The month of November was not kind to the James Bay Lithium Index as investors ratcheted up what they want to see in the form of fresh news from juniors while watching the lithium carbonate spot price crash through $10/lb, closing at $8.07 on Friday. Chinese spodumene refineries and battery makers are currently negotiating long supply contracts with concentrate producers, so are delighted by the price trend. Audiences that track the Canadian resource juniors are worried that the lithium price will suffer another lithium winter as happened in 2018 when the Australians were faster at mobilizing new supply from their pegmatites than demand growth from the EV sector. The lithium carbonate price crashed from a $10-$12/lb range below $3/lb, crashing lithium junior stock prices, discouraging new exploration, and stalling feasibility demonstration work on advanced pegmatites. That imbalance reversed itself in late 2021 and the spot price shot into the $30-$35/lb range where it stayed all of 2022 before new supply came on stream in 2023.

The problem with North American investors is that they are overly obsessed with metal prices which comes from decades of braying and praying for higher gold prices and hooking market sentiment to the trend in the price of gold. They do not understand that lithium, which was a $200 million market in 2005 when about 20,000 tonnes of lithium metal was produced, has undergone a nearly 600% supply growth since then, producing 130,000 tonnes in 2022 which at the nominal average spot price in 2022 was worth about $49 billion, but at long term contract prices likely worth in the order of $20 billion. The rapid demand growth experienced by lithium thanks to its key usage in electric vehicle batteries is unprecedented, and is required by an EV sector whose annual sales are still less than 10% of car sales. The IEA projects a 600% lithium supply expansion is needed to meet EV sales goals for 2030, and if claims about commercially viable solid state lithium ion battery breakthroughs by the likes of Toyota are true, the expansion need will hit 1,200% by 2035. That means the future lithium market will be worth $100-$200 billion annually.

The $30-$35/lb lithium carbonate range was never sustainable because at that price an awful lot of LCT-type pegmatites are in the money. If lithium carbonate stabilizes in the $5-$10/lb range that is high enough to encourage exploration and development of pegmatites grading 1% Li2O or better, and that is where the James Bay region is important because it is now host to several world class lithium pegmatite deposits, with Patriot Battery Metals' CV5 being confirmed as the biggest and richest when it delivered its maiden resource estimate in August 2023. PMET's CV5 and any other new discovery will not be in production before 2030, given Canada's anti-mining attitude and Prime Minister Justin Trudeau's apparent desire to bestow on First Nations the final say on Canada's future mineral development.

On December 1, 2023 President Biden, becoming ever more aware about the Global West's vulnerable dependency on raw material supply from China and Russia, took another step to limit EV tax credits to cars whose inputs are not sourced in the Global East (US Limits Chinas Ability to Benefit From Electric Vehicle Subsidies). If anything gets PM Trudeau bounced out of office, it will be his failure to understand Canada's critical role as a producer of minerals like nickel and lithium essential for energy transition goals. The Canadian financial sector also needs to pull itself out of its anti-mining funk and start bankrolling resource juniors engaged in exploration. The key to regenerating a robust resource junior eco-system starting with lithium is to understand that the current lithium price is irrelevant to market sentiment. Even if it does crash back below $3/lb, this would be short-lived because that price is too low to mobilize the future needs of EVs replacing ICE cars.

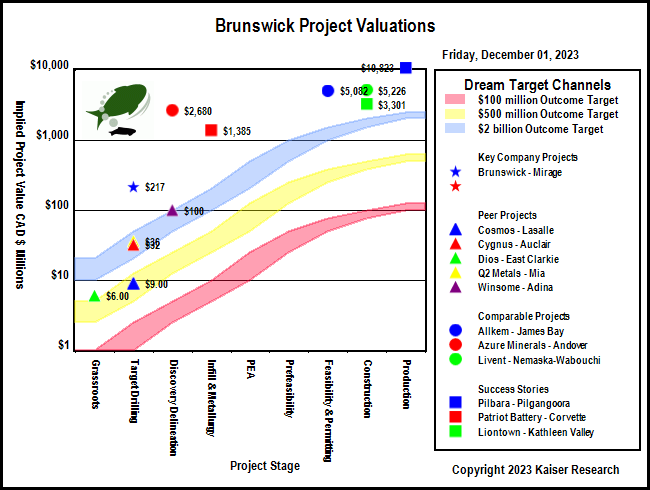

What the Canadian resource juniors now need is a Canadian lithium discovery champion. Patriot Battery Metals, although it started on the CSE and now trades on the TSXV, its initial funding and price appreciation came from Australian investors, and it is now dual listed on the ASX which sets the day's trading tone. PMET has lost a third of its value since Albemarle invested $109 million at $15.25, largely because the story is now in feasibility demonstration mode even though exploration drilling is building the resource bigger. So far the best shot at a Made in Canada lithium discovery champion is Brunswick Exploration Inc which is sporting an implied value of about $200 million based on speculation that its Mirage project in the James Bay region has world class scale.

Brunswick last provided a meaningful update on October 5 when it announced that drilling at Mirage has intersected spodumene bearing pegmatite over lengths up to 52 metres, though it cautioned that true width is unknown. The junior blew a chance to provide an update ahead of the XPLOR conference in Montreal during the first week of November, choosing instead to announce a $5.7 million flow-through financing which blacked out any further updates until it closed on November 17. This has left the market wondering if Brunswick is still struggling to grow a PMET out of a Peanut at Mirage. Assay turnaround for pegmatite core has been terrible, and the company is now caught in a trap where if it releases only a handful of intervals, the market might declare, "not good enough". What the market wants now is evidence of scale for Mirage and confirmation that Brunswick's drilling has yielded an understanding of the geometry of the Mirage pegmatite field. Assays can wait until January when Brunswick has hopefully received enough 1% Li2O intervals to allow the number-crunchers to start estimating potential tonnages and grades. What the market is dreading is news such as what Q2 Metals Corp reported for initial drilling limited to one end of the LCT-type pegmatite trend on its Mia project in the James Bay region. The market saw only a peanut sized scale and, unfairly and impatiently, trashed the stock.

On November 27, 2023 Brunswick did toss a bone to the market when it announced "Brunswick have notified Globex that they have met the minimum $1,000,000 exploration expenditures and Globex has received an additional $212,500 in cash and 216,395 Brunswick shares, representing a cash equivalent of $212,500 (216,395 shares at 30-day VWAP average of $0.982/share). The full exercise of the option has occurred approximately 11 months after signature of the 4-year option agreement." The market was not sure what to make of this accelerated 100% vesting in the Globex option. It was already a given that the low expenditure requirement would be fulfilled this year. The $500,000 in cash and/or stock is not much money at all, so it does make sense to take care of it all right now rather than be an over-optimizing accountant dribbling out the bits each year when they come due. The main reason to do this now is that it forces a vesting acknowledgement from Globex Enterprises which eliminates the risk something small that needs to be done at a later date gets overlooked and triggers a default, and the risk that if Mirage is a PMET rather than a Peanut, Jack Stoch's lawyers find some legal hook to claim the option deal was not valid. In my view getting rid of the title risk now can be interpreted as a sign that internally Brunswick thinks it has the goods.

The more impressive part of the announcement was that a winterized camp is now in place to support a 15,000 m drill program in 2024, not just for 2024, but to be executed during the Q1 winter. This is a sign they are shifting to delineation drilling, that they have sorted out the geometry of key pegmatite zones, and that the spodumene visuals are strong and abundant enough to signal grades over meaningful widths will run over 1% Li2O. The market, in its current bad mood, however, is in a mood of show me at least physically what the pegmatite field looks like, where have you found outcrops, where are your holes located so that we can see that your understanding of the geometry is evolving and you are seeing good geometry. If Brunswick can give this sort of update in early December, an entirely new audience can start to embrace Brunswick and its Mirage project as a new Canadian discovery champion in the James Bay region. And while Brunswick does not yet have an ASX-listing, Australian investors have quite a bit of experience interpreting LCT-type pegmatite results, especially having napped for 6 months after Azure Minerals Ltd first reported evidence of a big pegmatite field at its Andover nickel project in the West Pilbara region of Australia in October 2022 that attracted SQM as a 19.9% shareholder but not much respect from Australian investors until assays started showing up. The Andover project is now sporting an implied value of AUD $2.7 billion on a 100% basis and Azure has not even delivered a maiden resource estimate. That is ten times higher than Brunswick's Mirage implied value. (see KW Episode Oct 27, 2023).

The emergence of Brunswick as the new Canadian discovery champion for the James Bay region would also do a lot for all the other juniors that managed to get some work done after losing most of the 2023 boots on the ground prospecting season due to Quebec's forest fire closures. If the American transition from ICE to EV cars remains on track, dozens of world class lithium pegmatite mines will need to be built in Quebec by the 2030s. During the past week the James Bay Lithium Index sprouted a run of green shoots, despite the lithium carbonate price sinking lower. If Brunswick were to deliver concrete evidence that Mirage is another PMET rather than a Peanut, this greening trend could continue well into the new year. After this KW Episode was recorded Friday I joined Albert Laurin for a free-wheeling Lithium & James Bay Discussion which my KW audience may find entertaining. Brunswick, however, is key to getting the Canadian financial sector into the James Bay lithium play before the Australians once again eat their lunch. |