Hello Guest User, You are visiting this website from a computer with an IP address of 172.70.130.151 with the name of '?' since Sun Apr 28, 2024 at 10:13:46 PM PT for approx. 0 minutes now.

Kaiser Media Watch Blog - December 1, 2023 to December 31, 2023

KRO Blog Overview

The KRO Blog is where unrestricted content of a time sensitive nature is posted. It includes the Kaiser Media Watch Blog which features content involving John Kaiser produced by third parties such as the Discovery Watch series by HoweStreet.com, interviews by outfits such as Investing News Network, SDLRC related commentary, the KRO Monthly Summaries, and just about anything else John writes that is not intended exclusively for the fee based KRO Membership.

Kaiser Watch is a weekly audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees which have changed for 2024 as a transition to a $200 per month auto renewal program in 2025. During 2024 individuals can register for a KRO membership at a non-refundable price of $450 for a term that expires December 31, 2024. All active KRO members will be grandfathered to renew annually at $450 on Dec 31, 2024. Sign up here for this limited $450 offer. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch December 22, 2023: Walking in a Winter Wonderland

Jim (0:00:00): How did you turn Kaiser Research Online into a Winter Wonderland?

(KW Episode Dec 22, 2023 was recorded Dec 22 but posted after the end of the year to allow us to use end of year graphics). The past year has been very dreary for resource juniors with the market declining into what seems like an eternal winter. At the start of Q3 one could feel a sigh of capitulation flooding into the resource juniors even as general equity markets began to perk up amid signs that inflation was subsiding and the interest rate hikes had likely peaked. Because this capitulation wave was dragging nearly all resource juniors regardless the stage of their projects, it was shaping up to be an excellent bottom-fish research season. Kaiser Research has a very powerful search engine which allows you to combine corporate and project level criteria to generate a list of hits. The resulting display is very useful because it includes a short and long term chart, basic information such as working capital, fully diluted, and key people, a truncated version of the overview if it exists (its full version will display in the company profile), a list of all company projects that fit the project level criteria. This snapshot also includes links to the KRO profile, the company web site, a people tree, a social forum such as Stockhouse or Hot Copper, 15 minute delayed quotes on Big Charts, and not too long ago a list of SEDAR filings. For an experienced user such as myself I could very quickly determine if it was going to be worthwhile to dig deeper into a company's fundamentals. This is important because doing a deep dive consumes 90% of the time spent researching a particular company, and when your goal is to identify potential future winners, discovering your target is a dud means you wasted a lot of time. That, of course, is not the case if your goal is to identify short selling picks, but since I am targeting cheap juniors that may qualify as bottom-fish picks that could appreciate 500% or more if missing pieces fall into place, there is no money to be made selling short a dead fish.

The typical KRO member is a sophisticated investor who has dabbled in resource juniors for many years and understands that there are four basic ways to profit from them.

One is to get positioned through an initial by invitation only round of financing in what is being primed as an orchestrated ramp job where the price of the privilege is an implicit expectation that at some point one will pump the stock to others to generate buying that takes the stock higher. Very few KRO members have this strategy available to them.

The second is to jump into a junior that already has a visible uptrend and hope that the trend remains one's friend until one has sold. The problem with momentum gambling is that the rush of a fast buck on paper is intoxicating and typically provokes the shareholder into finding out what story is driving the momentum and falling in love with it which prevents one from accepting that the trend is no longer one's friend.

The third is to jump into a stock that is just starting to wake up at the beginning of what will be a powerful and sustained uptrend driven by evolving fundamentals. I try to spot these, but if you have not done prior research which has revealed what the story is which the company is chasing, the risk is that the stock runs away too fast or has rallied on a false alarm. Newsletter writers endeavor to make such picks for their subscribers.

The fourth is to accumulate juniors flat-lining along a bottom after one has researched the underlying story and identified what needs to happen to launch a speculation cycle. The risk of the fourth approach is that the missing piece never falls into place, or takes a very long time to do so, turning it into an opportunity cost. To mitigate this risk the truly sophisticated KRO members accumulate a dozen or so bottom-fish positions and monitor developments closely, while also keeping an eye on other bottom-fish in the KRO collection. When an existing bottom-fish position or a bottom-fish being watched starts coming to life for the right reasons, the investor can make a much bigger investment by adding to an existing bottom-fish position or jumping into the watched one not already owned. The bottom-fishing strategy is thus a form a self-disciplined knowledgable monitoring.

The KRO Slack Forum in which KRO members can be members who post or just lurk, provided they follow the Slack Rules of Order when posting, is a very useful platform for catching bottom-fish breakouts, or detecting an imminent breakout courtesy of the increased chatter about that stock, much of which comes from me. By flagging resource juniors as bottom-fish I reduce the set of stocks one needs to monitor, and, when there is a critical mass of KRO members willing to post about their own long positions, my ability to monitor the entire collection is leveraged by the collective activity of other members. I mentioned that KRO members tend to be quite sophisticated in the resource junior space, but the KRO Slack Forum serves as a learning platform for newcomers to this sector. When something is hot off the press I will dash off my interpretation as a quick and dirty post in the Slack forum. And if somebody posts something that I think is off the mark, I will add a post presenting an alternative interpretation. This, of course, works in both directions; members either with a public post or a private message will point out when I am confused or missing an important detail. The collaboration aspect of the KRO Slack Forum is why I call it a Bottom-Fish Workshop

Plodding through the KRO search engine results can become tedious, especially when we are in a seemingly eternal winter where spotting a fabulous gem dirt cheap is accompanied by a nagging concern that such gem will never be recognized as such by anybody but oneself. The research process needs to have an entertaining and aesthetic dimension to it, and grinding through snapshots of 400 juniors with at least $500,000 working capital, insiders holdings at least 5% of issued, and trading below $1 is, well, just a grind, especially during winter. The key is to introduce a visual interface that goes beyond stock charts, and what makes resource juniors different from non-resource juniors is that their stories can each be reduced to a set of GPS coordinates plotted on a Google Earth map.

Back in 2018 one of my summer student employees figured out how to do this with Google's Fusion tables and we spent a lot of effort adapting KRO's company-project database so that I could embed a Google Earth map in a KRO web page which displayed a range of color and shape coded icons. Even better, when you clicked on an item, a "card" would pop up with basic information and key links such as the project's location inside the company's KRO profile. At the same time one could zoom into the project area and explore its local features and potential issues such as a nearby village, as well as figure out what other companies are in the vicinity. I could even create embedded maps filtered for particular companies or projects with specific target metals. This was really cool but, unfortunately, a year or so later Google, although observing that journalists and all sorts of non-profits dealing with geo-location based information got tremendous mileage out of Fusion for common goods, could not figure out how it served the Google good and pulled the plug on Fusion.

That was a bummer but such is what life can be at times. My son was able to adapt a different platform for the kimberlite database that is part of the Pat Sheehan Diamond Literature Compilation I host as a free public good on KRO, but then covid came along and I never made the effort to adapt the new platform to the KRO database. But during the past year as I was covering what is supposed to become the Greatest Canadian Area Play ever, namely the James Bay lithium pegmatite hunt in Quebec, I got frustrated by the absence of regional maps such as Glen Jones used to produce, and the tendency of juniors to publish maps showing the location of their properties, but not that of any neighbors unless it happened to be a junior with a major discovery such as PMET's CV5 pegmatite. Although the James Bay region is a featureless region, I was usually able to pinpoint the center of a junior's property on Google Earth and capture the coordinates.

My frustration arose because a Great Canadian Area Play has a dynamic where fundamental success by one company tends to feed market interest in nearby companies. In the case of lithium where the world may need 600%-1,200% more lithium supply by 2030 to meet EV deployment goals and expectations than the 130,000 tonnes of lithium metal equivalent produced in 2022, there is no reason for juniors to hinder others from benefiting from that company's success. But despite my high expectations in Q1 of 2023 that a lithium exploration boom would sweep Canadian resource juniors, duplicating what happened to Australian juniors starting in 2015, the speculative winter that descended on the market in Q2 of 2023 compelled juniors to hoard information so that what little risk capital was coming into the market would not be sucked up by juniors with nearby properties.

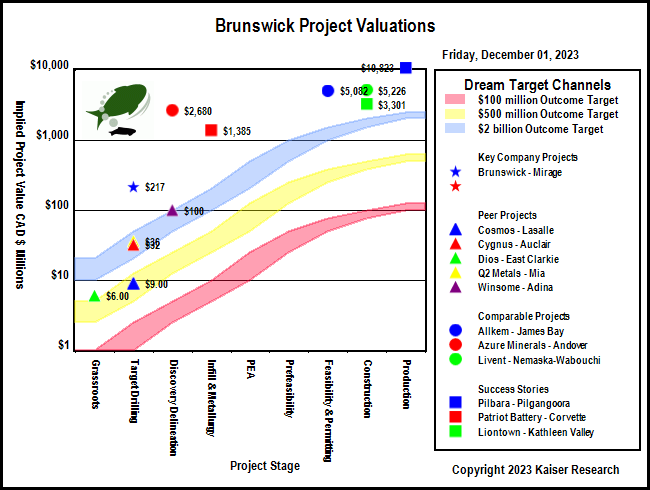

So in late November I bit the bullet and threw myself into reviving a map platform for KRO to light up the dreary winter as a wonderland. The icons come in 3 shapes with diamonds representing a company's flagship project, squares representing the secondary projects on which some activity is underway, and circles representing projects the company still has on its books but are either being held for a farmout or for a relevant miracle to happen that makes the project interesting. The icons are color coded to reflect the stages of the project, with green representing grassroots or target testing stages, blue representing discovery delineation stage (when there is still bluesky), purple the infill drilling and metallurgy stage (a JORC or 43-101 resource estimate has been published), yellow for the PEA or PFS stages (the PEA stage means a PEA has been published, and PFS stage means the company is now working on a PFS), orange for the feasibility and permitting stage, and red for the construction and production stages, with construction also doubling for a suspended mining operation. I may be suffering from advanced mental hypothermia, but these colorful maps do cheer me up like sparkling Christmas trees in a winter wonderland.

These maps are not visible to non KRO members because they make researching resource juniors more efficient and entertaining, and while information wants to be free, efficiency translates into time which is money, and what a KRO membership is to a degree selling is the saving of time, like renting a jackhammer to dig out those old fence post footings rather than wasting time and effort banging at them with a pick axe. As for entertainment, somebody might be entertained by enjoying a free Kaiser Watch episode or noting some member only analytical comment an unworthy KRO member has copied into social media, the entertaining exploration of the earth for potential resource junior winners is an individual experience to which there is an admission fee.

Right now the new KRO map platform has been embedded within the metal supply reports where you can spot all projects with say, copper or lithium as the primary target metal, or, cases like silver where silver is the first or second most important metal, and by-product metals such as platinum and palladium where the metal simply needs to be a target metal. Within the KRO database system once a resource estimate has been published only those metals included in the resource estimate are defined as target metals and in the position of importance defined by the company. Maps have also been embedded in country and state/province profile pages so that you can focus only on Nevada projects, though thanks to the Google Earth zoom function you can do that with the global map that features all projects for which we have GPS coordinates with at least approximate reliability. The company profiles also include a global scaled map featuring only that company' projects.

And we also have custom filtered maps, such as the map at the top of the current week's news release report which features icons for the flagship projects of companies that published news. There are separate news release web pages for the Canadian and Australian listings. Over time I will develop a catalog of maps with very specialized filters geared toward different "story themes". A key aspect of KRO is that it is a research platform whose members bring their own confidential criteria to the search engine. The KRO map platform does not have that search query construction facility, but members can propose filter sets via the KRO Slack Forum to be added to the catalog. I can't change the fundamentals of the resource junior market, but I am doing my best to make the experience more enjoyable and entertaining for KRO members.

Global Map with all Company Projects

Global Map showing all projects with gold as primary target metal

Global Map showing all projects with lithium as primary target metal

Example of Popup when you click Brunswick's Mirage project icon

Jim (0:04:38): What does your 2024 Bottom-Fish Collection look like?

The 2024 Bottom-Fish Collection has over 80 members and there remains a long list of candidates I have to take a closer look at before adding them to the collection. Unless there is a miraculous upswing during Q1 of 2024 that is more than a short-lived January Effect which forces me to focus on those juniors I have already vetted as bottom-fish, I will be adding many more to the 2024 collection. In a sense I am creating a Survivors Club because I am very concerned that the Canadian resource junior eco-system has crashed through an extinction threshold and is now on an irreversible path towards disappearing as a Canadian institution that has been the basis of my career since I first opened an account in 1978 to trade resource juniors. What I do not know is how quickly or slowly this decline will unfold, but there is a tenacious type of management team which will survive longer than the opportunists who will flee or just fade away in the face of how difficult the funding environment has become.

The financial statements for quarters as recent as September 30 have now been updated and I have a pretty good overview of the financial shape of the resource juniors, in particular the TSXV and TSX listings. I do not include the CSE listings because I am far behind adding to KRO the flood of new CSE listings focused on the resource sector, which really makes me wonder what these groups are seeing about the Canadian resource junior future that I am missing. This episode includes the key graphics I am about to describe.

Let's start with a chart which displays the daily traded value of TSXV resource listings and the TSXV S&P Index which is currently near a low achieved in late 2015 (not counting the steep plunge in Q2 2020 when covid erupted). Since the secular resource junior bear market began in 2011 the TSXV Index has wandered between 500-1000 which suggests a largely sideways trend. The reality is much, much worse. At the end of November the TSXV had 1,905 listings of which 1,035 (54%) are designated as "mining". The index as it is currently constituted has 136 members of which 86 (63%) are in "mining", the catchall term for resource sector that does not include oil & gas. KRO has 1,149 TSXV listings as being in the resource sector, though this will include companies that have been pushed onto the NEX board of inactive companies. The index reflects only 7.5% of the TSXV resource juniors, and because its composition is based on market capitalization criteria, and preserves the value of listings that migrate to a more senior exchange such as the TSX, it does not come close to capturing the misery afflicting resource juniors. Furthermore, during the past decade TSXV trading value shifted significantly in favor of non-resource listings such as cannabis and blockchain startups, many of whose winners migrated to bigger exchanges; their subsequent demise is not captured by the index.

The resource member composition of the index has a fairly good representation of the different types of juniors and stories, but the index does include juniors like Arbor Metals Corp, which is run by people who own zero shares, have none or little incentive options and minimal salaries, working for shareholders none of whom owns enough stock to be a reporting insider. After the stock split 3.5:1 in March 2020 it ramped to $2 in Q3 of 2020 on the basis of a Burkina-Faso project abandoned in 2022 after Arbor acquired the Jarnet lithium project near PMET's Corvette project in the James Bay region. Remarkably, along the way the placees of a 2019 private placement allowed 19 million vastly in the money warrants at $0.04 to expire! Since late 2020 Arbor has consistently traded above $2 until a sharp price decline in October 2023, but did not raise a penny until the decline. The balance sheet had a growing working capital deficit that was funded by loans from an obscure German entity which recently converted the debt into paper. There is no evidence of any marketing deals apart from a one time $26,000 deal in 2020 with a Vancouver outfit to prepare marketing materials, and the junior seems to be absent from social media networks. The press releases were typically congratulations extended to government agencies, EV and battery companies, and other juniors such as PMET. The web site is an ode to information minimalism and I could not find a link to a corporate presentation. Arbor did some boots on the ground prospecting at Jarnet in Q3, but has not yet reported anything to indicate that it is anywhere near making a lithium pegmatite discovery that would explain why the junior had a market cap in excess of $200 million during most of 2023 and traded 133 million shares with a value of $341 million, 40% of which was sold through Anonymous, but much of it bought through a respectable list of Canadian and American brokerage firms. Despite no indication yet that Arbor has a discovery on its hands, the junior managed to raise over $5 million in Q4 of 2023. This member of the TSXV Index is a shining example of what the Canadian regulatory and financial establishment represents and why the resource junior eco-system is dying.

So forget about the TSXV Index as an indicator of market sentiment with regard to the resource juniors. A much better indicator is a price range graphic I have been compiling since 2002 which features both TSXV and TSX resource listings. When I invented it I created 12 price range categories at a time before Canadian juniors tended to have less than 100 million shares issued. But during the past two decades the market became more tolerant towards high issued figures, in part because brokers became less important in "managing" markets and the liquidity of a high issued number was appreciated by investors trading through online brokers. The percentages of the different price ranges turned into noise except for the bracket representing stocks trading below $0.10 (the red line). During the China super-cycle peak of 2006-2008 the percentage of resource listings trading below a dime dropped to an astounding low of 4%. But with the 2008 financial crisis that figure soared to 53%. During the gold and M&A boom of 2009-2011 there was a remarkable recovery and the percentage dropped to 12.6% in early 2011 just before the secular resource bear market began. This massive sell-off hit its nadir in late 2015 when 66.1% of resource listings were languishing in the gutter below a dime. Many of them escape the gutter by doing a rollback, but in most cases it takes less than a year for such juniors to descend back into the gutter. I have found this percentage trading below a dime to be a reliable indicator of both inflection points and the trend of market sentiment toward Canadian resource juniors. The last major peak was in 2020 at 53.7% during the covid abyss, which was followed by a remarkable recovery that left only 22% of listings trading below $0.10 in mid 2021. Since then we have witnessed a trend of weakening sentiment, reversed briefly in late 2022 when I came to believe we were heading into a secular resource bull market based on geopolitics and energy transition requirements. The 2023 worsening sentiment trend peaked at 47.2% at the end of October, and finished the year at 46.5%.

During H2 of 2023 we saw a brutal wave of capitulation selling that coincided with a sharp drop in financing activity as shown by my monthly chart of TSXV resource junior financing activity going back to 2009. The situation is uglier than it looks because the financing total is based on a smaller number of companies raising capital, especially through private placements. I've annotated the chart to show past financing winters, of which the 2013-2015 period was the longest. The most recent one lasted two years between mid 2018 and mid 2020. The question today is how long is the 6 month old financing winter going to last?

The next graphic to look at is the one which uses my price range categories to tabulate the total positive and negative working capital of TSXV resource juniors in each price range (working capital is current assets less current liabilities, a figure the regulators have striven to make less useful by forcing juniors to record as fictitious current liabilities the financial consequence of not spending flow-through funds within the time required, which drags down the working capital figure, and makes it imperative to look at balance sheet details once a stock has triggered deep dive research). Overall resource juniors have just under $4 billion in positive working capital, of which $754 million is held by juniors trading below a dime. But those with negative working capital owe $3.3 billion of which a staggering $2.2 billion is owed by juniors trading below a dime. The latter are zombies waiting to be delisted or have all their debt converted to paper followed by a brutal rollback and subsequent price decline to the pre-rollback level. This is the minefield that bottom-fishers need to navigate.

The next graphic to examine is the one that shows how many companies and percentage of the total have working capital within one of the 17 ranges I have created. These can be broken down into three groups: 1) negative working capital which will be companies to avoid with a few exceptions, 2) zero to $500,000 working capital which will be companies that are still alive, but will need a market sentiment uptick to raise capital in order to get exploration work underway that could boost the fundamentals of their story, and, 3) those with more than $500,000 which not only allows them to get work underway, but which would be the first to follow upwards a sentiment change and would attract financing offers (capital markets hate giving money to juniors that need it except at severe knockdown prices). There are 1,149 TSXV resource listings in my database, of which 456 or 40% I can ignore as zombies, and 489 or 43% have more than $500,000 working capital and are the target of my bottom-fish research. There are 193 or 17% in the zero to $500,000 range which are also potentially interesting, but require more work to investigate, and will probably remain in the bottom-fish gutter until a bull cycle is clearly underway.

Assembling the 2024 Bottom-Fish Collection has been a difficult task because almost the entire resource junior sector is trading at depressed prices. I started building the 2024 collection in October, and while the basic parameters such as working capital and minimum 5% insider stake are easy to filter through the KRO Search Engine, the hard part is assessing management motivation and story potential. When I got the new map platform up and running I created a map that features only the flagship projects of those juniors in the 2024 Bottom-Fish Collection. I was shocked to discover how biased I am in favor of companies focused on Canada and the United States, especially in view of the First Nations and NIMBY blockade that is hindering juniors. I had hoped to be done by the end of the year, but I will be busy in Q1 of 2024 researching bottom-fish opportunities in Mexico, South America, Africa and Scandinavia. Most Canadian juniors are not active in Australia, and I am not yet comfortable creating an ASX Bottom-Fish Collection.

To help me overcome my aversion to these other jurisdictions I created a map which features the flagship projects of companies where insiders own at least 5% of issued stock, market capitalization is less than $500 million, the stock price is less than $1.00 per share, and working capital is at least $500,000 as of the most recent filing. And which have not already been tagged for the 2024 Bottom-Fish Collection. As explained earlier, KRO members can explore this winter wonderland by clicking on icons to get the popup, and if the basics look interesting, click through to the KRO company profile for a deeper dive. This is a lot more fun than grinding through a long list of KRO Search Engine results.

As a fan of equal opportunity I also created a Zombie Map featuring flagship projects of companies with negative working capital and where visible insiders own less than 5%. One that I still have to create will be the Gray Zone of juniors with positive working capital up to $500,000 and minimum 5% insider stakes. As I get rolling I will create a whole catalog of customized maps which will allow KRO members to explore those themes and criteria sets that interest them.

An important change for 2024 is that it will be a transition year at the end of which I will either shut down Kaiser Research Online as a public platform or continue it with a substantially higher membership fee, likely USD $200 per month available only on an auto-renewal basis. During 2024 the KRO membership fee will be fixed at $450 non-refundable and expiring on December 31, 2024 regardless when somebody subscribes. Obviously the value will reduce as the year progresses, but there might even be value in paying $450 as late as December 2024 because all members at the end of 2024 will be grandfathered to renew for $450 for another year. In 2025 and beyond new members will have to pay the substantially higher rate. Current KRO members with an expiry in 2024 can renew at a prorated price reflecting the days left in 2024.

Why am I doing this? Since the bear market began in 2011 there have been major changes in the dynamics of resource sector speculation, with a major shift to companies paying parties to pump stock picks to audiences that have signed up for free. There is a trend of information platforms that could emulate the KRO information platform and make structured data search available free or at a very low price. That threat could come from the currently mothballed Share Collective if it is revived or acquired by a properly bankrolled group. There has also been a proliferation of social media forums in which copyrighted material gets circulated. This is not a problem right now because nobody cares about resource juniors, but it is not impossible that a secular resource bull cycle will explode next year or perhaps in 2025, especially if the United States undergoes a leadership change that turns its dependency on raw material supply from anywhere but the United States into an acute liability. If we do get a bull market there will be an influx of amateurs jumping onto the bandwagon who would be absolutely bewildered by the KRO platform, especially if it is functioning as a bottom-fish workshop for sophisticated resource sector speculators. They can spend $200 for what amounts to a one month trial and discontinue if KRO doesn't work for them. The goal in 2024 is to attract a core group of bottom-fishers who will be part of a research club focused on resource juniors. If you want to be part of this club Sign Up Here.

TSXV Index and Resource Listiing traded value chart

Here is what makes the Canadian regulatory and financial establishment proud

Monthly Percentage of Canadian Resource Listings trading below $0.10

Monthly TSXV Resource Listing Financing Activity

TSXV Resource Listing Working Capital per Price Range: Positive vs Negative

Working Capital Range Breakdown for TSXV Resource Listings

2024 Bottom-Fish Collection Map

Potential Bottom-Fish Map

Zombie Map

Jim (0:11:32): What will your 2024 Favorites Collection look like?

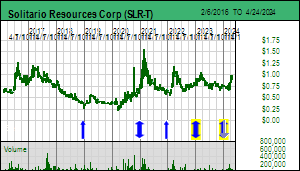

When I launched the KRO Favorites concept in 2022 as a free collection of stock picks covered through the Kaiser Watch series the idea was that it would feature graduates from the Bottom-Fish Collection. I was very optimistic about the 2023 Favorites Collection because I believed we were on the cusp of a major resource sector bull market driven by energy transition needs and geopolitics which would also boost the price of gold. The 16 companies represented multiple themes and metals. The 2023 Favorites Index got off to a good start, gaining 26.8% by early March, but it was downhill from April onwards when several banks failed due to the high interest rate policy of the Federal Reserve, China's post-covid rebound fizzled, and global macroeconomic demand stalled. Even though gold finished the year up 14.7%, the Favorites Index finished the year down 20.8%. Brunswick Exploration Inc was the star, finishing up 74.7% and will be part of the 2024 Favorites. Colonial Coal International Corp was the second best performer up 48.4% and will be continued. The only other Favorite that finished up was Faraday Copper Corp with a gain of 16.7%, but after the PEA showed that higher copper prices or richer ore were needed to make Copper Creek worth developing, it slumped back into a Bottom-Fish Spec Value rating. West Vault Mining Inc was added in April as a gold proxy and while down 6.9% continues to offer Good Speculative Value and will be continued. Solitario Resources Corp was down 11.9% thanks to the sluggish USFS permitting process, and while I've temporarily tagged it with a Bottom-Fish Spec Value rating, it will be a 2024 Favorite. All the rest have been consigned to the 2024 Bottom-Fish Collection. There will be a few new additions to the 2024 Favorite Collection, but it will be a much shorter list than 2023.

2023 KRO Favorites Index

2023 KRO Favorites Performance

Disclosure: JK owns Brunswick; Brunswick, Colonial Coal, Solitario and West Vault will be 2024 Favorites

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch December 15, 2023: Are anti-mining people Putin Poodles?

Jim (0:00:00): Is Solitario any closer to getting a drill permit for its Golden Crest gold project?

On December 12, 2023 Solitario Resources Corp announced that the US Forest Service has reported a Finding of No Significant Impact (FONSI) for a 25 drill site plan of operations application Solitario had submitted in early 2022. As explained in KW Episode May 12, 2023, Solitario's hope to have a drill permit by Q2 of 2023 to allow a summer drill program was derailed by an uproar created when a private group applied for a drill permit near the Pactola Reservoir in the southeastern part of the Black Hills region. This distracted the entire USFS staff which eventually dealt with the problem by creating a 8,329 ha mineral withdrawal around the reservoir. A draft environmental assessment by the USFS for Golden Crest was not completed until May 2023, but there was hope a final permit might be received by late August to allow a fall drill program. No such luck. The FONSI is an important milestone but it will be 4-5 months before Solitario has final approval to proceed with a drill program, assuming the anti-mining lobby does not file a lawsuit against the USFS.

The FONSI kicks off a 45 day public comment period which the USFS can extend for another 30 days and probably will because of the overlapping holiday season. Once the comment period has closed the USFS has 30 days to defend itself against all the complaints filed by the anti-mining crowd. The USFS can elect to extend its response period by another 30 days. It can then make a decision to grant a drill permit, which would be good timing because Solitario cannot mount a drill program until May. It is important to understand that Solitario's only role in any of this is to pay the cost of all the studies the USFS needed in order to make a competent and objective decision. The best case is 3 months for a decision, increasing to 4-5 months if all extensions are deployed.

However, once the USFS has approved a plan of operations there is a risk that one of the anti-mining entities will file litigation claiming that the USFS did not adequately address the objections. This may be the first drill permit the USFS would have granted in South Dakota in a long time (the drilling by Coeur and Dakota Gold in the northern part of the Black Hills is all on private land). The unknown question is how long would it take the courts to deal with such a lawsuit? At the state level South Dakota is entirely Republican and supportive of resource development, and since Golden Crest is only a low impact drill program, not a mining permit application, the courts might deal with a lawsuit quickly.

The stakes are very high, because Golden Crest continues to evolve as the hottest at surface gold prospect in the United States. Solitario has collected about 42,000 soil samples and about 10,000 bedrock samples during the past few years from about 75% of the property (the remaining 25% doesn't appear to be as interesting). CEO Chris Herald remains reluctant to publish a gold anomaly map because I suspect it would light up Golden Crest like a glorious Christmas tree. That, of course, raises the question, why was Golden Crest not discovered and turned into a mining district more than a century ago when the 90 million ounce Homestake district was discovered?

It turns out that even when Solitario has a carbonate rock sample that grades 100 g/t gold, no gold ever shows up when the sample is crushed and panned, the primary manner in which prospectors assessed the gold potential of interesting rocks. The gold grains apparently are micron sized, similar to the carbonate hosted Carlin type mineralization in Nevada. Unlike in the Homestake area, where the Precambrian banded iron formation rocks that host the former mine's 60 million ounces outcrop, the Golden Crest area is completely covered by carbonates that are even younger than in the Wharf area where Coeur is mining Tertiary aged carbonate hosted mineralization.

That may explain why earlier prospectors never dug any glory holes despite the abundance of altered structures at surface, but not why Homestake, which controlled the Black Hills district for a century, never paid any attention to the "other side of the mountain". Homestake drilled three 4,000 ft holes which confirmed the presence of Precambrian banded iron formation rocks with the same age as the Homestake deposit. Drill logs show the presence of alteration within the 1,200 ft sequence of carbonate cover rocks. None of the carbonates were assayed though presumably the BIF rocks were assayed for gold but came up blank. One of the holes still exists in a government storage unit but the bureaucrats have ignored all efforts by Solitario to gain access.

Historical research by Solitario has established that within Homestake there was a mindset that only Precambrian gold mattered, which is understandable in view of how rich the Homestake "ledges" were. The much younger Wharf mineralization in the carbonates at a tenth of the Homestake grade was apparently dismissed as inconsequential. This corporate culture quirk to which geologists are not immune may be the reason Solitario's Golden Crest project could turn into a multi-level monster gold discovery. Tracker Dec 20, 2022 explains how 3 different types and ages of deposits may be present.

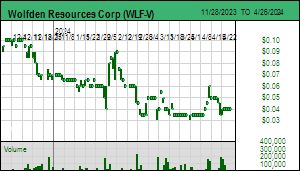

America's anti-mining lobby, however, is formidable, and we saw this in action when Maine's Land Use Planning Commission held a hearing on December 13, 2023 during which LUPC staff were to present their analysis of the mine rezoning application of Wolfden Resources Corp. There are 9 commissioners who are not experts in the areas of environmental impact assessment, and this hearing was intended to allow the expert staff who processed Wolfden's application to present their findings and allow the commissioners to question the staff and eventually make an objective decision.

Pickett Mtn hosts a polymetallic VMS deposit in an area of northeastern Maine that is a large scale tree farm where stands of timber get cut down regularly. Maine has a new mining code which establishes the protocols for approving a mine and which forbids open-pit mining. In September 2020 Wolfden completed a PEA to support a 1,200 tpd underground mining operation (see Tracker Nov 27, 2023 for background). To begin the feasibility study and permitting stage Wolfden needed to have the Pickett Mtn mine site rezoned for industrial use. The Land Use Planning Commission rejected the application on October 13, 2021 on the grounds that it did not have the capacity to assess the proposal, even though that is the responsibility of the Department of Environmental Protection. What the LUPC was worried about was the presence of a mill and tailings storage facility, and somehow Wolfden got the idea that if it planned to build the mill and TSF simply on land within a nearby township, the rezoning would be approved. So Wolfden has spent the last 18 months scouting out the nearby townships and securing support for building the mill and TSF on land outside the LUPC jurisdiction.

The LUPC currently has only 8 commissioners, with the new ninth member not scheduled to be sworn in until early January. The commission chairperson was unable to attend, so only 7 commissioners were present. I've clipped the key segments from the "Guide for Commission Deliberations" where the staff has identified the pros and cons for mine development with regard to six considerations (Financial Practicability, Socioeconomics, Wildlife Resources/Habitats, Natural Character, Historical and Cultural/Relevant Tribal Impacts, and Water and Fish/Aquatic Habitats). The LUPC staff had highlighted those items it deemed relevant to decision making, and these were all on the "supports approval" side of consideration segment. So the job of the commissioners was to stress test these items to see if the staff did their job properly. As it turns out, three of the commissioners are anti-mining fundamentalists and effectively hijacked the session to create the impression for journalists that a mine in Maine is a very bad idea.

There is a false dichotomy that presents ideology as a linear spectrum from left to right, but a better way to present this spectrum is as a horseshoe whose ends nearly meet. Both ends are characterized by righteous certitude, the "left" with abstract moral truths and the "right" with sacred text based moral truths. The middle, which used to be called "liberal", represents individuals who understand that only tautologies qualify as truths, that scientific truths are ever evolving descriptions of how the universe works, and moral truths are goal oriented prescriptions of how human relations in a reality of physical scarcity ought to be organized which to qualify as "moral" must have universal applicability. What makes the left and right ends of the horseshoe very different from the middle of the horseshoe is that the certitude at each end of the horseshoe is the basis for oppressing others who do not share that certitude. The "liberal" middle has to live with the realization that in the moral realm the set of commonly accepted values is inconsistent and requires choices that always create winners and losers, denying the luxury of righteousness. For the middle pragmatism and negotiation becomes the guiding principle, something that is missing from the extreme ends of the horseshoe where it is all about coercing others.

The right end of the horseshoe makes no bones about being Putin Poodles, eager to see Ukraine thrown to Putin, and adoring the idea of a "strong leader" who seeks to exterminate the "enemies of the state" like vermin. The left end of the horseshoe where Xi Jinping sits, reaching across the aisle to shake hands with his buddy Putin and throwing individuals under the bus for the collective good,includes anti-mining fundamentalists who are unwitting Putin Poodles in their zeal to "protect" countries within the Global West from mining. Some, I suspect, are in fact self-aware Putin Poodles who adore strongmen like China's Xi Jinping and Russia's Vladimir Putin, and are de facto agents undermining democracy possibly funded by donations from unknown sources.

I have prepared a bar chart that everybody should familiarize themselves with so that they can figure out if they are witting or unwitting Putin Poodles. The IMF's October 2023 World Economic Outlook projects that the 2023 GDP will be $26.9 trillion, China's $17.7 trillion, and Russia's $1.9 (Canada is $2.1 trillion). The combined China-Russia GDP of $19.6 trillion is 73% of America's GDP. And yet China and Russia dominate the supply of raw materials, with the United States generally supplying less than 10% of most of them and often nothing at all. The blue bar represents America's share of raw material supply, and the labels represent what share of total global supply China and Russia represented in 2022. China and Russia are now allies in the Global East, both autocracies inflicting their horseshoe certitudes on their own people while endeavoring to assert them over others. When anti-mining people undermine the exploration and development of raw materials in Global West nations as a matter of "principle", not only do they parasitically support the victimization of downstream parties powerless to defend themselves in jurisdictions like China and Russia, but they are also boosting the raw material vulnerability of the Global West, exposing democracy to the future predations of autocracies. Anti-mining people are implicit Putin Poodles and they might as well join the Putin Poodle Party.

US Vulnerability to China-Russia Raw Material Supply

LUPC Guide for Deliberation Wolfden Pickett Mtn: Financial Practicability

LUPC Guide for Deliberation Wolfden Pickett Mtn: Socioeconomics

LUPC Guide for Deliberation Wolfden Pickett Mtn: Wildlife Resources/Habitats

LUPC Guide for Deliberation Wolfden Pickett Mtn: Natural Character

LUPC Guide for Deliberation Wolfden Pickett Mtn: Historical & Cultural Resources/Relevant Tribal Impacts

LUPC Guide for Deliberation Wolfden Pickett Mtn: Water & Fish Resources/Aquatic Habitats

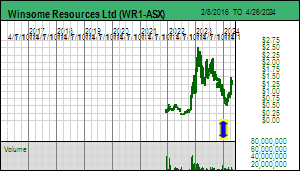

Jim (0:14:03): What did you think of Winsome's maiden resource estimate at Adina?

Winsome Resources Ltd published a maiden resource estimate on December 11, 2023 for its Adina lithium project in Quebec's James Bay region. Although the market initially had a positive response, trading Winsome as high as $1.25, by the end of the day the stock closed down a half penny at $1.04, and traded as low as $0.85 during the next couple days. The resource was estimated at 58.6 million tonnes of 1.12% Li2O based on 93 core holes (27,625 m) with 100 m spacing covering 1,340 m strike of the Main Zone (Jamar). Assays are pending for another 25,000 m drilled in 2023, with 5 rigs operating in December and another 50,000 m drilling planned for 2024. I thought it was an excellent maiden resource estimate and was puzzled by the negative market reaction.

One reason is the poor optics of a lithium carbonate price plunging as low as $6.30/lb during December amid hand-wringing media talk about how consumers are no longer lining up to buy an electric vehicle. That concern is irrelevant to resource juniors making lithium pegmatite discoveries today, because none of that lithium will be in production before 2030. You just need to look at the lithium price-grade rock value matrix to see that even a price in the $5-$10/lb lithium carbonate range makes most open-pittable gold deposits look pitiful.

The main reason, however, for the negative reaction to Winsome's maiden Adina resource is the decision to choose 0.6% Li2O as the cutoff grade, chosen I suspect to meet the market's expectation of a resource with at least 50 million tonnes. The trade off was a lower grade than the 1.42% achieved by Patriot Battery Metals Corp for its maiden CV5 resource of 109.2 million tonnes. But Winsome did publish a table with different cutoff grades, and at 1.1% the Main Zone delivers a resource of 26.7 million tonnes of 1.44% Li2O. Following an October financing Winsome has about $60 million, so dilution to fund expansion of the Adina resource is not a problem for 2024.

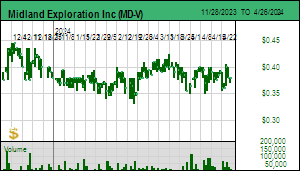

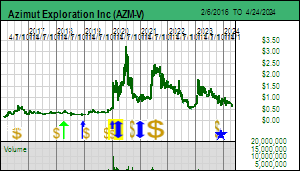

The Adina resource is good news for Comet Lithium Corp whose 100% owned Liberty property adjoins to the east of Adina and is on strike with Winsome's expansion drilling northeast of the Main Zone. Comet underwent a management change in November that brought on board the team behind Nomad Resources Partners Inc, including Vincent Metcalfe as the new chairman and Vincent Cardin-Tremblay as exploration VP. They were too late to influence a sampling program initiated by former management, but they did manage to get a gravity survey done in the western part of the property where the Trieste formation is present before it bends southeast onto the Galinee project Rio Tinto has optioned 70% from Midland Exploration Inc and plans to drill in Q1 of 2024. Azimut Exploration Inc, which is joint ventured 50% with SOQUEM on their own Galinee project to the south of Winsome and Midland, has drilled a dozen holes chasing the down dip projection of the Adina Main Zone and is awaiting assays. Azimut has not yet generated any LCT-type pegmatite targets elsewhere on its large Galinee project.

Silica rich pegmatite has a lower density than the country rock and Winsome has found gravity a useful tool for defining pegmatite drill targets where overburden obscures outcrop. Comet managed to secure drill permits for its pegmatite outcrops, so if they prove LCT-type (the sampling crew had no LIBS or XRF unit on hand to get a sneak preview), Comet may be drilling in early 2024. The key question for Comet's Liberty property is whether pegmatite emplacement was limited to the Trieste greenstone rocks, which gives Comet about 2.75 km strike potential, or also exploited a structural lineament that projects in a northeasterly direction for 6.5 km on the Liberty property. Comet is part of the 2024 Bottom-Fish Collection. Its Liberty project has an implied value of $12 million compared to Winsome's Adina implied value of $215 million, which itself is a fraction of PMET's $1.4 billion value. It will take some luck for Comet's Liberty to deliver a standalone resource, but there is a very good chance it has sufficient LCT-type pegmatite to deliver whatever shortfall Adina may deliver for Winsome.

Maps showing relative locations of Adina and Liberty Projects

Maps shwoing relative locations of Galinee projects of Azimut and Midland

Disclosure: JK owns shares of Wolfden; Solitario is a Bottom-Fish Spec Value rated Favorite; Comet, Midland and Wolfden are Bottom-Fish Spec Value rated

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch December 6, 2023: If not a Peanut or a PMET then what?

Jim (0:00:00): Why did the market not like Brunswick's Mirage update?

Brunswick Exploration Inc finally published an update for its Mirage project on December 5, 2023, and, not surprisingly, the market decided it was not good enough. It did not help that the spot price of lithium carbonate dropped below $8.00/lb, and that the hedge fund short attack against lithium producers has helped lithium producers drop to their lowest price in a year. Brunswick last provided an update on October 3 when it reported that it had completed 15 holes at Mirage of which 12 intersected spodumene bearing pegmatite intervals up to 52 metres. The company provided no information about drill hole locations nor what additional prospecting had turned up within the 5 km by 20 km northeast trending Mirage property. What the market wanted was a sense of the scale of the Mirage potential, especially in light of the 3 km by 500 m wide field of spodumene boulders as big as 6 metres identified down ice from a 2.7 km corridor of outcrops to the northeast. The update provided this week, however, was confined to a 2 km by 1 km area where the company has completed 36 core holes totaling 5,080 metres. These are shallow holes to a maximum vertical depth of 150 metres. A winterized camp has been established and Brunswick plans to return by mid January to conduct a 15,000 m program during Q1 of 2024.

Assays published for 14 holes indicate that Mirage has three northeast trending dyke sets which the company has labeled the North, Central and South zones (the North zone appears to have 2 dykes). The drilling strategy seems to have involved starting the initial hole under the three main outcrops in this 2 km by 1 km area. Brunswick has published a drill plan outlining the drill hole traces and highlighting spodumene pegmatite intervals. All but 3 holes intersected spodumene bearing pegmatite. It is disappointing that the company decided not to publish azimuth, angle and total hole length information, even for the assayed holes, supposedly because they are afraid potential predators might figure out what Brunswick has at Mirage. The company provided one section for each zone.

Of the first 14 holes all but #13 intersected spodumene bearing pegmatite (the first hole drilled in the South Zone was drilled in the wrong direction but map have nipped some pegmatite and assays are still pending- hole #14 intersected 16.2 m of 2.75% Li2O. Only about 100 m strike of the North Zone was tested with holes 1-4 of which #1 and #2 delivered 24.5 m at 2.18% and 25.8 m of 2.57%, with grades spiking to 3.08%. True width is estimated at 90%. The MR-1 dyke dips to the northwest. Holes 3 and 4 intersected a narrower dyke to the southeast which they call the MR-2 dyke.

Holes 5-12 were drilled along a 300 m segment of the MR-3 dyke and yielded intervals up to 50.6 m grading 1%-2%. MR-3 also strikes northeast but dips to the southeast. Toward the end of the program Brunswick stepped about 500 m northeast close to the boundary of the inlier claims optioned 75% from Osisko Development Corp and drilled holes #28-30 from what appears to be a single drill pad. The map shows spodumene was intersected where you might expect the MR-3 dyke to be, giving it a strike of 750 metres. Hole 35 returned to the main part of MR-3, but the surface projection of the spodumene interval suggests a separate parallel dyke has been intersected.

Assays were reported only for #14 of holes #13-27 drilled into the South Zone which call the MR-4 dyke. This hole yielded 16.2 m of 2.75% Li2O. The MR-4 dyke has been encountered along a strike of 750 m and dips southeast at 45 degrees. Brunswick makes the important statement that similar bonanza grade mineralization has been seen in all the MR-4 dyke holes.

After hole #27 they drilled the #28-30 holes stepping out northeast of the MR-3 dyke for which assays were reported, and then stepped back to the southeast to drill holes 31-32 which intersected spodumene of what looks like a separate dyke that lines up with the dyke encountered by hole #35. But things got really interesting with hole 33 and 36 which have a much greater extent of surface projected spodumene intervals than any of the other 34 holes. They have included these holes in the Central zone, but, thanks to hole #34 which intersected spodumene half way between #33 and the southwestern limit of the South Zone, it looks like #33 and #36 are the continuation of the 2%-3% grading MR-4 dyke.

What does this mean? Is it a Peanut or a PMET? The company states that it has intersected a combined strike length of 1,500 metres, but if you connect some dots it is at least 2,000 m. Just to get a sense of the scale, one can imagine 2,000 m strike by 25 m thickness by 300 m down-dip and 2.6 specific gravity. That gives you a tonnage footprint of 39 million tonnes. That is a lot more than a Peanut, but it also is not close to being a PMET whose CV5 zone yielded 109 million tonnes of 1.42% Li2O based on 163 drill holes representing 56,000 m. Brunswick has only drilled 36 holes for 5,080 metres. The market saw the small area footprint, realized that the 15,000 m program in Q1 of 2024 would be focused on delineating the dyke sets within this area, and while the average grade might prove better than CV5, the tonnage would remain below 50 million tonnes, which the market thinks is Mickey Mouse. In an earlier KW episode I had joked that when Brunswick reveals what it has at Mirage Gina Rinehart would come and eat up Brunswick. But in the KRO Slack Forum we ended up joking that in light of this update Gina would just send her cat to take care of Mickey Mouse.

But one thing puzzled me, namely this statement by Bob Wares: "I believe the distribution of the first four mineralized dikes at Mirage does not explain the three-kilometre-long trend of rich spodumene-bearing boulders that occurs to the southwest. With more outcropping spodumene-bearing dikes located another three kilometres to the northeast, we have considerable exploration work and drilling to do to unlock the full potential of this promising property."

I asked Bob on what basis he made that statement and he explained that the MR 1-4 dykes have high levels of tourmaline and low levels of muscovite, whereas the boulder field that stretches 3 km to the southwest has lots of muscovite and almost no tourmaline. He also pointed out that the abundance and size range of the spodumene crystals in the boulders is very similar to what they are seeing in the core of the MR1 and MR-4 dykes which is running 2%-3%. The difference between the mineralogy of the boulders and the bedrock hosted pegmatites makes it impossible for the MR 1-4 dykes to have been the bedrock source. I then queried him on why he was looking for more potential 3 km to the northeast where apparently they have outcrops? The company's boulder distribution map shows that boots on the ground found the boulders largely concentrated in what appear to be two linear trends within the 3,000 m by 500 m corridor that has the same orientation as the ice direction.

The important news in the Mirage update is that the MR 1-4 dykes have a northeast orientation which happens to be the same as the ice direction. Because the boulder train had the same orientation everybody assumed glacial transport dropped them where they ended up and that the roundedness was due to abrasion as the ice sheet entrains loose boulders and drags them along the bedrock. If the boulder gets into the ice sheet it can be transported hundreds of kilometers. When the ice sheet stops flowing and melts, these boulders called glacial erratics end up sitting on bedrock with completely unrelated geology. AntarcticGlaciers.org has a good publication on Glacial Erratics.

The problem with the ice sheet transport explanation is that the Mirage boulder collection is too uniform and concentrated to have been plucked from bedrock and dragged 5-10 km from their location. I asked Bob if there is any outcrop in the vicinity of the boulders and his response was that this area is completely covered by overburden in which these boulders sit. So the lack of outcropping pegmatite doesn't mean there is no pegmatite in this area. I suggested maybe these boulders are sitting on top of a big pegmatite, one with Greenbushes scale. This pegmatite may have been a ridge which over time got broken up through fractures and then underwent "chemical" weathering courtesy of the freeze-thaw cycle in the James Bay region which would cause the boulders to end up somewhat rounded without ever having been tumbled as happens in shoreline or river systems, or from extensive dragging when stuck in the base of an ice sheet. For an idea of how this in situ weathering happens, check out this Formation of Rounded Boulders Video which one my KRO Slack Forum members tracked down while we were having a discussion about the origin of the Mirage boulder field.

Bob Wares did concede that this was a possibility, and that a glacial expert on their team has suggested the displacement is less than 500 m. He does not like the idea of drilling a fence of scout holes to prospect the bedrock and hope to spear a blind pegmatite, especially given that a key talking point during the past two years has been that Brunswick is only chasing after outcropping pegmatites. But in light of the bonanza grades in the North and South Zone dykes, the similar spodumene crystal distribution within the boulders, the mineralogical difference of the boulders, and the scale of the boulder field, lining up with what appears to be an important structural trend suitable for pegmatite emplacement, it is plausible that the boulder field is sitting on top of its bedrock source. In 2012 when Talison Lithium Ltd owned Greenbushes it reported a resource estimate of 118.4 million tonnes of 2.4% Li2O within a pegmatite body roughly 2,000 m long, 250 m wide and at least 500 m deep. Over the next week or so the company will decide if it will include some boulder field scout holes with the 15,000 m winter program. If neither "Mickey Mouse" nor anything up ice plausibly explains the boulder field, perhaps it is sitting on top of a Green Giant. As it now stands, the market thinks all that will change over the next 6 months is that a resource estimate will emerge for the small North-Central-South area, and that for an outcome of this size the Mirage play is already fully priced. Hopefully they decide to test the Greenbushes in situ hypothesis this winter.

Price Charts for Lithium Producers and Advanced Juniors

Lithium Rock Value Matrix and Price Chart

Peanut, Mickey Mouse, PMET or Green Giant?

Mirage Assay Results

Where did that Boulder Field Come From?

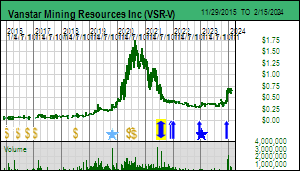

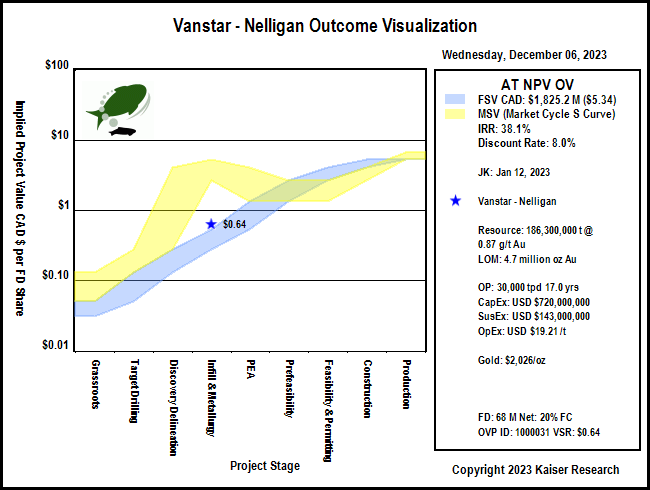

Jim (0:14:02): Why did Vanstar settle for a $0.69 buyout offer from IAMGOLD?

On December 5, 2023 Vanstar Mining Resources Inc announced a friendly buyout deal whereby IAMGold would issue 0.208 IAMGold share per Vanstar share which was valued at $0.69 at Monday's closing price. This disappointed some shareholders who were hoping for a higher price. In KW Episode November 10, 2023 I discussed the company's predicament as the minority stakeholder in the 5.2 million ounce Nelligan gold deposit in Quebec. However, I pointed out that by optioning the Amanda project in the James Bay region to Mosaic Minerals Corp Vanstar could perhaps attract some interim upside if Cygnus Metals Ltd continues to have lithium pegmatite success at its Auclair project which surrounds Amanda, and Mosaic discovers enough LCT-type pegmatite to eventually get Amanda acquired by Cygnus. This farmout deal is now a bad deal for Mosaic because IMG will inherit the Amanda project, and, if it becomes valuable, will decide to keep 50% when Mosaic vests rather than let it earn 80% by delivering a resource estimate before 2030. Since apart from JD Moore Vanstar management does not own much stock, there could be a problem getting shareholder approval for the plan of arrangement, which CEO JC St-Amour thinks could be completed by the end of January 2024. Since there is some overlap between the shareholders of Vanstar and Mosaic, maybe IMG will let Vanstar renegotiate the Amanda deal.

At first I was dismayed by the buyout terms, but on further reflection I have decided it does make sense. The uncertainty about when IMG would push Nelligan into the feasibility demonstration stage qualified Vanstar as part of the 2023 Bottom-Fish Collection and I had confirmed it for the 2024 Collection. IMG has been focused on getting its Cote gold project into production, but when it got wind of Vanstar management's effort to market itself as a buyout target for a royalty company, it initiated discussions. Since 2019 when IMG vested for 75% by delivering a resource estimate it has had the option to carry Vanstar until delivery of a bankable feasibility, at which point IMG's stake would increase to 80% and trigger a right to purchase the 20% interest at fair value based on the BFS numbers. Vanstar would retain an uncapped 2% NSR. So a royalty company had the potential to get a payout for the 20% carried stake plus retain a 2% NSR for the life of the mine whose gold resource is currently 5.2 million ounces and will probably grow over time.

In terms of the rational speculation model, if you accept my outcome visualization for a 30,000 tpd OP mine, the project would be worth CAD $1.8 billion on a 100% basis when ready to start production, which is $5.32 per share for Vanstar based on 20% and 68 million shares fully diluted. But a project stuck at the infill drilling stage has a fair value range of only 5%-10% of the expected outcome value, or $0.27-$0.53 per share. So the deal in rational terms is slightly better than fair value. The risk for Vanstar shareholders is that as Nelligan plods through the feasibility demonstration and permitting trough management might end up diluting the stock to pay the bills and stave off boredom by taking on other projects such as Amanda to generate interim upside. That would not be an issue for a royalty company. But there was a hitch.

The hitch is that at any time IMG could decide to form a 75:25 JV which would kill the option to buy the 20% for fair value and a 2% NSR. CEO JC St-Amour tells me that IMG never threatened to do this, but, given the endless bear market, it makes a lot of sense for a producer to embark on a 5 year economic study cycle, make all the decisions and control the disclosure timeline, and send monthly 25% cash calls to the poor junior partner stuck in the value trough. This risk would also have discouraged a royalty company from buying Vanstar. It is what management had to consider when IMG proposed negotiating an early buyout.

There is an outside chance a royalty company may make a hostile bid at a somewhat higher price, but I would discount that path. IMG has been through a development ordeal at Cote thanks to cost overruns and has had to sell off other projects to keep the development on track. It expects to pour gold in Q1 of 2024. Unless gold soars to the moon IMG will have a hard time recreating itself as a multi-mine producer. In 2024 we may see gold establish $2,000 as a floor rather than a ceiling, and that would boost IMG's price as Cote comes on stream. It would also boost the price of established producers who may move quickly to acquire IMG. The bet Vanstar management is making today is that while an implied $0.69 buyout price is disappointing, by the time the special meeting for the plan of arrangement is held in January and the acquisition is confirmed, possibly by late January, IMG's stock price could be trending higher. Furthermore, the change from dead money Vanstar paper into IMG paper is without capital gain consequences. If the status quo were maintained the risk is that Vanstar stays dead money while producers slug it out for control of IMG, and perhaps take even longer to turn their attention to Nelligan, or worse, declare a 75:25 joint venture where Vanstar's upside gets squashed through dilution funding its 25% stake which nobody but the 75% opertator will ever want to acquire. With this deal Vanstar's destiny has been hitched to IAMGold's destiny.

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch December 1, 2023: Are those green shoots for real?

Jim (0:00:00): How is the end of the year shaping up so far?

Although the capitulation selling is still widespread in the junior resource sector, and as far as I am concerned will continue to the bitter end of December, green shoots are sprouting here and there, suggesting that maybe 2024 will not be a requiem for the Canadian resource junior eco-system. White gold juniors are now getting competition from yellow gold which has breached $2,000 and is raising hopes that maybe this time around $2,000 will become the base rather than the ceiling. The market hope is that the high interest rate policy of the past 18 months has subdued inflation and that the Federal Reserve will begin easing rates next year and avoid a catastrophic recession for the US economy.

Inflation for October came in at 3.2% on an annualized basis, suggesting that inflation is stabilizing just over a point above the Federal Reserve's 2% target rate. General equity markets are creeping higher on the assumption that it is only a matter of time before Jerome Powell starts easing rates. Since late October the US dollar has begun to retreat against most currencies, but the change so far only qualifies as green shoots that a hard frost could easily wipe out. Short term rates (3 month T-bills) are 5.45%, a strong incentive for investors to keep their capital in money market funds, a major problem driving the capitulation selling in Canadian resource juniors. Gold without much corresponding fanfare among gold juniors and majors has quietly clawed its way back above $2,000, but it is too soon to conclude the green shoots we are seeing among beaten up gold juniors in the form of down-trending charts forming a bottom and exhibiting modest uptrends are sustainable.

The GLD ETF still has no visible pattern of net buying. I have assembled collages of all the key metal prices and in most cases there is no sign that the sideways pattern of 2023 is being broken on the upside. Even with gold you have to look very hard to see it. Battery metals are generally trapped in downtrends after experiencing abnormally elevated levels in 2022. The one notable metal exception is uranium, which at $81.38/lb U3O8 is at the highest level since 2008. Although the demand growth dynamics remain weak for uranium, the market loves the optics of a price uptrend. While I see green shoots of a turnaround at the macro level, it is too soon to conclude that 2024 will be a sustained turnaround for resource juniors, especially after Q1 of 2023 looked so strong only to fail massively to the point that Canada's national newspaper is writing an obituary series about the resource juniors.

And yet there are signs that a sub-class of speculators is starting to move into the resource juniors even while existing shareholders remain intent on liquidating the last of their positions. And this is creating an extraordinary bottom-fishing window for me. Every day I am adding juniors to the 2024 Bottom-Fish Collection, and some of them are starting to sprout as they put out news.

One example is Copper Road Resources Inc which I flagged as a bottom-fish for subscribers on October 25 at $0.085 on the premise that the market was woefully undervaluing the upside for pending drill results for the Copper Road project in Ontario, not to mention the big picture potential of a major rethink of the project's district scale copper potential from an IOCG model a decade ago, which a previous owner failed to validate by drilling, into a radical vision that beneath these high grade copper breccia pipes lie alkalic copper-gold porphyry intrusions such as Cadia Hill or Galore Creek, pencil like bodies whose copper-gold grades can improve at depth to support underground mining. This idea is radical because this part of Ontario has seen no intrusive activity since the Grenville orogeny stymied the Mid Continent Rift more than 1 billion years ago.

The drill program late summer did not test the deeper potential, but it tested known breccia pipes in the middle of the 30 km long property which had high grade underground mines operating until the early seventies at the western and eastern ends. The driver behind the radical rethink is Matt Rees, until recently chief geologist for IAMGold. The recent drilling yielded good copper results, but the holes were not deep enough to test the alkalic copper-gold porphyry hypothesis. That will come next year after the company completes a deep IP survey on a property that in its entire history has never had geophysical surveys that penetrate any deeper than 300 metres. On Thursday November 30 Copper Road released drill results which sparked buying of 7.8 million shares up to $0.16 before closing at $0.12. On Friday the stock was knocked back $0.035 to $0.085 on a tenth of Thursday's volume. There is good and bad news in this. The good news is that speculators who understood the bigger picture story stepped into the market and bought a lot of stock. The bad news is that pretty much all of $400,000 worth of flow-thru stock done in August at $0.07 per unit with a Bay Street brokerage firm which just came free trading was blown out into the market. In a sense this is good news for the buyers who did not have the chase the stock too much beyond the price before the news, but of course nobody likes to see their bottom-fish trade cheaper the day after loading up. The question to ask, now that this flow-through paper has been digested, how much stock will be available between here and $0.20?

That this financing was done is a sign of how difficult the resource junior market has become. The key backers behind Copper Road are Rob Cudney, Pat Sheridan Jr and a relative youngster called Jason Libenson. The best they could do during the summer was raise $400,000 flow-through at rock bottom prices from classic Canadian tax avoider flakes. You know things are bad when Rob Cudney can't flail his way out of a wet paper bag. But it is exactly these conditions which are creating the perception that the Canadian resource junior eco-system has crashed through the extinction threshold and is now terminally ill. And yet there was the green shoot buying on Thursday, and as bottom-fishers get their head around the Copper Road story, and start to believe that 2024 is going to be the opposite of a requiem, rather more like a resurrection, at least for resource juniors whose management has its act together and yet is still suffering bottom-fish valuations, the opportunity to load up ultra cheap is extraordinary.

But Copper Road isn't the only example of green shoots sprouting in the dead of winter. On October 4, 2023 I flagged Delta Resources Ltd as a bottom-fish at $0.165 based on its Delta-1 gold project in Ontario near Thunder Bay where drilling has been outlining a gold system that has potential to generate over 1 million ounces of open-pittable and underground mineable gold right next to a highway. The stock attracted strong market interest and funding in H1 of 2023 based on drilling that intersected high grade shoots within the shear structure. But when the drill marched past a fault it encountered lower grade mineralization, whose results came out just as a $10 million financing done at $0.45 for hard dollars and $0.63 for flow-through came free trading. This financing was brokered by at least 3 Canadian brokerage firms, and, no surprise, the stock got clobbered. Even though Delta has over $5 million working capital, an emerging gold discovery, and a potential VMS spinout property in Quebec it unimaginatively calls Delta-2 should a future resource estimate attract a buyout offer from a producer, the stock in the past month had sunk to $0.09 amid relentless capitulation and tax loss selling.