Hello Guest User, You are visiting this website from a computer with an IP address of 172.70.131.177 with the name of '?' since Sat Apr 27, 2024 at 10:54:15 AM PT for approx. 0 minutes now.

Kaiser Media Watch Blog - July 31, 2023 to July 31, 2023

KRO Blog Overview

The KRO Blog is where unrestricted content of a time sensitive nature is posted. It includes the Kaiser Media Watch Blog which features content involving John Kaiser produced by third parties such as the Discovery Watch series by HoweStreet.com, interviews by outfits such as Investing News Network, SDLRC related commentary, the KRO Monthly Summaries, and just about anything else John writes that is not intended exclusively for the fee based KRO Membership.

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

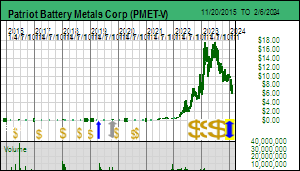

Kaiser Watch July 28, 2023: Countdown for PMET resource estimate

Jim (0:00:00): Will Patriot Battery Metals deliver its maiden resource estimate in July as promised?

Patriot Battery Metals Corp did promise a maiden resource estimate in July and Monday July 31 is the last opportunity to deliver, with the ASX getting it on our Sunday night. Given that Night Market Research challenged PMET's credibility about its MRE timing, which I discussed in KW Episode July 14, 2023, I would be shocked if CEO Blair Way and Chairman Ken Brinsden fail to deliver. The real question is how will the market react to whatever is published? The tonnage reported will be meaningless because PMET will likely publish a set of inferrred resources at different cutoff grades so that they can isolate the higher grade Nova portion. They do have to pick a base case resource and that will probably be one that allows a resource just over 100 million tonnes to prove Night Market Research wrong.

The real one, however, which potential bidders for PMET will be looking at, will be the one which allows an optimal scale for that region. What do I mean by optimal? A key factor will be the combination of mine life and open pit mining scale. Pegmatites tend to be elongated bodies and CV5 is no exception, but when they outcrop or are close to surface they deserve to be open pit mined. But because of their elongated nature the waste to ore stripping ratio will be very high, so giant 100,000 tpd open pit operations such as you see with copper porphyry systems or what FPX Nickel contemplates for the Decar nickel project just isn't feasible for LCT type pegmatites. And since the dip is sub-vertical, chasing the dip to a vertical 300 m pit limit does constrain the tonnage available.

There is also the additional consideration of the ideal mine life. Normally one likes to aim for a 20 year mine life, but, given that we would be lucky to see a James Bay lithium mine producing by 2030, would it be wise to plan such a long mine life? Lithium is not like copper or nickel whose fundamental uses as an electricity conductor and stainless steel input are unlikely to change in the long run. But lithium use is linked to a specific technology which may be on its way out by 2040, possibly eclipsed by hydrogen fuel cells. The mission critical problem for energy transition goals is meeting the demand surge between now and 2035, which suggests choosing a mine life of 10-15 years.

For these reasons selecting a higher cutoff grade and a smaller operating scale may be more optimal than shooting for maxium size and economy of scale. In the case of Corvette, the 50 km trend may have multiple similar deposits. It might be prudent to develop multiple open pits at lower mining rates but higher grades feeding a larger capacity central processing facility that could also include a refinery so that you do not need to ship concentrates long distances. Anybody looking at PMET as a buyout target will be thinking in these big picture terms.

My prediction is that the maiden resource will be presented in a manner that allows bulls and bears alike to all claim victory, but what counts is what the Albemarles and Rio Tintos of the world see as their preferred development scenario. I wouldn't be surprised to see a range of resource estimates at different cutoff grades which includes NMR's 76 million tonne estimate all the way to 150 million tonnes. The key will be the open-pittable cutoff grade. What becomes the true "base case" will depend on the desired mine life in the eyes of a future developer. Generally when a discovery shifts from resource estimate delivery to feasibility demonstration, in essence "cost discovery", the eventual proven and probable resource ends up smaller and higher grade than the base case maiden resource estimate.

We should also keep in mind that the cut-off grade is half determined by OpEx considerations, but the other half is the revenue side. What lithium carbonate price is it reasonable to assume for the mine life? With established metals like copper and nickel the cost curves of existing mines and potential mines provide a guide to the future, linked to macroeconomic predictions about overall demand growth. Electric vehicles represent a policy driven disruptive technology that entrains lithium demand. The world has never seen anything on this scale, except perhaps in the post WW2 period when uranium as the fuel for nuclear energy caught the market's imagination. Seven decades later uranium supply limps along with an annual value below $5 billion while lithium supply, worth $200 million in 2005, is heading towards a $100-$200 billion annual market if EV deployment goals for 2030 are to be met.

Every lithium bear out there, just as during the rare earth boom of 2009-2012, will moan that lithium is everywhere, and that the world will never be caught screaming, "my kingdom for a pallet of lithium". Along with the astonishing demand trajectory there is also the reality that extraordinary lithium resources are sitting under everybody's noses, Bolivia's salars among the most staggering. But what does it take to mobilize these resources? What the Lithium Mania 2.0 detractors do not understand is that time is of the essence. How long will it take out for Chile, Mexico and Bolivia to sort out a fair split for the lithium windfall? In the case of direct lithium extraction (DLE), or claystone flow-sheets, how much CapEx and time needs to be invested in order to "know" this supply is truly part of the cost curve? Never before has so much uncertainty existed about the future price of a metal.

The reason the James Bay lithium deposits are on the radar of downstream lithium users is that their cost structure is reasonably well understood, with caveats regarding the risks that Canada's tolerance for the anti-mining lobby or First Nations extortion is absolute. But this structural opposition can vanish overnight, especially once politicians start to connect a destiny of "burn baby burn" with opposition to resource development. When PMET publishes its cutoff-grade defined range of CV5 resources, what actually matters will be in the eye of the beholders, and those beholders may include parties like Toyota who think they have secured the holy grail of a solid state lithium ion battery, and are plotting to seize the EV mass market in 2030 and beyond. The lithium input cost, even though the future commodity price may range widely, will still be a fraction of the future overall cost of an EV.

The main line of attack by NMR was that under the Lassonde Curve logic the market will lose interest as PMET shifts into the cost discovery portion of the project. This becomes a game theory problem for the potential bidders. If they all stay quiet the price will sink. But I don't think the producers have the discipline to stare down PMET as it moves into tedious feasibility demonstration. The competition in the wings are giants like Toyota who are grappling with an existential crisis. In addition there are the big oil companies. The stupid idealist view is that tomorrow we all stop combusting fossil fuels and the evil oil and coal companies can promptly descend into hell where they can burn. But the idea of an "energy transition" is not that of a cold turkey break with addiction; it is a gradual weaning of dependency.

Big oil is waking up to the fact that the period of denial and suppression is over, and is developing strategies to adapt to a future reality at odds with its historical business model. And this shift need not be because they finally cave to the climate change lobby. It could very much be because they are watching developments in fusion energy and smelling a tipping point that could deliver commercialization by 2040. Fusion energy, because it does not include the hopelessly high radiation mitigation costs that doomed the post WW2 nuclear energy dream, will blow away not just fossil fuels like coal and natural gas, but also the solar and wind renewable energy sector. What will persist is an electricity grid and the capacity to use electricity to create alternative fuels like green hydrogen whose distribution can repurpose natural gas pipelines. It isn't just companies like Toyota sensing an existential threat and potentially making moves that shatter prevailing norms; big oil faces its own existential crisis but does have an intrinsic platform it can adapt to ensure its survival. Night Market Research is assuming that the only players to buy and develop major new lithium projects like PMET's Corvette are traditional mineral or metal producers. Once PMET has its Corvette resource on the map, assuming it meets expectations, a much broader range of interested buyers stands ready to pounce.

But that is me extrapolating about big picture forces that may not be ready to deploy themselves. The Night Market Research critique I most respect is one I made earlier this year, namely the structural instability that comes from PMET's origin as a horribly flaky Canadian junior. PMET has the problem that 24 million in the money warrants sit in the hands of parties who are likely not institutional shareholders. For whatever reason they have chosen not to exercise and collect their profits over the past couple years. If the potential future owners of PMET are truly disciplined, PMET will suffer from the market question "what now?" after the maiden resource is issued. NMR correctly puts its finger on opportunity cost. The market will not care if PMET trumpets that it will go on a drilling rampage along its 50 km land package to show that there are as many as a half dozen CV5 deposits present. With a $2 billion implied value already in place, what is left, another double after you spend another 2 years duplicating CV5? That is not how retail investors think. James Bay is not like the Ekati project within the Slave Craton during the 1990s where Chuck Fipke didn't quite get it all, but did get most of it. Replication of PMET's success within the James Bay region has a much greater probability than during the diamond hunt of the 1990s.

If the James Bay fire access restrictions ease and other juniors start finding LCT pegmatites, we will see PMET warrant holders exercise and exit PMET in order to redeploy the gains into new upside potential. This will create a tax hit in 2024 for them, which will create psychological incentive to engage in gambling on other much cheaper juniors, with potential horrific consequences in December when they dump the duds in order to collect the losses to offset the crystallized PMET gains. While that worry should deter, on the contrary, precisely because this negative outcome can be contemplated, profit soaked ex-PMET shareholders will be unable to resist rolling the dice again, this time without wondering about the legitimacy of Lithium Mania 2.0 or the strange ambitions of management such as merging with some private rare earth company. This time the story has solid legs.

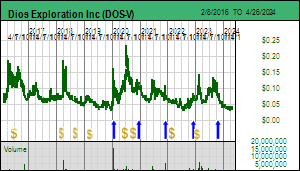

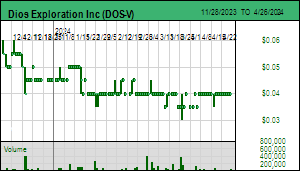

But what will be the driver that explodes the James Bay lithium junior space? This week Brunswick Exploration Inc announced that it has boots on the ground on the Mirage project where the goal is to find the bedrock source of a 1,700 m by 200 m field of spodumene bearing boulders. Should Brunswick report success in the next week or so, this junior with a tenth of the implied value of PMET will start to attract recycled PMET dollars. Within a few weeks Dios Exploration Inc which has a hundredth of the implied value of PMET will have boots on the ground checking out its second order precision targets. I have been following this junior's methodology closely, and I dare to say, its profound discovery potential value is not obvious from their news releases, their web site content, or their invisible corporate presentation. But Dios has significant individual shareholders whose holdings in PMET have a value bigger than the entire market capitalization of Dios. What happens if circumstances create a liquidity event that enables or forces them to exit the mother ship?

At the moment the James Bay lithium junior prices are tracking sideways. While the Canadian media is oblivious to Lithium Mania 2.0, along with both retail and institutional investors, the Australian equivalents, having experienced Lithium Mania 1.0, are completely plugged in. If PMET delivers a multi-grade cutoff set of resource estimates which allows everybody to claim to be a winner, be they bulls or bears, Australian capital could step up to absorb the paper from warrant exercise and sales by the earlier stage motley crew. This could jump start Lithium Mania 2.0 in the James Bay region in August after the juniors spent two months in the penalty box thanks to forest access bans created by Canada's pitiful firefighting capacity. I can't promise execution, but I can confidently point out the setup.

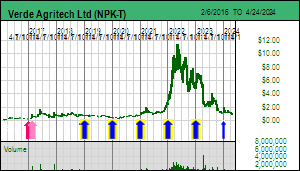

Last week Verde Agritech announced that it had received a study from Newcastle's Professor David Manning which confirmed that a tonne of K Forte was capturing 120 kg of CO2. This opened the potential for the sale of carbon credits linked to each tonne applied to a farmer's field. The company said it was still working on a life cycle analysis of the CO2 generated in mining, grinding, shipping and applying the K Forte so that we know how much net CO2 per tonne could be packaged as a carbon credit. I liked this strategy because if it is a meaningful amount, the company could offer a meaningful discount relative to potassium chloride which should motivate farmers to adopt K Forte as an alternative to KCl.

On July 27 Verde Agritech surprised us with a brief news release that it is in advanced negotiations to sell carbon credits to major international corporations that are established purchasers of permanent carbon offsets. That was a surprise to me because when I talked to Cris Veloso last week he suggested that the independent life cycle analysis by a Canadian consultancy was still 3-4 weeks down the road. How can you be in serious negotiations to sell a carbon credit when you don't know the net number? I guess the answer is that they already have a reliable internal net number and the independent verification is just a formality. The company did state that at its current production capacity, it could generate 300,000 tonnes of carbon credit annually. Since production capacity is 3,000,000 tpa which would pack away 360,000 tonnes of CO2 at Manning's rate of 120 kg/tonne K Forte, that means the carbon footprint is 20 kg per tonne of K Forte. So each tonne of K Forte generates 100 kg of saleable carbon credit. What is that worth? That depends on the quality of the carbon credit.

The press release included a link to a 58 page document produced by Microsoft called Criteria for High-Quality Carbon Dioxide Removal. This pdf document is worth reading because it describes the pros and cons of 8 key ways to remove CO2 from the atmosphere that do not involve capturing CO2 emissions at source. Microsoft has committed to becoming carbon negative by 2030, as opposed to carbon neutral, because it also has the goal of by 2050 to have captured and permanently stored all of its net CO2 emissions since Bill Gates and Paul Allen founded Microsoft on April 4, 1975. Microsoft works with Carbon Direct to establish carbon capture investments whose credits would offset Microsoft's emissions.

The sections relevant to Verde Agritech are pages 36-40 on Enhanced Rock Weathering in Croplands, and pages 41-45 on Carbon Mineralization. What is interesting is that ERW seems to involve dissolving CO2 in water with the help of silicates strewn onto fields which form a bicarbonate ion which supposedly ends up in the ocean which is the ultimate carbon sink. This represents a huge measurement problem and requires care not to add harmful elements to the field. Although NPK uses the term ERW, in this week's news it stated that the K Forte weathering permanently locks CO2 into a new mineral structure. That makes it the carbon mineralization type of capture similar to FPX Nickel's brucite strategy, except superior because it is also a fertilizer that provides non-salt related potassium.

Carbon credits are getting more and more media attention. Rio Tinto this week admitted that it would miss its 2025 carbon reduction goals and would as a "last resort" have to buy carbon credits. The Financial Times on July 27 had an article predicting that Brazil's Lula administration plans to launch an energy transition plan by September which will include trading carbon credits. Because Brazil generates 90% of its electricity from hydropower it wants to focus on renewable hydrogen technologies. Carbon credits related to shifting Brazilian potash consumption from 95% potassium chloride imports to a domestic source that does not harm the long term fertility of Brazil's farmland would seem to be low hanging fruit. Verde Agritech stated that it hopes to have its first carbon credit sale in Q3 of 2023. That may be too late to allow a discounted pricing strategy for 2023, but whatever sales news the company delivers for what will have been a difficult year in 2023 for the Brazilian farm sector, the market will have a basis for absorbing the 2023 results and then shifting its focus to a 2024 assisted by carbon credit sales.

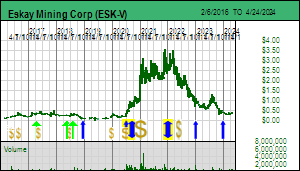

Eskay Mining had a difficult first half of 2023 amid uncertainty about its balance sheet and how it was going to fund a summer drill program. The stock traded as low as $0.50 on May 17 when CEO Mac Balkam put out a depressing news release about the need to conserve cash and plans to further develop targets at the 100% owned Eskay project in British Columbia's Golden Triangle. These plans included "potential drilling" which sent a signal to the market that this summer not much might change. This contrasted sharply with the big plans outlined in the January 2023 corporate presentation which, in addition to following up 2022 work in the Scarlet Ridge-Tarn Lake area with further drilling, would include "extensive drilling at SIB-Lulu" and "exploratory drilling at poorly-explored VMS targets property-wide". Oddly this presentation has not been updated on the company's web site.

The stock, however, began to perk up in June when Eskay Mining announced on June 7 that Seabridge had agreed to terminate the Coulter Creek Access Road agreement under which Eskay Mining was to contribute $6.25 million of the estimated $12.5 million cost. This deal in July 2021 seemed a bad idea at the time because Seabridge needed this road for its KSM copper-gold project which has been taken through feasibility while Eskay Mining was still a long way from a maiden resource estimate. It was as if the adjacent Hubris Peak had cast its shadow on Eskay management. Drilling during the past couple years on the TV and Jeff zones delivered lots of short high grade intervals but suffered from "structural complexities" which the company planned to think about in 2023 while trying to make a real Eskay Creek 2 discovery. By the start of 2023 Seabridge had loaned $2.7 million to Eskay Mining which was classified as a current liability. Since Seabridge was not going to focus in 2023 on the segment relevant to Eskay if and when a discovery with mining potential is ever made, Seabridge agreed to cancel the agreement which removed this amount from the current liabilities section of the balance sheet.

That was not good enough to help Eskay Mining raise any money to fund a serious drill program, but on July 10, 2023 Eskay Mining achieved a non-dilutive financing when it announced that Skeena Resources Ltd agreed to purchase 5 claims for $4 million of which $2 million was due immediately, $1 million on Oct 31, 2023 and the final $1 million on Dec 31, 2023. Skeena did not even put out a news release and Eskay Mining did not include a map with its press release, but disclosed that the claims were to the northwest of the main claim block. By comparing the map in the January 2023 presentation with the one included in the July 27 news release we can see that at least 4 claims were a floater block west of Skeena's property which was unlikely to yield a standalone discovery for Eskay Mining.

With the extra cash Eskay Mining announced on July 27 plans for 6,500 m of drilling 5 target areas missing from the January map. The immediate focus will be the Scarlet Knob-Tarn Lake area in the middle of which sits the Bruce Glacier target, and the new Storie Creek target to the west where the Eskay Creek Contact Mudstone has been found outcropping. The only older target to be drilled is TV South where one hole will be drilled in August south of where a gabbro dyke cuts off the TV zone. Two entirely new targets are Hexagon-Mercury northwest of the Jeff Zone and the Maroon Cliffs target in the northeastern corner of the property. These appear to be mainly geophysical targets. A surprise is the Cumberland target 6 km south of TV which was drilled a couple decades ago and which will receive two holes. My bet will be on the Storie Creek-Tarn-Lake-Bruce-Glacier-Scarlet-Knobb target group for which Eskay Mining provided a geological long section. I like Quinton Hennigh's declaration that "sharp-shooting multiple high-quality targets is the best approach to make one or more new discoveries in 2023". It gives me much greater hope for an Eskay Creek 2 score than a couple years spent swiss-cheesing the TV and Jeff Zones that emerged in 2020 when the company drilled areas that had previously delivered "smoke but no cigar" and ultimately only delivered ashes.

Eskay Mining Plans August 2023 after claim sale to Skeena

Disclosure: JK owns Brunswick Expl, Dios Expl and Verde Agritech; Brunswick is a Fair Spec Value rated Favorite, Verde Agritech is a Good Spec Value rated Favorite; Dios Expl and Eskay Mining are Bottom-Fish Spec Value rated

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch July 21, 2023: Capture Brazil potash market with carbon capture?

Jim (0:00:00): Why is Verde Agritech's carbon capture news potentially a big deal?

Verde Agritech Ltd announced on July 19, 2023 that an independent study by Newcastle University's David Manning, a soil scientist, has established that key products such as K Forte applied to fields in their current form naturally capture carbon dioxide at a rate of 120 kg CO2 per tonne of K Forte. That would mean K Forte at the current installed production capacity of 3,000,000 tpa would sequester 360,000 tonnes of CO2 annually while still delivering potassium and other nutrients to farm crops. If Verde Agritech achieved its production goal of 50 million tpa, which would replace about 50% of Brazil's potash consumption, 90% of which is imported as potassium chloride (KCl), a side effect would be sequestering 6 million tonnes of CO2 annually into an inert form similar to what FPX Nickel Corp hopes to achieve through ultramafic rocks rich with the magnesium mineral brucite. The next step is to establish the carbon footprint of K Forte through a "life cycle analysis" of CO2 generated by quarrying, grinding, shipping and applying K Forte, which is being done by an unnamed but "leading" Canadian consultancy firm. CEO Cristiano Veloso thinks the analysis could be ready within 3-4 weeks. The difference between the 120 kg of CO2 that K Forte sequesters and what it generates could be packaged into a marketable carbon credit sold internationally.

Verde Agritech has in the past mentioned "enhanced rock weathering" as an area of interest for its "greensand" product, a silicate called glauconite whose 6 billion tonne plus resource grades 8%-12% K2O. Similar glauconite deposits exist elsewhere in the world but their grade tends to range 3%-6% K2O, so to achieve the same potassium fertilizer effect a farmer would have to apply 2-3 times as much material as K Forte, which itself requires 5-6 times the volume as conventional potassium chloride. The fact that K Forte is currently ground into a powder form that has to be applied separately from other fertilizers such as nitrogen and phosphorous is an additional marketing obstacle. The farmers prefer to apply blended fertilizers which are supplied by blenders who insist on a granular form. Verde Agritech has indicated it is doing research on creating a granular form of K Forte which would open up the blenders as a distribution and marketing network. Veloso has told me that the granulated form would not change the CO2 sequestration rate because the granules would disintegrate once applied to the soil (granulation means binding the powder, not grinding to a coarser size).

The ERW news is timely because 2023 has been a rough year for the Brazilian farm community due to flat crop prices and higher interest rates, and that means it will be a disappointing year for NPK. We already know that revenues will be substantially lower than 2022 because the FOB Vancouver potash price had dropped to $328/t KCl at the end of June and NPK follows a KCl parity pricing strategy. The big question for NPK will be its ability to grow sales volume toward the 3 million tpa installed capacity. The TSX deadline for H1 financials with a December 31 yearend is August 14. Potash is the one key fertilizer farmers can leave out for a couple years, and in this regard Verde Agritech could have a difficult time growing sales in 2023, especially in a high interest rate environment where the K Forte producer cannot afford the credit terms demanded by farmers. The company does use modest discounts for volume and repeat business, but that is not enough to motivate farmers to try something new, especially when they are suffering financial distress.

The CO2 sequestration news is a big deal because it takes time to measure the sequestration process and until Professor Manning completed his study the ERW concept was just an idea. Additional verification studies will need to be done, but the next milestone is the K Forte carbon footprint data which is easier to collect. I suspect internally NPK already knows the numbers, which will be helped out by the fact that its electricity comes from hydropower. Once we know how much net CO2 a tonne of K Forte sequesters the company can start work on structuring a carbon credit linked to each tonne of K Forte sold. If Verde Agritech succeeds in creating a marketable carbon credit, it will have a killer market penetration strategy for Brazil that could eventually go far beyond supplying 5o% of Brazil's potash consumption.

The ERW news also explains the peculiar resolution NPK included in its AGM banning the sale of company products in 218 municipalities in 9 states covering 2,232,000 sq km. This area covers the northwestern part of Brazil where the Amazon is undergoing illegal deforestation to create land for farming and ranching. NPK's K Forte deposit is based in Minas Gerais and serves the southeastern part of Brazil where farming is concentrated. Because K Forte becomes less competitive with KCl the greater the distance it has to be transported, banning these distant states came across like pointless virtue signaling. But in light of the ERW news it is a preemptive move to guarantee that the carbon credits do not have a hidden carbon cost. The reason ERW could be a killer market penetration strategy is that carbon credits will be sold in a parallel market to international companies seeking to offset their carbon footprints, which would include technology giants such as Google, Microsoft and Meta. The farmers are unlikely to care about climate change and carbon footprints, but they are well versed in the language of money. Verde Agritech could use the carbon credit to sell K Forte at a substantial discount to KCl in K2O equivalence terms. Potassium chloride is a salt and has no CO2 sequestration potential so can never compete with a carbon credit linked pricing strategy.

Carbon capture, utilization and storage (CCUS) is being talked about ever more as a necessary part of the Net Zero Emissions goal for 2050. (Utilization is only a fraction of this concept - permanent sequestering is the main goal.) The Economist had an article on May 21, 2023 (Can carbon removal become a trillion-dollar business?) which discusses "direct air capture" as technology which sucks CO2 out of the air and injects into some sort of rock reservoir where it is permanently sequestered. The IEA's Energy Technology Perspectives 2023 report published in January has a section about CCUS which mainly deals with capturing carbon at source and transporting it by pipeline and/or ship to destinations suitable for storing the CO2 underground. The IEA says that worldwide CO2 capture is currently only 44 million tonnes but needs to expand 2,627% to 1.2 billion tonnes by 2030, and 14,000% to 6.2 billion tonnes by 2050.

Big oil, which has plenty of experience transporting CO2 for injection into oil fields for enhanced oil recovery, is getting interested in repurposing their pipelines, not just for hydrogen, but also CO2 captured at source such as natural gas powered electricity plants. Depleted oil fields could be turned into CO2 storage reservoirs. Direct air capture would require building a plant on top of the underground reservoir and suck the CO2 out of the air, which has CapEx costs and energy costs. The problem with this approach is that according to the Economist article it cost $600/tonne CO2 in 2011 compared to the EU emission-trading system where 1 tonne costs $100. Engineering has reduced the cost further, and CCS could become a reality if government policy lowers emission limits, forcing more CO2 emitters to buy carbon credits. What makes Verde Agritech's carbon credit proposal so interesting is that it is a form of direct air capture with no extra cost involved. And replacing potassium chloride with K Forte would preserve the fertility of Brazil's soil for generations.

Map showing Brazil states affected by NPK Sales Ban

Jim (0:12:21): Why do you think Toyota may be FPX Nickel's mystery investor?

FPX Nickel Corp surprised the market last November when it raised $12 million at $0.50 with a strategic investor which requested anonymity. This was at a premium to the market and did not include any warrants or flow-thru benefits. The investor ended up with 9.95% and the right to maintain 9.9% by participating in any future financings but no offtake rights of any nature. In May FPX raised $16 million from Outokumpu at $0.60, again at a premium to market with no warrants, but Outokumpu did secure the right to purchase up to 60,000 tonnes of nickel (7,500 tpa) at market prices. This offtake right was important to Outokumpu because it specializes in making low carbon footprint stainless steel; with Indonesia now producing more than 50% of global nickel supply with the help of coal-powered electricity clean nickel may become quite scarce in the future. Outokumpu also stayed at 9.9% with a two year standstill. The mystery investor elected to invest another $1.95 million at $0.60 to maintain its 9.95% interest. FPX shareholders are perplexed about the secrecy and from various comments CEO Martin Turenne has made we can pretty much rule out that the investor is a mining company, a high net worth individual, or a financial institution. This has led to speculation that it is a downstream nickel user such as a chemical company that makes battery precursor materials, a battery maker or even a car maker. However, such entities have made investments in resource projects and never had reason to keep such an investment secret, and investors generally shrugged at names like Tesla. When Martin insisted the market would be impressed by the identity and that I would then understand why the investor wanted to remain secret, that pretty much ruled out downstream fabricators.

I began to wonder if the investor might be a technology company like Apple or Google which is not yet in the carmaking business but is working on self-driving car technology. FPX Nickel has put a fair amount of effort into developing a flow-sheet to make nickel-sulphate for the battery market, even though it is not clear that this would add to profitability of mining Decar and would certainly add complexity. The mystery investor appeared interested in the nickel sulphate potential, especially from a secure jurisdiction and with a low or even zero net carbon footprint. Apple or Google, which might never commercialize self-driving cars, might be interested in supporting a project like Decar which would not come on stream until 2030 or later. When FPX Nickel formed an alliance in April with JOGMEC to explore for awaruite deposits elsewhere in the world I began to wonder if the mystery investor was a Japanese carmaker.

Toyota, the world's biggest carmaker, was not on my list of suspects because Toyota has resisted developing electric vehicles. Instead it has stuck with hybrids while it worked on a future generation of hydrogen fuel cell powered cars. That changed when in June Toyota announced that it hoped to be selling an electric vehicle as early as 2027 with a range of 1,200 km and a 10 minute charge time. Such a long range and short charging time would deal with the range anxiety North American drivers suffer and accelerate adoption of electric vehicles. A Financial Times July 6, 2023 article explained the basis for Toyota's boast, which was that Toyota has developed a lithium ion battery with a solid state electrolyte that allows lithium metal to substitute for graphite in the anode. Toyota apparently accomplished this not with a new configuration, but rather with a manufacturing breakthrough that reduces the cost of making a solid state electrolyte that avoids the dendrite growth problem which causes short circuits and thermal runaway. Chinese EV makers and Tesla are relying on lithium-iron-phosphate batteries for cars targeting the mass market. A LFP battery uses lithium, iron and phosphate in the cathode and graphite in the anode.

Toyota's solid state battery will initially be part of a higher end electric vehicle and, although the cathode material has not been disclosed, nickel is a prime candidate. If the cost breakthrough is of a manufacturing nature, it is conceivable that further cost reductions will emerge as the solid state batteries get commercialized, similar to what happened with solar panels which are a lot cheaper today and not because the price of raw materials has declined. By 2030 Toyota may be ready to turn its best-selling Corolla model into an affordable electric vehicle superior to the cheap LFP cars Ford, Tesla, Volkswagen and their Chinese competitors hope will coax North Americans into giving up their gasoline powered cars. Given that Toyota has lagged its competitors in designing and marketing electric vehicles, it is understandable that it would not want to tip its hand by disclosing it has bought 9.95% of a junior with a nickel project at the prefeasibility stage. Unlike the Chinese carmakers who hope to export their cars to American consumers, Toyota has a history of making its cars in the United States. If nickel is part of the cathode of its solid state lithium ion battery, it would make sense to support a project like Decar which promises to be a long lived nickel mine with a low carbon footprint and in a secure jurisdiction that qualifies for Inflation Reduction Act subsidies. If it turns out nickel is not part of the solid state battery cathode, then my guess that Toyota is the mystery investor is most likely wrong.

Jim (0:19:53): Any news on the James Bay forest access restrictions?

In last week's episode I was optimistic that forest access bans would be lifted for Quebec's James Bay region but the western half remained closed as did key transportation corridors such as the Trans Taiga Road. Projects such as PMET's Corvette and Brunswick's Mirage are outside the closed area, but getting boots onto the ground is a problem because helicopters are still under requisition to support the firefighters. CEO Marie-Josie Girard of Dios Exploration Inc tells me that while the East Clarkie and Nemiscau North projects are outside the access ban, they need helicopters because their second order sleuthing has developed precise targets. She has the contractor scheduled to start in mid August and believes there is plenty of time to make or break all the targets they have developed. I'm not sure they will be in a position to drill this fall but if they find any decent sized LCT-type pegmatites they could be drilling in Q1 of 2024.

Most of the projects of Brunswick Exploration Inc in the James Bay region are in closed areas, but the one that matters most, Mirage, is open. However, it is located 300 km from Nemiscau as the crow flies and the Trans Taiga remains closed. Mirage is only 100 km north of the Renard diamond mine so perhaps Brunswick can stage out of Renard to track down the bedrock source of its 1,700 m by 200 m spodumene bearing boulder field.

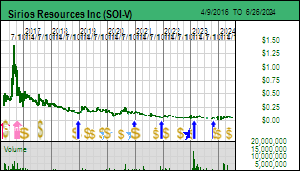

In the case of the Cheechoo project Sirios Resources Inc managed to extract its planned bulk sample for metallurgical testing, but the crew spent only 3 hours investigating the area up-ice from the gold deposit where a spodumene boulder was found when it was told to quit because of the fire bans. Sirios is stuck in a holding pattern with a persistent seller at $0.055 while it negotiates with Fury Gold Mines Ltd to acquire its 50.022% stake in the Eleonore South JV in which Newmont owns 49.978%. The problem with this situation is that Newmont has a right of first refusal if Fury and Sirios reach a deal. Most likely Fury will want a combination of cash and stock because the stock would allow Fury to participate in any upside once Sirios consolidates the entire area 100%. The most recent resource estimate gives Cheechoo 67.4 million tonnes indicated and inferred at 0.87 g/t gold (1.9 million ounces), but this estimate understates the reality because the pit shell can only be extended to the property line. This reduced intrusion related gold system has a potential resource in the 4-5 million ounce range, with at least 75% on the 100% owned Cheechoo property. With the whole being worth more than the sum of the parts, Fury would like stock, but if Newmont exercises its right of first refusal it would only pay the deemed cash value, denying Fury any future upside. Once Sirios owns 50.022% it would become operator, and it would make sense to approach Newmont with a deal to acquire its 49.978% stake, possibly for stock that takes its 12% Sirios equity stake up to 19.9%. As owner of the Eleonore underground mine it is the natural future purchaser of Cheechoo, assuming it does not sell Eleonore to a smaller producer.

There is also the bizarre potential that the northern half of the Cheechoo property which straddles the contact between the Opinaca and La Grande geological subprovinces hosts a decent sized pegmatite grading 1% Li2O or better which at $10/lb lb lithium carbonate would have a rock value of $545/tonne, equivalent to 8-9 g/t gold. In contrast the Cheechoo deposit has a rock value of only $55/tonne. The Eleonore South JV covers different geology and would not have LCT-type pegmatite potential. Sirios could split the pegmatite potential ground into a separate property and sell the consolidated Cheechoo gold project to Newmont.

Sirios did put out an update in early July about the Maskwa property which has been repurposed as a lithium play. Back in 2016 Sirios formed a 50:50 JV with Sphinx Resources called the Cheechoo-Eleonore Trend which was a conceptual play. They conducted till sampling which did not deliver much joy and in 2018 Sirios sold its 50% stake to Quebec Precious Metals Corp, a company related to Sphinx by way of Normand Champigny. Dominique Doucet revisited the area in 2020 with the idea that they should have been looking at the subprovince contact for intrusion related gold systems, which in this area was perpendicular to the Cheechoo-Eleonore "trend". Sirios conducted a till survey in 2020 seeking gold and tungsten grains whose 3 lines did yield gold and tungsten grains at the down ice limit of the property. Although the property does have anomalous lithium lake bottom sediment values these do not mean much because Maskwa was covered by the Tyrell Sea during a prior round of global warming. But tantalum is a heavy element (density 16.4 compared to 0.53 for lithium) it would have been recovered during heavy mineral screening (gold is 19.3). So they went back to samples and counted the tantalum grains which are anomalous. The only problem I have with the results is that all 3 lines perpendicular to the ice direction have similar elevated values, so no obvious vectoring. The source could be to the northeast on somebody else's property, or there could be several pegmatites near the subprovince contact. Maskwa is well inside the part of James Bay still closed to access, but for now Sirios is focused on trying to acquire the Newmont/Fury property next door to Cheechoo.

As an aside, I asked Dominque if Sirios still had the till sampling data from the 2000s when Sirios and Dios co-funded a regional survey with the gold targets going to Sirios and the diamond targets to Dios. That led to the Pontax lithium discovery now owned by Cygnus and Stria. He did, but only in paper form. The Cheechoo property offers first order pegmatite discovery potential because nobody ever looked hard at the lithium potential. Dios, in contrast has digitized its copy of the till survey data set and scrutinized it for clues to less obvious pegmatites, what I call second order exploration. Sirios would have have to walk the entire Maskwa and Cheechoo properties to find outcropping first order pegmatites. In contrast Dios has used multiple data sets including satellite imagery to pinpoint likely pegmatite locations. So even with a late boots on the ground start in August Dios could leapfrog other juniors who need to look at everything in order to find anything.

Maps of the Cheechoo gold project with LCT pegmatite potential

Yellow Gold Cheechoo Resource Estimate & White Gold Rock Value Matrix

Origin of the Maskwa Project repurposed as a liithium play

Comparison of Maskwa 2020 Till Survey Results

Disclosure: JK owns Brunswick, Dios, FPX Nickel and Verde Agritech; FPX Nickel and Verde Agritech are Good Spec Value rated Favorites, Brunswick is a Fair Spec Value rated Favorite; Dios and Sirios are Bottom-Fish Spec Value rated

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch July 14, 2023: Short Attack boosts PMET Credibility

Jim (0:00:00): What do you think of the short attack launched against Patriot Battery Metals?

On July 6, 2023 an outfit called Night Market Research that specializes in identifying short selling opportunities published a length report title: Patriot Battery Metals: Aggressive Vancouver Promotion with Multiple MRE Delays and Fake Buyout Rumors Running Headfirst into Wall of Risk (and Warrants). This caused the stock price to decline on July 7 and the ASX requested PMET to provide a response which the company did on Monday July 10 when it also published the final assays for the winter drill program. The ASX will allow a stock to be halted for a number of days while material news is disseminated, but the remaining assays are not material because they are all within the CV5 pegmatite body and do not really change the market's perception of the extent and grade of CV5 for which a resource estimate is anticipated in a "few weeks". The TSXV allowed the stock to trade on Monday while the ASX allowed trading to resume on July 11, enabling the Canadian market for the first time in a long time to set the tone for PMET. The stock recovered into the $15-$16 range as the market shrugged off the Night Market Research report's allegations which fall into two categories.

The first is that in fundamental terms the Corvette project is over-valued and is destined to correct downwards as the project proceeds into the feasibility demonstration stages of the 9 stage exploration-development cycle that starts with grassroots exploration and finishes with commercial production. In terms of my rational speculation model this is true, for the stock is in S-curve territory, the initial valuation surge of what is commonly called the Lassonde Curve, namely the discovery delineation stage where the sky is the limit as to how big the discovery can become until a maiden resource is delivered, after which the market sees the limits and focuses on cost discovery which forms the basis for a discounted cash flow model valuation expressed as a net present value (NPV) accompanied by an internal rate of return (IRR). (Nicholas LePan of the Visual Capitalist has done an excellent job Visualizing the Life Cycle of a Mineral Discovery.) I have observed that the peak valuation frequently matches that of what the project ends up being worth in DCF valuation model terms years later when the project is ready to go into production. The valley in between while the company engages in cost discovery after deposit discovery has been completed is called the "value trough" from the perspective of those who don't already own the stock. Whatever back of the napkin valuations are done during the transition usually shrink as flow-sheets and permitting requirements are sorted out. An additional source of outcome value shrinkage can be the future metal prices, though sometimes they end up higher, the perennial hope for gold projects.

An example of the Lassonde Curve in action is Dia Met Minerals whose Ekati diamond discovery reached a peak $2 billion valuation in 1993, two years after the initial discovery announcement. Three years after Ekati went into production in 1998 BHP acquired Dia Met and its 29% interest for cash at an implied value of $2.3 billion on a 100% basis. Why did Ekati hit a $2 billion value during the discovery stage before we had any numbers for tonnage, grade and carat value? Because this was a brand new diamondiferous kimberlite field outside of Africa where it was legitimate to dream that world class monsters like Jwaneng or Orapa in Botswana might emerge within the Slave Craton of Canada. This did not happen, but the collection of pipes selected for production did end up having a world class value.

Completely missing from the Night Market Research short attack is any discussion of the "district scale" implications of the Corvette property which covers 45 km of the La Grande Shear Structure of which the CV5 resource will represent only a portion. NMR is making the assumption that the CV5 maiden resource estimate will be the culmination of what the Corvette property has to offer, something which the Australian and Canadian brokerage analysts think will be comparable to what Liontown accomplished with Kathleen Valley, which earlier this year attracted a conditional bid from Albemarle that priced the project at about AUD $5 billion (see KW Episode Mar 29, 2023 for background on Liontown's 8 year journey from grassroots lithium exploration in 2015 to the current status of mine construction). Liontown rejected the conditional bid but the stock has since then consistently traded above the proposed Albemarle buyout price. NMR correctly points out that Liontown has pushed Kathleen Valley through 5 years of feasibility demonstration to get the current valuation, as a result of which it has 2.2 billion shares issued, but what it ignores is that Kathleen Valley is now an optimized mining scenario for that project. This project is as good as it is going to get.

PMET's situation at this stage is equivalent to owning the entire 40 km long Carlin Trend in Nevada, and CV5 is the equivalent of finding Goldstrike as the first Carlin-type gold discovery within this trend. And we know a lot more such gold deposits were subsequently found. How many more CV5 deposits might be found within the Corvette property that could be developed as standalone open-pit mines? Perhaps 3-5 more, perhaps none. The point is we don't know yet because the first order lithium discovery boom in the James Bay region is only 2 years old; all the other advanced lithium deposits (Galaxy-Cyr, Wabouchi, Moblan, Rose) were discovered decades ago and are valuable today only because of the climate change crisis and the electric vehicle as a partial solution to achieving the goal of net zero emissions by 2050. How many Kathleen Valley deposits are left for Liontown to find on its property? If there were any more would they not have been found during the past 5 years while the main pegmatite plodded through the feasibility demonstration stages? If the big producers knew that CV5 is all that will ever be found and developed within the Corvette property, there is no way they would consider paying $2-$3 billion to own PMET.

The IEA has projected that the world will need 600% more lithium supply if 2030 EV rollout goals are to be met. That is with existing lithium ion battery technology. Rio Tinto has made even more aggressive predictions. If the EV sales goals are met, the lithium market will be worth $100-$200 billion in 2030-2040 assuming current battery technology remains unchanged. During the past few weeks Toyota, which was in the vanguard with its Prius hybrid model but has been a laggard with full plug-in electric vehicles while it focused on leapfrogging lithium ion battery technology through hydrogen fuel cell technology, made the stunning announcement that it had solved the processing cost problem for a solid state electrolyte which allows lithium metal to substitute for graphite in the anode. Toyota predicts that by 2027 it will be selling a high end model that has a range of 1,200 km and a charge time of 10 minutes. Neither the IEA nor Rio Tinto forecasts allow for this greater usage of lithium in future electric vehicles.

Since you are probably not going to achieve the required lithium supply if the price of lithium crbonate tanks back below $5/lb, what we are facing is a massive scramble to find and harvest the low hanging LCT-pegmatite fruit that is suddenly in the money, and which faces a 5-10 times demand expansion. Australia has already been through this low hanging fruit cycle which I call Lithium Mania 1.0; the second phase targeting stable regions such as Brazil and Canada is Lithium Mania 2.0 for which PMET is the poster child. Rio Tinto has said the world needs 60 Jadar scale lithium mines; the James Bay region has the capacity to deliver a couple dozen Jadar equivalent mines.

The timing of this report just ahead of PMET's plan to publish a maiden resource estimate appears designed to force a stock price retreat if the resource proves lower than the lofty conceptual estimates published by various Australian and Canadian brokerage firms. I have speculated the resource will come out within the range of 50-100 million tonnes grading between 1%-2% Li2O, but Night Market Research has presented a range of estimates from 90-160 million tonnes with grades ranging 1.12%-1.35% Li2O. It offers its own prediction of 73 million tonnes of 1.28%, whose grade is near the upper range of the analyst predictions, though its tonnage is lower than the 90 million tonnes at 1.35% Li2O it attributes to National Bank. NMR claims that PMET CEO Blair Way has been encouraging the market to think in terms of at least 100 million tonnes, which has supposedly set up the market for disappointment. NMR is predicting that the CV5 resource will be similar to the 68.5 million tonnes of 1.34% Li2O proven and probable reserve Liontown is putting into production.

The reality is that we do not know what cutoff grade PMET plans to use. If it uses a higher grade cutoff the tonnage will be lower but the grade higher. Initial development could focus on the higher grade Nova zone within the CV5 deposit. NMR has in fact created a straw man to knock down the market if we see a resource closer to its number. The reason it thinks the analysts are over-estimating the resource is that PMET stopped publishing sections along with its holes last year. However, PMET has an excel spreadsheet with all the drill hole data which includes the azimuth direction and dip angle for each hole, plus all mineralized intervals greater than 2 metres. Combine that with the drill plan and an analyst can construct a 3D model, especially if they have Leapfrog software at their disposal. What the company has not published is the assay interval breakdown which would allow analysts more granularity in defining the geometry of their choice using their own cutoff grades. NMR argues that the implied project value of about CAD $2 billion on a fully diluted basis is excessive if the estimate is more in line with its own prediction, but it does not provide a quantitative basis for this view which requires one to visualize an operating mine and calculate a net present value from the resulting cash flow.

Once we have a 43-101 resource estimate the market will be in a position to create an outcome visualization in the form of a DCF model which depletes the resource within 15 years. For example, NMR's resource would be mined at about 13,000 tpd to be depleted within 15 years. The economic value of that scenario will depend on CapEx and OpEx as well as the long term price of lithium carbonate. Suppose the DCF model does generate a future target outcome of CAD $5 billion. Under my rational speculation model fair speculative value should be 2.5%-5.0% for a project that has delivered a resource estimate but not yet done cost discovery in the form of a PEA. So we are talking a fair value range of $2.50-$5.00, well below the current valuation. However, if the project moves to PFS stage the FSV should be 50%-75% of the target outcome, which would be $25-$38 per share. What NMR is arguing is that the current valuation is an S-Curve peak which will follow the Lassonde Curve downwards once the project enters feasibility demonstration stage and follows into the value trough.

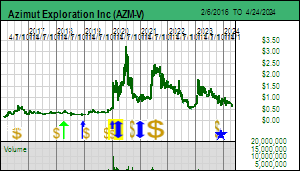

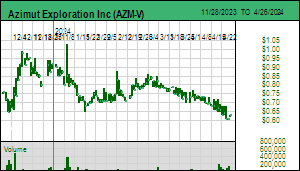

This can be expected to happen if PMET stays in charge of moving the project through the feasibility demonstration stages, but a likelier outcome is that a major producer will buy out PMET and do it properly. The most obvious candidate is Rio Tinto which has been optioning nearby properties from Azimut and Midland in what amounts to an effort to tie up as much of a new district as possible. NMR seems to be trying to talk down the price of PMET in order to help a third party get a better deal. But this may not work because we are talking about an emerging world class lithium district serving a market that by 2030 will be worth $100-$200 billion, more if Rio Tinto's own predictions are to be believed, and even bigger if Toyota is not bullshitting us. CV5 represents only a fraction of an LCT-pegmatite mineralized trend. There may be multiple CV5 deposits present, each of which could be developed as a standalone mine. It is conceivable that Rio Tinto, Albemarle or Pilbara Minerals would be willing to pay an S-curve valuation based on the strategic district value. Far from making a case that PMET's stock price will be a lot lower once the maiden resource estimate is published, Nigh Market Research has in fact boosted the credibility of PMET's discovery.

NMR's other angle of attack is to slag the history of Patriot Battery Metals, such as the sordid 18 month marketing deal PMET did at USD $500,000 per 6 month term with some obscure entity based in an ordinary Vancouver residential neighborhood. This deal was made just before the company announced an RTO of a private rare earth company that was canceled a couple months later when Blair Way became CEO and steered PMET back to the Corvette lithium project. I abhor these awful and expensive marketing deals Canadian juniors do to pump their stock, and sometimes I wonder if these deals are just ways for hidden insiders to steal their private placement money back into their pockets. In the ASX requested response to the short attack Blair Way stated the marketing deal was terminated after 6 months when PMET had a market capitalization of only $20 million, a hundredth of what it is today. Regardless how sleazy the marketing deals a junior may have done, none of that matters if the company has delivered a fundamental success. One thing I keep repeating is that the nature of Lithium Mania 2.0 is such that even juniors with horrible management practices can achieve a huge fundamental success, provided they spend money on competent exploration. Whatever questionable marketing deals PMET management has done, it did let Darren Smith's competent exploration team do their stuff.

NMR also tries to scare PMET shareholders by pointing out that Ken Brinsden, who played a key role in the success of Pilbara Minerals during Lithium Mania 1.0, was previously involved with an iron company that failed. Who cares? That is like arguing that Robert Friedland's Mongolian Turquoise Hills copper-gold discovery in Ivanhoe One, after he delivered a $4 billion buyout for the Voisey's Bay nickel-copper discovery by Diamond Fields, is doomed to fail because Friedland's earlier company, Galactic, crashed and burned. Not every Friedland effort is a winner (Kaizen and Cordoba come to mind), but Ivanhoe Two's Kamoa-Kakula grassroots copper discovery in the DRC is a monumental fundamental success. This complaint is the most feeble one NMR makes.

NMR does make a valid point when it frets that PMET has a large overhang of unexercised warrants that are very much in the money. Many of the holders will already have dumped the long positions from those private placements done in 2021 and are sitting on huge paper profits. Frankly I do not understand why so many cheap warrants remain unexercised. I pointed out this problem in KW Episode March 17, 2023 and it is still a problem. NMR's main strategy is to prime the market for a sell-off after the maiden resource estimate is released by predicting it will be lower than analysts are projecting. During the past year there have been several rumors about possible takeover bids for PMET, none of which are credible because no producer is going to pay a "strategic" premium without at least a resource estimate in view to explain its reasoning. The market risk is that even if the resource estimate come in within the analyst predicted range, there may not be a quick follow through. The attitude of the warrant holders is that they will exercise when they have to, such as in the event of a takeover bid. But if that does not promptly happen because Pilbara, Mineral Resources, Albemarle and Rio Tinto are all disciplined and reluctant to start a bidding war, the stock could stall. At Friday's $15.70 closing price the 24,330,190 warrants that expire between December 21, 2023 to March 21, 2025 have an implicit profit of $365 million, which to collect would require $382 million worth of buying at $15.70. Psychologically this type of warrant based paper profit is more unstable than if the holders exercised them a long time ago without selling any. NMR is in effect reminding all the warrant holders of their prisoner's dilemma situation and setting up a selling cascade after the resource estimate is released. The potential bidders for PMET are right now chortling with glee at the predicament of the warrant holders.

NMR also worries about the permitting regime in Quebec which is fairly detailed and could benefit from streamlining. It also mentions a lake sturgeon that supposedly lives in the lake which would be disrupted by open-pit mining CV5. The Canadian and Quebec governments are going to have to do a cost-benefit analysis. Billions are being shoveled at downstream fabricators serving the EV market to encourage them to set up their operations in Canada. One reason to do so is they can all see the potential lithium supply coming from Canadian pegmatites. But if the government is going to take a purist stance that there must never be a local loser, at the expense of net zero emission goals, there is a surprise coming. This year is shaping up to deliver a new round of extreme weather records, as Quebec's forest fire debacle has already shown. It is time to become pragmatic about all aspects of the various climate change mitigation solutions, in particular the discovery and mining of critical minerals.

NMR also invokes Goldman Sachs which has been predicting that Chinese and Latin American lithium supply will meet all demand growth, and mentions a GS prediction of $34,000/tonne for lithium carbonate in 2024. That is equivalent to $15.42/lb. If lithium carbonate is at that level rather than $10/lb as I assume, what is there to worry about? In fact $10/lb will be hugely profitable for pegmatites grading 1% Li2O or better. Demand will probably grew faster than supply, which NMR dwells on but treats it as a negative for PMET along the lines of "your project will take a lot longer to permit than anybody else's project, so by the time you are producing the market will be in oversupply and the lithium carbonate price will be a lot lower". Understanding the discovery exploration game is not something Goldman Sachs has much experience with because it is such a small space; its revenue generating strategy will involve helping downstream raw material consumers secure their supply. So of course GS is trying to talk down the prices of the lithium developers. And Night Market Research appears to have volunteered itself as foot soldier in this process. But in fact it has helped fulfill the requirement that no major new discovery is real until it has attracted a major short attack.

Where NMR thinks PMET sits in the Lassonde Curve, its own resource estimate prediction, and the Warrant Time Bomb

Dia Met's Ekati as an illustration of the Lassonde Curve

Liontown's Kathleen Valley reserve and price chart

Lithium Carbonate Price Chart and Price-Grade Rock Value Matrix

Jim (0:16:52): What do you think of the farmout deal Azimut did with Rio Tinto?

Azimut Exploration Inc announced a farmout deal on July 10, 2023 that has very positive implications for the James Bay region, though perhaps less for Azimut despite it being a stronger deal than the one Rio Tinto did with Midland Exploration Inc in mid June. Rio Tinto can earn up to 70% in the Corvet and Kaanaayaa properties by spending $114 million split between the properties over 9 years. The first stage requires Rio Tinto to spend $7 million on each property over 4 years to earn 50%, of which the first year is a firm commitment of $1.5 million for each property which Azimut gets to operate. In addition Rio Tinto must pay $850,000 per property, of which $250,000 is up front and $150,000 on each anniversary of the initial term. On this basis alone the farmout deal is much stronger than the one Midland secured from Rio Tinto on June 13, 2023.

Under Midland's deal Rio Tinto can earn up to 70% in 10 James Bay properties by spending $64.5 million over 10 years, with $14.5 million over the first 5 years to earn 50%. Unlike the Azimut deal where the amounts are split between the 2 properties, allowing Rio Tinto to spend only half the total if it drops one of the properties, the Midland deal appears to allow Rio Tinto to vest in all the properties regardless on which one it spends the money. Midland gets $500,000 up front and $100,000 on each anniversary of the five year 50% vesting term. The first 18 month expenditure is a firm $2 million but Rio Tinto is the operator and as such has complete control over where the money gets spent. In this deal Midland CEO Gino Roger handed off the lithium potential of its James Bay properties to Rio Tinto to figure out so it can concentrate on its other Quebec prospects.

Although similar in terms of spending requirements and vesting timelines, there is a dramatic difference that makes the Azimut deal superior and which undermines Rio Tinto CEO Jacob Stausholm's bluster that valuations of major LCT pegmatites (ie Patriot Battery Metals) are too expensive. Azimut's CEO Jean-Marc Lulin was able to secure an option where once Rio Tinto has vested for 70% in either property Azimut, instead of becoming a 30% joint venture partner at the mercy of Rio Tinto's cash calls, can elect to reduce to a 25% interest carried through production in the form of a loan from Rio Tinto that is repayable from 50% of Azimut's 25% share of cash flow. If Rio Tinto makes a major discovery on either Corvet or Kaanaayaa and quickly blows through $57 million on either property, Azimut can avoid the risk of death by cash call funding dilution. This is a part of the value trough within the Lassonde Curve that is deadly to juniors who must fund all or part of the boring feasibility demonstration stages. Midland did not get this option, perhaps because CEO Gino Roger did not ask for it. No doubt Lulin studied the Midland deal and the market's less than enthusiastic reaction to it, which allowed him to push for a stronger deal. What is surprising is that Rio Tinto capitulated to this demand.

However, neither deal is truly strong and both are strategic blunders created by an obsession with the prospect-generator-farmout model and what appears to be a dismissive attitude about Lithium Mania 2.0. Rio Tinto is doing its best to lock up title to claims near PMET's Corvette project for which we should get a maiden resource estimate by the end of July. Midland already blundered on November 10, 2022 when it optioned 85% of the "critical mineral (lithium)" rights to the Mythril property adjoining to the north of Corvette to Bob Wares' Brunswick Exploration Inc for $700,000 and $3.5 million exploration over 5 years. If there is any lithium pegmatite potential on Mythril, Brunswick will find out within 2 years and reap all of the speculative upside because the market does not care about the residual 15% contributing interest Midland will end up with.

Neither of Azimut's farmed out properties directly adjoins Corvette, so they represent potential for a parallel trend to the south, similar to the Champion Electric trend to the north owned 100% by Champion Electric Metals Inc. One hopes that by now Champion's CEO John Buick sees the wisdom of rebuffing similar farm-in overtures by Rio Tinto. So far Rio Tinto does not have any exposure to the La Grande Shear Structure trend which PMET's Corvette property straddles for 45 km, which continues another 15 km westward through the Pikwa property owned 50:50 by Azimut and Soquem, and another 30 km through the Cancet property of Winsome Resources Ltd, and then bends northwest into Brunswick's 90% optioned Plex property which straddles another 40 km of the prospective trend.

Why is Rio Tinto doing these apparently strong deals with Azimut and Midland? In the case of Midland only one property, Mythril East is near the Corvette trend; the rest are scattered throughout the James Bay region, with Galinee near Winsome's Adina discovery and the Komo property west of Allkem's Galaxy-Cyr project the most interesting in terms of standalone discovery potential. Rio Tinto was unable to secure the Galinee project of Azimut because it is already a 50:50 JV with Soquem. While it looks like Azimut got the better deal out of Rio Tinto than Midland, the opposite is actually the case. It will not take much exploration work to kill the low hanging fruit LCT pegmatite potential of Azimut's Corvet and Kaanaayaa blocks. Within two years after spending $3 million Rio Tinto can drop these properties knowing that they are not part of emerging world class lithium district. Its willingness to meet Jean-Marc Lulin's demands is really just a shoulder shrug for Rio Tinto, whose real target is PMET despite its professed aversion to high early stage valuations.

Whereas Rio Tinto is letting Azimut do the first pass lithium exploration, it is doing its own work on the Midland properties because some may have real but not obvious potential for major LCT-pegmatites. I am frustrated that Midland chose not to spend its own money on first pass boots on the ground exploration, but the company is busy with its many other Quebec projects and does not appear to believe Lithium Mania 2.0 is real. I don't think Azimut believes Lithium Mania 2.0 is real either; the James Bay map JML included with the news release is speckled with red dots representing claims targeting nickel which is where JML thinks the James Bay future lies, and perhaps the Patwon pencil deposit at Elmer into which Azimut has sunk $25 million without yet delivering a maiden resource estimate. In fact at the Metals Investor Forum in Vancouver in January 2023 JML spent 30 seconds on his lithium slide and at least 60 seconds on his nickel slide. It will be interesting to see how much the Azimut-Soquem JV gets done on Pikwa and Galinee this summer, the two most promising LCT-pegmatite properties accidentally in Azimut's James Bay portfolio. The real importance of the Midland and Azimut deals by Rio Tinto is that if PMET becomes the target for a hostile takeover bid, and the army of timid Canadian investors sitting on the sidelines swarms into the market as FOMO takes hold of the James Bay Great Canadian Area Play, they will be targeting those juniors who retain 100% of their holdings and have meaningful exploration strategies underway.

Regional Map of James Bay showing Azimut's Nickel and Lithium Postage Stamps

Map showing location of Midland's James Bay Properties

Azimut spending $3 million on peripheral plays but how much on Pikwa, the one that counts?

Pikwa is where Azimut's boots should be pounding the ground in 2023!

Jim (0:25:56): What did the market like about Brunswick's latest news?

Brunswick Exploration Inc announced on July 13, 2023 that it had identified multiple spodumene bearing dykes on its 90% optioned Anatacau Main project east of Allkem's Galaxy-Cyr project where Brunswick's Anatacau West property hosts the eastern extension of the Galaxy-Cyr system at least 300 metres onto Brunswick's property. The northern part of the Anatacau property hosts the continuation of the Galaxy-Cyr structure 22 km to the east, and Brunswick managed to have boots on the ground for 5 days in late May before sending the team off to the Mirage property where it spent a day outlining a spodumene enriched pegmatite boulder field about 200 m wide and with a 1,700 m strike perpendicular to the ice direction. Brunswick would have spent more time at Mirage to track down the bedrock source but on June 6 the Quebec government issued a forest access ban due to the fires in southern Quebec whose threat to infrastructure and communities forced the requisitioning of all helicopters to support firefighters.

The James Bay region is still subject to forest access bans, but these are expected to be lifted soon as heavy rains make their way across Quebec. Southern Quebec has in fact shifted to flood warnings as severe thunderstorms pummeled the Montreal-Ottawa areas and spawned tornadoes. The government has been letting fires in the James Bay region burn because they are not near infrastructure and the setting of height-challenged spruce tree stands separated by lakes and swamps makes wildfire spread in this region a much smaller threat than in the incendiary south. Resource juniors are lacing up their boots in anticipation of a green light next week.

The market reacted strongly to the news, bidding the stock as high as $0.82 on just over 1 million shares of trading after touching $0.68 on July 12 when the Red Cloud unit financing done at $0.85 in March came free trading. The stock had stalled as the market waited for a surge of clip and flip selling from Canadians no longer gripped by fear of missing out on Lithium Mania 2.0. But it was not obvious what the market was so excited about. The news was that prospecting had identified a cluster of parallel pegmatite dykes within which the largest was one that outcropped for 100 metres and at surface was 15 metres wide. Brunswick took 19 grab samples which assayed 1.2%-3.8% Li2O, generally above 2%. The Main dyke has light grey spodumene crystals up to 20 cm long and so these values are not representative but do confirm this is an LCT-pegmatite. The company did not disclose this outcrop earlier because it is small, similar to the Decoy outcrop at the Hearst property in Ontario where the absence of an update from a 1,000 m drilling program that began April 24 hints at disappointment. Brunswick wanted assay confirmation for the Anais showing before announcing it.

As Brunswick makes clear, its exploration strategy is one of search and destroy; if a property survives the first pass boots on the ground, it is followed by drill to kill, a massive process of elimination strategy. With properties in Saskatchewan, Manitoba, Ontario, Quebec and Atlantic Canada the junior's hope is that a discovery will emerge sooner than later. The forest fire ban has sabotaged this goal as far as its James Bay properties are concerned, for these have the highest potential to deliver a discovery comparable to PMET's CV5 pegmatite on its Corvette property.