Hello Guest User, You are visiting this website from a computer with an IP address of 172.70.130.213 with the name of '?' since Fri Apr 26, 2024 at 10:23:49 PM PT for approx. 0 minutes now.

Kaiser Media Watch Blog - March 1, 2023 to March 31, 2023

KRO Blog Overview

The KRO Blog is where unrestricted content of a time sensitive nature is posted. It includes the Kaiser Media Watch Blog which features content involving John Kaiser produced by third parties such as the Discovery Watch series by HoweStreet.com, interviews by outfits such as Investing News Network, SDLRC related commentary, the KRO Monthly Summaries, and just about anything else John writes that is not intended exclusively for the fee based KRO Membership.

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch March 29, 2023: Albemarle helps put Liontown into play

Jim (0:00:00): What are the implications of Albemarle's conditional bid for Liontown and its Kathleen Valley lithium project in Australia?

Liontown Resources Ltd announced on March 28 that it had received a proposal from Albemarle to acquire the company at AUD $2.50 per share, which at 2.2 billion issued assigns a value of AUD $5.5 billion to the Kathleen Valley project in Western Australia. At current exchange rates that is about USD $3.7 billion or CAD $5 billion. However, the proposal, which offered a 64% premium above market, was only indicative, not binding. Albemarle wanted Liontown to agree to an exclusive due diligence period and a number of conditions such as regulatory approval before the offer would become binding.

Since December 2022 the price of lithium carbonate has been falling back to earth, and is currently between $17-$18/lb. The optics have had a negative affect on the price of lithium producers and advanced developers such as Liontown which was languishing between $1.40-$1.60 after peaking at $2.22 in November. I am assuming that lithium carbonate will bottom somewhere between $10-$15/lb, but until it does, the Lithium Mania 1.0 companies will be under pressure. The Albemarle proposal not only prevented Liontown from engaging in an auction of itself for other producers, but exposed itself to being tainted if Albermarle comes up with an excuse not to make the offer binding.

It turns out Liontown had received similar proposals form Albemarle at $2.20 on October 20, 2022 and at $2.35 on March 3, 2023 just before PDAC where Albemarle had a booth for the first time ever in the Investors Exchange. Unlike the earlier proposals which Liontown did not make public, this time Liontown went public and also stated that Albemarle has apparently accumulated a 2.2% equity stake in the open market. The stock traded 137 million shares on Tuesday, ten times its usual daily level, and closed up 69% at the day's high of $2.57. This development is a big deal because the producers are taking advantage of the lithium price slump to go after near production companies like Liontown. It is bad news for the investment banks who have been talking down the sector as over-priced because they hope to represent car and battery makers launching their own bids to secure their future lithium supply needs. And it its good news for the transition of Lithium Mania 1.0 to Lithium Mania 2.0.

Lithium Mania 1.0 represents the awakening of the lithium boom in 2015-2018 when Tesla sales took off and the world started taking electric vehicles seriously as a partial solution to the energy transition goals of limiting global warming to 1.5 degrees celsius by 2050. During Lithium Mania 1.0 juniors focused mainly on hardrock pegmatites in Australia and brine salars in the Lithium Triangle of South America. Although some Canadian juniors such as Patriot Battery Metals' predecessor acquired Canadian pegmatite plays, these did not get the attention the Australian juniors attracted. PMET never got around to drilling its Corvette pegmatites in James Bay and inflicted two rollbacks on its shareholders until it caught the start of Lithium Mania 2.0 in 2021.

Liontown was a typical Australian junior with gold projects in Australia and Tanzania when in late 2015 it decided to branch into lithium exploration in Western Australia. It acquired the Kathleen Valley project in 2016 from gold producer Ramelius Resources for 25 million shares. The property had multiple LCT type pegmatite showings within a greenstone setting on the Yilgarn Craton. Lithium carbonate prices were in the $10-$15/lb range at the time which made developing 1%+ Li2O pegmatites very lucrative, but in 2018 the price crashed as new supply from Australian pegmatites came on stream and overwhelmed EV demand. Despite the slump Australian companies like Liontown persisted at the cost of diluting their issued shares into the billions.

In the case of Liontown exploration of its various lithium prospects resulted in Kathleen Valley becoming the flagship, with a PFS for a 2,000,000 tpa (5,000 tpd) mine delivered in December 2019. Although the lithium carbonate price didn't bottom at about $3/lb until late 2020, Liontown persisted with a DFS which it delivered at 2.5 million tpa scale in November 2021. The 2017-2020 Trump administration was hostile toward the idea of climate change and Trump did his best to promote the fossil fuel sector at the expense of climate change mitigation goals. The rest of the world, however, stuck to its EV rollout policy goals, especially China, which had a strategic reason for shifting away from ICE vehicles to electric vehicles. Much of China's electricity is generated by domestic coal, but its ICE fleet depends on imported oil, and that could become a problem for China's imperial goals. After voters dumped Trump in November 2020 the Biden administration started to support energy transition goals.

The big surprise, however, was that the car makers, despite Trump knocking down fuel efficiency targets, had on their own made strategic decisions to embrace electric vehicles. It was no longer just Tesla the maverick, but all car companies designing and building EVs. While there are different configurations for the lithium ion battery, all of them require lithium. The over-supply situation began to reverse itself in the second half of 2020, and by the end of 2021 the lithium carbonate spot price had increased 10-fold. In fact the imbalance was so badly reversed that lithium carbonate spot prices spent all of 2022 in the $30-$35/lb range which is much higher than required to mobilize the six-fold supply expansion the IEA projects as needed to meet 2030 EV deployment goals. But it was a huge windfall for lithium producers, including Albemarle which has its Silver Peak brine operation in Nevada, Salar de Atacama in Chile, and joint venture stakes in the Greenbushes and Wodinga pegmatite mines in Australia.

Liontown is currently building a 3,000,000 tpa facility (about 8,000 tpd) with a projected CapEx of AUD $895 million, most of which is funded by equity and a credit facility. Construction is expected to be complete by mid 2024. It is based on a proven and probable reserve of 68.5 million tonnes at 1.34% Li2O, of which 65.4 million is slated for underground mining. At $17.15/lb lithium carbonate this reserve has an in situ value of USD $87.5 billion and a rock value of $1,280 per tonne. If we assume $10/lb as the long term reality, the rock value drops to $746/tonne, still an impressive number, while the in situ value drops to $51 billion (the recoverable value will be lower). The latter is equivalent to AUD $76 billion, which makes the Albemarle worth about 7% of the gross metal value. The reserve sits within a resource of 156 million tonnes of 1.4% Li2O, which gives the owner the capacity to double the production rate down the road. The price Albemarle is offering is thus reasonable. The big question now is whether other potential buyers of Liontown will come to the table and start a bidding war without conditions. The fact that Liontown's price is higher than the $2.50 Albermarle offer suggests that the market thinks so.

Jim (0:13:47): What are the implications of the Liontown bid for Lithium Mania 2.0 juniors like Patrtiot Battery Metals and its much earlier stage Corvette project in the James Bay region of Canada?

If Liontown does become the focus of a bidding war that results in it being acquired by a much larger company it will accelerate the transition from Lithium Mania 1.0 to Lithium Mania 2.0. Lithium Mania 1.0 was characterized by a rush into Australian pegmatites and Lithium Triangle salars. In both settings the low hanging fruit is now owned and already in production or heading into production. Whatever is left to be found in Australia will require riskier exploration probing under cover. When you use Google Earth to fly over Western Australia, you can see that the northern two thirds has little vegetation, swamp or lakes, very unlike much of Canada. Much of the bedrock is covered by dirt, but then most of eastern Canada is covered by glacial till and overburden. The difference between Australia and Canada is that exploration of Canada's outcropping pegmatite potential is just getting underway. Those LCT pegmatites such as Galaxy/Cyr, Rose, Wabouchi and Moblan which were found decades ago were acquired and explored as part of Lithium Mania 1.0. These are now heading into production.

Lithium Mania 2.0 is based on a market realization that the supply potential identified by Lithium Mania 1.0 is insufficient to meet the lithium demand projected for 2030 and beyond. Liontown's most recent corporate presentation has a very useful slide with a graph that presents supply and demand projections based on work done by Wood Mackenzie and Albemarle which also shows future supply deficits. This chart shows a balance being achieved in 2026, beyond which the supply deficit widens dramatically, peaking at 51% in 2036. This is based on lithium in the current supply mobilization pipeline. Lithium Mania 2.0 is about identifying the pegmatite supply that will take care of the supply deficits that emerge in 2028 and beyond.

Patriot Battery Metals was bootstrapped in 2021 by Australian investors who understood what was happening to future lithium demand and the limits of Australian pegmatite and Lithium Triangle brine supply alone delivering that demand. The outcropping spodumene enriched pegmatite zone on the 55 km long Corvette trend represented low hanging fruit similar to what the Australian juniors harvested in Western Australia during 2015-2018. Lithium Mania 1.0. however, was haunted by uncertainty about whether consumers would actually embrace electric vehicles on a large scale. While the logic behind future lithium demand was sound, the timing of its arrival was uncertain, and that ripped the rug out from underneath Lithium Mania 1.0 when the Australians proved highly efficient at mobilizing new supply and tanked the price of lithium carbonate to a level where nobody has economic incentive to develop pegmatite based lithium supply. But today the car makers have gone beyond the point of no return and the future supply requirements are so well understood that car makers themselves are willing to violate the taboo about getting involved with upstream raw material supply. Furthermore, if the recent slowdown in demand from the Chinese EV sector does threaten to drop the price of lithium carbonate below $10/lb, the battery and car makers will soak up the surplus supply and stockpile it because they understand that if Lithium Mania 2.0 collapses, and the resource juniors who are the exploration engine behind identifying the new supply lose their funding audience, there simply won't be sufficient lithium to make planned EV sales for 2030 and beyond a reality. Albemarle making a tentative move on Liontown in the current environment of a plunging lithium carbonate price reflects this reality.

PMET has during the past 18 months drilled over 150 holes into the CV5 pegmatite and is now marching 6 drill rigs along strike to try to double the footprint by demonstrating that the CV4 outcrop on the north shore of the lake is part of the CV5 pegmatite system. Drilling will pause on April 20 for a month to accommodate the Indigenous goose hunting season. The potential to delineate a 50-100 million tonne body grading 1%-2% Li2O is already visible through the published drill results, which would make CV5 comparable in scale to Liontown's Kathleen Valley deposit. On Wednesday afternoon ahead of the Thursday ASX trading session PMET published the first batch of assays for the 2023 drilling. The results include significant intervals in the 3%-5% Li2O range.

PMET currently has an implied project value approaching CAD $2 billion which represents S-Curve territory ahead of a maiden resource estimate, but that milestone should be achieved by the end of Q2. It has been 7 years since Liontown acquired Kathleen Valley from Ramelius as a pegmatite prospect, with production scheduled by year 8. PMET acquired Corvette at the same time but is only in its second year delineating the CV5 discovery and one might think its valuation is very far ahead of the fundamentals. However, PMET has the Lithium Mania 2.0 advantage over Lithium Mania 1.0 in the form of very big stakeholders understanding the urgency behind identifying the lithium supply that will prevent supply deficits from emerging in 2028 and beyond as Wood Mackenzie projects. While Corvette may look like another Kathleen Valley, the project still needs a couple years of de-risking to attract a bid with a comparable valuation, but the times are such that a $2-$3 billion offer from a party that wants a district scale trend with a flagship deposit already outlined is not inconceivable. The Lithium Mania 1.0 operations were all developed with scales that reflected the uncertainty about the size and timing of the EV future. In the Lithium Mania 2.0 context a much more aggressive production scale can be justified as soon as Corvette passes the maiden resource estimate milestone.

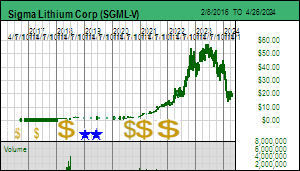

Jim (0:22:11): Is the Albemarle proposal for Liontown good news for Sigma Lithium and its Grota do Cirilo project in Brazil?

Sigma Lithium Corp has been the subject of rumors that Tesla is planning a buyout which have never panned out. With 102 million shares fully diluted its flagship Grota do Cirilo lithium project in Brazil's Minas Gerais state has an implied value of CAD $5.2 billion based on the TSXV $51 closing price on Wednesday. Sigma's primary market is NASDAQ where it closed at USD $37.62. The project is similar to Liontown's Kathleen Valley project except that it expects phase 1 to be in commercial production next month. The proven and probable resource at 54.8 million tonnes at 1.44% Li2O is similar to Kathleen Valley's 68.5 million tonnes at 1.35% though it does not have a total resource more than the double the reserve within it. Albemarle's CAD $5 billion conditional bid for Liontown is good news for Sigma Lithium that a buyout at the current valuation is plausible. It is not so good news for Grizzly Research and short sellers who think a proper valuation should be 50%-75% lower.

Last week an outfit called Grizzly Research which claims to be short Sigma published a 42 page report titled Bogus Feasibility Studies & Production Delays will leave Investors Praying for a Buyout. Over the next couple days the report knocked the stock down from USD $36.50 to as low as $31.57 on Friday. The Liontown news has helped the stock bounce back though in CAD terms it is still below the $54.23 peak achieved on October 31. The Grizzly Report makes two key arguments.

One is that Tesla is unlikely to buy Sigma Lithium because Elon Musk thinks the world is over-flowing with lithium and the real bottleneck is lithium refining capacity to make battery grade material. Tesla is building such a facility in Texas which would process spodumene concentrates into battery grade lithium hydroxide. He also supposedly thinks that Nevada's claystone deposits are the most likely lithium supply for his GigaFactory near Reno. The nature of claystone deposits is such that a mine would produce battery grade lithium, so separate refining capacity is not needed. The problem with the claystone deposits is that it remains to be demonstrated that proposed flow-sheets for projects like Lithium Americas' Thacker Pass and Ioneer's Rhyolite Ridge will operate as predicted. It will take several years to find out. Pegmatite mines that produce spodumene concentrates which get converted into battery grade material with established technology do not have that technical risk.

Grizzly also thinks that Musk would not want to rely on lithium supply from a country run by a left-winger like Lula rather than a wannabe autocrat like Bolsonaro. Given the ignorance Elon Musk has publicly demonstrated about the nature of the mining industry and its timelines, I tend to share Grizzly's skepticism that Tesla is a serious contender to buy out Sigma Lithium and turn Grota do Cirilo into an in house supply of pegmatite sourced lithium. A much likelier candidate would be one of the Chinese companies who would have no problem doing business with a right or left wing government. Grizzly warns that the Canadian government would not allow such a bid, just as it forced a Chinese shareholder to divest itself of an equity stake in Lithium Chile even though Lithium Chile has no properties in Canada. However, the American shareholders of NASDAQ listed Sigma such as Blackrock would tell Justin Trudeau to piss up a rope if he tried again to interfere with the sovereignity of other nations. With Albemarle willing to pay AUD $5.5 billion for Liontown in a country that is no longer happy with China and which would probably block a takeover by a Chinese company, Sigma Lithium may lot more appealing today.

Grizzly nitpicks about a number of issues that seem frivolous, but its second important argument for a lower takeout price in the CAD $10-$20 range is that it falls into the Goldman Sachs camp which predicts lithium surpluses as we approach 2030 that justify using lower long term prices. This is the opposite of what Albemarle and Wood Mackenzie predict in that Liontown supply-demand graph. In that regard the Albemarle bid is very inconvenient for Goldman Sachs, which seems to be in the business of talking down the price of lithium producers and developers on behalf of the car and battery makers who would prefer to pay as little as possible for their long term lithium supply which internally they know could very well be in deficit by 2030. Lithium Mania 2.0 is premised on the idea that it is better to know where the future supply can come from than to speculate about China's supposed domestic supply expansion capacity, Russia and China somehow getting the giant Bolivian salar into production as well as the DRC deposits, and direct lithium extraction becoming viable for oilfield brines. Lithium Mania 2.0, the search for LCT pegmatites in relatively unexplored jurisdictions like Canada, Scandinavia and Brazil, is insulated for the next few years from the outcome of this supply debate.

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch March 24, 2023: Will Tower graduate to the 2023 Favorites Collection?

Jim (0:00:00): Has Brunswick Exploration started drilling yet on any of its lithium projects?

Brunswick Exploration is finally drilling after spending nearly a year assembling a portfolio of Canadian lithium prospects based largely on archival research followed by boots on the ground field inspections that have identified 650 pegmatite bodies the junior plans to test with make or break drilling programs. Drilling is underway on Anatacau West adjoining to the east of the Galaxy/Cyr lithium deposit Allkem is putting into production. In fact, Monday's news release benefits from drilling having started during the past week. An expanded drill program with substantial eastward stepout fences suggests to us that the initial fence of holes 50 m of the border has confirmed the Allkem pegmatites extend onto Brunswick's ground.

The sexy part of Monday's update is about the Plex project, which Virginia Gold called the "Poste Le Moyne Extension". A chopper visited Plex just ahead of PDAC and not only confirmed the location of the core shack, but also that the core boxes are intact and have not been vandalized (ie not dumped and kicked around so that samples cannot be linked to drill hole locations and position within the core). In testing the Orfee gold zone Virginia drilled through pegmatite that was only vaguely logged and not split for assaying. Brunswick does not yet know if these pegmatite intervals, 96 greater than 8 m occurring over a 1,300 m strike encountered while testing the Orfee gold zone, are LCT type, but within two weeks it will have a crew on site to test pegmatite intervals with an XRF gun, and designate those intervals whose pathfinders indicate LCT for sample preparation and assaying. These pegmatites adjoining the gold zones in a coincidental rather than genetic manner may prove to be barren, but, if instead they prove similar to those of another former Virginia claim block called Corvette which currently supports a $2 billion implied project value for Patriot Battery Metals, will launch Brunswick into S-curve territory. If Brunswick announces that it has shipped Plex core samples for assaying, it will then allow drill permitting to begin ahead of July. The realistic plan was to spend the summer putting boots on the ground and perhaps drilling in the fall. Although Hearst drilling in Ontario is expected to begin in April, the market will be focused on Plex if core gets shipped for lithium assays.

Drill Plan for Allkem's Galaxy/Cyr project west of Brunswick claim

Regional Map of Brunswick's Plex Project

Orfee Zone Drill Plan and proximity to pegmatites

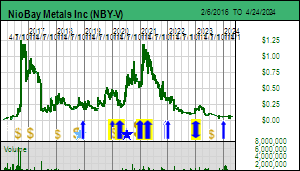

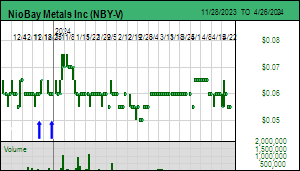

Jim (0:09:08): It has been a month since NioBay rejected assay results for the Crevier project and asked the lab to redo them. Should NioBay shareholders be worried?

NioBay was a risky bottom-fish graduation to the 2023 Favorites Collection because the flagship James Bay niobium story has been neutered by the Moose Cree First Nation which is caught in a community conflict between an anti-mining faction and a pragmatic faction which believes that the best path to preserve ethnic identity is to become locally engaged in commercial enterprise which stops the exodus of the brightest into the melting pot of Canada while ensuring that resources are responsibly exploited.

For those who are not indigenous this topic is a third rail, which I am herewith touching at cancellation risk, which doesn't trouble me because as a cosmopolitan stateless being I am already a zero. The anti-mining lobby has authentic roots in its opposition to practices that dump emissions onto powerless downstream victims while harvesting a one sided profit. But after accomplishing major reforms in places like Canada that resulted in strict standards for mines in jurisdictions that have accountability grounded in democracy, these forces have mutated into a cynical process no longer grounded in pragmatic goals.

Typically classified as "left-wing", the anti mining lobby has in fact become synonymous with a right wing End Timer mentality where the future is subordinated to absolute ideals without any regard to pragmatic goals like generation after generation building on the prior and still flourishing rather than spiraling down a slope of diminishing returns. The pursuit of purity is the ultimate dirtiness, and it really is time for pragmatists to stand up and cry bullshit on both ends of the political spectrum which itself is a fraud because left and right wing are synonymous with autocracy.

However, since this debate at the local level can only be decided by the Moose Cree First Nation, outsiders, and that includes the market, have defaulted to an outcome that can best be described as accepting the Moose Cree as the Left Behind Nation which in its "cling on" form would be obliterated with nobody caring when Tucker Carlson's vision of America annexing Canada becomes reality, which benefits neither MCFN nor NioBay stakeholders. There is substantial upside in the NioBay stock price should the MCFN pragmatists prevail, but the reigning view is that End Timers are in charge of the jurisdiction claimed by the Moose Cree First Nation. NioBay was graduated from the Bottom-Fish Collection to the 2023 Favorite Collection because of a project called Crevier in an entirely different First Nations jurisdiction, one that has embraced pragmatism as the key to its survival.

NioBay's stock price at the moment is entirely dictated by expectations about the future of the Crevier niobium project in southern Quebec. A drill program was done last fall which partly tested to see if there was more to the Main Zone than established by several decades of exploration since 1975 (apparently not). But it also included 4 holes drilled westwards from the shore of Lac Touladi which intersected a pyrochlore mineralized host rock very different from the late stage nepheline syenite dyke that defines the Main Zone whose niobium and tantalum grade just aren't high enough to be commercial, especially given the metallurgical characteristics of the Main Zone's mineralogy. These Lac Touladi holes, first described in mid December, alerted me that there was something new and different about Crevier, perhaps something much bigger than the James Bay deposit trapped in First Nations existential politics. But lately my enthusiasm has started to look foolish, leading some of my subscribers to speculate I have been played by the CEO.

Jean-Sebastian David (JS to reduce 5 syllables to 2), who became CEO in late 2021 when Claude Dufresne resigned to focus on a niobium story more related to technology than geology, started off with about 900,000 shares and during 2022 has bought 532,700 shares in the open market to bring his position to 1,432,152 shares. He stopped buying in late October 2022 when the stock was $0.11. On February 13 NioBay reported that the Crevier assays had been received but were unreliable because the sample assays did not match the interval logs and expectations. Some niobium values were very high where none were expected and very low when pyrochlore was visible in the interval. The lab was instructed to conduct another set of assays and a segment of the preserved half core was sent to another lab as a quality control test.

Since then JS David has bought 151,000 shares in the open market between $0.17-$0.22 with the last reported purchase on Thursday. Now cynics may point out that this is only $30,000-$40,000 worth of stock, and could be just a strategy to paint the tape. But that is to ignore the context of the buyer who is a salaried CEO with no train of successful stock plays in his resume. He is in fact a loner. Only one other insider bought stock in 2022 and that director stopped in late October. When I asked him this week if updated assays had been received he said no and indicated he would keep buying until he receives them at which point he will be blacked out. When was the last time the market saw insider buying and interpreted it as a "stay away" signal?

When I asked other insiders or people close to the company what they thought about the Lac Touladi intersections the best I got was that they were intrigued; none seemed to think that Crevier was turning into bigger and higher grade niobium discovery than the existing nepheline syenite hosted Main Zone which has about 41 million tonnes of 1900 ppm Nb and 241 ppm Ta. One party who should have known better thought the pending assays were about the mineralization related to the Main Zone! So what is going on here? It is making me start to think I am a fool!

NioBay's JSD got back to me this week with the message that he does not yet have assays and will continue to buy until he is in poesseion of material information, so anxiety that NioBay is staring at reliable but crappy assays is misplaced. He says regardless what the holes average, the system they intersected under Lac Touladi is very large and different from the nepheline syenite hosted Main Zone. He has negotiated an arrangement with the Pekuakamiulnuatsh Nation and is taking steps for a serious summer drill program because this new aspect of the Crevier alkaline complex needs to be explored in greater detail.

Based on the spacing of holes 6, 8, 9 and 10 and their depth NBY is looking at a footprint of 2,000 m by 300 m wide by 350 m deep which at 2.6 SG implies a tonnage of 546 million. There is room for a dozen or so 50 million tonne zones in this blob. NBY has posted a bunch of core photos on its Facebook page and I've assembled some in a graphic below. Some of the core photos have crayon grade markings which are probably based on an XRF gun so the readings will be very localized. The point is that decent clusters of pyrochlore are present in the core, and we should not read too much into the thin section analysis about what grade will be (see Crevier Thin Section Report). Note that the core photo with a 1.64% Nb grade has a 0.24% Ta grade marked; the thin section study found no evidence of tantalum bearing minerals, though of course those samples are just tiny slices of a half billion tonne blob.

I don't own enough stock to be over the moon crazy about the potential, but NioBay matters to me because my job as a bottom-fisher and story hunter is to find plays the market and even some insiders hate. NioBay is such a junior which is why I have dug deeper to understand the story. I've obtained a government mag map which clearly reveals the outline of the alkaline complex. In addition I have created a combo graphic which shows the drill plan side by side with an image which allows us to see how the magnetic low (the blue from the government mag image) around the southern end relates to Lac Touladi. The whole thing reminds me of a lobster arm with the claw at the northern end. The dark NW linear in the middle is the nepheline syenite Main Zone where all the historical drilling took place.

The Lac Touladi zone sits where the alkaline intrusive complex transitions into a magnetic low. At this stage the Crevier story should be viewed as an entirely new dimension of the Crevier intrusive complex with a wider range of mineralogy than what characterizes the late stage Main zone dyke. It is prudent to dial back expectations that the assays will include long intersections with blockbuster grades above 0.5% Nb2O5 that sends the stock soaring as the market wonders if another Niobec scale deposit is emerging. More likely detailed drilling to define the zonation within this Lac Touladi zone is needed to properly understand the economic implications.

I suspect the market weakness is coming from shareholders who interpret the assay delay as bad news and who are perhaps realizing that this is not going to be an overnight hole 109 sensation (ie Eskay Creek BZone discovery hole). But I think the assays will have enough juice in them to propel the observers on the sidelines beyond being intrigued. Depending how you look at it, the market is either 100% discounting a social license breakthrough at James Bay or discounting the notion that Crevier is becoming something new, different and better than the Main Zone, perhaps even better than the James Bay project caught up in MCFN politics. My inclination is to continue to accumulate the stock, though, because the results are unlikely to be blockbuster, there may be a better opportunity to buy, albeit at a somewhat higher price, after the assays are out and the uncertainty about a total bust is gone. It's not like JS David has a history of crying false wolf. This is the first time he is crying wolf and just about everybody with clout is ignoring him.

CEO JS David's lone wolf insider insider trading activity

Regional Magnetic Survey showing Crevier alkaline intrusive complex

Crevier drill plan contrasted with map showing magnetic low of intrusive complex

Core photo shots of Lac Touladi Holes at Crevier

Main Zone outrcrop and core photos

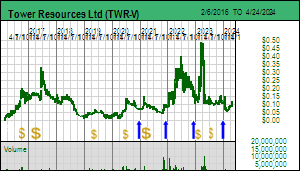

Jim (0:15:45): Last year you talked often on Kaiser Watch about Bottom-Fish rated Tower Resources but it never made your 2023 Favorites Collection. The stock has nearly tripled during the past month. What is going on?

Tower Resources Ltd is currently Bottom-Fish Spec Value rated and is a candidate for graduation to the KRO 2023 Favorites Collection. I published Tracker March 22, 2023 as an update on what Tower was all about in 2022 and what has happened in early 2023 to triple the stock price from its year end bottom-fish level and explain why the stock could head a lot higher. Tower expects assays for the new Thunder Zone on the Rabbit North project by early April, and if these are good, Tower will be graduated to the 2023 KRO Favorites. Most of the Tracker is covered by the 8 minute segment of this Kaiser Watch episode, but I am not providing the details here in written form because discussion of the Bottom-Fish Collection is supposed to be restricted to KRO members paying USD $450 annually for access to the research platform and the Bottom-Fish Workshop.

Time is money, and personally I prefer to read rather than listen or watch because when I read my mind dictates how much time is consumed, whereas audio and video dictate how much time I must donate to consume the content. The trend these days is toward mediating content via video or audio rather than the written word. KRO members post links to such content in the KRO Slack Forum which is especially appreciated when the member includes a synopsis of the topic and an explanation why it is worthwhile. The written word, however, is superior because the time needed to digest its wisdom is unrelated to the time taken to craft it. I took a lot more time to craft the Tracker than to blurt out from memory without the visual cues of a powerpoint presentation the 8 minute KW segment about Tower. Yes the audio is free, but the written version is better and costs less time. This week's NioBay segment is an anomaly, but not really, for NioBay is already a Favorite and thus not subject to the KRO paywall. However, the gist of the KW segment on NioBay was presented earlier this week within the KRO Slack Forum which is an interactive privilege extended to paying KRO members provided they stick to basic decorum rules.

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch March 17, 2023: Will the bank run scare help resource juniors?

Jim (0:00:00): How will the banking crisis affect resource juniors?

The failure of Silicon Valley Bank last Friday has shone a light on a problem created by the Federal Reserve's determination to subdue persistent inflation by rapidly reversing the ultra low interest rates of the past decade. When the covid pandemic hit in 2020 the Federal Reserve flooded the system with liquidity to prevent a serious recession arising from the disruption of business activity and consumption. The result was that savings deposits climbed, but because of the economic uncertainty the depositors' money was not lent out to support businesses and real estate purchases, but was instead parked in low yielding government bonds whose yield was slightly better than what the banks were paying the depositors. When interest rates rose sharply the value of the banks' bond assets dropped, but the value of customer deposits stayed the same, which meant that the difference had to be accounted for by the bank's capital which belongs to the equity shareholders of the bank. Normally this should not be a problem, but Silicon Valley Bank was unique in that it specialized as the preferred banker for the countless startups that the west coast venture capitalists had funded until the tech bubble ended in 2022.

Many of these startups remain private and some achieved "unicorn" status which means that based on the price of the most recent financing round, the private company had a market capitalization in excess of $1 billion. Most of these startups are simply spending machines as they develop whatever fin-tech or other concept that supposedly will eventually conquer the world. Even when they have revenues these are dwarfed by "market development" costs, which became acceptable with the original dot-com bubble that ended in 2000. The end of ultra low interest rates in 2022 put a lid on valuation increases because when government bond risk free rates are 4% that translates into a Price-Earnings ratio of 25 rather than 200 as was the case when yields were 0.5%. The prospect of even higher interest rates would further reduce the value of future success. Investor interest in funding these unicorns in danger of losing their horns dried up in 2022, which disrupted the assumption that the startup world could continually replenish its treasury with new funding.

Much of the money spent by tech sector startups goes toward human labor, with payrolls being met on a semi-monthly basis. Because the west coast venture capitalists encouraged the startups they were backing to bank their cash at the Silicon Valley Bank, that bank had an excessive concentration of deposits which in 2022 were being depleted by the ongoing payroll expenses that the venture capitalists were having a hard replenishing with new funding. This was a de facto run on the bank whose bond assets were suddenly worth less and represented losses if liquidated to generate the cash to meet withdrawals. It was different from a more typical bank run where ordinary depositors start withdrawing their money to chase better yields elsewhere and not caring that they forfeit the tiny interest that was being paid on their ultra low yielding term deposits.

The startups were not like ordinary depositors who at most leave $250,000 in bank deposits because that is the maximum amount insured by the FDIC (we have since learned that super-libertarian Peter Thiel left an enormous amount of his capital in SVB even as he urged his fund to sneak out the back door). But when you are a business you have to maintain a much larger cash balance to fund ongoing expenses. Venture capitalists like Peter Thiel became aware of SVB's vulnerability and started alerting the startups they were backing about the risk of a bank run that could wipe out their remaining cash which was becoming increasingly difficult to replenish with new funding, especially at prices higher than the last round. Making payroll is a sacrosanct rule, so the recognition of a payroll catastrophe risk would have unleashed panic within a startup's management. This created a classic prisoner's dilemma well known from game theory. The venture capitalists were watching this with horror from the sidelines, because if the startups they are backing blow up because their capital has vanished and the brain trust that underpins the development story disperses when payroll is no longer being met and their options and RSUs are worthless, the VC's investment is down the toilet. Unfortunately, many of these VCs are chest-thumping full of merit libertarians who celebrate the superiority of the individual rather than the collective, so it was natural that some chose to bolt before their competitors did the same. And once that was underway, the Silicon Valley Bank was dead in the water and had to be seized by the government.

The equity of the Silicon Valley Bank's shareholders has been wiped out and there is no way of getting that back, which is why bank stocks in general tumbled last week and continue to be under pressure. Instead of letting SVB depositors take a haircut on their deposits above $250,000, the government decided to guarantee the full amounts. This has been widely criticized as creating absolute moral hazard of the sort that created the savings and loan fiasco of the 1980s because it is assumed the government will now guarantee everybody's bank deposits. While plenty of individuals may have had deposits in excess of $250,000 at SVB, most of them likely have much of their wealth stashed directly in treasury notes, mutual funds or equities held by a brokerage firm where they are segregated from the firm. So bailing them out would not have been a priority for the government, but preventing the collapse of the entire west coast startup eco-system, putting tens of thousands workers on the street and effectively destroying whatever concept they were developing, would be a different matter. Seeing some of these fin-tech (aka crypto) startups vanish might not be a bad thing, but killing the rest would be.

Unfortunately the consequence of the Silicon Valley Bank failure is that it has awakened everybody to the structural risk created for the banking sector by the monetary fight against inflation unleashed by Jerome Powell in 2022 which is only a quarter so far of what Paul Volcker needed to do in 1981 to subdue inflation. The inflation back then was difficult to subdue because the rapid increase in oil prices had created a wage-cost push spiral (COLA clauses - cost of living adjustment) which was not unwound until the mid eighties. Today's inflation has two different drivers which are likely immune to monetary policy.

One is that demographic change is shifting pricing power into the hands of Millennials and Gen Z as the Boomer generation drifts into retirement and plans to live off its concentrated wealth until the sun sets on them around 2040-2050. The Boomers, the most selfish generation ever, have exhibited reluctance to sacrifice any of its wealth for the energy transition goal of preventing global warming from ruining the future of their children and grand-children. It is easy for a Boomer to be a climate change skeptic and argue that the planet may fix the problem all on its own because very few Boomers will be around to find out if they were right or wrong. Whereas past generations all bought into the idea of family formation and enduring mid-life sacrifice that guarantees success for their children, after which the parents can enjoy retirement, today's younger generations are to a fair degree embracing the same End Timer mentality as their elders by refusing to work on terms that guarantee their survival in what is shaping up to be a terrible future without miraculous intervention. The only way the economy can fight this attitude is by rushing to deploy automation and AI to substitute for a shortfall of workers, a path that Japan and China are now aggressively pursuing because they have a terrible demographic problem. But the automation-AI replacement will not happen overnight, so wage based inflation pressure will be difficult to eradicate without plunging the economy into a deep recession or depression, which will have the consequence of radicalizing the younger generations.

The other inflationary pressure is the reversal of the deflation created by the globalization of the past two decades which enabled China to become a great power rival to the United States. China's embrace of autocracy and decision to have state owned entities reach deeper into all aspects of the Chinese economy is creating geopolitical tensions and wiping out the multinational dream of selling goods and services to the Chinese population. Western businesses are now withdrawing from China, and while they initially looked at relocating production capacity to China's neighbors in southeast Asia, the clear signs that China sees this as its turf is forcing them to look at India with its complicated bureaucracy or reshoring to home bases like the United States where higher environmental and human costs prevail. Reshoring production capacity will involve higher CapEx and OpEx than businesses have enjoyed in a globalized economy. In addition, the geopolitical fracturing of the global economy threatens to disrupt raw material supply from environmental shit-holes like China and Russia who together dominate 40% or more of the supply of most metals. Sourcing new metal supply not subsidized by autocracy which leaves downstream victims powerless to protest will be a source of raw material input cost inflation.

Jamming interest rates through the roof will not make these structural inflationary pressures go away. But doing so will deflate the value of the assets in which banks have parked their customers' deposits. Almost everybody now understands this and containing the rising panic will be difficult to do while continuing to jack up interest rates. Bitcoin has rallied 20% since Monday when it became clear that the west coast crypto startups would not be allowed to die. People are buying Bitcoin because they see only price risk in its ownership, not evaporation risk as they now see with their bank deposits. But Bitcoin is a Ponzi scheme and could overnight suffer its own monster "bank" run.

The biggest beneficiary of the bank run scare will likely be gold, because gold is energy stored in a physical form, not in the sense that gold can be burned to make the wheels turn, but to extract it from the ground and concentrate it into a gold bar requires energy. Although the world adds about 100 million ounces annually to the gold stock, the incremental addition is a declining percentage of the total above ground gold stock. Without a higher real price this trend cannot be reversed. Unlike Bitcoin, you cannot make gold disappear by pulling the plug on it. Bitcoin is an ongoing energy liability whereas gold is stored energy. Inflation will not go away, keeping investors fearful of additional haircuts to the value of their bonds and equities if the Federal Reserve resumes raising interest rates. Gold's price theoretically will track inflation, which means owning gold should allow one's purchasing power to remain stable, except for the inconvenient fact that countries like the United States treat gold as a "collectible" whose nominal value gain is subject to an onerous capital gains tax. Owning gold as an inflation hedge is thus a stupid strategy. But gold's real role is to hedge against uncertainty, the risk of massive dislocations. The era characterized as the "end of history" has come to an end, and gold's role as a hedge against uncertainty is now ascendant. There is now a solid reason to shift some of one's wealth into gold, which, combined with growing demand from autocracy central banks eager to escape a weaponized US dollar, could allow gold to break through $2,000 and finally establish $2,000-$3,000 as its new trading range.

The resource juniors will benefit from the banking crisis because gold will once again be topical if $2,000 becomes the new base. One could worry that the banking crisis and high interest rates will negatively impact macro-economic demand for metals, which should result in lower prices and thus chill investor interest in juniors exploring for or developing non-gold metal deposits, making gold the only game in town. But that worry is offset by the fact that the need to replace metal supply that currently comes from increasingly unfriendly autocracies is only going to worsen, even if America becomes an autocracy which I guarantee you will not make America best buds with China and Russia, regardless what Tucker Carlson and Donald Trump think. And there is the fact that the car makers are now hopelessly committed to the energy transition as far as electric vehicles are concerned, and the IEA has made it clear how much additional supply of copper, nickel, lithium and rare earths beyond macroeconomic consumption are needed to make those EV deployment goals reality. Naturally investors in resource juniors cowered in fear this week as they watched the global banking sector, according to the Financial Times, see $450 billion in equity value vanish. But on Friday while the general equity market trembled further, the GLD ETF gained ounces and the traded value of TSXV resource listings jumped dramatically.

Daily Gold Holding Change for GLD ETF

TSXV Trade Value Split between Resource & Non-Resource Listings

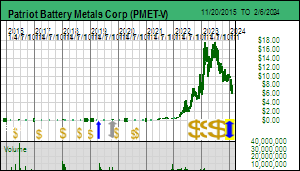

Patriot Battery Metals was halted on Tuesday to allow completion of a $50 million charity flow-through financing and did not resume until Thursday. The financing was done in the form of 2,215,000 shares at $22.57 and gives PMET working capital in the $60-$70 million range depending on how much has been spent at Corvette since the start of the year. The entire financing was actually bought by Australian entities. After Peartree stripped the flow-through benefits from the stock all of the shares were sold through Australian brokerage firms or the subsidiaries of Canadian firms to Australian investors in the form of 22,150,000 shares so called Chess depositary interests (CDI) at AUD $1.20. Just as British and Australian listed companies trade on North American exchanges on a 10:1 rollback basis (ie Piedmont Lithium), stocks with a primary listing on North American exchanges trade on a 10:1 split basis on the ASX. So whenever you see the PMT price on the ASX, multiply by 10 and adjust by the AUD-CAD exchange rate to calculate what the TSXV equivalent price will be. The stock is down from its $14-$15 range during PDAC week in part due to overall market weakness as the banking crisis began to emerge, but also to reflect the discount needed to place the stock in Australia.

The big question is whether or not PMET will bounce back after loading its treasury with an extra $50 million. The timing of the halt during a week when conservative investors watched the banking sector lose nearly a half trillion dollars in equity value, stocks that are supposed to be safe and boring, has injected a new dynamic into the PMET market structure. The stock will likely come under pressure from the exercise of 4,038,409 warrants at $0.25 that expire June 30, 2023, and 26,850,727 warrants at $0.75 that expire mostly at the end of the year. Normally a warrant overhang is a problem for a junior when the exercise price is above the market price because the holders will short against the warrants every time the stock rallies through the exercise price. An then cover the stock in the market when the stock price sags, sucking up incoming new risk capital. PMET has a different problem in the $0.75 warrants represent a paper gain of $286 million at, say, $11.41 per share where it was trading mid day Friday. If the holders wanted to collect their profit by exercising and selling their stock, the market would need to eat about $300 million worth of stock. That is not chump change.

The warrant holders may until last week have been happy to wait for a potential buyout later this year, but during the two days while the stock was halted to complete the financing and the general market was shuddering from the bank run crisis, they probably experienced a considerable amount of fear that their paper profits might evaporate. The premise behind PMET's recent $2 billion valuation is the idea that the world is determined to go through with the energy transition in order to ensure an inhabitable future for the children and grandchildren of the Boomers. One plank in the energy transition strategy involves electric vehicle replacement of internal combustion engine vehicles. The IEA projects that the for the 2030 EV goals to be achieved the world will need to expand its lithium supply by 600%. But none of that will happen if the world descends into an apocalyptic End Times mentality. So what happens on the global stage matters to shareholders of PMET.

Then there is also the recent financing reality in the resource sector where major financings are done at major discounts to the market. Nobody knew what the term structure would be for a financing most knew was coming, so existing shareholders likely weren't happy to see in effect a bought deal at AUD $1.20 or $12 which, because $1.00 AUD is worth about $0.91 CAD, implied a $10.92 CAD price for PMET. During the past year we have seen a spate of bought deals at 20% or more discounts to the market price, which resulted in an instant haircut for existing shareholders that was not rewarded with a rebound after the financing was completed. So although PMET post-financing has $60-$70 million working capital to finish delineating the CV5 lithium deposit and proceed with an economic study, spooked warrant holders will likely start exercising the warrants and banking the profit.

The good news about the Australian purchase is that the stock went into strong hands which apparently included Mineral Resources and Pilbara Minerals, two $14-$16 billion market cap ASX listed lithium producers with apparent ambitions to dominate a future $100-$200 billion market while established majors like Rio Tinto, BHP, Vale and Anglo American pick their noses. Earlier this year there were unconfirmed rumors that Mineral Resources was accumulating PMET in the open market, which raised hopes that it might launch a hostile bid for PMET, perhaps ahead of a maiden resource estimate expected in late Q2. Since nobody has disclosed passing the 9.9% insider threshold, all this is largely rumor, though the paperwork for the Australian purchase would make clear who bought what in the current financing. If it is true that Mineral Resources and Pilbara bought toeholds, this bodes well for the stability of the PMET market as it digests stock from the warrant exericse.

Changing the subject, while updating the PMET financials for my KRO database I noticed a peculiar entry in the balance sheet of a kind I had noticed last year in the case of another junior whose CEO suggested I talk to the CFO for an explanation. The Dec 31, 2022 balance sheet shows current assets of $20,990,581 and current liabilities of $10,537,259. A standard measure of a junior's financial health is working capital, which is current assets minus current liabilities. On this metric PMET had only $10.6 million working capital at the end of 2022. But one of the current liabilities items is called "flow-through premium liability" and it is $8,553,172. This is an accounting fiction which new regulations now require companies to include in current liabilities. The amount represents what the company would be liable for to Canada Revenue Agency (ie the Canadian equivalent of the IRS) if an audit determines that the flow-thru funds were not spent properly. There have been cases in the past were flakey life-style juniors raised flow-through money and failed to spend it on qualifying exploration, which resulted in the flow-thru benefits of the placees being reversed by CRA. This resulted in a huge mess for the junior and the investors, especially for the investors if the junior has effectively blown all its capital and the pump and dumpers behind the junior have walked away.

While the intent is to alert investors that the company has an obligation to spend flow-thru money properly, it does cause the working capital number to understate the financial health of a company that has flow-thru funds in the bank. When it is confirmed that the money has been spent properly, this line item vanishes via "amortization" recorded as an inflow rather than outflow. Of course the cash by then has also vanished because it needs to be spent by the end of the year subsequent to the one in which it was raised. In the case of PMET's Dec 31 financials the FT premium liability is linked to the $20 million charity FT financing PMET did in September at $13.27 when the stock was trading at half the price. If you trust the junior as being run by competent management trying to create real value through exploration, this line item is not necessary, and potentially misleading. We will have to watch for this distortion of a junior's financial health, just as we have to do with an expense line item called stock option compensation which is also an accounting fiction that must be stripped out to reveal the true burn rate of a junior. It is unfortunate that the more regulators try to achieve transparency, the more they achieve obfuscation.

Jim (0:23:54): What is the status of Eagle Plains royalty spinout?

Eagle Plains created some confusion last week with an update that declared March 17 to be the day of record without making clear what that day of record referred to. This led some to conclude that March 17 was the day of record to get the 1:3 Eagle Plains royalty spin out. With 2 day settlement that meant March 15 was the last day to buy Eagle Plains to get the spinout. The date is important because the stock will likely drop somewhat to reflect the absence of the royalty portfolio. On Thursday morning Eagle Plains put out an emergency news release clarifying that March 17 is the record date for being eligible to vote at the April 26 special meeting to approve the spinout. That makes sense because how do you declare a record date for a dividend in specie spinout before you have shareholder approval? Eagle Plains management went to great effort to poll its shareholders about their views on the spinout before it formalized the spinout deal, but none of that guarantees slam dunk approval. Just consider that a week ago everybody though the banks were solid after the post 2008 reforms, and now everybody is freaking out.

I'm not sure how this slipped past the lawyers, but if March 17 were truly the record date for the spinout, but anybody buying Eagle Plains after March 17 wouldn't know if they still get the spinout or not. In any case, this confusion is now fixed. The record date will be declared after the April 26 meeting approves the spinout, and this usually comes in the form of an official TSXV notice. Eagle Plains continues to be a KRO Favorite which is now up 50% to reflect the $0.10 implied value of the spinout, but the stock has potential to go a lot higher in Q2 when drilling gets underway at the Vulcan project. In addition, on March 2 EPL announced that it had staked 2 lithium prospects in British Columbia and 4 in Saskatchewan. It has not disclosed claim locations or sizes because it is busy staking additional lithium pegmatite plays and does not want to tip its hands. Saskatchewan is now shaping up as a hot lithium province.

One of my year end bottom-fish stocking stuffers, Searchlight Resources, tripped up in late January when it optioned 100% of the Hanson and Jan Lake lithium prospects to Brunswick Exploration for $35,000 up front. Brunswick's Bob Wares couldn't believe his good fortune. While the LCT-type potential of the Jan Lake pegmatites is at this stage unknown because nobody ever checked, the Hanson Lake pegmatites to the south are confirmed LCT-type pegmatites. I was surprised during the recent Toronto MIF Backstage Interview when Bob mentioned that after drilling the Anatacau target in James Bay and Hearst target in Ontario Brunswick will be drilling the Hanson Lake pegmatites, possibly by June. Searchlight's Alf Stewart and Stephen Wallace, who were quite pleased to have quadrupled their $8,500 staking expense in less than 3 months, were taken aback by the shareholder blowback they received. Searchlight is supposed to be about the Kulyk Lake rare earth play, and secondarily the high grade Bootleg Lake gold play not so far from the Tartan Lake gold play of Satori which Rob McEwen thinks might be his next Red Lake. For god's sake, lithium is Plan C!

Wallace was not pleased by the blowback, mumbled a string of expletives, rolled up his sleeves, and burnt the midnight oil rummaging through Saskatchewan's archives. On February 27 Searchlight announced the acquisition of 7 new staked claim groups, one of which, Davin Lake, at 27,632 ha, is a substantial land package. Stephen, what can you tell me about it? Sorry, you will have to wait a bit. It seems that Saskatchewan may be an unsung lithium hero which smart groups like Eagle Plains and Searchlight are now intensely parsing, hence all the secrecy. That is why neither Eagle Plains nor Searchlight are publicly revealing the locations of their new lithium claims, though of course as experienced users of Saskatchewan's MARS system they know exactly where each other's claims are located unless obscure numbered companies are being used to do the staking.

The market has not rewarded Searchlight for its replacement lithium claim package, but that is due to an overhang of 19,040,000 warrants at $0.05 that expire May 26, 2023. Searchlight had $1.8 million working capital at the end of December 2022, so is not desperate to raise money. This situation is a special opportunity to bottom-fish for Searchlight (yeah, I want to prove this stocking was not stuffed with coal). Over the next two months lots of disgruntled stock can be accumulated by nailing a nickel bid to the wall. As the warrant expiry approaches and the supply at a nickel dries up, smart bottom-fishers can post a bid at $0.055 to coax warrant holders to capture a short term 10% gain by exercising their $0.05 warrants and selling the stock at $0.055. In a climate where ultra sophisticated investors are losing 10%-15% on their ultra conservative portfolios, who will sneeze at a fast 10% gain? But everything is a matter of context. KRO members know why Searchlight is a multi-pronged bottom-fish whose missing piece in the form of a structural problem will vanish in two months. If Brunswick, with its $16 million treasury, makes Hanson Lake rather than breaks it in early Q3 of 2023, Stephen Wallace and Alf Stewart may yet have the last laugh as the market has a "Saskatchewan WTF" reaction. And you can count on the Eagle Plains team to also be tethered to the Saskatchewan lithium rocket launch.

Disclosure: JK owns shares of Brunswick and Eagle Plains; Brunswick and Eagle Plains are Fair Spec Value rated Favorites; Searchlight is Bottom-Fish Spec Value rated

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch March 10, 2023: "Lithium, Lithium, Copper" - PDAC Buzz

Jim (0:00:00): You just came back from a week in Toronto attending the Metals Investor Forum and the PDAC conference. What was the Metals Investor Forum like?

The Metals Investor Forum held in Toronto on March 3-4, 2023 was the best yet for the Toronto location, but it was a far cry from the standing room crowds at Vancouver MIF in late January. The lower turnout may be due to the blizzard predicted for Friday and Saturday that discouraged investors from traveling downtown. The blizzard also disrupted travel plans for delegates headed to Toronto for PDAC who saw numerous flights delayed or canceled. My MIF session was the last one at 4:30 and my group presented to a room about 75% full. The presentation and backstage interview links are now available in my KMW MIF Blog. Here is a link to the pdf for my MIF March 2023 Presentation: The Eye of the Hurricane.

Of the 40 or so MIF companies my group was still the only one with exposure to critical minerals (not counting copper of which there were several good juniors present) and specifically lithium. The rest of the companies were precious and base metals juniors. Last year during the June 2022 Toronto MIF I introduced the idea of Lithium Mania 2.0 featuring Brunswick Exploration Inc, at the time trading at $0.15. Brunswick has since soared above $1 and filled its treasury with $16 million to support its multi-pronged strategy of testing the 600 plus pegmatites management has identified and staked or optioned in Canada. A large number of its properties are located in the James Bay region of Quebec which is evolving into a Great Canadian Area Play, the first one since the 1990s and possibly the mother of all such plays thanks to the prospect of lithium becoming a $100-$200 billion market by 2030. While the corporate presentations provide the basic outline of each junior's story, for more nuanced insights about the underlying potential check out the Backstage Interviews.

One junior I would like to highlight from my group is VR Resources Ltd because of a very surprising development announced a couple weeks ago and which CEO Mike Dunning spent a fair bit of time describing. Last fall VR conducted a drill program on the Hecla-Kilmer rare earth prospect in the James Bay Lowlands of Ontario as well as a single hole on a large magnetic low to the north on a property called Northway. VR is focused on the northeastern third of the Kapuskasing Structural Zone which runs from James Bay 500 km to Wawa where the 20 million ounce Hemlo deposit was found in 1982. Rifting caused the KSZ to become thermally active between 2-1 billion years ago which spawned intrusive complexes such as Hecla-Kilmer and NioBay's James Bay carbonatite. A 400 million year old limestone platform covers the Archean aged basement in the northern third which means targets like Hecla Kilmer and Northway are geochemically blind. VR's strategy is to test geophysical anomalies to see if they might be an IOCG system or an alkaline intrusive complex that includes critical mineral enriched carbonatites. The region saw a wave of drilling during the 1960s and 1970s typically testing magnetic highs as potential carbonatites or kimberlites. No kimberlites were discovered, though this was not a big deal because Archean aged diamonds in the diamond stability field would have been turned to graphite during the mantle upwelling 2-1 billion years ago.

VR finished its drill program in mid November and spent the next few months consulting various diamond exploration experts about the unusual "diatreme breccia" intersected in the bottom 40 m of a 282 m hole. All of them have declared the rock to be kimberlite, though thin section petrology still needs to be done to deliver formal confirmation. The hole was a puzzle while being drilled because the basement rocks were supposed to have a limestone cover only 50 m thick in this area based on nearby past drilling. Instead the hole passed through limestone into a thick interval of mudstone with igneous rocks intersected at about 240 m depth; the geophysical data has now been remodeled to show what appears to be a 1,200 m wide kimberlite whose eruption, likely in a marine environment, excavated a giant crater that later filled with sediments that became the mudstone. If this is indeed a kimberlite, or a dense cluster of of kimberlite eruptions as is the case with the world-class Grib and Jwaneng kimberlites, this will be a very large tonnage kimberlite.

Based on the age of the mudstone Mike Gunning and Justin Daley believe the kimberlite was emplaced between 410-450 million years ago before the limestone covered the area. The magnetic low appears to have been caused by the earth's poles having been reversed during this period relative to when the basement rocks formed. VR has now staked a couple dozen similar but smaller magnetic lows on the premise that these might also be similar aged kimberlites which tend to erupt within a similar time period. It is a testament to market skepticism that nobody has bothered to map stake claims around these "postage stamps". The tantalizing idea is that VR may have discovered an entirely new field of kimberlites under fairly shallow limestone cover. This field would be completely blind and invisible to till sampling for indicator minerals because they were never exposed to glaciation. The Northway target itself was never drilled, likely because it was "too big" to be a kimberlite and nobody was sure what else it might be that was potentially of economic interest.

While it is a fascinating story Northway at this stage is still a long shot. The kimberlite will not have entrained any diamonds formed more than 1 billion years ago because the KSZ thermal event would have wiped them out. However, diamonds can form fairly quickly if the pressure-temperature regime that allows diamond formation returns. For example, the diamonds at Victor 300 km to the northwest have been age-dated at about 700 million years. The Victor pipe does not have the harzburgite or eclogite normally associated with diamondiferous pipes, but instead a form of lherzolite (G9s) is the main diamond bearing xenocryst present at Victor. Eclogite typically occurs deeper than harzburgite because it is formed from basaltic ocean slab that has been subducted at a continental margin and underplated the craton keel.

VR has decided the sample is too small to submit to caustic fusion for the recovery of micro diamonds. The hole was drilled on the margin of the anomaly in the hope that this is where critical mineral enrichment took place. The plan now is to drill a long angle hole from the existing drill pad across the anomaly to confirm its width and determine the extent of multiple vertically zoned pulses. Another hole will be drilled in the center once a drill permit has been received for the new location (Ontario, in what appears to be a make work program for bureaucrats who would otherwise be on welfare, requires specific permit applications for each drill location). The earliest one could thus hope for micro diamonds would be late in Q3 or early Q4 given slow turnaround.

The next milestone after confirming micro diamonds are present would be to conduct a mini bulk sample to confirm macro grade extrapolated from the micro diamond distribution curve if present. The earliest thus one could hope for macro diamond confirmation is a year from now, given the timelines for diamond exploration results turnaround. Meanwhile VR will have the option of testing the other magnetic low anomalies to see if they are also kimberlites, or possibly a different type of intrusive with critical mineral potential.The junior will continue delineating the higher grade rare earth zones within Hecla-Kilmer.

The James Bay Lowland area does have a bad First Nations reputation because of opposition to NioBay's James Bay niobium project. Most of the rivers in the James Bay Lowlands are muddy silt laden water bodies, but the North French River system has clear water and its watershed is effectively off limits for mine exploration and development. The James Bay carbonatite is near the NFR watershed but outside it, though that does not register when the emotional buttons of Moose Cree First Nation members are pushed by outsiders who make a living from opposing mining. The area being explored by VR is well to the west of the NFR watershed, and close to rail and power infrastructure.

JK: better than past attendance, but hampered by a snowstorm that included thunder and lightning. Spoke to 3/4 full hall compared to 1/3 full last June when I introduced Brunswick Expl at $0.15 as one of my companies. I was still the only speaker at MIF with lithium as a topic and companies involved in lithium. The Eye of the Hurricane. The YouTube links to my talk and the corporate presentations and backstage interviews are now available.

James Bay Lowland Map and Location of North French River Watershed

Will the Northway kimberlite prove part of a new diamondiferous kimberlite cluster?

Jim (0:04:51): What was the Prospectors and Developers Association conference like?

PDAC 2023 was the first full-fledged in-person conference since 2020 and recorded 23,819 delegates. Although this was lower than the 28,000-30,000 delegates PDAC used to attract, the aisles in the Investors Exchange and Trade Show were packed with people, forcing one to bob and weave past people marching with smartphones in their faces. What was not packed was the Sunday Newsletter Presentation Session which Peter Botjos organized for several decades before retiring last year. This all day session featuring newsletter writers with 25 minute speaking slots was hugely popular during the 2000's, but began to wane during the decade long resource junior bear market that was underway by 2013. In 2020 I was no longer welcome because I was also participating in the Metals Investor Forum which overlapped with the Sunday though this is no longer the case. Last year I participated in an hour long panel of newsletter writers at 11 AM (2022 PDAC was only Monday-Wednesday) which I thought went very well though I nearly missed it because Exhibit Only Day Pass holders were not allowed into the convention center until 1 PM on that Monday because of a bottleneck (I had to be smuggled in with somebody else's All Access Pass). Needless to say, any retail investors who bought a Day Pass for CAD $25 last year missed out on this shortened version of the newsletter session, which might explain why the room which seats several hundred people was only quarter full last year.