Hello Guest User, You are visiting this website from a computer with an IP address of 172.69.59.32 with the name of '?' since Sat Apr 27, 2024 at 4:53:11 PM PT for approx. 0 minutes now.

Kaiser Media Watch Blog - October 1, 2023 to October 31, 2023

KRO Blog Overview

The KRO Blog is where unrestricted content of a time sensitive nature is posted. It includes the Kaiser Media Watch Blog which features content involving John Kaiser produced by third parties such as the Discovery Watch series by HoweStreet.com, interviews by outfits such as Investing News Network, SDLRC related commentary, the KRO Monthly Summaries, and just about anything else John writes that is not intended exclusively for the fee based KRO Membership.

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch October 27, 2023: What does SQM's Azure bid mean for James Bay?

Jim (0:00:00): Why is Azure Minerals such an interesting story?

ASX-listed Azure Minerals Ltd came to my attention last week when it was halted on October 23 for an announcement on Monday that management had accepted a takeover bid from SQM, the Chilean producer of lithium from brines. I remembered Azure as one of the few ASX-listed juniors from the past decade that would exhibit at North American conferences while it was advancing a couple Mexican epithermal gold plays. By mid 2020 the market had lost interest in the Mexican projects and the stock was limping along just below $0.10. On July 17, 2020 Azure did a deal to acquire 4 projects in Western Australia's Pilbara region from Mark Creasy, the legendary Australian prospector. One of these was the Andover nickel-copper play near the coast just east of Karratha and south of Roebourne. The other 3 were gold plays of which the most interesting was Turner River which is in the area where De Grey Mining Ltdd made the Hemi gold discovery in 2020 by grid drilling shallow holes. Mark Creasy received 40 million shares and retained a 40% stake in Andover and a 30% stake in the gold projects.

The Azure story is very interesting because while the Australians were embracing Lithium Mania 2.0 with a focus on the emerging Corvette discovery of Patriot Battery Metals Ltd in the James Bay region of Quebec in Canada, they were ignoring a major emerging lithium discovery in their own backyard. Lithium Mania 1.0 kicked off in 2015 when the market started to notice the success Tesla was having with its electric vehicles. While Canadian resource juniors flocked to the Lithium Triangle of South America where SQM had long been the dominant producer from the lithium brines beneath the salars, Australian juniors flocked to exposed basement parts of the Pilbara and Yilgarn cratons in Western Australia where pegmatites had been documented ages ago. Most of the Pilbara craton is buried beneath the younger rocks of the Hamersley Basin which is a major producer of iron. But in the exposed area south of Port Hedland there emerged two world class lithium pegmatite mines, Pilgangoora controlled 100% by Pilbara Minerals Ltd, and Wodgina controlled 40% by Mineral Resources Ltd and 60% by Albemarle. The exposed western part of the Pilbara was dominated by precious and base metals exploration, most notably by Novo Resources Corp which developed the Wits 2.0 conglomerate gold play in 2016-2018 that was subsequently eclipsed by De Grey's discovery of 10 million plus ounces of conventional hydrothermally emplaced gold at Mallina.

The prevailing assumption within Australia seemed to be that its juniors had harvested all the low hanging pegmatite fruit in Australia as part of Lithium Mania 1.0, and the new frontiers for Lithium Mania 2.0 were the Archean cratons of Canada and Brazil, and Africa if one dared. Lithium Mania 2.0 emerged in 2021 when it became clear that the car makers had fully embraced EV deployment, the supply imbalance created by the productivity of Australian pegmatite mine developers reversed, and groups like the IEA started projecting a 600% increase in lithium supply by 2030 if EV deployment goals required for 2050 net zero emission goals are to be met. In 2023 Toyota announced a manufacturing cost breakthrough for solid state lithium ion batteries which allow lithium metal to be used in the anode instead of graphite without the problem of dendrite growth which can cause shorts and the dreaded thermal runaway that turns EVs into firebombs. The initial skepticism that the holy grail of the EV sector has been found is shifting to profound optimism, as indicated by this Financial Times October 27, 2023 Big Read: How solid state batteries could transform transport. If this is the coming reality, the world will need 1,200% more lithium supply than the 130,000 tonnes of lithium metal produced in 2022, and lithium will almost certainly become a $100-$200 billion annual market during 2030-2040.

Azure Minerals focused its initial efforts at Andover on delineating a couple small nickel-copper deposits for which an initial JORC estimate was delivered in March 2022 and updated again in 2023. In May 2022 Azure sold the Mexican projects for AUD $10 million cash and $10 million worth of stock in a private company that plans to secure a listing on a Canadian exchange. While Azure continued to explore Andover for nickel-copper zones, a separate exploration team in April 2022 started mapping and sampling outcropping pegmatites. Azure finally reported in October 2022 that it had outlined a swarm of 700 lithium mineralized outcrops within a 4 km by 9 km corridor that also contained the nickel-copper zones. Azure even mentioned that a hole testing a VTEM target for nickel had intersected spodumene. The nickel-copper zones are older than the pegmatites, but both seem to have exploited a structural zone of weakness within the Andover intrusion. The nickel-copper story had helped Azure get to the $0.40 level but by late 2022, despite this revelation and all the buzz about what PMET was accomplishing in Canada's James Bay region with pegmatite within what was once a Virginia greenstone belt gold play, the price had sagged back to about $0.20 by the end of 2022.

Australian investors ignored this lithium development which occurred in the middle of an area Quinton Hennigh had briefly made famous with Novo's Wits 2.0 gold in conglomerate play. SQM, however, was paying attention and approached Azure with a proposal to invest $20 million at $0.26 to secure a 19.9% equity stake which Azure accepted in January of 2023. The market remained unimpressed, even though SQM is a 50:50 partner in the Mt Holland project with Wesfarmers which acquired its stake by paying $776 million in 2019 to acquire Kidman Resources Ltd even as the chill of lithium winter was bringing Lithium Mania 1.0 to an end.

On February 13, 2023 Azure finally reported the assays for the pegmatite interval in the nickel hole, 7.2 m of 1.52% Li2O. That still didn't do much for the stock. In February 2023 they started drilling Target Area 1. On March 15 they reported visuals for the first two lithium focused holes (second graphic). After the May 10 RIU conference where Azure showed some "spodumene" drill section photos the volume began to pick up. On May 31 Azure adds two RC rigs to the 2 core rigs in an effort to speed up "mapping" the pegmatites.

On June 12, 2023 Azure published assays that included 105.0 m @ 1.26% Li20 (including 22.8m @ 3.57% Li20) and all hell broke out as the Australians rushed back home even as a short seller published a report denigrating the resource potential of CV5 (wrong - see KW Episode August 2, 2023) and highlighting the seedier aspects of Canadian marketing methods (cringe). On August 14 in response to ASX pressure about market speculation Azure put out news that on July 12 it had received a non-binding offer at $2.31 from SQM which Azure rejected. Adjusting for the 60% project interest and the 400 million shares fully diluted, this implied a value of AUD $1.6 billion on a 100% basis. On August 22 Azure raised $120 million at $2.40.

On October 25, after being halted on Monday October 20, Azure announced that it had accepted a binding offer from SQM at $3.52 per share which prices Andover at AUD $2.4 billion (Mark Creasy is going to likely get a wonderful payday for his 40% whose implied value is $960 million). The only conditional is that Foreign Investment Review Board (FIRB) needs to approve the takeover. Gina Rinehart, who from June 29 thru October 17 had bought 21,509,214 shares in the market, buys 53,979,114 shares at $3.50 the day trading resumes (Oct 26), and another 6,073,886 on October 27 when she files a substantial shareholder report disclosing that she owns 81,562,214 shares (18.3%).

The SQM bid has 2 components. The $3.52 offer is the plan of arrangement type Albemarle tried with Liontown which required approval from 75% of votes cast for the $3.00 offer which Gina's 19.9% Liontown stake was large enough to de facto block, so Albemarle walked away. That was bad news for shareholders who didn't sell, because Liontown subsequently did a deeply discounted equity financing as a part of a major financing to make sure Kathleen Valley is funded to production by mid 2024. On paper Gina Rinehart took a $400 million bath on what may be a temporary queen's gambit sacrifice (see KW Episode October 20, 2023). Last week I was not sure I was correct about my speculation that Gina is on the warpath to secure a major stake in a future lithium market that will be in the $100-$200 billion annual value range. But her decision to step into Azure with a major equity stake in a project that won't be in production until about 2030, probably later than PMET's CV5 deposit in James Bay, and where the takeover structure is more nuanced that with the Liontown-Albemarle bid, convinces me that Australia's richest citizen is dead serious, and is going to leave Australia's iron men sitting on the fence picking their noses.

The Azure situation is more complicated because SQM also has a takeover offer at $3.50 which does not require shareholder approval. If I understand this correctly, assuming no FIRB objection, SQM can buy everything that comes out at $3.50 while Gina has to stop at 19.9%. If nobody else steps in with a superior bid, SQM could end up in an 80:20 JV with Gina. But that is for only 60% of Andover, with Mark Creasy owning the other 40%. No doubt he is in talks with SQM and Gina about selling his stake because as a private party he can do whatever he wants unless there is a right of first refusal held by Azure which I have not spotted as a disclosure and is not something Creasy would likely have tolerated. If it does exist, and Gina is willing to a higher implied project value (on a 100% basis) for Creasy's 40%, SQM may have to boost its Azure bid and thus secure for Gina a short term trading profit. The problem for SQM is that if Gina scoops Creasy's 40%, SQM's 80% of 60% is 48%, though that may be fine for SQM because at this stage Gina's Hancock Prospecting will have to acquire in house lithium expertise if she is indeed bent on owning part of the lithium supply future.

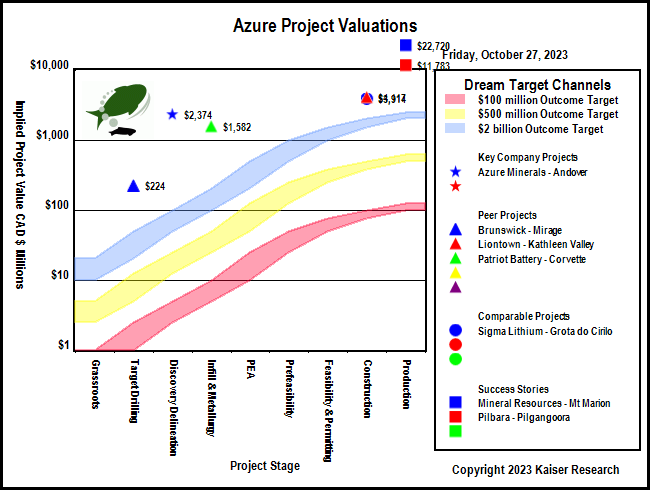

Why is this so interesting? It is monstrously interesting because this takeover drama is unfolding before there is even a maiden resource estimate, and this has interesting for the sleepy Canadians who are shunning Lithium Mania 2.0. On October 17 Azure published a new presentation which declares an exploration target of 100-240 million tonnes of 1.0%-1.5% Li2O for 3 target areas. A 100,000 m drill program using both RC and core rigs is underway and a maiden resource estimate is expected in Q1 of 2024. This is amazing because 1 year ago this was a crappy nickel-copper play pumped as a battery story with a feeble resource estimate. A year later SQM is prepared to pay $1.4 billion cash for 60% of a property whose swarm of pegmatites Quinton Hennigh and I probably drove over in 2016 when he gave me a site tour of the region and its Wits 2.0 gold story. And Australia's richest person has bought an 18.3% stake in the open market at close to that valuation. This is absolutely stunning!

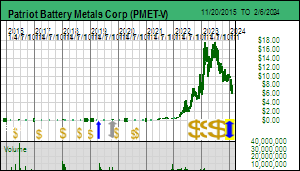

In August Patriot Battery Metals reported a maiden resource estimate of 109 million tonnes of 1.42% Li2O for the CV5 zone within the Corvette project in the James Bay region. The 55 km trend has multiple LCT type outcrops and plausibly shares the same 100-240 million tonne exploration target range as Azure's Andover project. When Albemarle invested $109 million in PMET stock for a 4.9% equity stake it priced PMET at CAD $2.3 billion. Corvette is at least a year ahead of Andover. The aggressive nature of SQM's bid and Gina Rinehart's willingness to get close to a 19.9% stake at the implied AUD $2.4 billion. SQM's only other hardrock lithium exposure is the Mt Holland project where Wesfarmers is the 50% partner after buying out the Australian junior that discovered the deposit. The Chilean government is trying to grind a bigger state share of Chile's lithium portion of the Lithium Triangle, an excellent recipe for fast track supply mobilization. SQM and Albemarle are the primary non-Chinese producers of lithium for the EV sector. Are they going to let the lithium supply future end up being dominated by others? What if Rio Tinto, BHP, Anglo, Glencore and Vale wake up? PMET is currently priced at about $1.5 billion, more advanced than Azure with a similar expansion potential footprint, but only two-thirds the value. PMET is now a sitting duck for a takeover battle. And watch out if Gina Rinehart notices what is happening in Canada's James Bay region.

Whether or not my speculations about the likes of SQM, Albemarle and Hancock turning their attention to the emerging lithium discoveries in Canada's James Bay region prove correct, the most important aspect of the Azure story is that there may be a lot more left to find in Australia than is assumed. The very way the Australians ignored the news flow from Azure about Andover, news flow that North American audiences are starting to appreciate with regard to Canadian lithium pegmatite plays, tells us that the Australian mindset has shifted to seeing greener pastures abroad. For North American investors there may be a Canadian listed opportunity in the form of Quinton Hennigh's Novo Resources Corp which continues to be a substantial landholder on the Pilbara craton, especially the western part where Andover is located. It is also an opportunity for Australian investors because Novo recently secured a dual ASX listing. Despite having a property next door to Azure's Andover project, Novo is crawling along the bottom and may not even qualify for a bottom-fish spec value designation. Why? Because Novo is backed by people like Eric Sprott and Backhoe Bob who are right wing gold bugs not keen about the energy transition. Unlike Gina Rinehart who is a Trumper but not when it comes to assessing business opportunities, these folks are just plain ideologues. The corporate presentation on Novo's web site has a slide which highlights the properties in the West Pilbara and notes that a "divestment process is underway" for the tenements that have "battery" potential. WTF?

Back in 2017 this region was the focus of Novo's Wits 2.0 play, the hypothesis that the gold nuggets fossickers were finding with metal detectors originated from a thin conglomerate bed sitting between the 3 billion plus year old Pilbara Craton and the slightly younger Mt Roe flood basalt that covered everything except a 10-50 km strip between the coast and the edge of the basalt. The steady erosion of the basalt had over time exposed the conglomerate bed whose gold nuggets spilled into the overburden and with rising and falling sea levels got reworked into marine terrace deposits on the basement beyond the edge of the Mt Roe wedge. Quinton Hennigh's hypothesis was that these nuggets were laterally extensive within these conglomerate beds as they are in the Witwatersrand Basin in South Africa. The prevailing view is that the Wits 1.0 gold endowment formed when gold precipitated out of seawater as the first forms of organic life, blue algae, blossomed in shallow lagoons and started emitting oxygen which changed the chemistry of the water. The difference between Wits 1.0 and Wits 2.0 is that the detrital gold grains from Wits 1.0 have the thickness of a hair whereas those in the northern Pilbara were placer style nuggets often the size and shape of watermelon seeds.

In South Africa when you drill through a 1-2 m Wits 1.0 horizon it yields a consistent high grade gold assay because the gold is fine and distributed evenly throughout the horizon. Drilling in the Pilbara had never encountered such gold grades within the conglomerate at the unconformity between Pilbara basement and Mt Roe basalt. The nuggets in the Pilbara craton flats were dismissed as an exotic novelty with no commercial source. Quinton proposed that something similar to Wits 1.0 but also different was going on during the algae cycle in the Pilbara area which caused nuggets to form rather than fine grains that rolled around on the sea floor and abraded their edges to make them look like placer gold. Furthermore, this took place on a systematic large scale. The reason it was not found before was because it is hard to intersect a nugget with drill core. The Wits 2.0 hypothesis was that an enormous gold endowment was embedded within the thin conglomerate bed between the older Pilbara basement and the younger Mt Roe basalt which preserved these beds. Novo staked or acquired all the land straddling the edge of the Mt Roe basalt. The story foundered when it became clear that a resource could only be established with bulk samples which needed to be on a scale of 100,000 tonnes. Under Australian permitting rules that was equivalent to mining which could only be done with the support of a JORC resource estimate. This became a Catch-22 problem because without a large bulk sample Novo could not deliver a JORC resource estimate.

The story died because there was never an explanation for how "nuggets" formed in the quiet lagoons as a result of precipitation from seawater which begins at a microscopic scale. Wits 1.0 has no nuggets, just tiny grains the width of a hair whose edges have been rounded off. Eventually even Quinton Hennigh concluded that these Pilbara nuggets formed from conventional hydrothermally emplaced gold deposits from which they eroded and ended up in these conglomerate beds as is the case on the coast of Alaska and lots of other paleoplacer settings. This killed the Wits 2.0 story which hinged on the idea that the nugget distribution was laterally systematic from lagoon precipitation rather than following some localized river delta pattern emanating from a pinpoint source. Backhoe Bob's vision of just start mining the thin edge of the wedge would have ended up in bankruptcy. Ironically De Grey found such basement hosted gold deposits within the Pilbara craton in 2020 and emerged from the penny gutter to its current trading range between $1-$2 where its 1.5 billion shares give its Mallina project a $2 billion value. Novo has even formed a joint venture with De Grey.

The Azure folks were also initially only interested in the nickel-copper style "battery metals" associated with Andover intrusion. But the team headed by chairman Brian Thomas and managing director Tony Rovira were scientists, not ideologues, and diverted capital to assess this lithium pegmatite potential that was barely visible in the reddish landscape and historically ignored because as recently as 2005 the value of the annual lithium market limped along at around $200 million, far cry from the 1,000 times bigger potential $200 billion future annual market value. This is the story now unfolding on Canada's cratons, and other cratons such as in Scandinavia and Brazil, where pegmatite outcrops were viewed as places to have lunch away from insects. It may be that Quinton Hennigh has already secretly assessed all Novo's Pilbara holdings and concluded there is no LCT-type potential, and is plotting to dump the critical mineral rights onto some sucker group. But until we hear that from Novo management it might be foolish to assume that the Andover intrusion is just a local LCT-type pegmatite freak show which the ever clever Mark Creasy staked for nickel-copper and managed to grab only that part of the intrusion with pegmatite potential, while the Canadian chumps staked the western portion which just had pathetic nickel-copper potential. My gut, however, is that even though Novo's staking strategy was guided by the Wits 2.0 hypothesis, its vastness could very well have captured all sorts of LCT type pegmatite potential obscured by the red landscape. We shall see.

The complex gold and lithium dynamics of the West Pilbara

Chart showing major news events for Azure Minerals

Andover and Ridgeline Ni-Cu Resources

Andover Pegmatite Distribution & Exploration Target Scale

Example of how initial assays improve once the geometry gets sorted out

Beware Novo's plan to ditch energy transition related upside

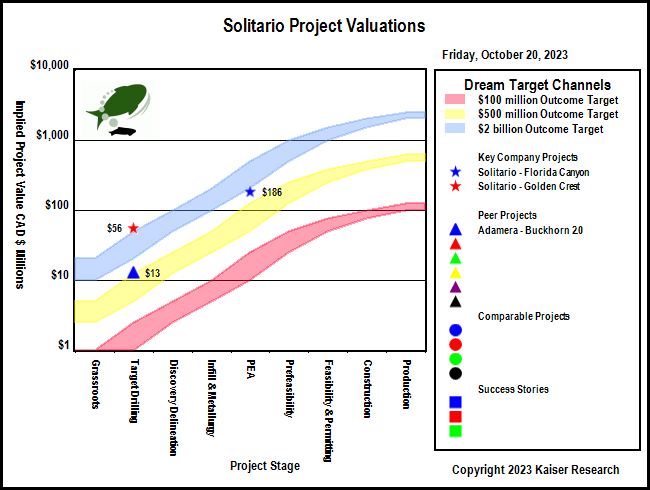

IPV Chart for Azure's Andover and similar projects

Jim (0:19:02): Anything new with the James Bay lithium area play?

The James Bay Lithium Index, which now has 70 members, had a good week, managing to close up modestly every day, but it is still down 23.3% from August 1, 2023 when I created it. Lithium Mania 2.0 has by no means caught on with general audiences. The lithium carbonate price weakened this week again as more bad economic news emanated from China which retaliated against western moves to limit export dumping of state subsidized electric vehicles by declaring export restrictions for natural and synthetic graphite. This is really a warning shot about potential measures that would be much more drastic for car makers outside China. While China dominates in graphite production from natural sources, and making synthetic graphite from hydrocarbon sources, the rest of the world could easily ramp up synthetic production from hydrocarbons, especially the United States. But because China is the lowest cost jurisdiction (don't mention the downstream victims of lousy emission and worker safety standards), everybody is happy to import cheap Chinese graphite. The same applies to gallium and germanium whose export China has also restricted; the way to strip gallium from bauxite conversion to alumina and germanium from zinc smelters is present outside China when the will to do so develops.

Rare earths are another matter, but apart from Japan, what non-Chinese nation makes the rare earth based magnets required for electric vehicles? China exports magnets made from its super-abundance of rare earths, and it is unlikely China will curtail the export of a value added down stream product. However, if supply curtailment turns out to be not China's explicit choice, but rather a functional by-product of western reaction to Chinese aggression such as trying to annex Taiwan or becoming more overt in supporting Iran's proxy war against Israel and Russia's invasion of Ukraine, then Global West car makers will have a problem. And everybody has their heads in the sand about the future rare earth supply problem. Not so, however, about the future lithium supply problem. Although Goldman Sachs thinks China will become a limitless supply of cheap lithium, nobody else does. The corporate takeover actions of major lithium suppliers like Albemarle and SQM in Australia signal that nobody believes China will own global supply for lithium as it does for rare earths, antimony, graphite, and tungsten. China's stranglehold on lithium today involves downstream refining of spodumene concentrates into battery grade lithium hydroxide and carbonate. This vulnerability, however, is well understood, and so it only takes an abundance of will to harness the existing way into conversion capacity outside China.

The scramble afoot now is to secure the future lithium supply needed for an EV sector on an unstoppable track to displace ICE cars. Nothing highlights this more than SQM's decision to try to buy out Azure Minerals Ltd for the astronomical implied amount of AUD $2.4 billion before Azure even has a maiden resource estimate for its Andover pegmatite field which nobody knew about until just over a year ago. Meanwhile, Patriot Battery Metals Corp, which had a similar implied value for its CV5 maiden resource and on trend expansion potential when Albemarle invested CAD $109 million to acquire a 4.9% equity stake in August, is bumbling along at a value of about CAD $1.6 billion. Is this a Prime Minister NoCanDo discount being applied to Canadian resource projects? Gina Rinehart has injected complexity into SQM's straight forward bid for Azure's 60% stake because Mark Creasy, owner of 40%, represents a wild card. However that plays out, what matters is that Gina is no longer just looking at near term production assets, but is also looking at emerging pegmatite lithium discovery plays with world class footprints, discoveries that will not come into production before 2030. Gina Rinehart now personifies the vision of lithium supply becoming a $100-$200 billion market in the 2030's, not as big as iron, but rivaling copper and aluminum, and gold if you want to include useless metals. The iron lady is brushing aside the iron men as if they were mere tin men from the land of Oz.

Next week is important for the James Bay juniors because the AEMQ will hold its annual mining and exploration XPLOR 2023 conference in Montreal from October 30 through November 2. Only 8 James Bay Lithium Index members are exhibiting, but I am sure representatives of all the serious juniors will be present to network and sponge up information. Hopefully government officials will be plugged into what is happening in the James Bay region. The Abitibi greenstone belt activity at this stage is largely a mechanical process which cynics might even dismiss as lifestyle activity. There is zero buzz about Quebec's gold potential. Nor does anybody care about base metal projects. The buzz is all about Quebec's lithium potential, with anxiety focusing on what stance Quebec's First Nations will ultimately take about the development boom in their backyard, and to what Canada's Prime Reconciliation Minister will do to stymie mine exploration and development.

This conference I wish I were attending so that I could take the pulse about the will to turn Quebec into a critical supplier of the lithium needs of the energy transition. The ones I attended during the past decade were fun while held in Quebec City, because they had the cozy feel from when PDAC took place in the Royal York and Roundup in Hotel Vancouver. But the later ones in Montreal were held in this dreary Soviet style concrete dungeon attended by very few delegates, though the low attendance was because the resource junior bear market had extended well beyond the usual 2-3 years of gloom. Attendance was so sparse in 2015 I got to hang out with the Osisko gang (and discover why all these new Osisko juniors were named after scotch brands) which enabled me to have a chat with Bob Wares. I had noted unusual zinc-lead-silver assays coming out of the Hermosa-Taylor project of Arizona Mining, and because Bob was a director we started chatting about it. Based on that happenstance conversation I took a closer look at it, tagged it as a $0.35 bottom-fish for the 2016 collection, and, after I met Don Taylor at the VRIC conference in January 2016 who walked me through the geological story, I turned it into a major recommendation whose $2.2 billion South32 buyout outcome at $6.25 I accurately projected with the help of my rational speculation model, outcome visualization method, and IPV charts. That was so long ago.

Lithium Mania 2.0 was premised on the idea that after the Canadian awakening in 2022 about the world's future lithium supply needs the summer of 2023 would be the most intense "boots on the ground" prospecting season in the history of Canadian exploration. Alas, nobody foresaw that in 2023 Canada would go up in smoke. The most depressing moment for me this year was that weekend in early June when word got out that most of Quebec had been closed to exploration due to unprecedented forest fires. Not only were vast regions closed for safety reasons, but all air transport equipment such as helicopters were requisitioned to support fighting fires in the vicinity of threatened communities. This was not something on could complain about. It was a shot from left field that had to be absorbed. The James Bay region lost two critical prospecting months, and in many areas even August was not accessible. Most juniors got boots on the ground in early September, but many of them had to cease work on September 15, the beginning of the Cree moose hunting season which runs until October 15.

As a result only a handful of juniors are currently drilling pegmatite targets, and only a handful have done enough target development work to justify mobilizing a drill program in Q1 of 2023. Not much gets done during Q2 in the James Bay region other than wrapping up drill programs because spring thaw is a nasty, foggy time of the year, and May is the Cree goose hunting season. Work does not resume until late May when the fog has dissipated and the ground is exposed for prospecting. But within several days of prospecting kickoff in 2023 all field crews were called home to sit out most of the summer. The only consolation emerging from the lost 2023 exploration season is that so much forest burned that 1) not much is left to catch fire in 2024 if we get the same intense conditions, and, 2) a lot of otherwise hidden outcrop will be exposed after the spring rains have washed away the soot. In rugged terrains like northern British Columbia the retreating glaciers give prospectors fresh hope to discover newly exposed goodies, but the glacial retreat is of an incremental upslope nature. The vegetation "retreat" caused by the 2023 forest fires will be laterally monumental. I might add that a third consolation is that all those people who felt they missed the boat will have in fact missed only a very few boats. One I think they will have missed which I introduced in Q2 of 2022 is Brunswick Exploration Inc which has done sufficient work to shortly be in a position to lift off in the manner Azure Minerals did in June 2023.

On September 7, 2023 Brunswick Exploration Inc announced that it had started a 5,000 m drill program at its Mirage project. On October 3 Brunswick reported that it had drilled 1,000 m representing 15 holes of which 12 had intersected spodumene bearing pegmatites up to 52 m in width. A big question with pegmatite outcrops is the orientation and extent of the bodies beneath the surface. "True width" talk is not allowed until drilling has sorted out the geometry. Brunswick indicated assays would be available in the second half of October. Brunswick, unlike Azure, has not been overly helpful with providing graphics to help shareholders understand what is unfolding. KW Episode October 6, 2023 is the most recent discussion about what might be going on at Mirage. An update early next week ahead of the XPLOR conference in Montreal is reasonable to expect. Mirage has the scale to be comparable to Azure's Andover pegmatite field. If Gina Rinehart knows about Canada, and Brunswick delivers evidence that Mirage is a major emerging lithium discovery, be prepared to hold onto your hat. We already know Albemarle knows about Canada. The real question is whether or not SQM also knows about Canada. SQM so far is missing in action as far as Canada is concerned, but SQM did have a booth at PDAC this year along with Albemarle. In light of what happened with Azure Minerals the past week, do not be surprised if positive news from Brunswick about Mirage lights a fire under the James Bay Great Canadian Area Play.

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch October 20, 2023: A queen's gambit or a $400 million bath?

Jim (0:00:00): After Albemarle withdrew its $6.6 billion bid for Liontown on Monday, the company undertook an equity financing at a 36% discount to last week's closing price which caused Gina Rinehart to take a $400 million bath on her 19.9% stake. Was that part of the plan?

Liontown Resources Ltd was halted on Monday October 16, 2023 after Albemarle announced that it was formally withdrawing it non-binding offer to purchase Liontown at AUD $3.00 per share which is about AUD $6.6 billion or USD $4.3 billion. KW Episode October 13, 2023 described the drama created by Gina Rinehart accumulating 19.9% of Liontown's issued stock. Albemarle had spent just over a month conducting due diligence and did not indicate any reason for the decision other than "noting "growing complexities associated with the proposed transaction as a factor in its decision". The complexity was the announcement on October 12 by Gina Rinehart that the 180 or so subsidiaries of Hancock Prospecting Pty Ltd had purchased 19.9% of Liontown's 2.2 billion issued stock at a price close to Albemarle's "final offer" of $3 per share. Under Australian law if a purchaser exceeds 19.9% it must make a bid for the entire company. As I discussed in last week's KW Episode, Hancock first disclosed having a substantial 7.72% position last April when Liontown made public the second private overture Albemarle had made in the prior 12 months. When Liontown agreed to open its books in early September for a 30 day due diligence period after Albemarle made a final $3 offer that was not binding, Gina stepped up her buying activity, most of which took place close to the $3 offer price.

The threat this presented to Albemarle was that the acquisition, if it decided to make it biding, would require a shareholder approval vote of 75% of votes cast. If Gina chose to vote her 19.9% against the deal, at least 1.3 billion shares or 60% would have to be voted yes, more if there were other shareholders casting no votes. Liontown management would have a hard time getting enough yes votes cast to pass the deal. With a vote likely a waste of time and money Albemarle had no choice but to withdraw.

The big question is what would cause Gina to vote in favor of the acquisition? Since the cost base of her position is close to the acquisition price, there are only two rational objectives for her to have. One is to grind a higher price from Albemarle, which would hurt Albemarle's market credibility. If she got a 10%-20% boost out of Albemarle that would be a tidy short term profit. But the risk that Albemarle might walk away was high, so it makes no sense that Gina's goal was to extort a short profit.

The other rational goal is that Gina did not want Albemarle to acquire Liontown whose Kathleen Valley is the only large Australian lithium pegmatite deposit going into production within a year that is owned by an independent pre-production company. Was the reason some sort of Australian patriotism to keep Kathleen Valley out of the hands of another foreign company? That may be a reason but it would not be the reason. The most obvious goal would be that Gina has a plan to make hardrock lithium production a counterpart to Hancock's iron mining business. That makes a lot of sense if you believe lithium demand will grow 600%-1,200% by 2035 and become a $200 billion annual market in the same league as gold and copper production.

Gina won the battle to keep Liontown out of the hands of Albemarle, but ended up taking a $400 million bath when Liontown used the trading halt to secure a AUD $365 million equity financing with institutions at $1.80, which was a 36% discount to Friday's $2.79 closing price. When trading resumed on Friday October 20, 2023 the stock traded 54 million shares to close at $1.90. Liowntown also secured a $760 million debt financing package which partly refinances an existing debt facility and with the equity financing allows Liontown to complete construction with production projected in Q3 of 2024. Non-institutional shareholders will be eligible to participate in a share purchase plan to buy up to $30,000 each at $1.80 for a total of $45 million. I'm not sure if Gina's 180 subsidiaries each qualiy as an eligible shareholder, but if they do she can only buy about 3 million shares for $5.4 million. If she buys no stock her position drops to 18.2% after the equity financings.

Does Gina simply like expensive baths, or has she in effect played a queen's gambit opening? If her goal is to ultimately own 100% of Liontown, she has a year to make her move in the form of a hostile unconditional all cash offer which may end up being less than what Albemarle was prepared to offer. It is possible that Albemarle might come back with a higher bid if Hancock does make a bid, but the Foreign Investment Review Board might be an obstacle. The queen may have taken an expensive bath, but the gambit hands her control of Liontown's destiny unless Pilbara Minerals or Mineral Resources make paper bids for Liontown.

Graphic showing how Kathleen Valley compares to other lithium deposits

Timeline Path to Production for Kathleen Valley

Liontown's Offtake deals with LG, Tesla and Ford

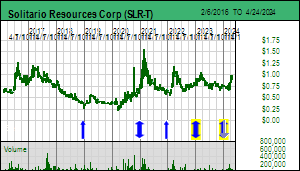

Jim (0:12:01): Any permitting breakthrough yet for Solitario Resources?

Solitario Resources Corp is still waiting for the US Forest Service to publish a "finding of no significant impact" (FONSI) for the Golden Crest plan of operations Solitario first filed in February 2022. CEO Chris Herald had hoped to reach this milestone by the third week of August because that would still allow time to mobilize a drill program in Q4 of 2023. Once the USFS publishes a FONSI it kicks off a two month period that allows the public to comment on the FONSI and the USFS is required to defend its decision. Since the permit application is only for a drilling program, not developing a mine, the FONSI usually survives the comment period. But with October more than half over there will be no drill program until May of 2024 due to winter conditions in South Dakota. The urgency around the drill permit is now gone, though getting the FONSI tomorrow and surviving the two month comment period would still be a welcome development. It has been almost two years since Solitario applied for a drill permit, a ridiculously long time, and shareholders are beginning to wonder if a permit might never be granted.

On October 13, 2023 Solitario announced that it had raised USD $4,747,500 at USD $0.55 with non-US investors. This follows an August 2 announcement that Newmont had invested USD $2.5 million by purchasing 4,166,667 shares at $0.60 bringing its stake to 9.95%. The latest financing boosts working capital to about USD $9.5 million with 77.6 million issued and 87.2 million fully diluted. About 80% of the latest financing was taken down by a Canadian institution which had conducted due diligence for the past couple months. Apparently this is a serious institutional investor with the capacity to invest more down the road.

Solitario is two stories in one package. It has a 30% carried interest in the Florida Canyon zinc-lead-silver project in Peru where Nexa is conducting a prefeasibility study for an underground mining operation. If you go by the rule of thumb that NPV must match or exceed CapEx, and assume Florida Canyon will have a CapEx of USD $350 million, Solitario's 30% share would be USD $105 million which based on 87.2 million fully diluted would be worth USD $1.20 per share. The uncertainty is the timing of a decision by Nexa to buy out Solitario's 30% stake, but if you adopt a two year time horizon and double the current USD $0.55 stock price that is a good worst case scenario return.

The best case scenario, however, is the second story, namely Golden Crest which I described in Tracker December 20, 2022. Golden Crest covers the northwestern portion of the Black Hills region opposite of the area which has yielded over 90 million gold ounces from the Homestake mine and the Wharf and Gilt Edge open pit mines. The 14,000 hectare Golden Crest property covers a limestone plateau that has very little evidence of past exploration. Homestake drilled 3 holes through the younger sedimentary rock package into the Precambrian basement back in the 1980s and confirmed that the formation which hosts the Homestake deposit is present in two holes but never did any followup exploration. The rocks at surface are younger than the ones that host the Wharf deposit and it was assumed that if any gold mineralization is present it would under barren cover. But Solitario started exploring in 2021 the company was amazed to discover discrete zones og gold mineralization at surface. Although it cannot yet drill any holes, Solitario has been free to conduct surface prospecting and channel sampling during the past couple years, and some time before the end of this year will publish a update. They have now unearthed evidence of a powerful hydrothermal thermal system with a 40 sq km lateral footprint covering a 200 m thick package of receptive carbonates. That this was overlooked by the prospectors of yore is a mystery.

Golden Crest is the last American frontier wehre a massive gold discovery not hidden by barren cover rocks or gravel can still be made. The scale is such that Solitario now has a couple additional plan of operation applications underway covering new areas of mineralization distinct from the targets covered by the 2022 application. Once Solitario starts drilling it can target 3 types of deposit: the banded iron formation hosted type such as Homestake in the basement rocks, the Deadwood formation sediments that host the Tertiary aged Wharf system, and the overlying Mission Canyon limestone missing in the Wharf area but at whose surface Solitario has encountered high grade values. Finding a Homestake style deposit in the basement rocks between 300-500 m depth might seem like a longshot, if any such deposit outcropped before the sediments buried the basement, they may have formed placer deposits as happened in the vicinity of Homestake. If Solitario encountered a thin veneer of paleoplacer gold it could use those intersections to vector towards the source. The bluesky is that Golden Crest is a mirror image of the Homestake district, which, if confirmed, allows shareholders to dream of a $100 stock price. There is a larger range of lesser outcomes which initial drilling could tease into view, making a $1-$5 target range plausible within a year of a drill program's commencement. Perversely, some investors are delighted that the USFS is so slow, because now they have another 6 months to accumulate the stock. And Chris Herald is happy because with the recent financing he doesn't have to worry about trying to loadthe treasury if the permit arrives in the midst of an economic and market meltdown.

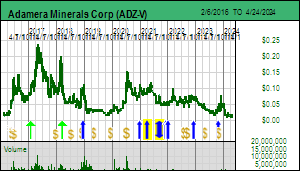

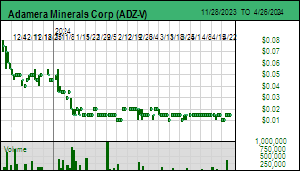

Chris Herald is also a director of Adamera Minerals Corp which owns the Buckhorn 2.0 property surrounding the now depleted Buckhorn Mine which Crown Resources Corp, at the time run by Mark Jones and Chris Herald, discovered during the 1990s. Kinross acquired Crown and developed the gold enriched skarn deposit as an underground mine. As the mine approached depletion Kinross applied for a monster plan of operations to drill targets in the vicinity, but the USFS never granted approval and Kinross eventually dropped all the surrounding claims and now only owns the original mining lease. Adamera acquired all the surrounding ground and last year cut a royalty deal with Kinross for its database which included a 2009 geophysical survey. Permitting has been a headache because the BLM, Washington State and the USFS all have jurisdiction over certain parts. Adamera has reprocessed the geophysical data and identified several dozen VTEM anomalies. Adamera drilled several of these last year on the BLM ground for which it had received permits, but the results were disappointing in that not only did they fail to intersect gold, but they didn't even intersect iron sulphides or graphite to explain the conductor. The USFS finally granted a permit in late 2022 but it expires at the end of October 2023.

Adamera's treasury was low, the stock price had sagged beneath a nickel, and despite a promising start 2023 has proved to be very difficult for resource juniors. VTEM-30 was a subtle conductor located about 1.5 km southwest of the mined out Buckhorn deposit and interpreted to be 200-300 m deep. Chris Herald, who along with Mark Jones had joined Adamera's board after CEO Mark Kolebaba generated the Buckhorn 2.0 play, pointed out that the Crown Jewel skarn deposit was a nearly flat lying body that dipped about 15 degrees, and was found because it outcropped. To build confidence about VTEM-30 Adamera conducted an audio frequency magneto-telluric survey over the conductor. AMT surveys can see conductors much deeper than VTEM surveys. Much to their delight the AMT survey revealed to strong flat laying conductors at 200-300 m depth. The company has produced a which explains why they view this as a compelling target. I've assembled several screenshots from the video and mashed them up to give a quick portrait of this target.

On October 4, 2023 Adamera announced it had scheduled drilling of the VTEM-30 target at Buckhorn 2.0 but did not state when. On October 18 Adamera announced that it is doing a private placement of 5 million units at $0.05 (with a full 3 year warrant at $0.05) to raise $250,000, plus $58,000 flow-thru at $0.05 to pay for work being done at its new Hedley gold project in British Columbia. When I discovered the USFS permit expires at the end of October, I realized management was scrambling to mobilize a rig and get at least one hole into this target before having to stop and re-apply for a permit. With 229 million issued and 291 million shares fully diluted (30 million warrants at $0.10-$0.14 plus the new 5 million at $0.05) Adamera's stock is screaming for a rollback. This drill program if successfully completed to target depth has 3 potential outcomes. One is that a Crown Jewel style skarn zone is intersected which assays in early December confirm as gold bearing, signaling a new discovery without needing a rollback. Adamera would need to reapply to the USFS for a drill permit, but this might take only a few months during which, as with Solitario's Golden Crest project in South Dakota, wouldn't matter because Adamera would not be drilling again until Q2 of 2024. The second outcome is that the VTEM-30 anomaly corroborated by the AMT survey is indeed a conductor, either graphite or iron sulphides, which provides Adamera with a new tool to upgrade its VTEM anomalies as legitimate drill targets, one of which might be gold bearing.. That outcome will likely require a rollback to put Adamera on a better footing to fund the Buckhorn 2.0 storty. The third is that no conductor of any sort is encountered, which would not be good news for anybody. If there ever was a hail mary hole, this VTEM-30 hole would qualify.

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Lithium carbonate prices, which hit $10.42/lb on Sept 26, have started to bounce off a bottom, reducing fears that the price would crash into the $5-$10 range. It does not appear that there has been a substantial boost in demand, for the reason behind the uptick seems to be that refineries whose lithium concentrate feed is purchased under long term contracts are now starting to lose money converting the concentrate into battery grade lithium carbonate not sold to battery makers at long term contract prices. So they are cutting back on production which is reversing the lithium carbonate price decline. The spot price for 6% lithium spodumene concentrate, which ranged $5,000-$6,000 per tonne in 2022 until starting to decline in March 2023, is now at $2,325 per tonne and not yet showing signs of a reversal. In fact, if it is true the refineries are cutting back on concentrate conversion, the concentrate spot price will continue to weaken. So far the hopes that China's Golden Week celebration would stimulate domestic consumption have not yet turned into reality.

Meanwhile, the rest of the world, in addition to worrying about the economic impact of persistent high interest rates chasing a 2% inflation target which encourages hunkering down in 5% plus risk free instruments, be they short term treasuries or term deposits at the bank, is now fretting about what the Israeli response to the Hamas terrorist attack will do to disrupt global supply chains and further fuel inflation. These are concerns that discourage consumption and help explain why Chinese caution is spreading globally. But they are irrelevant to the energy transition, which in the Global West is being pushed to restrain greenhouse gas fueled climate change, and, in the oil supply deficient parts of the Global East and South, is being pushed to help escape the tyranny of the world's biggest old producers: the United States, Saudi Arabia and Russia.

Dialing back from this big picture hand-wringing, the recent focus of lithium stock investors has been the optics of lithium carbonate prices bouncing off $10/lb, possibly back to $20/lb, rather than crashing into the $5-$10/lb range and spawning fears of another 2018-2020 style lithium winter when it crashed below $5/lb. My counsel is to ignore the lithium carbonate spot price. I continue to be of the view that exploration for LCT-type pegmatites should seek 1%+ Li2O deposits which can be profitably mined in the $5-$10/lb range. No new discovery will be in production before 2030, so the focus should be on finding 1% plus Li2O deposits and, if you want to be religious, praying that a Direct Lithium Extraction (DLE) technology breakthrough with unlimited scalability that drops the unit cost well below $5/lb lithium carbonate never happens. That scenario is the bugbear of Lithium Mania 2.0, which is the focus on LCT-type pegmatites to supply the bulk of the world's future lithium needs.

The first week of October, which was also Golden Week in China, was pretty grim for lithium companies in general, but Liontown Resources Corp was an exception. This week we found out why. After Albemarle presented Liontown with a revised AUD $3.00 per share offer on September 4 conditional only on due diligence, Hancock Prospecting, a private company owned by Gina Rinehart that specializes in iron ore mining but is diversified into a lot of other areas, filed a notice of becoming a substantial Liontown shareholder on September 11, following a purchase of 59,281,147 shares on September 7 at an average $2.98 price. On September 11 Hancock owned 169,914,764 shares or 7.72%. While other lithium companies retreated since then, Liontown has held up well because Hancock has continued to buy in the open market.

On October 11 Hancock reported that it had reached 19.9% with 438,248,862 shares. A day later on October 12 Liontown announced that it had granted a 7 day due diligence extension to Albemarle which presumably now has until the middle of next week to make a decision. So you might ask, why, with lithium carbonate prices finally bouncing off a bottom, and Gina Rinehart owning 19.9% of Liontown at close to a $3 average price, has Liontown's share price sagged to $2.79 in the past couple days? One explanation could be market concern that next week we will find out that Albemarle has decided to walk away from acquiring Kathleen Valley, which would be definitive because the recent proposal indicated the $3 offer would be the final offer, which means Albermarle cannot manipulate the Liontown stock price by playing games. Such an outcome would make Australia's richest woman look like a doofus.

Since it is hard to imagine that the woman who expanded her father's iron mining business into a colossus is a doofus, there is an alternative explanation with interesting implications. Under Australian rules if a third party acquires 20% or more of a company it is required to make an offer for 100% of the company (according to a recent FT LEX comment). The market expectation is that Hancock will not exceed 19.9% but will instead vote against the plan of arrangement if Albermarle decides to go ahead with acquiring Liontown at AUD $3 per share. For the acquisition to become reality it must receive 75% of votes cast, and, while Hancock doesn't have the 25.1% stake needed to prevent approval, the reality is that most shareholders don't bother voting their shares, so if just under 80% of Liontown's 2.2 billion shares are voted in favor of the deal, Hancock can still kill the deal with its 19.9% stake. Albemarle's extension request is ostensibly about needing just a little bit more time, but in reality it is so that it can work out a deal with Hancock to secure a yes vote, and since the stake was bought close to the offer price, such a deal would require a better offer.

The two main potential outcomes are that Albermarle increases its offer to a level that secures the vote of Hancock, or Albemarle has to walk away. That would pave the way for Hancock to make its own bid for Liontown, not necessarily at a higher price, but one that is unconditional and perhaps done in conjunction with a partner. The slightly sagging price of Liontown reflects market uncertainty about how this will play out. The most important question right now is, "What is Gina's plan?" The big picture implication, however, is that deep-pocketed players are valuing Kathleen Valley at minimum USD $4 billion, despite the recent lithium carbonate price declines.

Price Charts for Lithium Carbonate, Hydroxide and Concentrate

Pie Chart for Sources of 2022 Oil Supply

Liontown Purchase History by Gina Rinehart's Hancock Prospecting Group

Jim (0:10:35): What are the implications of the various Liontown outcomes for the James Bay Lithium Area Play?

Albemarle has a 49% stake in Greenbushes with Tianqi holding the other 51%, and it has a 60:40 JV with Mineral Resources Ltd in Wodgina, both producing mines, so Albemarle already has meaningful pegmatite sourced lithium supply in Australia. Not to be taken lightly, Albemarle is an American company, not like Rio Tinto which is sort of Australian but has no meaningful pegmatite based lithium stake. A big question is whether Hancock is merely trying to squeeze Albemarle into offering a higher price so that the binge buying during the past month turns into a nice short-term profit (Gina messing with the big boys), or if Hancock it is in fact trying to muscle Albemarle aside and turn itself into a major lithium supplier by acquiring Liontown and its Kathleen Valley project which will be in production in mid 2024?

The preferable outcome for Lithium Mania 2.0 is that Hancock expands from iron mining to include mining pegmatite deposits for lithium. I believe the IEA projection of a 600% lithium supply expansion needed by 2030 to fulfill the EV deployment part of the 2050 net zero emissions goal will happen regardless what people thing about the efficacy of global warming mitigation measures. I also believe that Toyota's solid state lithium ion battery breakthrough is commercial not just for the high end models it plans to sell by 2027, but ultimately also cheap enough for its affordable and popular Camry and Corolla models. If a solid state lithium ion battery becomes reality, it will be because of manufacturing efficiencies, not a decline in the price of the critical mineral inputs. In that case we may need 12 times as much lithium supply by 2035 compared to the 130,000 tonnes of lithium metal equivalent produced in 2022.

Unless there is a miracle breakthrough in direct lithium extraction that opens up an unlimited supply with a cost well below $5/lb lithium carbonate, that future lithium supply market will be worth $100-$200 billion, the same league of aluminum, gold and copper, though not as big as iron whose output was worth $312 billion in 2022. Barring the DLE miracle, the bulk of future lithium supply will come from pegmatite deposits. Rio Tinto has already recognized the future importance of lithium, but other major western mining companies have not. If Hancock were to acquire Kathleen Valley it would be just the start of the miner expanding into lithium production while biggies like BHP and Anglo American pick rust out of their noses, one more major with lithium supply growth ambitions. The more majors looking for a serious chunk of a future $200 billion annual lithium market, the better for the juniors looking for LCT-type pegmatites in the James Bay region.

If Hancock's strategy is merely to grind some chump change out of Albemarle, then the only implication for the James Bay region is that Liontown shareholders will end up with over AUD $6 billion cash to redeploy elsewhere, and the best emerging destination is the James Bay region of Quebec where Albemarle already has a 4.9% equity stake in Patriot Battery Metals Corp, owner of the world class CV5 deposit. Regardless how the Liontown story plays out, it should send a new flood of money and interest into the James Bay region to which ASX-listed companies are already flocking.

The James Bay region suffered a serious setback this year thanks to the forest fire closures which prevented access to most of the region during June through August, a key prospecting season for boots on the ground. Some areas such as the Mia and Radis projects of Q2 Metals Corp and Ophir Gold Corp had even less time because they were off limits during the moose hunting season that runs September 15 to October 15. Those companies got in only a couple weeks in the field before having to leave. Logistics, however, was a problem even for those juniors with properties in areas that opened early andf were not impacted by moose hunting season. As a result very few companies will be in a position to drill meaningful targets in Q4, and even Q1 will not see anywhere near the number of drill programs that a full 2023 summer prospecting season would have made possible. For those of us who embraced Lithium Mania 2.0 last year, this is an annoying delay, but for those on the sidelines, perhaps wondering if they missed the boats, the sight of boats returning to the dock is a joy to behold. I was not wrong, just early and only because I was blindsided by the forest fire closure, which only the dumbest bag of hammers refuses to link to climate change.

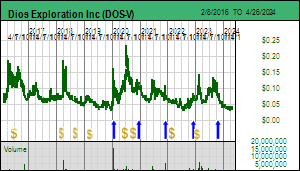

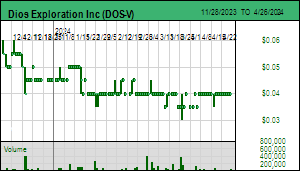

Take the example of Dios Exploration Inc which this week provided an update about its Lecaron project which left the market cold. The junior's third party contractor was able to visit four of the five property groups, but spent only 14-21 days in the field. At Lecaron this resulted in a 50% expansion of the claim package after the geologist led team observed prospective geology not indicated by the government maps. But there were no reports of spodumene observed in outcrop at Lecaron. Samples were collected and sent for assaying, but there was no mention about using a LIBS or XRF to determine the LCT-type nature of outcrops. Dios won't have the assays until November though by then it will be too late to go back into the field, especially if this year's prediction of an early winter proves correct. The press release didn't mention the number of samples, but management told me that about 200 outcrop samples have been shipped for assaying, which is an impressive number, though management did not know how many outcrops these came from. Management also told me that much of the area prospected turned out to have heavy bush cover and there simply wasn't enough time to assess the scale and continuity of pegmatite outcrops, which of course you don't want to waste time on before you know it is an LCT-type pegmatite. The bush cover problem is not a surprise, because the Dios properties are what I call "second order", meaning that they are being generated by a combination of datasets, including a proprietary database from the diamond indicator mineral till sampling days of Dios in the 2000's which the company has used to vector into prospective areas. These are not geologically obvious areas which have seen intense exploration for precious or base metal deposits, and while pegmatite showings have been documented, they are not highly visible in satellite imagery. To assess these second order prospects requires a full summer prospecting season, which Dios was not able to undertake. After enduring the lost summer of 2023, the market has no patience for so-so descriptions about boots on the ground efforts.

The glum reaction among KRO members who are Dios shareholders was "oh, dead money until the summer of 2024". That isn't a fair reaction, because once Dios has assembled and published everything it has learned about its 5 claim groups, there will probably be a positive market reaction, especially if drilling activity by some juniors has confirmed significant new discoveries. My James Bay Lithium Index membership is now up to 69 companies, with new additions mainly by ASX listings which acquired claims or options during the past 5 months. The Australian resource junior interest in James Bay keeps growing; Dios CEO Marie-Josie Girard tells she is getting plenty of inquiries from ASX listings seeking to option a property. But until she has a better understanding of the potential based on the short sampling season in September, she is not considering farmouts at this stage.

Without question, however, the market's attention is shifting towards drill intersection based confirmation of grade and scale of an LCT-type pegmatite outcrop. Who is on track to deliver the next PMET CV5 discovery over the next year? All eyes are now on Brunswick Exploration Inc which is busy drilling within its 850 m by 2,700 m corridor of spodumene bearing outcrop at Mirage with preparations already underway for a winterized camp that will allow drilling to resume in January 2024.

With regard to drilling expectations, consider the plight of Ophir Gold Corp whose Radis project I discussed in KW Episode September 1, 2023. Ophir and its neighbor Q2 Metals Corp got in only a few weeks of prospecting before they had to quit for First Nation moose hunting season. The Mia project of Q2 Metals is more advanced, so the targets were already sufficiently developed to allow a meaningful drill program. Q2's stock price has held up because on October 16, the day after the end of moose hunting season, it will mobilize a drill rig to the property. Ophir, which last week published an Update about its brief sampling efforts at Radis which continued to support the potential for meaningful LCT-type pegmatites, and certainly read more promising than the sparse Dios news release about Lecaron, saw its stock get hammered from the $0.30 plus level below $0.20 when the market realized that there would be no drill program in 2023. However, CEO Shawn Westcott tells me that their target is sufficiently developed to justify a drill program in late January 2024 which will stage out of the winterized camp Q2 Metals is preparing at Mia. And Ophir has a $5 million treasury so that it doesn't have to go begging to the brokerage sector later this year when it is recommending dumping all its former picks for tax loss purposes.

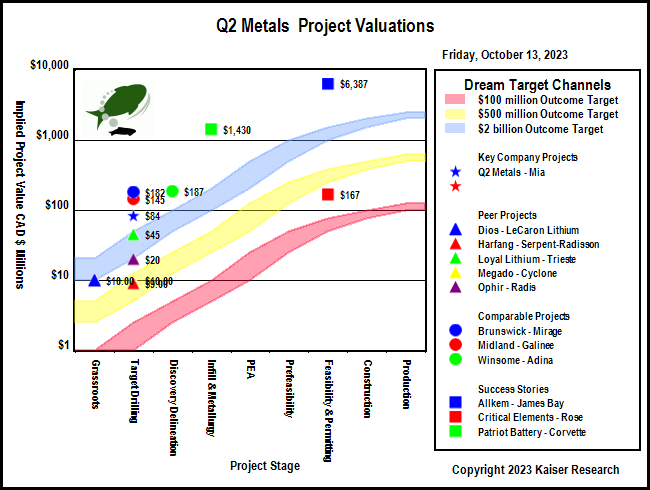

The challenge at Q@ Metals' Mia is the same challenge Brunswick has at Mirage. What is the sub-surface orientation of the outcrops, is it an en echelon series of parallel dykes like at Allkem's Galaxy-Cyr project, or elongated bodies like with PMET's CV5 pegmatite? And what is the dip so that one can convert the outcrop's surface width into true width and start estimating tonnages? Ophir will benefit from whatever Q2 learns drilling at Mia in October-November, and if Q2 delivers confirmation of a discovery, the market will no doubt turn its attention to Ophir Gold because right now the market is assigning an $84 million value to Mia but only a $20 million value to Radis. The Q4 bottom-fishing season for James Bay Lithium Index juniors could be very lucrative this year, especially given the capitulation mood in the market.

With the recent filing of financial statements for the period ending June 30 it is time to start researching my 2024 Bottom-Fish Collection. The slump in financing this year has made my job easier, so long as I insist on working capital being $500,000 or more when I look at three criteria - money, people and story. (I used to focus on structure, namely how much of the stock was controlled by management and its allies, but these days a thumbs up on this count usually implies vulnerability to a pump and dump operation - much more interesting is a meaningful management stake in a sea of liquidity.)

A tougher question than bottom-fishing strategy is what to do about the 2024 Favorites Collection which are supposed to be graduates from the Bottom-Fish Collection. The 16 juniors in my 2023 Favorites collection are down 17.2% this year, with only 3 showing gains, of which the winner is Brunswick Exploration Inc, among a handful that don't deserve to be demoted to the 2024 Bottom-Fish Collection. The missing piece for many of 2023 Favorites is a positive outlook for their target metal and a return of investor interest in the resource sector. But with 5% risk free interest rates being threatened by central banks well into 2026 in pursuit of their 2% inflation targets, the more likelier outcome is a major economic downturn that does not boost metal prices, and leaves most juniors gasping for air.

I recently used the KRO Search Engine to do a quick survey of resource juniors with at least $500,000 working capital among which I spotted about a hundred bottom-fish candidates, many of which have yet to form a bottoming chart pattern. What was truly awful, however, was the large number of prominent companies that normally do not qualify as bottom-fish because they are well promoted and financed by Bay Street, but which now have ski slope charts turning into cliffs. This is a sign of collective capitulation, and, with tax loss selling usually not kicking in until December, Q4 of 2023 looks awful. But not if you are today doing your homework and preparing a bottom-fish watch list to load up in December's tax loss selling season (don't worry about the tax losses being taken earlier, the optics and threat of the resource junior ecosystem approaching an extinction threshold will generate capitulation selling by shareholders who aren't underwater, just fearing the opportunity cost posed by dead money and risk free 5% plus interest bearing deposits. But while I am rubbing my bottom-fishing hands, coming up with the 2024 Favorites Collection is going to be a challenge unless it becomes a collection of my favorite bottom-fish.

A major focus of Kaiser Watch in 2024 will be the James Bay Lithium Index because its macro story is intact and does not require a higher metal price to boost the value of resource juniors. The individual company story will be grassroots discovery exploration, the simplest kind that takes me back to the 1980s when making money on resource juniors required a grassroots discovery and a wave of "me too" juniors. As part of my bottom-fish research I will pay particular attention to the JBLI members, of whom I recently confirmed Midland Exploration Ltd and Ophir Gold Corp as part of my 2024 Bottom-Fish Collection. To encourage new subscribers to sign up for a USD $450 annual individual KRO membership I am extending the term of all new signups to the end of 2024. You may not be in hurry to buy anything yet, but you ought to be building your watch list now for later this year.

Bar Chart displaying value of 2022 Metal and Fossil Fuel Production

Graphics from Ophir's recent Radis Update

Graphic from Q2's recent Mia Update

Graphic from Dios' recent Lecaron Update

IPV Chart for Q2 Metals showing relative valuations of James Bay projects

Snapshot of 2023 KRO Favorites

Disclosure: JK owns shares of Brunswick and Dios; Brunswick is a Fair Spec Value rated Favorite; Q2 Metals is Fair Spec Value rated; Dios and Ophir Gold are Bottom-Fish Spec Value rated

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch October 6, 2023: Chief slaps Prime Minister with NoCanDo

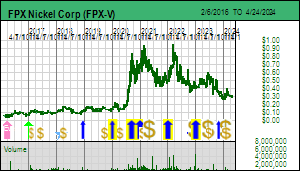

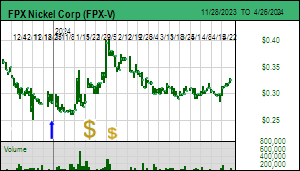

Jim (0:00:00): Why, despite recent news that Toyota and Panasonic want to work with FPX Nickel on developing a nickel sulphate refinery, did the stock price drop this week?

FPX Nickel Corp's stock price dropped on Wednesday October 4, 2023 after Chief Leslie Aslin published an October 4 Letter on behalf of the 1,565 member Tl'azt'en Nation repeating an August declaration that this First Nation had unilaterally cancelled a 10 year memorandum of understanding with FPX Nickel and would absolutely oppose any mine on Mount Sydney Williams which he had recently discovered was sacred despite his First Nation community collecting millions of dollars from clear-cut logging the region. I discussed this development in KW Episode August 11, 2023 and pointed out that there is a lot more going on behind the scenes than FPX Nickel can talk about because of confidentiality restrictions. But the latest iteration did knock the stock back below $0.40, and cynics might be forgiven for speculating about unregistered foreign agents acting behind the scenes to harm the Canadian mining sector, especially ones who are concerned about all this talk about cheap EV's with very dirty critical mineral inputs heading for North American and European markets.

Last week in KW Episode September 29, 2023 I talked about the cooperation deal Japanese officials signed in Ottawa with federal officials and pointed out that it made no sense for Japanese companies to invest in manufacturing capacity in Canada unless Canada can supply critical minerals that qualify as clean. If companies like Toyota and Panasonic cannot get clean nickel or lithium from Canadian mines, they might as well build their factories in the United States where the resulting quality jobs will be welcomed, even in states whose Republican leaders decry global warming as a scam and promise to pull the plug on all energy transition policies once in charge of America's destiny (Why Trump and the Rest of the G.O.P. Wont Stop Bashing Electric Vehicles).

On that same day JOGMEC and a JV between Toyota and Panasonic signed a non-binding agreement with FPX Nickel to collaborate on the development of a nickel sulphate refinery that would process ferro-nickel concentrate from the Decar mine that would otherwise go to the stainless steel market. The PFS indicated extra cost of this refinery coupled with the likely market value of the nickel sulphate output does not make economic sense for the operator of the future Decar Mine, but it does for a company like Toyota which wants to sell EVs in the United States it can claim are made from responsibly mined critical minerals (see KW Episode September 8, 2023). This news briefly boosted FPX Nickel's stock price back above $0.50 because the market assumed that Prime Minister Justin Trudeau would make policy decisions that are good for Canada as a whole rather than just for a 5% race based minority that aspires to aristocratic privileges not available to ordinary Canadians by playing a reconciliation guilt card for which the vast majority of Canadians bear no responsibility.

On Monday government employees got to enjoy a holiday funded by the taxes of the 95% of Canadians who do not have indigenous DNA which the Prime Minister calls Truth and Reconciliation Day. Chief Aslin's repeat of his earlier letter is not really aimed at FPX Nickel, because there is nothing new in it. What it really represents is a slap in the face of Justin Trudeau to remind him that all federal government decisions involving Canada's mineral resources must be subordinated to the will of Canada's First Nations who have traditional territory claims over a land mass several times the area of Canada thanks to overlapping and competing territory claims by different First Nation groups.

Trudeau, of course, will not have noticed because he lives in a bubble world fretting about stuff that is irrelevant to Canada becoming a key player in the energy transition and buttressing with real economic growth the values that distinguish Canadians from the increasingly lunatic Trump base in the United States. But FPX Nickel shareholders did notice, and, realizing that Trudeau may be just stringing the Japanese along with false promises, which they will soon enough figure out as they observe a complete absence of any pushback from federal and provincial governments face-slapped by Chief Aslin, dumped the stock back below $0.40.