see the lake separating the "north" and "central" zone has an anticlinal fold axis for what was once a continuous dyke but which has now been split into north and south limbs, with the north limb dipping north and the south limb dipping south. The southern limb has a shallow dip, so those holes I have circled in orange are potentially important. With regard to the 200 m gap between MR 3 and MR6 which each have a small stepout fence of holes, the reason they did not infill this gap was because it can be drilled during the summer. The focus during the winter was to test targets where access during winter is easier.

When I talked to Bob Wares at VRIC in Vancouver he was dismissive of geophysics as useless for targeting pegmatites, including gravity which Winsome claims has been very helpful. He still is of this view, but Killian told me that in late January they started doing gravity and that the area drilled by #60 has a gravity low, so the team is of a different opinion from Bob. The test will come later this summer when they tackle the barbell at the southwestern end of the lake which has a similar shape to that at the northeastern end on the inlier claims where I have my fingers crossed about those 6 holes in the blue circle. And it has a similar gravity low anomaly. A skeptic like Bob would argue that lakes distort gravity data and the correlation of the dyke with a gravity low is just coincidence.

When Killian mentioned they were eager to test the southwestern barbell this summer because of the gravity low, I pointed out that the most recent map they published showing the location of outcrops and boulders shows nothing down ice from this target. Killian explained that this area is largely overburden covered but they did find spodumene bearing boulders, just not giant ones like within the 3.5 km train of micaceous pegmatite I have circled in green.

As far as this 3.5 km boulder train is concerned, the last two holes of the season are those southwest of the "south" zone (MR-4 dyke) and were drilled in opposite directions as scout holes at what is the head of the micaceous bolder train. Killian would not say what was hit, but elsewhere in our chat he declared they still have not intersected pegmatite or sampled outcrop whose mineralogy explains that of the micaceous boulder field. The mystery of its origin will be given a hard look this summer, and remains a potential blockbuster discovery.

As far as weather is concerned, although this was a warm winter and the geese have started heading north early, causing the Cree to scramble to get in position for the annual goose hunt, unlike last year this has been a typical moist winter. While things can still go dry in May and June, the risk of huge forest fires is lower this year. One issue is that in some locations where the peat caught fire these fires smoldered through winter. But the authorities are aware of these locations and are monitoring closely for flareups. Brunswick expects to report assays for the remaining holes in bigger batches during May and plans to have boots on the ground in June to further prospect Mirage after getting kicked out last year in early June due to fire closures, with drilling at Mirage to resume in July for what promises to be a very busy exploration season.

Kaiser Watch is a weekly audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees which have changed for 2024 as a transition to a $200 per month auto renewal program in 2025. During 2024 individuals can register for a KRO membership at a non-refundable price of $450 for a term that expires December 31, 2024. All active KRO members will be grandfathered to renew annually at $450 on Dec 31, 2024. Sign up here for this limited $450 offer. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch April 12, 2024: A gold favorite if you distrust gold's uptrend

Jim (0:00:00): Gold has made another new high, this time breaking $2,400. In a recent Kaiser Watch Episode you mentioned Favorites Solitario and West Vault as gold exploration and ounce in the ground extremes of the gold junior spectrum. Where does Favorite Arizona Gold and Silver fit in this spectrum?

Kaiser Watch Episode March 29, 2024: Is $2,000 finally the floor for gold? discussed the unusual situation where gold has been making new highs since bottoming at $1,985 in mid February despite the absence of any new reason for gold to break out. High interest rates, continuing US dollar strength, and inflation in the 3%-4% range, well off the 2022 high of 9.2%, do not explain why physical gold is being bought so aggressively that this week gold breached $2,400 on the LBMA. Central banks prefer to buy discreetly in a manner that does not drive an uptrend. In the absence of a clear explanation for gold's uptrend investors have been reluctant to embrace resource juniors, fearing an abrupt reversal that knocks gold back below $2,000. With regard to non-producing gold juniors I presented two examples of the extreme ends of the gold junior spectrum.

At the very high risk end is the discovery-oriented exploration junior, and my favorite in that regard is Solitario Resources Corp whose Golden Crest project in South Dakota on the western side of the Black Hills could host a gold endowment mirroring the 90 million ounce bounty identified and mined during the past century by Homestake and others on the eastern side. Surface sampling during the past three years has revealed previously unrecognized widespread gold mineralization. The USFS is in the final stretch of responding to comments lodged against the FONSI it issued in December for Solitario's Golden Crest Plan of Operations. A drill permit could be in hand by the end of April, in time for drilling to start in May when road access opens up. But until Solitario has a drill permit and starts to intersect ore grade mineralization, this play remains high risk, but with extraordinary upside reward potential.

At the other end of the spectrum sit the shovel-ready ounce-in-the ground projects waiting for higher gold prices to spark a buyout frenzy. My favorite in that regard is West Vault Mining Inc whose Hasbrouck project in Nevada just outside of Tonopah is fully permitted and backed by a PFS updated early 2023. Under the mining plan Hasbrouck would produce 560,000 ounces gold over 8 years, though there is room for resource expansion by the future developer. I have created a DCF model which shows how the after-tax net present value per share varies at different gold prices. The graphic shows the tremendous leverage West Vault's stock price has to gold prices as high as $4,000, assuming inflation stays at current levels. Whereas with Solitario you have to worry that a drill permit will never get granted or surface values prove misleading about what is at depth, with West Vault you just buy the stock and forget about it. The worst that can happen is that gold tanks below $1,500.

In the middle of the gold junior spectrum sit projects with an emerging gold discovery whose upside has not yet been capped by a maiden resource estimate. Arizona Gold & Silver Inc is my favorite in that category. The junior is conducting a final drill program at its Philadelphia project in Arizona which will allow it to deliver a maiden resource estimate for the 1,500 m long Philadelphia vein by the end of 2024. The resource would extend only 300 m down dip because since acquiring the project in 2019 Arizona Gold's drilling has been confined to the three patented claims which represent a fraction of the overall property. The drill permit application filed with the BLM is in the final comment response stage and a permit could be in hand by May when restrictions related to bighorn sheep calving are over. If Arizona Gold receives this BLM drill permit, not only will it be able to test the Philadelphia vein along strike beyond the patented claims and test the down dip extent by drilling from BLM ground to the southeast, it will also be able to test the hypothesis that under the barren cover rock there sits a stockwork hosted bulk tonnage gold system whose open-pittable endowment could be substantially larger than the underground mineable high grade vein resource. Higher gold prices are not needed for the vein exploration target, and may not be needed for the bulk tonnage target if the grade is high enough and consistently distributed. Investors who distrust the current gold uptrend, and fear the price will sink back below $2,000, confirming that $2,000 is still the ceiling and not yet the floor, can buy Arizona Gold just for the emerging high grade gold discovery, and the possibility of the bulk tonnage scenario being confirmed by drilling. At the same time, if the gold uptrend is sustainable, Arizona Gold's stock price will undergo a substantial upwards revision as investors swarm off the sideline.

Gold closed at $2,401.50 in London on Friday, a new all time high, but the action Friday in the NYSE-listed GLD ETF was on the downside with heavy volume and closing down roughly the equivalent of $29 per ounce from the prior day. The GLD volume, which in April has ranged 10-13 million shares daily, soared to 30.7 million shares, the highest since 47.2 million traded on March 8, 2022 as the world gasped at Russia's invasion of Ukraine. During 2020 the GLD traded a peak volume of 44.4 million shares on August 11, 2020. This pales against the 117 million that traded on March 12, 2010 as gold's assault on $2,000 was just getting underway, or the 93.2 million that traded on April 15, 2013 as gold plunged below $1,500. The daily file published by the GLD ETF showed no changes in holdings for Friday, but Monday's data file will be interesting to see if the GLD gained or lost gold ounces. In any case, the GLD did lose ounces this week and is back to being down about 1.7 million ounces for the year.

At the same time the NYSE closed down 476 points on Friday, closing off a bad week for general equity markets. From a closing peak of 39,807 on Friday March 28 the Dow at 37,983 was down 1,824 points or 4.6%. Fueling the decline was this week's inflation report which saw the CPI come in at 3.5% compared to 3.2% in February. Coming on the heels of higher than expected jobs growth in March this indication that inflation is not fading lifted long term T-Bill yields. Clearly the US economy is doing very well despite all the lamentations about what a terrible job Biden has done for the economy. The prospect of sustained high interest rate levels to subdue the economy and its underlying inflation helped the US dollar stay strong against other currencies. Normally these circumstances should discourage demand for gold, and yet the price of physical gold soldiered higher.

The mysterious gold uptrend has so far had little impact on the trading activity of resource juniors. Yes, TSXV resource junior traded value tends to be 60%-70% of all traded value, but overall resource listing traded value has increased only modestly, though traded volume has increased more though without creating a visible uptrend in average traded share price. The market remains on the sidelines and what we are seeing is bottom-fish accumulation by investors who sense a sea change is coming. There is no evidence yet of major money inflows for the resource juniors. It is as though the entire market has chosen to sit on the sidelines like some sort of NASCAR event and wait for the price of gold to crash and burn, though I suspect the audience that might be inclined to buy resource juniors are really waiting for general equity markets to crash. The experience in 2008 was that when the market crashed, so did gold, just as happened in March 2020 when the world realized that the covid pandemic was serious.

With traditional resource junior audiences on the sidelines waiting for a train wreck to unfold, and perhaps rushing in once the accompanying downdraft is over, what should diehard resource junior speculators do today? On the plus side resource junior valuations remain beaten up, and there are lots of stories to choose among that can flourish from evolving project fundamentals. Given the sense of disbelief that the uptrend in the price of gold is sustainable, Arizona Gold and Silver Inc is an ideal Favorite because it is half way between a pure discovery exploration play like Solitario Resources Corp and its Golden Crest project in South Dakota, and a shovel ready ounces in the ground junior like West Vault Mining and its Hasbrouck project in Nevada. Arizona Gold owns 100% of the Philadelphia project in the Oatman District of western Arizona which it has assembled in stages since 2019.

The Philadelphia vein is a low sulphidation epithermal gold-silver system covered by three patented claims staked in the late 1800's which were the focus of small scale mining to a depth of 700 ft from 1915 until 1941 when the War Orders Act shut down gold mining and the shafts flooded. Between 1979-1990 several groups including Crown Resources and Meridian Minerals explored the claims, completing 30 mainly RC holes. Several historic resource estimates were done for the Rising Fawn claim but these were in the order of 30,000-35,000 ounces at a grade of about 1.5 g/t, not very interesting at all. The Oatman District in contrast has a historic resource of 3,695,000 tonnes of 16.5 g/t gold representing 1.96 million ounces gold.

Since acquiring the Philadelphia project Arizona Gold as drilled 35,885 m in 111 holes represented by 43 core and 68 RC holes along the 1,500 m strike of the patented claims. On April 10 Arizona Gold initiated a 26 hole 2,400 m drill program mostly focused on the undrilled Resaca claim. The patented claims cover the northeast trending Arabian Fault which is tracked by the Philadelphia Vein that dips about 70 degrees to the southeast. These claims represent only 3% of the 975 ha land package, most of which Arizona Gold acquired by staking BLM ground.

The problem encountered by Arizona Gold is that to chase the Philadelphia vein deeper than 200-300 metres down-dip it needs to step to the southeast onto the BLM ground, but to drill from BLM land it needs a BLM drill permit for which the junior initiated permitting in 2022. The patented claims are private land and not subject to BLM permitting. An added complication is that the BLM land to the east is characterized as bighorn sheep habitat, which restricts drilling activity during the calving period from January until April. The impetus for the BLM permit application came in 2021 when Arizona Gold recognized the Red Hill target as a potential low grade stockwork zone in the hanging wall of the high grade vein that could be open pit mined with grades in the 1.0-1.5 g/t gold range.

Philadelphia thus represents two types of target. The first is the high grade gold vein which represents a tonnage footprint of 4-6 million tonnes along a strike of 1,500 m to a depth of 300 m with widths ranging 3-5 metres. The current drill program will boost the hole count that can be used for a 43-101 resource estimate to 150 holes. Results should be in hand by June, with a resource estimate possible in Q3 of 2024. Assuming a grade range of 2-5 g/t gold this resource footprint could yield a resource range of 250,000 to 1 million gold ounces. In its corporate presentation Arizona sets itself a goal of 9 g/t gold which would represent a 1.0-1.5 million ounce high grade outcome. If the junior delivers that grade within the vein tonnage footprint it would be a fantastic fundamental outcome.

The second target is the hanging wall stockwork above the Philadelphia vein, a portion of which on the patented claims yielded 116 m of 1.34 g/t gold and 104 m of 1.57 g/t. The potential tonnage footprint is in the order of 100-200 million tonnes, mostly on the BLM land. If drilling confirms the Red Hill hypothesis the high grade resource would become part of the open pit mining resource. The permit application is in the final comment response stage, similar to Solitario's Golden Crest plan of operations with the USFS in South Dakota, and a permit could be in hand by May, setting the stage for a major summer drill program. Even if the Red Hill hypothesis proves a bust for a bulk tonnage scenario, the drill permit will allow Arizona Gold to chase the Philadelphia vein deeper until it reaches that depth where grades in a low sulphidation epithermal system disappear. It will also allow Arizona Gold to chase it along strike beyond the patented claims.

Arizona Gold is cashed up after raising $1.6 million through a $0.30 unit financing, which boosts fully diluted to 97 million shares. The implied value for the 100% owned Philadelphia project at $0.38 stock price is CAD $37 million, which, for a project at the discovery delineation stage that represents the mid-point of the fair speculative value range under the rational speculation model, implies a potential outcome of CAD $875 million or $10.13 per share, assuming no further equity dilution. That is a plausible outcome for a discovery that ends up yielding 1 million plus underground mineable high grade gold ounces. The chart history indicates that the Philadelphia project has not become the subject of S-Curve action. If Arizona Gold were at a peak S-Curve price, it would imply a future outcome value of only CAD $44 million, which is far less than what CapEx is likely to cost. S-Curve market action signals a future mine, which Arizona Gold's current valuation is not at all telling us. This is a reflection of the current bear market, the fact that Arizona Gold has not had permitting liberty to properly delineate the vein target nor test the bulk tonnage hypothesis, and the difficulty investors have stitching vein drill results into an outcome visualization.

In a market context where investors are uncertain about the sustainability of gold's uptrend, this story, which involves rethinking an old high grade system with the help of extensive drilling never done before that has already revealed a well mineralized gold-silver system, and applying a new model with a bulk tonnage potential outcome, is an ideal balance between waiting for a brand new gold discovery and waiting for an existing gold deposit to be dragged well into the money by a higher real gold price.

Long Term chart of GLD trading activity and daily gold holdings

Short Term chart of daily changes in GLD ETF gold holdings

Dual chart comparing DJIA from 1920-1934 and 2010-2024

Chart from 2009 showing the balance of daily trading value represented by TSXV Resource and Non-Resource listings

Chart from 2009 showing daily traded value of TSXV resource listings

Chart from 2009 showing daily traded volume of TSXV resource listings

Chart from 2003 showing daily average traded price of TSXV resource listings

Southwest View of Arizona Gold's Philadelphia project

Google Earth views of Oatman District and Philadelphia project

Map showing the full extent of the Philadelphia project awaiting a BLM permit

Drilling program now underway to delineate the Resaca Gap within the Philadelphia vein

Conceptual Model of Bulk Tonnage Target proposed BLM drilling

Implied Outcome Chart for Arizona Gold's Philadelphia project

Disclosure: JK owns none of the companies mentioned; Arizona Gold and Solitario are Fair Spec Value rated Favorites, West Vault is a Good Spec Value rated Favorite

Kaiser Watch is a weekly audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees which have changed for 2024 as a transition to a $200 per month auto renewal program in 2025. During 2024 individuals can register for a KRO membership at a non-refundable price of $450 for a term that expires December 31, 2024. All active KRO members will be grandfathered to renew annually at $450 on Dec 31, 2024. Sign up here for this limited $450 offer. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch April 5, 2024: Goodbye Diamonds, Hello Lithium!

Jim (0:00:00): What is the significance of Winsome's deal to potentially purchase the Renard diamond site from the bankruptcy trustee?

Winsome Resources Ltd announced on April 3, 2024 that it had secured an exclusive option to acquire the physical assets of the Renard diamond mine site for a CAD $4 million cash payment that allows it until September 30, 2024 to conduct due diligence on the suitability of repurposing the mine site to process spodumene bearing ore trucked from its Adina project where 58.5 million tonnes of 1.12% Li2O inferred has been outlined. The option agreement is subject to approval from the Superior Court of Quebec by April 30, 2024, which, if not obtained, will result in Winsome getting its $4 million payment back. Winsome has the option to extend the due diligence period until December 31, 2024 for another $2 million payment, and again to February 28, 2025 for a further $2 million payment.

To exercise the option Winsome must pay CAD $52 million in cash and/or shares in three stages over 2 years, with $15 million due on election, $22 million after one year, and $15 million after two years. The option exercise also requires a separate approval from the Superior Court of Quebec. Winsome would only inherit reclamation liabilities. Stornoway Diamond Corp declared bankruptcy in September 2019 after starting commercial production in January 2017. Osisko Gold Royalties and the Quebec government acquired control of Renard and continued operations until giving up in October 2023. The Renard Mine initially had breakage problems but it got that under control. The blame for the second bankruptcy has been given to weak diamond prices since 2022. The up front cash fee payable by Winsome was designed to pay the care and maintenance costs of the Renard site.

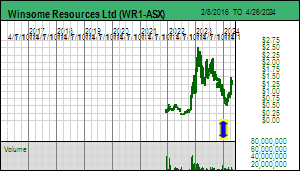

When Winsome resumed trading on Thursday the stock jumped to $1 and on Friday closed at $1.13, a sign that the market liked this development. It is a strategic move by Winsome that helps it deal with the fact that the current Adina resource, which appears to dip south onto the Galinee 50:50 JV of Azimut Exploration Inc and Soquem, is not yet large enough to support standalone development with an onsite mill to produce spodumeme concentrates. Winsome has a 50,000 m drill program underway this year to upgrade the inferred resource and expand it with the goal of increasing grade and tonnage. Purchasing the Renard site would shorten the permitting cycle, provided the proposed La Grande Alliance Road between Renard and the Trans Taiga Highway which services the hydroelectric reservoirs ends up being fast-tracked. Winsome has begun feasibility study related work on Adina as well as environmental baseline studies. But if the 100 km of road needed to connect the Trans Taiga to Renard is not happening, to which a short spur from Adina would need to be built, there is no reason to purchase Renard. The Renard site is desirable because a 500 km road already connects it to Chibougamau in the south where a railhead exists. If Renard becomes a major facility for converting lithium pegmatite ore into spodumene concentrates that can be shipped south for processing at a hydroxide refinery near the St Lawrence Seaway, Renard could serve as a hub and spoke system for multiple pegmatites into the region to the north.

Some parties have dismissed the plan as a marketing ploy for Winsome, arguing that Winsome does not have critical mass to justify committing to the purchase of Renard within 6-11 months (depending on to what degree Winsome makes the exclusive period extension payments), and that in any case it is too early to take control of a bankrupt diamond mining site which is not going anywhere and which appears to have annual care and maintenance costs of CAD $8 million. But there are two reasons why Winsome's deal may be very timely. The first is that the land ownership situation in the area of Adina's Jamar resource is fragmented and it remains to be seen if any of the landholders can generate a resource large enough like Patriot Battery Metals' CV5 deposit (109 million tonnes of 1.46% Li2O inferred with 200 million tonnes a reasonable expansion target). It also remains to be seen if this area - let's call it the Trieste region after the greenstone formation with which the Jamar resource is associated - can yield large pegmatite bodies with higher grades than 1.12% Li2O. Assuming the Trieste region is not going to yield a CV5 equivalent resource, but still a fair number of "in the money" deposits like Jamar at Adina, the Trieste district will be ripe for consolidation. In striking this Renard deal Winsome has embraced a leadership role that one might at a later date have expected Rio Tinto to adopt. There are limits to what properties Winsome can consolidate over the next year, but the Renard deal puts it in the consolidation driver seat.

The second reason the Renard deal is timely is that the tight timeline for WInsome to make a decision, which hinges on the pace with which the La Grande Alliance Road gets permitted and built, puts the spotlight on the Quebec government. Apart from the reservoirs created to generate hydroelectricity, the James Bay region has been a bust in terms of development. Gold exploration during the past few decades has resulted only in the Eleonore Mine whose feasibility study did not clear development hurdles but which got built for political reasons during a time when gold had assaulted $2,000 in the wake of the 2008 financial crisis. Smaller deposits like Eau Claire, now controlled by Fury Gold Mines Ltd, have been investigated for decades without ever reaching development thresholds. A deposit like Cheechoo of Sirios Resources Inc needs a higher real gold price to justify development as an open pit mine, and while this finally seems to be underway, until it is an established reality it is not a relevant factor for infrastructure decisions. Base metal exploration has yielded an even weaker endowment than gold. Until recently the Renard diamond pipe cluster in the Otish Mountain area was the most interesting development, but it proved to be a smallish cluster, not replicated elsewhere in the James Bay region, and diamonds for now are a bust as far as Quebec's James Bay Plan Nord is concerned.

The James Bay region, however, does have a world class endowment of lithium enriched pegmatites, but even that possibility has not mattered because until a few years ago it was assumed that whatever growth the EV sector underwent, its lithium demand would be met by pegmatite sourced supply from Australia and brine sourced supply from the Lithium Triangle in South America. In early 2022 the IEA projected that the world's lithium supply would need to grow 600% by 2030 to meet energy transition goals for net zero emissions by 2050. A year earlier Rio Tinto had declared that the world will need 60 Jadar deposits (the Serbian deposit stuck in limbo) by 2035, which is the equivalent of sixty CV5 deposits. The IEA emphasized that this projection assumed solid state lithium ion batteries would never become a commercial reality. In May 2023 Toyota, which had shunned the EV sector while it focused on its hybrid models, announced a manufacturing breakthrough involving a solid state LIB, with a high end model due as early as 2027.

Since then there has been a slowdown in EV sales growth which is not really a surprise because the current EV models are of little interest to ordinary consumers because of cost, range anxiety, and lengthy charging times. Toyota ignored the EV sector because it knew the technology was inadequate for its mass market sales goals, but did engage in R&D to solve those problems. It is not guaranteed to happen, but what if Toyota hits the market in 2030 with an affordable Camry EV that can do 1,200 km on a 10 minute charge? In fact the head of China's CATL last week, clearly concerned about the leading battery maker's own failure to make a commercial solid state LIB, crapped all over talk that solid state LIB could become a reality, clearly a dig at Japan's Toyota, which recently bought out Panasonic's stake in a battery JV they had operated for decades. If lithium metal can be used as the anode instead of graphite, the future demand would require a more than ten-fold expansion of lithium supply. That sort of scale is not possible from Australia and the Lithium Triangle brines, and will have to be helped out by other pegmatite regions such as Brazil, parts of Africa, and, of course, Canada, in particular the James Bay region of Quebec. Winsome's Renard deal, while it may never result in acquisition of the Renard site, puts the spotlight on Quebec's infrastructure plans for the James Bay region that would eliminate the "remoteness" of these new discoveries. Repurposing the Renard diamond mine site to process spodumene bearing pegmatite ore trucked from multiple open pit mines in the Trieste region would save time in the permitting cycle because the processing facility's footprint is already permitted and disturbed. Maybe CATL's sodium battery will rule the EV world in 2030, but why assume this will actually happen? It is time for Quebec to declare "Goodbye Diamonds, Hello Lithium"!

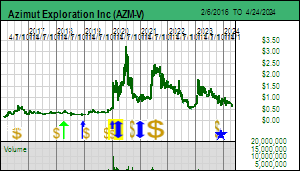

Although Winsome's stock price responded positively to the Renard diamond site deal, its implications seem not to have washed over any affected juniors. The Renard site deal puts the spotlight on the Trieste project of Loyal Lithium Ltd and the Liberty project of Comet Lithium Corp, the two most obvious players in the area which Winsome could target with consolidation. Azimut's work last year during the limited exploration season thanks to the forest fire closure did not turn up any promising targets on the bulk of its Galinee property, but drilling just south of the Adina border did yield some promising lithium enriched pegmatite intersections. However, these intersections seem to be too deep to be open pittable, and their geometry does not make sense relative to the Jamar pegmatites of Winsome. The 50:50 Azimut/Soquem Galinee JV is of no interest to Winsome unless further drilling reveals that the pegmatites to the south are in fact parallel bodies that do not daylight but are close enough to surface to be open-pittable.

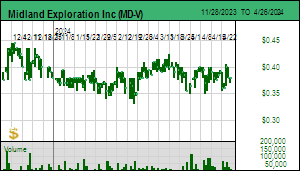

The other Galinee property owned by Midland Exploration Inc and optioned 70% to Rio Tinto as part of a multi-project James Bay regional deal, although beginning 4 km east of Adina and covering the same Trieste Formation that hosts the Jamar pegmatites, is not a consolidation target for Winsome in 2024 because Rio Tinto controls its destiny. Rio Tinto has mounted a CAD $5.8 million drill program on the Iceberg dykes discovered last year and which have been traced over a strike of 600 metres. Including further boots on the ground work during the summer, which could lead to additional target drilling, Rio Tinto will have a good idea of what Midland's Galinee property is all about. The chutzpah behind Winsome's bid for Renard is that if this part of James Bay has critical mass to support a major lithium processing center, it should be Rio Tinto which consolidates the district and acquires Renard out of bankruptcy. Winsome's gambit is that Rio Tinto finds enough at Galinee to justify ultimately taking a run at Winsome and consolidating the rest of the district Winsome has not already consolidated.

Of immediate importance to Winsome is the Liberty property of Comet Lithium Corp through whose southwestern corner the Trieste Formation continues for just under 3 km before projecting onto Midland's Galinee project. Comet, which is part of the 2024 KRO Bottom-Fish Collection, has conducted a gravity survey over this area which appears to indicate structures that could host pegmatite. Comet plans to have boots on the ground to prospect this area in June as soon as goose hunting season is over, and, hopefully be in a position to justify a summer drill program. The junior has $2 million working capital, some of which it will spend on till sampling the Troilus East project for lithium, gold and base metals. The southwestern corner of Liberty is too small to host a standalone deposit, so whatever Comet finds would naturally fit into Winsome's Adina portfolio. A wild card for Comet is the possibility that a structural trend that streaks off 6.5 km to the northeast into other rocks could also be an emplacement host for LCT-type pegmatites, though that potential will not be assessed until later in the summer. For now Comet's focus is to see if the 3 km segment at the southwestern end of Liberty has sufficient high grade pegmatite to become part of Winsome's Adina project.

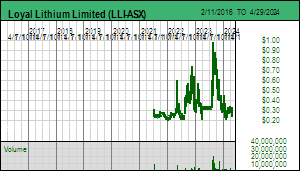

The other important player in the region is ASX listed Loyal Lithium Ltd which owns 100% of the Trieste project which covers Trieste formation rocks east of Midland's Galinee. Last year Loyal Lithium was able to obtain decent grade and length channel samples across several dykes as well as drill 40 m of 1.2% Li2O in Dyke #1. A 2,500 m drill program to test Dykes #4 and #5 began in February. Dyke #5 has yielded good intersections in the 1.4%-2.2% range to which the market has barely reacted. Loyal Lithium has 103 million issued and 154 million fully diluted; at the moment it is the best bet in the Trieste region for an Adina equivalent or better discovery delineation play to emerge. The Loyal Lithium pegmatites are interesting because they are hosted by the metasediments adjacent to the Trieste greenstone formation that hosts Jamar and Midland's Iceberg target. Loyal has developed a conceptual model about how the nearby Tilly granitoid may have spawned these pegmatite dykes. The market will be watching closely to see what size, geometry and grade Loyal unveils in this host rock.

In terms of speculative upside, the IPV Chart shows that Loyal Lithium's Trieste project has an implied value of AUD $46 million which is within the fair speculative value range for a $2 billion outcome. In contrast Winsome's Adina has an implied value of $236 million, five times higher and also in the fair spec value range for a $2 billion outcome - it is at the infill drilling stage with a published resource. Comet's Liberty in contrast has an implied value of only $9 million reflecting the fact that no LCT-type pegmatite has yet been found on the property. If the 3 km segment between Adina and Midland's Galinee starts to reveal spodumene bearing pegmatite Comet's stock price has the greatest upside potential. The Galinee projects of Azimut and Midland have similar implied values of $124 and $132 million, which is rich for projects with no lithium enriched pegmatite bodies with meaningful size yet indicated; but both companies have lots of other projects so are not vulnerable to significant downside if they fail to deliver anything consequential this year. Brunswick's Mirage, which is at the discovery delineation stage, has an implied value of CAD $90 million or twice that of Loyal's Trieste project, which is also fair speculative value for a $2 billion outcome. In terms of news flow, Brunswick is best positioned to exhibit S-Curve action in the short term if the winter drill program has scaled the Mirage footprint substantially larger.

The Trieste District Consolidation Play that Winsome's Renard deal kicks off

Winsome's Adina Property and Quebec Transportation Map

Winsome's Adina lithium resource

Geology Map of Trieste District

Plan View of Azimu/SOQUEM Galinee Drill Program

Section View of Azimut/SOQUEM Galinee Drill Program

Map of Midland/Rio Tinto Galinee project

The potential importance of Comet's Liberty clain to Winsome's Adina resource

Map showing Loyal's Trieste Property

Plan View of Loyal Lithium's Trieste dykes and conceptual section

Drill Results for Loyal Lithium's Dyke #5 at Trieste

IPV Chart showing how Loyal Lithium compares to other Trieste District players

Jim (0:12:39): Would Brunswick's Mirage project benefit from the Renard mine site as a destination to truck its pegmatite ore?

The scale of the Mirage project of Brunswick Exploration Inc for now opens the potential for an onsite milling facility to produce a spodumene concentrate, but if Mirage does fall short, it could end up being a spoke that feeds the Renard processing hub. While so far the dykes intersected have not screamed tonnage volume, the 2% plus bonanza grades would be helpful in justifying the trucking of raw ore to Renard. The main benefit of Winsome's Renard deal for Brunswick is that it forces the Quebec government to think hard and quickly about the infrastructure development of the James Bay region if it is to become a major pegmatite sourced lithium supplier in 2030 and beyond when timing for exponential mass adoption of EVs is plausible. Mirage is further north than Adina but a spur would connect it to the La Grande Alliance Road between Renard and the Trans Taiga Highway.

Brunswick announced on January 22, 2024 that it had initiated a drill program at Mirage which will test a 2.8 km by 2.0 km area where spodumene bearing outcrop has been identified. Last year's drilling tested only a 2 km segment on the 100% owned claims which intersected 3 distinct dykes with 2.0%+ bonanza grades. Much of this delineation drilling will assess this dyke swarm to a vertical extent of 250 metres, perhaps with sufficient density to yield a resource estimate. When I talked to CEO Killian Charles this past week he said the program was a week away from wrapping up and there was a slight chance Brunswick might drill a couple scout holes beneath the 3 km boulder train that begins at the southwestern limit of the delineation target drilling area about whose results the market turned out to be not overly impressed. In fact, so far this year every time Brunswick has put out a news release it triggered a new round of selling. So the perception has emerged that Mirage is going to be another Jamar, with the high grades getting sacrificed to deliver critical mass tonnage. Surprisingly, although the market shrugged a couple weeks ago when Brunswick announced staking lots of additional pegmatite targets in Quebec as well as in Greenland, this week Brunswick had its best upside day of the year when the Winsome Renard news came out.

Although one could have guessed from the January news release that testing 2.8 km of strike with pegmatite outcrops meant Brunswick would be drilling the 75% optioned Osisko inlier claims (since spun out into a new Sean Roosen deal called Electric Elements Mining Corp), Brunswick has not made a lot of noise about this strike expansion drilling which may have passed right through the Osisko claims back onto 100% owned ground. When Brunswick finishes drilling this month it will provide a drill exploration summary for Mirage that may surprise the market. The area has a series of narrow lakes which track the ice direction, which by coincidence may also be a structural trend of weakness that would have attracted the emplacement of wandering pegmatites. These lakes would have been frozen enough to allow drilling from ice to track the pegmatites efficiently. We may hear of additional parallel dykes within the segment of the swarm drilled last year. The surprise potential lies within what was found on the Osisko inlier claims onto which the dyke swarm extends.

Killian Charles wouldn't provide any details, but one important detail he did share was to answer in the negative if any of the drilling has intersected pegmatite with the same micaceous mineralogy as the big boulder field that begins where the dyke swarm disappears under overburden. If Brunswick has marched its drill 3 km beyond the head of that prominent boulder train and found lots of well mineralized pegmatite lacking the micaceous mineralogy, it has deepened the mystery of the origin of these boulders which were assumed to have been glacially transported from an up ice source. In fact it boosts the chance that maybe these boulders have not been transported by ice at all, but may be sitting on top of the source from which they were broken by weathering and eventually frost-heaved to the surface as this zone structural zone filled with overburden. Killian was unsure if it was worthwhile to drill a couple blind high risk scout holes, and I suspect it is because Brunswick will have a lot to talk about when the winter drill program results are released. It might be much better to line up a scout drill for the summer to drill a systematic fence to sort out what is going on in bedrock beneath the overburden.

Brunswick's Mirage Delineation and Expansion Winter Drill Porgram

Disclosure: JK owns Brunswick; Brunswick, Winsome and Patriot Battery are Fair Spec Value rated KRO Favorites; Midland and Comet are Bottom-Fish Spec Value rated.