Hello Guest User, You are visiting this website from a computer with an IP address of 172.70.127.129 with the name of '?' since Sat Apr 27, 2024 at 5:13:12 PM PT for approx. 0 minutes now.

Kaiser Media Watch Blog - September 1, 2023 to September 30, 2023

KRO Blog Overview

The KRO Blog is where unrestricted content of a time sensitive nature is posted. It includes the Kaiser Media Watch Blog which features content involving John Kaiser produced by third parties such as the Discovery Watch series by HoweStreet.com, interviews by outfits such as Investing News Network, SDLRC related commentary, the KRO Monthly Summaries, and just about anything else John writes that is not intended exclusively for the fee based KRO Membership.

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kauser Watch September 20, 2023: Rio Tinto success at Midland's Galinee

Jim (0:00:00): What do you plan to talk about at this weekend's Metals Investor Forum in Vancouver?

This KW Episode was recorded September 20, 2023 and was supposed to be posted ahead of the September 22-23, 2023 Metals Investor Forum in Vancouver but travel complications got in the way. I have consequently converted the written portion into a summary of the conference. Compared to the January MIF when a much larger speaker hall had only a few empty chairs and some of the audience was standing, turnout was considerably lower, though better than I had expected given the pall that has settled onto the junior resource sector. The speaker hall was typically two-thirds full. One thing that struck me as odd was the relative absence of industry people not involved with the presenting companies who usually remain in the exhibit area while investors flock to the talks. The videos of the presentations, panel discussions and backstage interviews are starting to show up on the MIF YouTube Channel.

I only had time to see Joe Mazumdar's presentation, Into Thin Air - Oxygen Required to Support Junior Companies which, as suggested by the title, dealt with the difficult financing environment for resource juniors. Joe tends to be more focused on juniors with advanced projects which are still able to do bought deals placed with institutional investors (these tend to be free trading right away), though almost always at a steep discount to prior trading levels to which the stock almost never recovers. As I watched his parade of charts, most of which had a closing price below the recent financing price like the stock was heading off a cliff, it struck me the message Joe was offering is that the better the junior, the more ordinary investors should avoid them in this market.

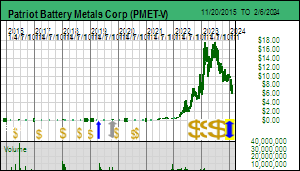

The difficult financing environment became clear to me when I processed the private placement data the TSXV publishes in its monthly review. Since 2009 I have had the ability to separate the resource listings from the rest. The resource listing only chart shows strong financing periods occurring in mid-2009 to 2012, 2016-2018, and mid-2020 until mid 2023. July's resource sector private placement activity of CAD $119 million was the lowest since April 2020 when the market was reeling from the eruption of the Covid pandemic. But I was shocked by August's surge to $328 million until I drilled into the data and realized that $109 million represented the financing Albemarle did in Patriot Battery Metals after it published its CV5 maiden resource estimate in Quebec's James Bay region, and $86 million was raised by NGX Minerals Ltd for its Los Helados and Lunahuasi copper-gold projects in Chile. Subtract these two financings linked to very strong exploration results and the total was $133 million, slightly better than July's total. But when you take away the $33 million raised by Jervois Global (623 million at $0.053 - Australian money) and $21.5 million by Electra Battery Materials, both of which are cobalt refinery stories, the total was only $79 million spread among only 45 TSXV resource listings. This is bad and I will be curious to see how September fared, usually a stronger "back to work" financing window.

I recently updated the financial status of the 1,160 TSXV resource listings which brings them up to date to the end of June 30 and the outlook is very dismal. There are 714 juniors (62%) with positive working capital totaling $4.5 billion while 446 (38%) have negative working capital totaling $3.2 billion. Of those with positive working capital about $2 billion is parked in juniors trading below $0.30. Next month I begin research for my 2024 Bottom-Fish Collection. The KRO Search Engine that is part of the annual USD $450 membership will save me a lot of effort. The only positive news from my TSXV financing charts is that TSXV resource listing traded value, which was substantially less than non-resource listing value from 2013-2021 except for that crazy gold window in H2 of 2020, has been higher than non-resource listing traded value since 2022. The numbers are in fact worse for the non-resource listings because these are artificially boosted by a few oddball listings like Topicus.com which are established foreign companies that don't belong on a venture exchange.

My September 23, 2023 MIF presentation, Exploring for Yellow and White Gold (PDF version of Powerpoint), continued the theme I kicked off at the January MIF, namely that the dominant big picture trends shaping the resource junior future are the geopolitical conflict between Global West and East and the energy transition. In the September talk I focused on gold and lithium to emphasize the entirely different narratives behind these two metals. The basic argument for gold is that a higher real price will emerge as the Global East works to reduce its reliance on the US dollar to settle international trade. A recent theme has been the emergence of a premium for Chinese domestic gold above the international price caused by a Chinese gold import ban to stop the outflow of US dollars. The optics of a domestic gold premium, however, is an affront to Xi Jinping's message that everything is wonderful in his autocratic China. He can censor just about everything else but not the fact that gold costs Chinese citizens more to buy than anybody else in the world and that isn't stopping them. The import ban has been lifted but the curious fact remains that China has not banned the purchase of gold by its citizens.

Gold seems stuck in the $1,800-$2,000 range, unable to convert $2,000 from a ceiling into a base for further gains. That is a problem because $400 gold in 1980 inflation adjusted to the present is $1,489, which means that at the current price gold has achieved a real price gain of only 29% during a period when mining doubled the above ground gold stock by harvesting all the low hanging fruit created by the gold's price move during the 1970s after it was liberated from its $35 per ounce prison. A common refrain these days is one of puzzlement, "why does the market not care that gold is at current levels?"

To explain this conundrum I created a gold rock value matrix where I show the in situ rock value for different combinations of grade and gold price. I then colored each cell in the matrix red where the rock value is too low even for open pit mining, yellow where only open pit mining is possible, and green where underground mining is also possible. I enclosed in a red box the rock values possible at the various gold grades between $1,800-$2,000 gold, and in a blue box between $2,000-$3,000. You have to look very hard to see the value difference a move by the gold price into the $2,000-$3,000 range makes. And yet, every time gold makes a surge toward the $2,000, and sometimes, as has happened twice now since 2020, breaches $2,000, risk capital flows into the resource juniors, whether or not their flagship project is focused on gold. The $2,000 gold price ceiling has become an optical obstacle for the resource juniors. If gold can definitively pass $2,000 so that $2,000 becomes the base, it would unleash a bull market for resource juniors, even though in value terms it would not make a huge difference.

The hesitation I have about this hope for gold establishing a new $2,000-$3,000 price range is that I am not sure what will cause such a move, and worry it will be something so catastrophic for investors in the Global West that there will be zero risk appetite for exploration and development resource juniors. During the May 2023 MIF I introduced West Vault Mining Inc as a leveraged proxy for a real price move beyond $2,000. West Vault is a Good Speculative Value rated KRO Favorite on the premise that a strong upward move in gold will not be of "end of the world as we know it" nature. In the September 2023 MIF I pivoted to the opposite end of the spectrum by introducing Silver Range Resources Ltd, a traditional prospect-generator-farmout junior focused on high grade gold-silver epithermal and carbonate replacement prospects in southwestern United States. The strategy here is that if we are stuck with $1,800-$2,000 gold as a tradeoff for geopolitical conflict not escalating into catastrophic territory, then we should be placing bets on juniors positioned to make high grade gold-silver discoveries in secure jurisdictions.

CEO Mike Power did an excellent job with his Silver Range Presentation, which included a simple slide explaining what sort of prospects he is seeking. Nevada has seen a lot of exploration for epithermal deposits in the nearly two centuries since Comstock was discovered, so the chance of face-planting into a mineralized outcrop is pretty much zero. However, after my June site visit to Nevada, described in KW Episode - Tonopah Adventure Tour Part I and KW Episode - Tonopah Adventure Tour Part II, I am convinced Nevada will undergo a revival of interest in high grade epithermal plays.

Mike presented 4 target scenarios: 1) another Comstock sticking out of the ground, 2) a tiny or weakly mineralized outcrop, 3) no outcrop but alteration at surface hinting at a hydrothermal system, and, 4) deep conceptual targets. Silver Range is only interested in the second type because these can be identified through archival research and prospecting in the field that looks for old workings where previous operators gave up. This is a tip of the iceberg exploration strategy where the focus is not so much the mineralized outcrop but what Silver Range can learn about the strength of the underlying system based on the geochemical nature of the alteration at surface. This involves new field instruments and deposit models not available to the prospectors of yore. It involves a lot of field work and geological knowledge, and it is not the sort of strategy a life-style junior can pursue. Because Silver Range is seeking to make discoveries grading 5 g/t gold equivalent or higher, all of which will likely have to be underground mined, a higher gold price is irrelevant to the success of this junior. It's all about applied method. On the other hand, the optics of gold trading in the $2,000-$3,000 range would stimulate strong farm-in interest, with Silver Range able to get increasingly stronger terms. So indirectly the success of Silver Range, thanks to the work it is doing now in Nevada, Arizona and soon also Utah, is positively leveraged to an upside move in the price of gold.

Silver Range Resources Ltd is Bottom-Fish Spec Value rated because it does not have a strong treasury, but that is something which could change when one of the private companies to which it vended property goes public. In the main presentation Mike Power mentioned that one of them has a pricing which implies a $19 million value for the 10% equity stake Silver Range acquired when it contributed its namesake Silver Range (Keg) project in Yukon's Faro silver-lead-zinc district to Broden Mining Ltd. He goes into greater detail in the Backstage Interview. If Broden goes public in 2024 as an advanced junior, Silver Range may be able to monetize its equity stake by selling it to an institution. Such a non-dilutive "financing" via an asset to which the market currently assigns zero value would be transformative for this junior.

With regard to the energy transition I focused on lithium, a white gold contrast to yellow gold because speculation about lithium plays has nothing to do with expectations for a higher lithium price. During 2022 the price of lithium carbonate was stuck in the obscenely elevated range of $30-$35/lb, a far cry from the price below $3/lb during the 2018-2020 lithium winter caused by the extremely successful mobilization of lithium supply by Australian companies during Lithium Mania 1.0 in 2015-1017 from Australia's strong endowment of LCT-type pegmatites. Below $3/lb the EV sector will never reach the car sales required for the 2050 net zero emission goal unless meanwhile there is a miraculous breakthrough in the cost and efficiency of direct lithium extraction (DLE) technology or a better and cheaper battery than lithium ion emerges. The lithium winter slowed supply development which resulted in a reversal of the imbalance in 2021 as EV sales took off, especially in China which has a non-climate change related strategic reason to shift transportation away from oil to electricity. The elevated spot prices of 2022 are not sustainable over the long run because at that price far more claystone and pegmatite lithium is in the money than the world will ever need. During 2023 the price of lithium carbonate has plunged into the $10-$20/lb range where it has gyrated and is currently threatening to drop through $10/lb, creating fear of another lithium winter.

The resource junior audience, trained by decades of obsessing about the need for a higher gold price, does not like the optics of a crashing metal price, so Lithium Mania 2.0 has been slow to get rolling. However, I like the lithium sector because I do expect the price of lithium carbonate long term to settle into the $5-$10/lb range, though during the rest of the decade we may see periodic surges back to the $30/lb level. But because lithium carbonate or hydroxide is sold under long term contracts, such spot price spikes will do little for the bottom line. I have done to my lithium rock value matrix the same as I did to the gold rock value matrix; colored red those grade-price cells where for hardrock deposits (claystone and pegmatite) production will never be profitable, yellow those where only open pit mining is possible, and green those where underground mining is feasible (note that the grade is lithium oxide - Li2O - claystone resources are usually reported as elemental lithium which you must multiply by 2.153 to get lithium oxide equivalent). I've also boxed in blue the $10-$20/lb price range prevailing this year and in red the $5-$10/lb price range I think will be the long term reality. Assuming your target is a 1% plus Li2O grade, the shift to the lower price range does not change the underground mineability of a pegmatite. Yes, the after-tax net present value will be lower, but most pegmatites that will be discovered will be outcropping or near surface and be at least partly open-pittable. What the general investing public not based in Australia does not quite yet understand is that exploration for LCT-type pegmatites in jurisdictions like Canada and Brazil has barely begun and there is an awful lot of low hanging fruit available for harvesting.

In my presentation I contrasted Silver Range Resources Ltd with Dios Exploration Inc which had indicated in Q2 that it would be ready to participate in the September 2023 Metals Investor Forum. I liked the contrast because both juniors are engaged in science based target generation. Many of the members of the James Bay Lithium Index are there simply because they owned land in the region for its gold and base metals potential whose prospective rocks happen to overlap with LCT-type pegmatite potential. Quite a few members own land optioned from armchair speculators who map-staked claims based on closeology and not so much on relevant geology or meaningful interpretation of lake bottom sediment data. But with the James Bay district only very recently being recognized for its world class LCT-type pegmatite potential, and with historical exploration laser-focused on gold and base metal related geology, which does not have a perfect overlap with LCT-type geology, the dumbest, most horrible resource junior could make a billion dollar discovery so long as it retains a competent exploration team and puts boots on the ground.

A small group of companies which includes Brunswick Exploration Inc and Dios started acquiring land in 2022 based exclusively on LCT-type pegmatite potential. In the case of Brunswick Bob Wares' team conducted archival research for documented pegmatite showings and analyzed commercial satellite imagery to stake land in James Bay where a pegmatite of some nature was outcropping. This is first order exploration because once boots land on a pegmatite the use of a handheld XRF or LIPS reader will quickly establish if the pegmatite is LCT-type. If spodumene crystals are present a visual assessment of the distribution within the pegmatite can give a rough idea of grade potential. Another type of first order exploration is being done by juniors like Champion Electric Metals Inc which have acquired large land positions covering rocks that have seen comparatively less field exploration because they are not as prospective for precious or base metals as trends like PMET's Corvette trend. The archives would have a much lower frequency of references to mapped pegmatite outcrops, which means grid-based prospecting will need to be done that could result in the discovery of a major LCT-type pegmatite peeking out from under the moss.

Dios did not start taking the LCT-type pegmatite potential of its James Bay backyard seriously until last September, so it was late to the game. But the tools it brought to the game included a detailed knowledge of the region's glacial history learned during its decades of till sampling activity, initially for diamond indicator minerals and later for precious and base metal indicators. Coupled with internal proprietary till sample data, Dios went after second order targets by analyzing lake bottom sediment chemistry in the context of glacial transport and relevant geology, leading it to areas where commercial satellite imagery revealed outcropping pegmatite and in some cases, even documented pegmatite when you dug deep enough into the archives. This science based approach to generating targets is similar to what Silver Range is doing in southwestern United States. The result is a collection of second order exploration generated claim blocks in the middle of nowhere within the James Bay region. The reason I am keen about this junior whose marketing budget in H1 of 2023 was only big enough to buy a bottle of two buck chuck is that its type of prospect could contain low hanging fruit nobody has ever seen because there wasn't a precious or base metals reason to walk the ground.

Unfortunately the forest fire closure of the James Bay region that began at the end of May robbed the industry of 3 critical summer months for boots on the ground prospecting. Dios thus declined to participate in my MIF session because it realized it needed to get as much done in September-October as possible to put it in a position to drill meaningful LCT-type pegmatite outcrops in Q1 of 2023. Many juniors will not get sufficient work done in the remainder of the prospecting season to have a good story to tell at the end of 2023, some because logistics has become scarce, some because their claims are in areas impacted by the September 15-October 15 moose hunting season, and some because James Bay may get an early winter onset. Once the ground is blanketed with snow, if you do not have a clearly outlined drill target, there will be nothing more to do until June of 2024.

This frustration may, however, be a blessing in disguise. During the May 2023 MIF conference I moderated a Panel Discussion. The bad fire closure news was still around the corner and I was pretty pumped about Lithium Mania 2.0 exploding during the summer, but dismayed that my peers were uniformly negative about lithium plays. Some of this negativity was due to being a Trumper stuck dismissing anything to do with climate change mitigation. Some of it was due to skepticism that EV adoption would ever go beyond society's economic elite. But most of it, I suspect, was due to a sense that they had missed the boat.

However, the bleak overall resource sector market decline after Q1, the forest fire closure of James Bay, and the nasty bungee plunge undertaken by lithium carbonate delayed lift-off, stranding most boats at the dock. At the same time since that May MIF panel discussion PMET delivered a world class resource at CV5, Allkem upgraded Galaxy-Cyr to world class status confirming the widespread nature of the lithium pegmatite endowment of the James Bay region, Albemarle came back to Liontown with a AUD $6 billion bid for Kathleen Valley accepted by management but subject to due diligence, and Toyota stunned the world with a boast that it had figured out how to cost effectively make a solid state lithium ion battery that is safe, the holy grail of the industry because it would allow lithium metal to substitute for graphite in the anode.

Toyota, which has sat out the EV boom by focusing on selling hybrids and working on hydrogen fuel cell technology, arguing that current battery technology is not good enough to scale to the sort of mass adoption required by net zero emission goals (one of the May panel's reasons for rejecting the EV story), claims it will be able to sell a high end model by 2027 which will get a range of 1,200 km on a 10 minute charge. But most important of all, it claims that it achieved this with a breakthrough in manufacturing cost which previously had made a conceptually viable solid state battery configuration prohibitively expensive to build. The reason lithium metal cannot be used in the anode with the conventional fluid electrolyte between the cathode and anode is that the ion flow causes lithium dendrites to grow. If these puncture the electrolyte wrapper the short will cause thermal runaway and turn the car into a fire bomb. So graphite became the compromise anode and remains the anode even for the lithium iron phosphate (LFP) batteries with which cheaper EV models are equipped but which come with the range and charging limitations that make a cheap EV of little appeal to consumers accustomed to refueling their ICE cars at a nearby gas station within 10 minutes. The beauty about a manufacturing breakthrough is that over time Toyota will make the process more efficient, just as happened with solar panels during the past decade. Thus by 2030 it is possible that Toyota relaunches its popular Camry and Corolla models as affordable EVs with a better range than the ICE versions and the same refueling time. Toyota, which was threatened with marginalization by its non-EV strategy, has positioned itself to become a Tesla killer.

Rio Tinto in 2021 predicted that the world will need 60 Jadar equivalent mines by 2035 if the EV contribution to the 2050 net zero emission goals is to become reality. This prediction was premised on the assumption that a solid state lithium ion battery will never become reality. But if what Toyota claims is true, the amount of lithium used in a battery will more than double, so the world will need at least 120 Jadars by 2035. And a Jadar is roughly equivalent to a Kathleen Valley or CV5 pegmatite deposit. And how did lithium stock prices respond amidst all this good news? They generally went down.

The Canadian attitude toward lithium, however, is changing. First, I was surprised to see Targa Exploration Corp be part of the September MIF show, one of Gwen Preston's picks. Targa has assembled lithium pegmatite plays in Saskatchewan, Manitoba, Ontario and Quebec. Among its first acquisitions was the Opinaca project it acquired from Zach Flood's Kenorland Minerals Ltd in late 2022 for stock and a 3% NSR. Kenorland is a Fair Spec Value rated KRO Favorite based on its status as a prospect-generator which develops large conceptual plays and farms them out to both majors and juniors. The Opinaca project is in the James Bay region in the middle of nowhere. Why? Because back in 2021 Kenorland looked at the James Bay region for its lithium potential, well before Brunswick's Bob Wares started looking, and conducted its own till sampling program in an effort to tighten the source of the lake bottom sediment anomalies visible in the government data set. The brains behind this strategy was Francis Macdonald who has since left to head Li-FT Power Ltd after it acquired 3 James Bay lithium prospects from Kenorland. Li-FT used the James Bay prospects to expand its market cap so that it could acquire a collection of known LCT-type pegmatites in the Northwest Territories east of Yellowknife which is now its primary focus. Kenorland in turn has managed to sell the Li-FT stock for about $14 million in proceeds. It holds a 9.9% stake in Targa which only recently finally put boots onto the Opinaca ground. This is a second order type of target similar to those Dios has generated, so it is entirely possible that overnight Targa becomes a discovery sensation.

Not only was I pleased to see a James Bay lithium junior at September MIF recommended by a newsletter peer, but I also observed a dramatic attitude change in the two panel discussions I was part of. On Saturday September 22 Joe Mazumdar moderated the Day 1 Panel Discussion: Making Money in the Current Resource Equity Markets. Whereas at January MIF neither he in his presentation nor Jean-Marc Lulin of his pick Azimut Exploration Inc could barely bring themselves to utter the word "lithium", on Saturday he was very much on top of the evolving lithium space and enthusiastic about the potential. On Sunday September 23 Gwen Preston moderated the Day 2 Panel Discussion: What Caused Excitement this Summer? And What's Next?. Again there was a brand new openness to the idea that a lithium exploration boom was a distinct possibility.

Yes, most people including me missed the PMET boat, and yes, the Brunswick boat I recommended in June 2022 at Toronto MIF has gone up five-fold since then, but most juniors, including those with projects in the James Bay region, have barely moved on the upside since getting into the pegmatite lithium sector. Meanwhile Brunswick's boots on the ground have established a substantial corridor of spodumene enriched pegmatite outcrops at the Mirage project which the market is pricing at just under $200 million, a tenth of the valuation of PMET at the price where Albemarle bought a 4.9% equity stake for $109 million after the CV5 resource estimate was released. Most investors do not understand that the EV future will not happen unless lithium grows into a $200 billion annual market by 2035. They do not understand that a lower lithium price is not a bad thing for the market because it ensures that only the better grade and size discoveries will undergo a rocket launch toward a $2 billion valuation. They do not understand that the future pegmatite lithium sourced supply hinges on the exploration efforts of juniors in jurisdictions like Canada and Brazil. But the pool of those who do is starting to expand beyond Australians, and the most important takeaway from the September 2023 Metals Investor Forum is that my peers are starting to understand and research their own favorites. Lithium Mania 2.0 may start lifting off in Q4 of 2023, but it will definitely be exploding on the upside in 2024 as it gains eyeball critical mass. The 2023 forest fire closures, bad as it was for James Bay juniors, has bought everybody else time to get positioned.

Two Global Crises as Key Drivers for Resource Juniors

TSXV Financing Activity 2009-2023: Resource and Non-Resource

TSXV Resource Sector Fianncing 2009-2023 by Financing Type

TSXV Resource Junior Working Capital Distribution

TSXV Positive & Negative Working Capital Distirbution by Stock Price Range

Comparing the Long Term Gold Price Trend to its Inflation Adjusted Price

Gold Grade vs Price Rock Value Matrix

Lithium Price vs Grade Rock Value Matrix

If Toyota's solid state Li ion battery is real there world will need 150 Jadars by 2035

China's embrace of Electric Vehicles is Irreversible

Silver Range and Dios have similar second order prospect generation strategies

Jim (0:08:29): Is the James Bay Lithium Index waking up yet?

The James Bay Lithium Index is still weakening as the price of lithium carbonate approaches $10/lb on the downside. As of September 26, 2023 it was down 14.1% from the August 1, 2023 initialization date. The optics of a declining metal price never makes the market happy, but as I argued in the MIF overview portion of this KW Episode the long term price range will be $5-$10/lb within which pegmatite deposits grading 1% Li2O or better still have rock values that allow profitable underground mining and where open pit mining is possible that brings tears of envy to gold explorer. There is also the index downward bias created by my decision to include all companies which have land in the James Bay region on the premise that the novelty of the pegmatite hunt makes it possible for even the dumbest, most horrible lifestyle juniors to get lucky so long as they mobilize a prospecting program run by a competent exploration team. JBLI is now colliding with the reality that the loss of three months of critical boots on the ground prospecting will limit the number of juniors that have drill ready targets for Q1 of 2024. This causes the penny dreadful members who were added to the index with the same value weighting as all the rest to register big percentage drops. But there is some discovery joy trickling through despite the curtailed season that will focus new money coming into the James Bay Great Canadian Area Play. The value of the JBLI is that it creates a monitoring framework and will reveal a rising tide when that begins to happen, possibly late 2023 but definitely in 2024.

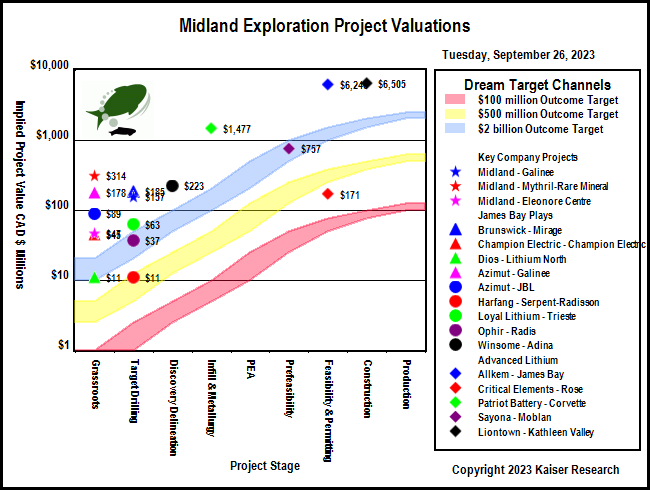

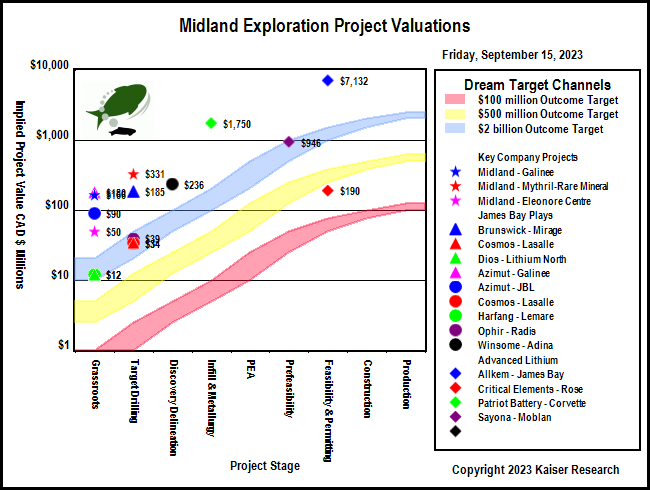

The most important development during the past week was news from Midland Exploration Ltd that Rio Tinto has discovered spodumene bearing pegmatite outcrop on the Galinee project optioned 70% from Midland. In KW Episode September 15, 2023 I made the case that Midland is so far the best way to bet on Rio Tinto's exploration efforts in the James Bay region and is also the best way for nervous speculators to have exposure to James Bay lithium discovery upside without the downside risk. This is due to the fact that Midland is a Quebec focused prospect-generator-farmout junior with numerous projects, some farmed out to majors, in other parts of Quebec such as the Abitibi and northern Quebec. In addition not all its James Bay projects have been farmed out to Brunswick or Rio Tinto and the junior is now reviewing them for their LCT-type pegmatite potential. Gino Roger may have let a good number of Midland's James Bay boats slip out to sea, but he is taking a hard look at those still moored at the dock. Needless to say, because Midland's net 30% stake in Galinee already implies a valuation of about $161 million, the market did not reward the stock with upside. That will happen when drilling reveals the scale and geometry of the Galinee discovery, and it is noteworthy that operator Rio Tinto is planning a 2023 fall drilling program.

Midland only revealed that outcropping spodumene bearing pegmatite had been identified along several hundred metres, with no indication of the lateral distribution of these outcrops. In contrast consider that Brunswick has now identified pegmatite outcrops within a corridor of 2,700 m by 850 m, and a solo outcrop 6 km to the northeast from the southwestern end of the outcrop corridor where a 3 km boulder train begins. Brunswick started a 5,000 m drill program on September 7 and will be in a position to tell us by mid October to what extent the Mirage outcrops hang together beneath the surface.

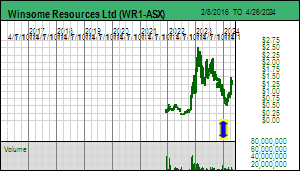

So, given the so far relatively puny outcrop area at Galinee, why is Rio Tinto already planning a drill program? The Galinee area is emerging as a focal district within James Bay created by the Adina discovery in late 2022 by Winsome Resources Ltd. The Adina LCT-type pegmatites are associated with the contact zone between the easterly trending amphibolite Trieste Formation and felsic intrusives to the north. Winsome has now traced LCT-type pegmatite along a 3.1 km trend with the best drill results at the Jamar showing whose pegmatite body dips to the southeast onto the Galinee 50:50 JV between Azimut Exploration Inc and SOQUEM.

Azimut recently reported that its boots on the ground had found spodumene bearing boulders on its side of the boundary from Winsome's Jamar Zone, but so far failed to find any outcrop on the rest of the property. The ice direction indicates that these boulders came from the Jamar Zone and Azimut's hope is that there is a meaningful downdip extension onto its property and possibly blind parallel bodies as it has hypothesized in a diagram. However, the combination of the lake bottom sediment lithium map and geology on Azimut's Galinee project suggests that if anything outcropping is present it will be in the southern part of the property where a narrower amphibolite trend is present.

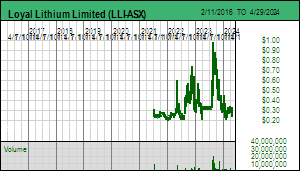

The forest fire access closure has been particularly harmful for Winsome which planned a major discovery delineation drilling program this summer to stitch together the pegmatite zones at Adina, but this program was only recently able to get underway. Winsome's Adina project is carrying an implied value of AUD $223 million, another example of an emerging discovery in the James Bay region that could deliver 5-10 fold gains from current levels if drilling can deliver a deposit resembling PMET's CV5. Rio Tinto is being aggressive about Midland's Galinee because it sits between Winsome's Adina and the Trieste project of Loyal Lithium Inc which has discovered LCT-type pegmatite on the southern flank of the amphibolite trend. Loyal has an option to acquire most of its Trieste project from Osisko Development Corp whose Sean Roosen is apparently planning to spin out the remaining James Bay holdings into a new vehicle. Comet Lithium Corp's Liberty property to the north has a small segment of this trend between Adina and Galinee, but this junior has so far demonstrated itself as management challeneged.

I've patched together several maps to try and make it easier to understand who has what land where; the various companies tend not to outline and identify their neighbors unless they have a discovery worth pointing out, so we are stuck with a fragmented perspective of relative land positions. The reason I think Rio Tinto is being aggressive about Galinee is that it sees the potential to consolidate this district which doesn't really have a name so I will call it the Trieste Trend.

Not every junior is reporting spodumene-bearing pegmatite outcrop news. Champion Electric Metals Inc has assembled a large 53,000 ha land package it calls Champion Electric that parallels to the north the amphibolite trend of PMET's Corvette trend. This belt of rocks has seen less historical exploration from the likes of Virginia so will lack archival references to pegmatites observed while exploring for precious and base metal deposits. But because there is no genetic relationship between LCT-type pegmatite emplacement and the formation of precious and base metal deposits, Champion's land position has the potential to deliver first order surprises when prospected on a detailed grid.

During 2022 Champion completed a LIDAR survey over those portions mapped as "mafic volcanic rocks" (hard to tell what Champion means because its map assigns the same color to the amphibolite rocks of the Corvette Trend to the south while the dark green color it calls amphibolite are patches to the north of its land package). LIDAR surveys reveal topographical variation which is useful for homing in on ridges that may represent pegmatites whose harder rock than the country rock causes them to resist weathering and grinding away by ice sheets to a higher degree than the surrounding rock. (Geologists are now scratching their heads why the CV5 deposit of PMET recessively tracks a long lake.) Andre Gaumond during the Virginia exploration era famously forbade his field crews from sampling light colored bush and mosquito free ridges because those were worthless pegmatites with zero precious and base metal potential.

Champion announced on August 3 that it had sent boots onto the ground to prospect the areas of the 2022 LIDAR survey. The next update came on September 19 when CEO John Buick revealed that Champion had completed a LIDAR survey on the rest of the property and would soon be sending prospecting crews into the field. Given that a 7 week prospecting window had just passed, it was shocking not to hear an update about what was or wasn't found. Given the company spent $324,000 on investor relations during H1 of 2023, you would think that if there was anything positive to report, Champion would have done so. The glum conclusion is that the first boots on the ground pass turned up nothing interesting and the race is now on to prospect the rest of the property before snow blankets the region. Champion should still have about $5 million working capital left, so if it can generate targets worth drilling in Q1 of 2024 it will not have to go to the market. The main obstacle to upside is that Champion has an overhang of 54,536,266 warrants exercisable at $0.10-$0.25 which boost its fully diluted to 323 million shares and which implies a lofty valuation of $45 million for a project which so far has no evidence of LCT-type pegmatites.

James Bay Lithium Index Daily Performance Last 120 Days

Lithium Rock Value Matrix and LC Price Chart

Various Maps of Trieste Trend where Winsome's Adina Discovery is located

Winsome's Adina Discovery and Azimut's Geochem Map

Azimut's hopes for its Galinee Project

Lidar & geology Maps for Champion's Champion Electric Project

Vhampeion Electric Financial Snapshots

Midland IPV Chart

Disclosure: JK owns shares of Brunswick and Dios; Crtical Elements is a Fair Spec Value rated Favorite; Dios, Midland and Silver Range are Bottom-Fish Spec Value rated; Champion & Targa are not rated

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

The James Bay Lithium Index had a downward bias this past week until the last couple days when it perked up, though it is still down 6.2% from its initiation date August 1, 2023. During the past week I found four more ASX listed juniors with exposure to the James Bay region and have added them as members, bringing the total to 62 members of which 50 are Canadian listed and 12 are ASX listed juniors. One recent new ASX listing had the chutzpah to name itself James Bay Minerals Ltd! I've included a list below. If anybody is aware of Canadian or Australian companies missing from the list, please send me an email at [email protected].

The price of lithium carbonate weakened slightly but the second plunge following the May rebound seems to be slowing, though with regard to the James Bay Great Canadian Area Play where the goal is large deposits of 1% Li2O or higher we should not worry about lithium carbonate price fluctuations so long as it does not drop below $5/lb such as what ushered in the lithium winter for Australian lithium pegmatite plays in 2018-2020. Even at $5/lb the rock value of 1% Li2O is $273 per tonne, equivalent to 4 g/t gold and 3% copper at current gold and copper prices. The goal in the James Bay region is to find 50 million tonne plus deposits grading 1% Li2O or higher, of which two world class deposits have already been delineated, Allkem's Galaxy-Cyr within its James Bay project and Patriot Battery Metals' CV5 within its Corvette project. If you are having trouble convincing others about the merits of the lithium boom, show them my Lithium Rock Value Matrix and ask them where any junior is going to find a large open-pittable gold deposit grading 4-8 g/t gold.

The price of gold, which seems determined to keep $2,000 as its ceiling, continues to torture resource junior investors who are gold bugs and spend most of their energy wailing about how the price of gold needs to be a lot higher. We don't need a higher lithium price because the story is all about the extraordinary demand growth that lithium is undergoing as a result of the energy transition and the fact that the car sector is shifting its production lines away from ICE to EV cars regardless of energy transition policies. Russia and Saudi Arabia, in their effort to get Trump elected in 2024, are helping out by curtailing oil supply so that ICE car drivers pay through the nose for gasoline.

If lithium ion batteries continue to power the EV sector, the world will need a six-fold supply expansion by 2030, 12-fold by 2035 if Toyota's boast of a solid state lithium ion battery which uses lithium metal in the anode instead of graphite becomes commercial reality. (Fans of FPX Nickel Corp should check out this Electrek September 14, 2023 article by Peter Johnson which confirms that the cathode of Toyota's solid state battery will need lots of nickel.) Quebec's James Bay region may rival Western Australia in terms of LCT-type pegmatite endowment. And that is a good thing, because Australia can't do this on its own, which is why Australian investors and companies are swarming into Canada's James Bay region, for they understand that the Lithium Mania 1.0 that profited them handsomely is about to repeat as Lithium Mania 2.0. To appreciate why Canadians are generally asleep at the switch I recommend viewing the MIF Vancouver May 2023 Panel Discussion. But as I tried to emphasize last week, there is no shame in waking up today, because only a few boats have put out to sea, and most are still idling at the dock or puttering in the harbor. There is so much latent opportunity!

Uranium is starting to create some joy for uranium bugs; its spot price at $66.25/lb U3O8 is now at the highest level since 2011. The Russia backed coup in Niger, which supplies 4.1% of the world's uranium, seems to be the tipping point, though apparently, according to a Financial Times LEX blurb, Russia has figured out how to constrain Kazakhstan's ability to supply the world from its seemingly unlimited in situ leachable deposits. But at the $49.70/lb average price for 2022 the value of 2022 production was only $6.3 billion compared to $49.2 billion for 2022 lithium supply at the average $32.26/lb price. Very little U3O8 or lithium carbonate gets sold at their spot price because producers deliver into long term contracts. But when you compare the supply evolution charts for uranium and lithium, and realize that consumer demand is driving lithium demand while regulatory red tape stymies the growth of nuclear power capacity and accompanying uranium demand, the real game is all about finding LCT-type pegmatites big and rich to be put into fast-track production. I urge investors to consider, what if the passion that invigorates the uranium juniors discovers the Canadian pegmatite lithium sector? There is one James Lithium Index member which has its feet in both the uranium and lithium worlds, some of the latter in the James Bay region joint ventured with an ASX listed company. It trades at $0.02-$0.03 and has 342 million fully diluted which will shrink if management has the fortitude to resist the plea of warrant holders to extend their free lunch another couple years. (Yeah, there is a reason why $450 for a KRO membership might be worth the money.) For uranium bugs this junior is a free lithium lunch.

The big story this week was the European Union decision to initiate a probe into whether or not Chinese EV makers benefit from unfair state subsidies. European makers of solar panels are now going bankrupt after a 2018 decision to remove tariffs from imported Chinese solar panels in order to drive the cost down and encourage installation of solar polar as part of the energy transition agenda. Europe's car industry, however, is much more important to Europe's economy than solar panel makers. While China heavily subsidized its EV sector so that it can escape its oil import dependency, the Europeans, operating in the world of laissez faire capitalism, have been much slower to develop their EV divisions. No European in their right mind would ever want to buy an imported low quality Chinese ICE car, but in adapting to the brand new EV technology the Chinese car makers like BYD underwent a quality revolution. These Chinese cars are good and well suited for Europe's small spaces, not so much for America's wide open spaces.

Xi Jinping's mishandling of the covid pandemic as a demonstration of autocracy's superiority over democracy along with other oppressive measures have pushed Chinese consumers into a funk. The result is EV over-capacity and, of course, China wants to sell the surplus to the rest of the world. If the Europeans impose heavy tariffs to offset Chinese subsidies to its industry, which include environmental rules that are not enforced so that powerless downstream victims eat the cost for the greater good of China, something not possible in the Global West, they may discover a new problem, which is that although China is not a major lithium producer, it is the dominant processor of lithium concentrates and producer of lithium ion battery precursor chemicals. Supply chain ignorance (indifference as in the geopolitically blind mantra of globalized free trade supposedly dominated by shareholder serving corporations?) is the fatal flaw of the Global West. Trump sounded the alarm during his administration, and Biden, acting on behalf of America, took the torch and has run with it to foster the KAG goal of Keeping American Great. This, however, is a problem for Europe, for IRA is designed to serve American interests, not those of Europe, and it has lots of subsidies available to American companies and friends of America.

This is where Canada should end up playing a critical role, not just as a producer of lithium concentrates from the James Bay region and perhaps other parts of Canada, but as a downstream processor of lithium concentrates and perhaps even battery plants. And also with regard to lots of other useful metals such as niobium, nickel, rare earths and copper to name the more familiar ones. Canada's environmental rules are second to none, and enforcement is not a farce like in China. When a mine is going to be profitable after complying with Canada's permitting system, nothing should stop it from happening.

This is Canada's opportunity to shine. Now is the time for Prime Minister Justin Trudeau to stop cruising in social justice cul de sacs and start making it clear that local stakeholders such as First Nations and foolish young people who don't understand geopolitics and where physical things they take for granted come from will not prevent Canada from becoming a critical minerals powerhouse for the Global West, and in doing so provide an economic foundation that sustains what it means to be a Canadian. It is time for Canada to cease being the perpetual also ran. And one way to do so is to abandon the aspiration to ethical purity, and accept that, when a decision to "make it so" is made, there will be losers and acknowledge such. No decision that is good comes without some degree of shame, for the core principles humanity takes for granted are an inconsistent set, something Nietzsche made a lot of hay out of, and which underpins his definition of tragedy. The path to redemption beckons Justin Trudeau, but it requires him to become a tragic figure.

This weekend while reading reviews about the new movie "Dumb Money", it occurred to me that all these young people in 2021 buying a junk company like Gamestop, only to eventually get blown up either by Gamestop returning to fair value before they sold or recycling their profits into some other junk company that repeated the Gamestop cycle, could make a lot of money by getting their heads around the James Bay Great Canadian Area Play, most of whose junior participants are still very cheap. By swarming into the James Bay Great Canadian Area Play they would also help shape the future in terms that benefit them and their children.

This is not a fraud fantasy like cannabis or blockchain, frauds because cannabis production and supply has no competitive barriers and will become a low margin business, and because blockchain applied as crypto currency is a solution in search of a problem. Climate change is a pressing problem. Reliance on Global East titans China and Russia for key raw materials is a pressing problem. Young people are ill-equipped to solve most other of humanity's existential problems, but as a collective they are well equipped to deliver partial solutions to these two problems by backing resource juniors focused on lithium and other critical minerals. Let the not so dumb money discover the James Bay Lithium Index as a leveraged way to change the world.

September 15 is the start of the moose hunting season in the James Bay region which ends October 15. This is not when planeloads of camouflage dressed white people descend upon the region to bag their trophy whose meat will be donated to local homeless shelters. Moose hunting is for First Nations members only. In KW Episode September 1, 2023 I talked about how Q2 Metals Corp and Ophir Gold Corp were scrambling to get as much prospecting work done as possible on their respective Mia and Radis properties straddling the Yasinski greenstone belt where they have confirmed outcropping LCT-type pegmatites before the start of moose hunting season. Not everybody, however, is affected by this month long moose hunting closure.

September 15 to October 15 is open season in the James Bay region for members of First Nations to hunt moose. I don't know if there are any kill limits, but there are practical limits as to how many moose one can kill, dress, and store in freezer. None of this activity is characterized as "sportsmanship", the white person hunter-gatherer fantasy of the individual using his or her wits to stalk and bag a wild animal not necessary for the hunter's survival. I have heard stories about wonton slaughter for the sake bloodthirsty satisfaction, but that is third rail territory I prefer to avoid. My interest is in how resource juniors can work around moose hunting season, and I have heard from a number of juniors, unlike Q2 Metals and Ophir Gold, that their boots on the ground prospecting is not affected. It boils down to the location of your properties.

The biggest concern from First Nations is helicopter noise frightening the moose away. There are three ways to hunt moose: 1) drive along the roads until you see a moose and blast it, as that pair does in the Koneline segment I highlighted in the first segment of KW Episode September 1, 2023 (I do urge everybody to watch this Koneline clip so that, when you are stuck arguing with somebody braying about how wonderful indigenous rituals are, you can show them an example and ask what they think), 2) use boats on rivers and lakes to scan the shoreline for moose they can blast with high powered rifles, 3) set up a camp in accessible (aka near a road) "favorite" locations they know moose like to frequent and wait for them to show up so that they can blast them from the comfort of their camp. I am not very keen about stalking moose from a truck or boat, but I do sympathize with the camp strategy because 1) it reflects strategic prior observation and planning, 2) the waiting by the group creates an opportunity for reflection that makes this non-stalking form of the hunt rather spiritual, and, 3) you only kill what comes to you (which is probably not a lot of moose), and, when you are done, it is time to go home so your freezer is stocked with fresh frozen meat. The camping group, understandably is most worried about noise from helicopters passing over their camps and frightening away moose that might finally be approaching their hangout.

Companies that have historically worked in James Bay have established relationships with the communities in the vicinity of their properties and consult the locals about where they do not want helicopter traffic that might spook their quarry. It's not like there is a total ban on helicopter usage, but there is a standing request that helicopters choose routes that do not impact moose hunting. That means Sept 15-Oct 15 is bad news for properties that straddle roads like the Trans Taiga, Billy Diamond, and various spurs, as well as waterways accessible by boat. Through consultation juniors can figure out where First Nations do not want helicopter traffic and design alternative routes. Yes that will cost extra money, but that is a small price to pay to allow First Nations to execute a seasonal ritual without disruption, especially given the size of the prize if your boots land on ground that proves to be an LCT-type pegmatite with large and abundant spodumene crystals.

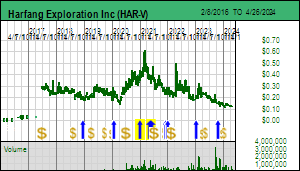

Although some James Bay juniors have to cool their heels over the next four weeks, others will be very busy with ongoing prospecting of their properties. One of these, whose CEO Ian Campbell claims that his company's properties fall outside areas First Nations have "reserved" for moose hunting, announced on September 13, 2023 that Harfang Exploration Inc had identified outcropping LCT-type pegmatite with a broad range of spodumene crystal sizes associated with a similar boulder field on its Serpent project. Ironically, Serpent was the focus of Harfang's exploration during the past few years based on a gold in till anomaly whose apron highlighted an area in the western part of the property. Drilling failed to yield a commercial scale explanation for the gold anomaly and in late 2021 CEO Francois Goulet chose to retire, which set the stage for a merger between Harfang and another junior with an adjacent property whose CEO Ian Campbell inherited Goulet's job. Goulet in turn went to work for Brunswick which had secured options on land once owned by Andre Gaumond's Virginia Mines and for whom Goulet worked as a junior geologist. Gaumond is the "godfather" of Harfang so it has been a somewhat difficult journey for somebody who was an exploration pioneer in the James Bay region seeking to establish its credibility as a source of precious and base metal mines, only to realize that those annoying pegmatites within the greenstone belts, whose outcropping mosquito and bush free ridges he strictly forbade junior geologists such as his protege Francois Goulet to waste time and money sampling, are in fact the world class foundation of the James Bay district.

Campbell was familiar with LCT type pegmatites because he had worked on the Big Whopper pegmatite the late Don Bubar's Avalon discovered in western Ontario in 1996. Once he got his head around the Lithium Mania 2.0 concept he used geology and lake bottom-sediment data to identify several other lithium prospects in the James Bay region he staked for Harfang. But the Serpent property had generated its own reports of pegmatites in the field, so when the forest fire closures ended he sent his boots to this ground first, and, lo and behold, the pegmatite dyke system is extensive, shoots via XRF as LCT type, and has large visible spodumene crystals. Just to make everybody feel stupid, the pegmatite system is located in the southeastern part of the property, far away from the Serpent gold target and the inlier claim owned by the Campbell company Harfang absorbed in 2022 in order to control the entire footprint of the gold system. It is too soon to determine what the average grade of the Serpent pegmatite system will be, or what sort of tonnage footprint it represents, but the market responded positively to it, sending the price from a $0.15-$0.16 range to as high as $0.23 before closing the week at $0.185 where Harfang's Serpent project has an implied value of only $12 million. Given that Harfang has $5 million working capital, multi-project exposure to James Bay, a top notch management team and backers, and now evidence of LCT type pegmatite outcrop on one its 100% owned projects, with boots heading to other projects in the next 6 weeks not impacted by the moose hunt restriction, why is the valuation so cheap?

In the case of Harfang it is possible that the selling is by grumpy gold bugs programmatically required to exit anything to do with climate change and energy transition policies. This sort of ideologically driven stock supply should be red meat for the Gamestop crowd; the enemy of the future is selling stock because the company may have a major lithium discovery in the James Bay region! Canadian companies, however, tend to have a different explanation for inexplicable selling activity, and that is the flow-through concept.

Canada has a system designed to encourage investment in exploration, where money spent by a junior can be written off against ordinary income by the investor who provided the money, often with a multiplier as is the case with Quebec, with the caveat that the cost base for the equity position becomes zero, so that whatever you sell the flow-thru stock at, all of it is subject to Canadian capital gains tax. Capital gains tax in Canada, however, has no long or short term distinction and has a favorable fixed rate rather than the progressively increasing rate applied to income. This allows all sorts of complicated strategies, though the expected outcome of them all is to postpone tax consequences into the future. This injects into the Canadian resource junior market a perverse investment dynamic that has little to do with fundamental outcome expectations. Harfang has done flow-through financings, so it is at risk of liquidation by shareholder who have neither knowledge about nor interest in Harfang's gold potential, let alone its relatively new lithium potential. Again, this is an opportunity for the Gamestop "Dumb Money", buying stock that the financial engineers are dumping as worthless.

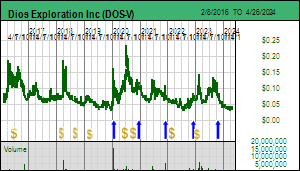

Another James Bay junior whose boots are pounding the ground and which is not affected by local moose hunting restrictions is Dios Exploration Inc. The stock should be trending up but is in fact sagging as a result of large scale selling through "anonymous". Who with a large position could possibly be selling at this stage in the story timeline?

The answer is so banal that it is a huge signal to post a bid below $0.10 and pray that you get lucky with a fill. In December 2022 Dios did a flow-thru private placement at $0.20 with two parties. One of the placees was a Toronto based entity called Marqeust that took 4 million shares at $0.10. The other 2.5 million was taken by the Maple Leaf group. When investors buy into a flow-thru fund they get a writeoff of their investment which starts at 100% and expands based on the province's special provisions. What happens to the stock in the flow-thru fund?

The Maple Leaf fund apparently transfers the entire stock portfolio into a general resource sector fund in which the FT fund holders receive units or shares they can elect to redeem or sell if it is publicly listed. That fund gets managed on the fundamental outcome potential of the companies in its portfolio. Given the way James Bay is shaping up I doubt the Maple Leaf fund manager will be in any hurry to sell its 2.5 million DOS shares.

Marquest, on the other hand, does a distribution in October which requires the fund holders to elect by some deadline to receive cash or shares. If 100% elect for shares all the stock ends up in the hands of individuals who will make independent decisions about those positions which does not constitute a structural overhang. This year, perhaps because of 5% plus interest rates being offered after a decade of near zero interest rates, apparently 70% of the Marquest fund has requested a cash distribution. This means Marquest must sell 70% of each stock position by the distribution date. In the case of Dios that is 2.8 million shares of which I estimate since last week about 1 million have been sold, leaving just under 2 million shares Marquest must still liquidate.

When the distribution date happens the fund holders who elected cash get a pro rata share of the cash pot while those who elected stock get a pro rata share of the remaining 30% of the original stock positions the fund purchased. Once we see another 1.8 million shares come out, probably through anonymous, Marquest will be gone. So I think if anybody wants to get a position below $0.10 without reaching for offers now is the time to post an open order.

Apparently none of the Dios properties are impacted by moose hunting restrictions due to their location. We probably won't hear any field results from Dios until late October when all the data has been received and analyzed unless something really obvious and big shows up. But how long will Dios and other James Bay juniors be able to prospect their properties?

As if it wasn't enough to lose 3 months of prime prospecting season to fire closures, and then in some cases another month to moose hunting season, now meteorologists are warning of an early hard winter arriving in October that will prevent random snow dumps from melting away. Once snow blankets James Bay boots on the ground are useless. If this weather trend prediction is correct, those companies hoping to get another 6 weeks of prospecting done after October 15 will be out of luck. The primary objective of serious James Bay juniors is to have an LCT-type pegmatite target sufficiently delineated to justify a drill program in Q1 of 2024 when the James Bay region is buried under a blanket of snow. From a market upside perspective, the bets on James Bay Lithium Index juniors will be about who will be in a position to drill a meaningful target in Q1 of 2024?

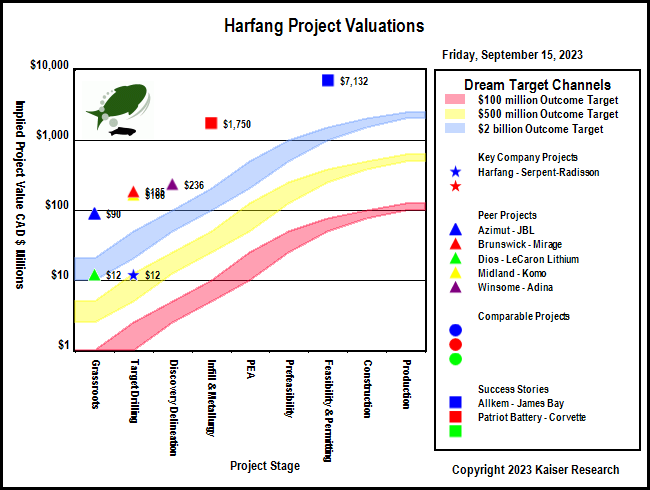

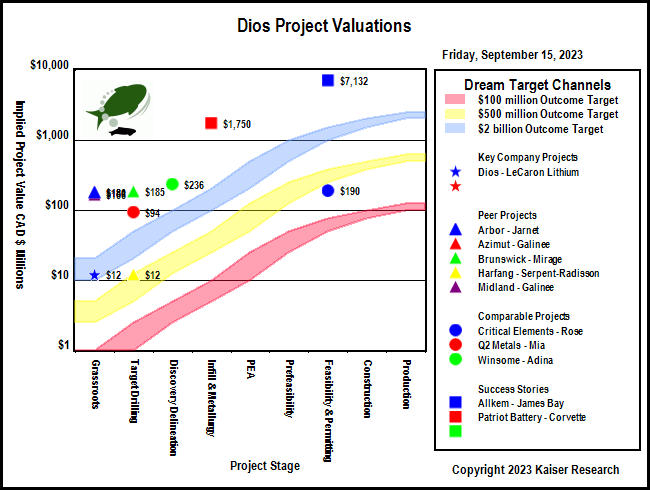

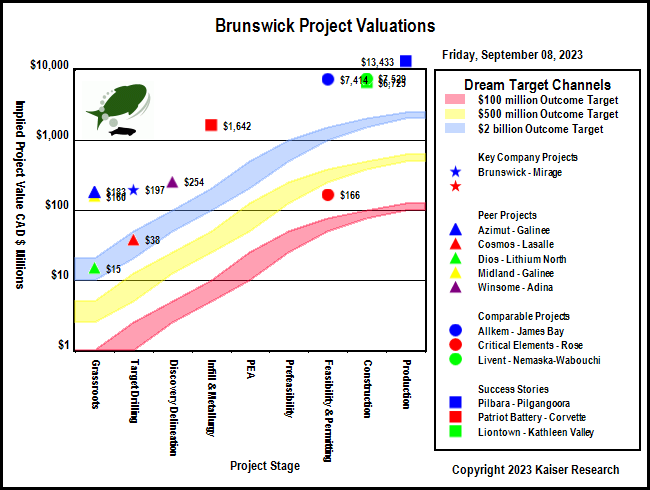

How can the Gamestop "Dump Money" learn to navigate the junior resource sector without getting nailed by juniors that have become over-priced because they are wasting shareholder money paying various social media entities to pump the stock, ones whose valuation is linked to an asset unrelated to the James Bay lithium exposure, or one whose flagship James Bay lithium play is farmed out, leaving the junior with a minority net interest that usually offers limited speculative upside during the early exploration stages? The key is to understand the rational speculation model and read my implied project value charts (IPV Charts) which visually show how a project's valuation on a 100% basis relates to the fair value certainty ladder for the different stages of the exploration-development cycle. An excellent tutorial is available in the Mining Stock Education Interview Bill Powers did with me in 2020, in particular the 21-46 minute segment.

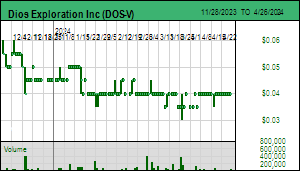

The IPV Charts I have included for Harfang and Dios show that the 100% owned James Bay lithium projects have an implied project value of only $12 million (fully diluted X stock price X net interest) compared to $185 million for Brunswick's 100% owned Mirage project which for the moment is Brunswick's flagship play. Within two years Mirage could command a $1.75 billion valuation if it turns out host a deposit similar to Patriot Battery Metal's CV5 deposit. The Harfang and Dios prices can increase ten times from the current levels just by demonstrating they have a similar lithium tiger by the tail, and Brunswick can increase another ten times by delivering a lithium tiger identical to or better than CV5.

List of Members of James Bay Lithium Index as of Sept 15, 2023

Regional James Bay Map showing locations of Harfang's projects

Map of Harfang's Serpent Project showing Spoumene Discovery Location

Photograph of Serpent pegmatite boulder field and spodumene crystals

IPV Chart for Harfang Exploration

IPV Chart for Dios Exploration

Jim (0:13:08): What is the best way to play Rio Tinto's exposure to the James Bay Great Canadian Area Play?

Among the world's major mining companies Rio Tinto is the only so far to take a serious interest in the lithium sector. More than a decade ago Rio Tinto discovered the Jadar lithium deposit in Serbia which is similar to claystone deposits except that the grade is comparable to the better LCT-pegmatites. No other deposit like it has yet been discovered, and Rio Tinto invested a fair amount of effort in developing a flowsheet for the jadarite mineral that hosts the lithium. The Jadar project, however, is now in limbo after Serbia revoked the license, ostensibly because mining would alter the bucolic nature of the valley that hosts that deposit. Rio Tinto is on record stating that the world will need 60 Jadar equivalent mines by 2035 if the EV contribution to net zero emission goals is to become reality. Jadar is equivalent to Allkem's Galaxy-Cyr deposit and Patriot Battery Metals' CV5 deposit. In its statement Rio Tinto underlined that its projection assumed a solid state lithium ion battery that uses lithium metal in the anode instead of graphite would never become commercial reality. We now know that Toyota claims it has solved the problem, and if it can continue to bring the manufacturing cost down to the level where it can offer its popular Camry and Corolla models as affordable quality cars with excellent range and very short charging times in 2030 and beyond, the world will need 120 Jadars by 2035. And unless there is a miraculous DLE breakthrough that crashes the production cost below $5/lb lithium carbonate, a substantial part of the future lithium supply will have to come from LCT-type pegmatites. And that means the future lithium market will be worth $200 billion annually, up ten times from $20 billion in 2022 (assuming lower long term contract prices than the spot average for lithium carbonate), which in turn is up a hundred times from the $200 million value of lithium supply in 2005.

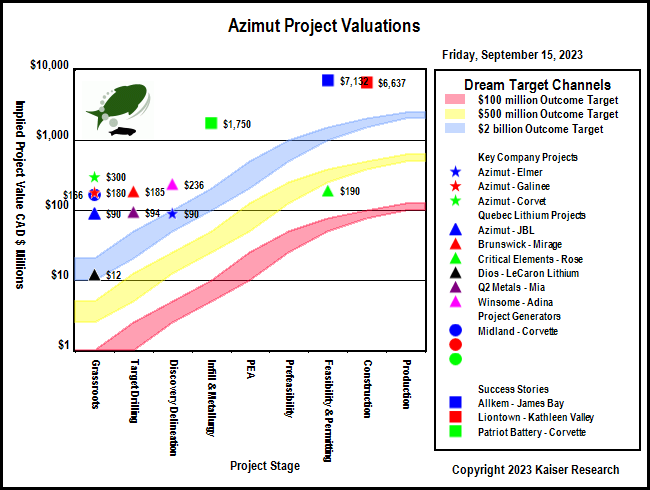

Rio Tinto gets this concept, but it is also reluctant to buy out Australian success stories such as Liontown, or emerging success such as Patriot Battery Metals. Instead it has chosen to do farm-in deals with juniors that have strategic land positions in Quebec's James Bay. Rio Tinto did its first deal with Midland Exploration Inc in June which I blasted in KW Episode June 16, 2023 because Midland gave to Rio Tinto the first pass opportunity to harvest low hanging fruit on its properties. In July Rio Tinto did a similar deal with Azimut Exploration Inc which I described as superior in KW Episode July 14, 2023 because Azimut retained the option once Rio Tinto vests for 70% to elect to reduce to a 25% carried interest, whereas Midland will have to contribute 30% of costs once Rio Tinto vests. The Azimut deal did not annoy me because it included only two properties, Corvet and Kaanaayaa, both located south of PMET's Corvette trend. Jean-Marc Lulin has dressed them up with 99% percentile lithium lake bottom sediment colors, but by themselves these numbers don't mean much because we do not know from where the sediments were transported. Midland in contrast included 10 properties scattered throughout the James Bay district which Rio Tinto selected for their LCT type pegmatite potential, including the Komo project west of Allkem's Galaxy-Cyr and Galinee east of Winsome's Adina project.

Both Azimut and Midland have since become a lot more enthusiastic about the lithium potential of the James Bay district where they have explored for gold and base metal deposits for decades. Azimut has staked a collection of new claims it calls the JBL group northwest of the Eleonore gold mine which it plans to explore on a 100% basis. Midland has not disclosed staking any additional James Bay properties for lithium potential, but it is now taking a close look at the properties Rio Tinto did not option. I suspect we will eventually hear more about Midland's 100% owned properties. But the question is, what is the best indirect bet on Rio Tinto being successful in the James Bay lithium district?

The hands down winner is Midland for multiple reasons. First, I do not think Azimut's properties will deliver any joy for Rio Tinto, and I was of the view that Rio Tinto would drop them in 2024 after Azimut has spent $3 million on them. However, the 3 month fire closure has pushed most of that spending into 2024, so Azimut will get to talk about its Rio Tinto farmout until at least 2025. As operator Azimut will of course do a very detailed exploration program that should generate lots of information about the non-lithium potential which was the reason Azimut staked them more than five years ago. Rio Tinto, in contrast, is operator of the Midland portfolio, and for the very reason I was annoyed by the farmout deal, has incentive to take a very hard and fast look to see if there is any low hanging fruit that can be quickly harvested. I would not be surprised if Komo and Galinee end up with drill programs in 2024, though the other properties could also deliver surprises. Within a year I expect Rio Tinto to have turned one or more of the 10 properties into discoveries that become the focus for discovery delineation. Since it is unlikely Rio Tinto will stay at 50% if it has a potential Jadar on its hands, Midland will be carried for the first $64.5 million exploration required for Rio Tinto to vest for 70%. And 30% of a $2 billion prize would be worth $6.75 based on 88.8 million fully diluted.

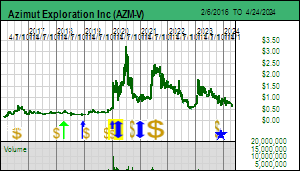

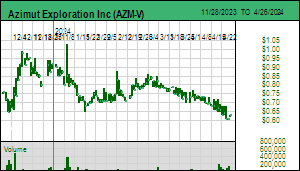

The second reason Midland is the better choice is the cheaper implied project value its exposure to Rio Tinto represents. Azimut's grassroots properties farmed out to Rio Tinto have an implied project value of $300 million based on 85.6 million fully diluted, a $1.05 stock price and a net 30% interest. In contrast Midland's portfolio of Rio Tinto farmouts has an implied value of $180 million, just over half that of Azimut, thanks to its $0.56 stock price. The reason Azimut is more expensive is that the company its being priced on the basis of its 100% owned Elmer gold project on which it has spent $25 million since 2020 without delivering a resource estimate. Elmer has an implied project value of $90 million. The problem with Elmer is that unless Azimut can duplicate the zone with similar discoveries within its shear corridor, Elmer is worth zero, and a black hole for exploration capital. This week Azimut secured an $8 million flow-thru bought deal which has prompted Agnico-Eagle to exercise certain rights to increase its equity stake from 10.06% to 12%. Azimut does not disclose what the money will be spent on, but you can be sure much of it will go into Elmer. For Azimut to become an interesting James Bay lithium play it needs to spin out Elmer as a separate company. As long as Elmer muddies the valuation water because we do not know what it is worth, Azimut offers poor speculative value even for its 100% owned lithium projects which share the $90 million implied project value of Elmer.

The third reason Midland is the better choice is that its remaining 100% owned James Bay projects carry an implied value of $50 million, which admittedly is 4 times what the market is assigning to the 100% owned projects of Harfang and Dios, but just over half what Azimut commands. To achieve parity pricing with, for example, Brunswick's Mirage project, Midland would only increase 4 times in price if it found a similar outcropping LCT-type pegmatite system. The fourth reason is that Midland is a prospect-generator-farmout junior with an extensive portfolio in the Abitibi greenstone belt with a number of those gold projects farmed out. Plus it has base metal farmouts in northern Quebec to Rio Tinto. Any one of these projects could deliver a discovery that justifies an upwards repricing of Midland's stock. Midland doesn't have the explosive upside potential of Harfang and Dios, but it has downside protection from as a result of its business model.

Jim (0:23:07): Will the James Bay Lowlands become a major diamond play?

The James Bay Lowlands should not be confused with the James Bay Lithium District which is in Quebec east of James Bay whereas the James Bay Lowlands are west of James Bay in Ontario. This vast area which drains northern Ontario is a water-logged black fly and mosquito infested region whose only communities are populated by First Nations. The only commercial activity to emerge from this region was the Victor diamond mine developed by De Beers which recently decided to shut down operations in the face of relentless criticism from the Attawapiskat First Nations and outside NGOs (see the anti-mining film After the Last River). The Ontario Cree are different from the Quebec Cree because the James Bay region was developed to produce hydro power for Quebec and the Quebec Cree have benefited from both the infrastructure and economic opportunity in their backyard. Northern Ontario in contrast is an absolute shit hole with no productive economy, and zero chance of developing one except through mining such as the Victor Mine. It is home to First Nation communities who subsist on government welfare payments, complain that they deserve more, and block any effort to create a real economy through mining. NioBay Metals' James Bay niobium project is in limbo thanks to a power structure within the Moose Cree First Nation that gives the upper hand to the NoCanDo members of the community.

During past periods of global warming when sea levels rose the James Bay Lowlands were covered by water, as a result of which the older basement rocks are hidden beneath a limestone cover that itself has zero mineral potential. The area from Moosonee south to Kapuskasing is known as the Kapuskasing Structural Zone. The KSZ was active between 2-1 billion years ago during which various intrusive bodies such as carbonatites made their way to surface. NioBay's James Bay deposit is an example of a carbonatite sufficiently enriched with niobium to be economic at current niobium prices which are not going lower because CBMM controls the niobium supply from its giant Araxa deposit in Brazil. VR Resources Ltd in recent years has explored the Ranoke and Hecla-Kilmer intrusions, the first as a potential IOCG system, and the second now as a rare earth system. There have been waves of exploration starting in the 1960s by large companies, including Selco which tested magnetic anomalies in the hope that they represented kimberlites. No kimberlites were ever found, and none of the carbonatites yielded commercial quantities of metal except the James Bay niobium deposit which was never developed because of its remote location and the superior Niobec niobium deposit in southern Quebec.

In September 2022 VR Resources drilled a longshot hole into large 1.2 km wide magnetic low anomaly called Northway which was never tested because there was no obvious explanation for what sort of orebody it might represent. It turned out to be a diatreme breccia body that erupted during the Devonian period before the area was covered by limestone, much younger than the carbonatite intrusions. Its magnetic low signature turned out to be due to the earth's magnetic poles being reversed during that period. When a magma cools and magnetite crystals form they line up according to the earth's polarity, which in this case was the opposite of the polarity when the basement rocks crystallized. It doesn't mean there is less magnetic material in Northway-1 than the country rock, just that the polarity is reversed. Because Northway-1 had the textures of a kimberlite, and was associated with a different emplacement period than the nearby much smaller alnoites Selco drilled in the 1970s, VR, on the hypothesis that a blind kimberlite field was hidden under the James Bay Lowlands' limestone cover, went on to stake 19 additional magnetic low anomalies ranging 100 m to 500 m in width.